Cocoa Market Call Summary: Market Overview and Outlook for the New Cycle

- Cocoa futures fell more than 10% in the week ending October 3, after reaching their lowest level in a year, influenced by supply pressure and technical factors.

- The macroeconomic environment continues to influence the market. The Federal Reserve cut rates in September in response to inflation and a weaker labor market, while the ECB kept rates unchanged in a relatively more stable environment.

- US net cocoa imports rose nearly 70% year on year until July, returning close to historical averages. Ecuador now accounts for 30% of bean imports, compared with 13% on the five-year average, while the share of Ivory Coast and Ghana declined.

- In the European Union, net imports are down nearly 5% compared with 2024, reflecting higher procurement costs.

- Projections for the 2025/26 season point to a potential surplus of up to 360 thousand tons, conditional on balanced rainfall in West Africa.

Cocoa Market Call Summary: Market Overview and Outlook for the New Cycle

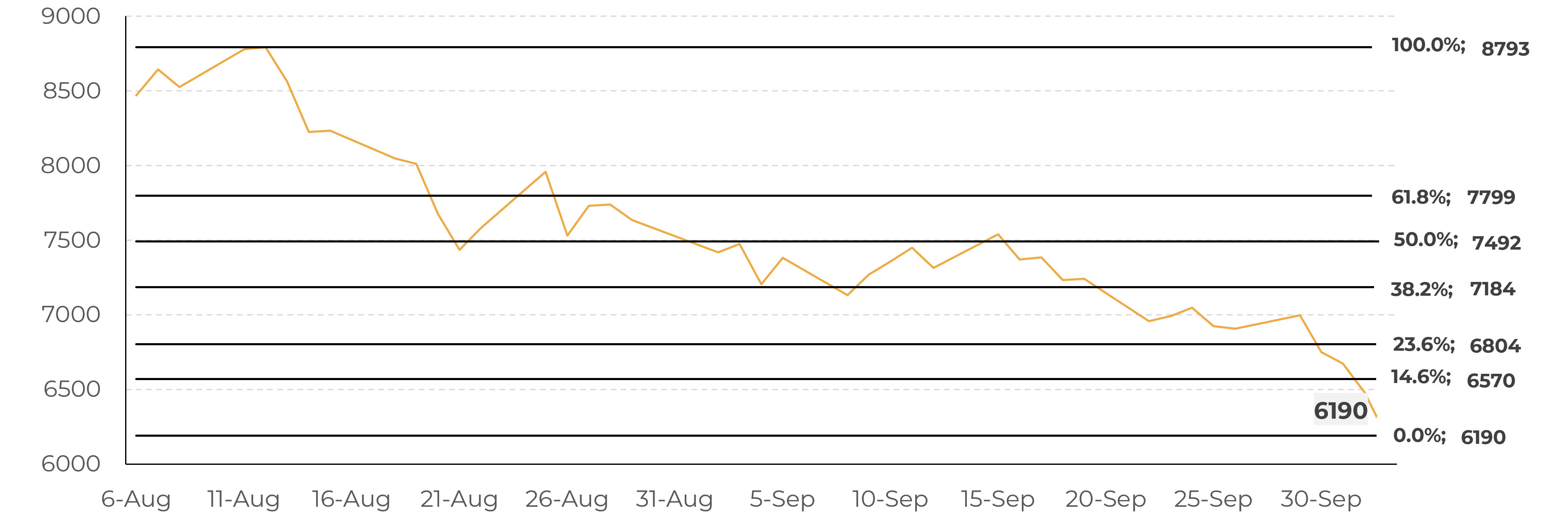

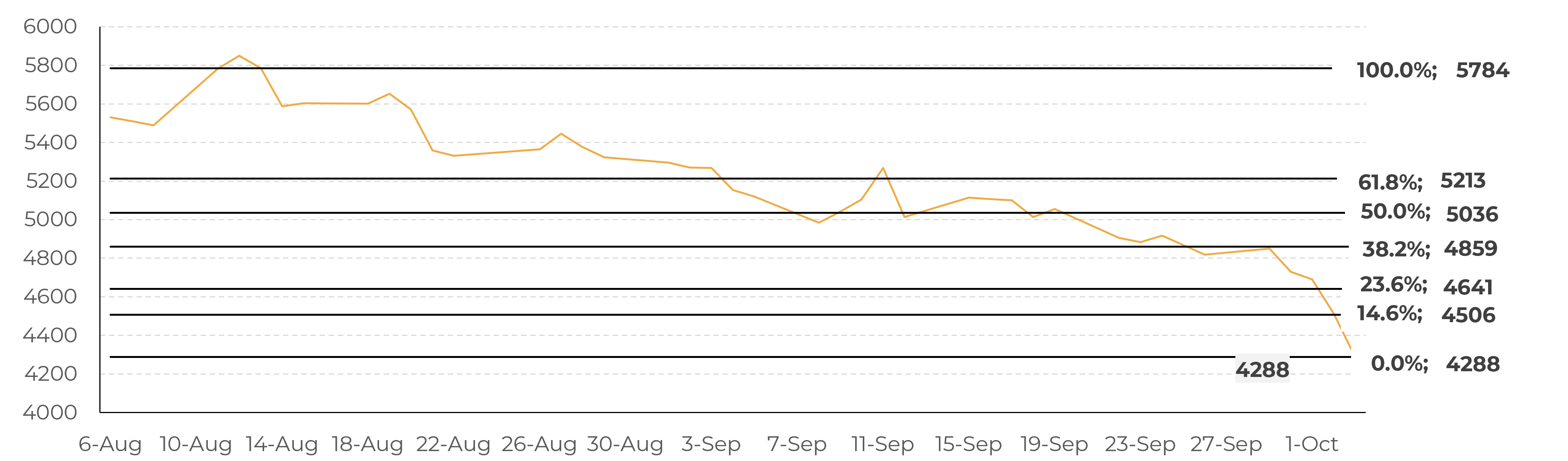

After reaching their lowest level in a year, front-month contracts closed the week of October 3 at 6,190 USD/t in New York and 4,288 GBP/t in London, with weekly reductions exceeding 10%. Against this backdrop, Hedgepoint Global Markets launched discussions on one of the most challenging markets of recent years during its first Cocoa Market Call on September 30, bringing an outlook on the main factors currently driving prices.

NY Cocoa first contract (USD/t)

Source: LSEG

LND Cocoa first contract (GBP/t)

Source: LSEG

Macroeconomic Context

In the United States, the economy has been reflecting the potential impact of tariffs imposed on key trading partners. The move has kept inflation under pressure and, combined with a slowdown in the labor market, led the Federal Reserve to deliver its first rate cut in September, with the possibility of further adjustments later this year. This monetary policy shift affects domestic activity and demand, and through the dollar, the performance of other currencies, directly influencing commodity markets. In Europe, the ECB kept rates unchanged in a relatively more stable environment, although risks linked to US tariffs, fiscal pressures in Germany, and political uncertainty in France remain on the radar.

Fund positioning in cocoa remains cautious, in line with the more uncertain macroeconomic environment. Until now, prices have been reacting mainly to technical factors, reflecting market adjustments. In recent days, however, the increase in farmgate prices in Ghana and Ivory Coast encouraged stronger deliveries, adding supply pressure and contributing to this week’s correction.

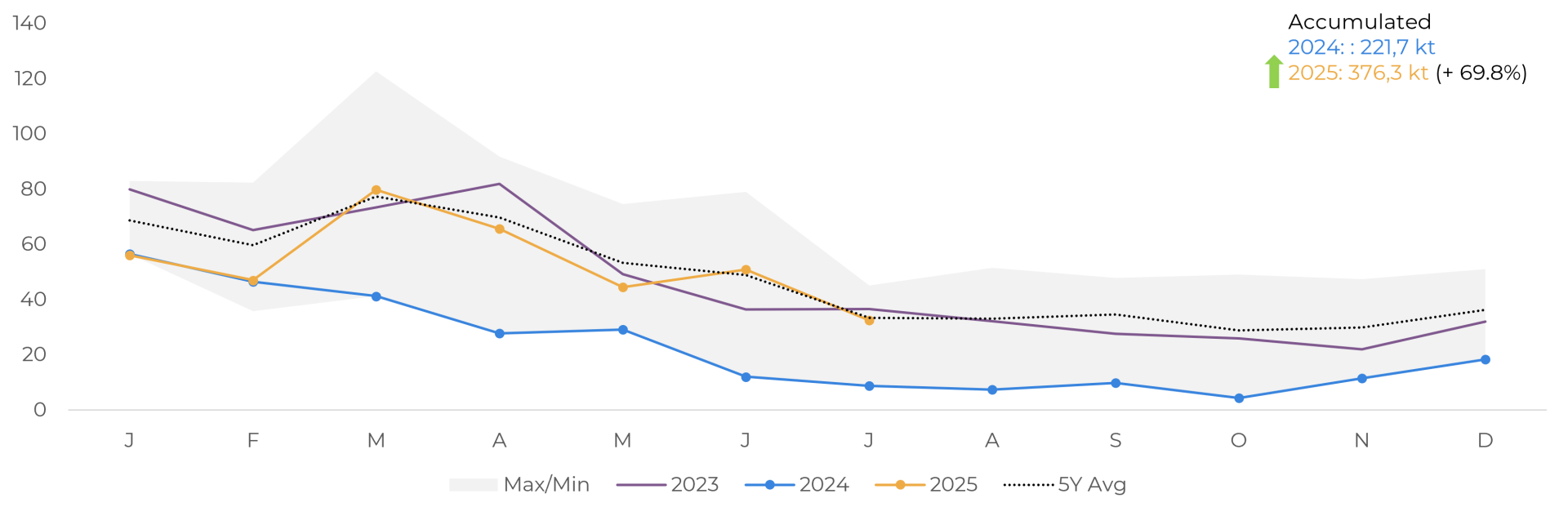

US Imports

Despite elevated prices, US net cocoa imports rose nearly 70% compared with last year, returning to levels closer to the historical average. The result points to resilient demand and suggests support for grindings in the region, which showed the smallest contraction among the main processors in Q2.

US: Total net cocoa imports ('000 tons)

Source: United States International Trade Commission (USITC)

From January to July, the composition of these imports shows significant changes. Ecuador accounted for around 30% of total beans received, compared with a five-year average of only 13%. This increase came alongside a lower share from Ivory Coast and Ghana and is also visible in ICE US certified stocks, which now reflect a more diversified origin profile, including Colombia, Papua New Guinea, Peru, and Venezuela.

This trend, initially explained by reduced supply from key origins, could be reinforced by trade policy decisions. Cocoa was included in the list of potential tariff exemptions in the United States, but implementation will depend on negotiations with partners, cases such as Ecuador, Malaysia, and Indonesia. As a result, tariffs could intensify changes in trade flows and competitiveness for cocoa products from countries like Brazil and India.

In addition to trade policy effects, prices have also influenced flows. Between January and July, cocoa butter’s share of US imports rose from 15% in 2024 to 20% in 2025, while powder declined from 17% to 15%, likely reflecting the higher relative price of powder.

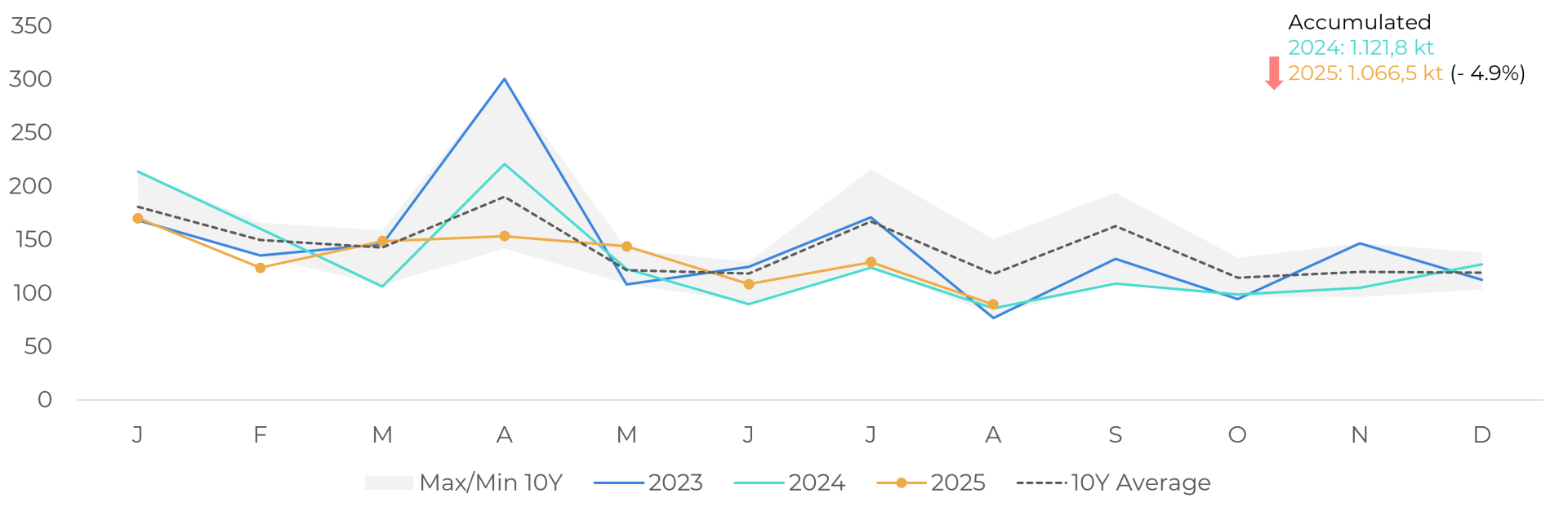

EU Imports

In the European Union, the picture is different. The accumulated net volume is still almost 5% below the previous year, although the difference has narrowed since the beginning of 2025. The preference for higher quality African almonds keeps costs high, as Ivory Coast and Ghana have higher differentials compared to other origins.

EU: Total net cocoa imports ('000 tons)

Souce: European Commission

Assessing demand, second-quarter grinding figures confirmed a decline in all regions, with greater resilience in the United States, sustained by stronger imports. Europe, in turn, experienced a more pronounced decline, reflecting lower imports in an environment of higher costs. The market now turns its attention to the next releases, scheduled for mid-October, which will be key to calibrating demand expectations at the start of the new cycle.

Supply and Weather

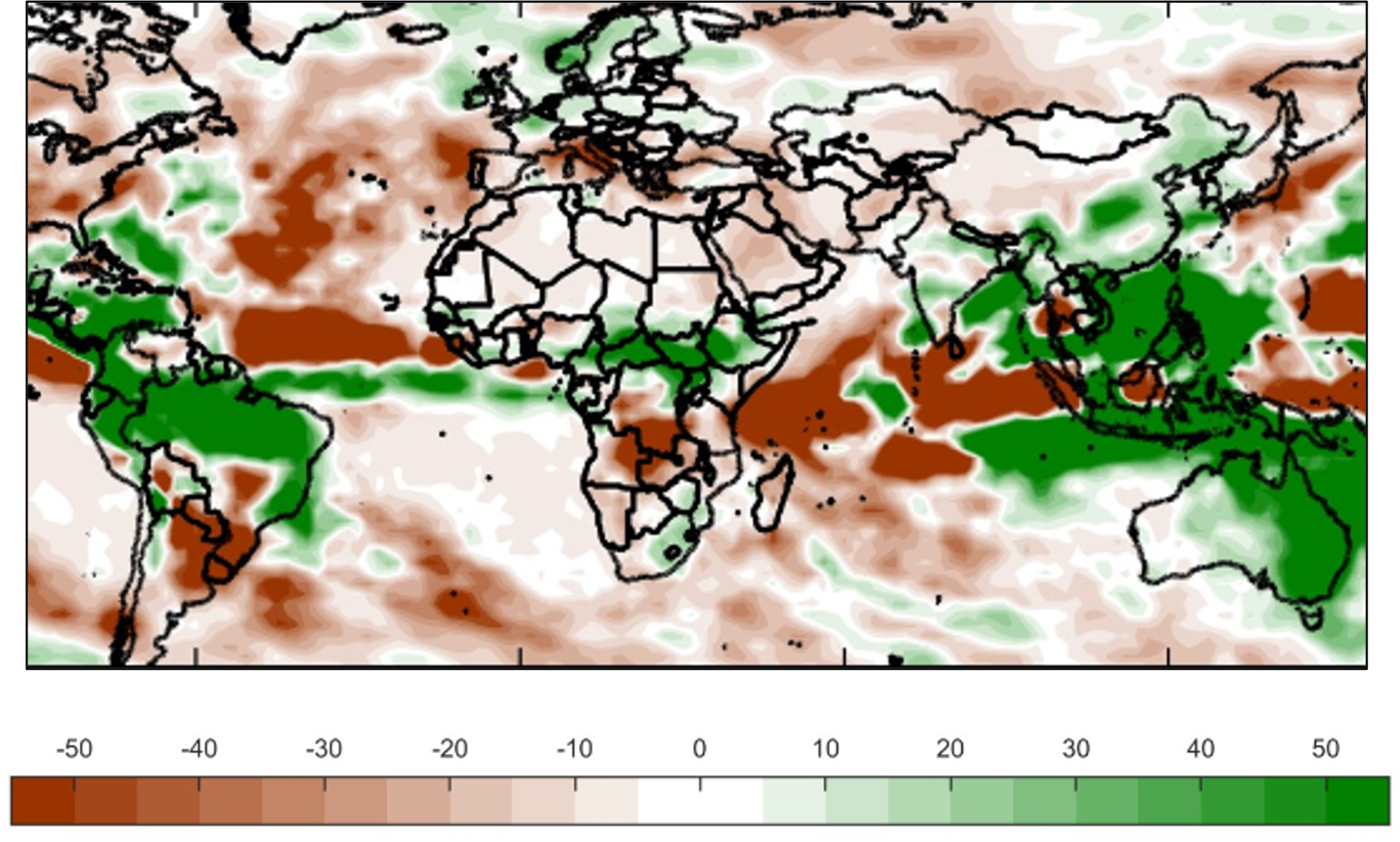

Initial forecasts for the 2025/26 crop indicate a possible surplus, but the volume of this surplus will depend on a balanced water regime in the coming months. The NOAA/CPC has raised the probability of La Niña occurring between October and December to 71%, a phenomenon that tends to bring more moisture and mild temperatures to West Africa, reducing the risk of water stress during the dry season. One point of concern, however, is the impact of La Niña on the harmattan winds, dry, dust-laden currents that can compromise fruit development. In Ecuador, La Niña may reduce rainfall at the beginning of the rainy season, increasing the need to pay attention to soil moisture.

La Niña September-November Precipitation Anomalies (mm)

Source: LSEG

Although the 2024/25 season is once again heading for below-average cumulative rainfall, as in the previous cycle, the occurrence of rainfall at critical periods has favored a higher fruit survival rate. This factor, combined with the recent increase in prices paid to producers in Ghana and Ivory Coast, reinforces expectations of greater grain availability at the beginning of the 2025/26 crop. Still, the weather remains a determining factor: unfavorable conditions in the coming months could reduce delivery potential in West Africa both at the end of the main crop and at the beginning of the mid-crop (April 2026). On the immediate supply side, ICE certified stocks, although recovering from the lows seen at the beginning of the year, remain well below the historical average.

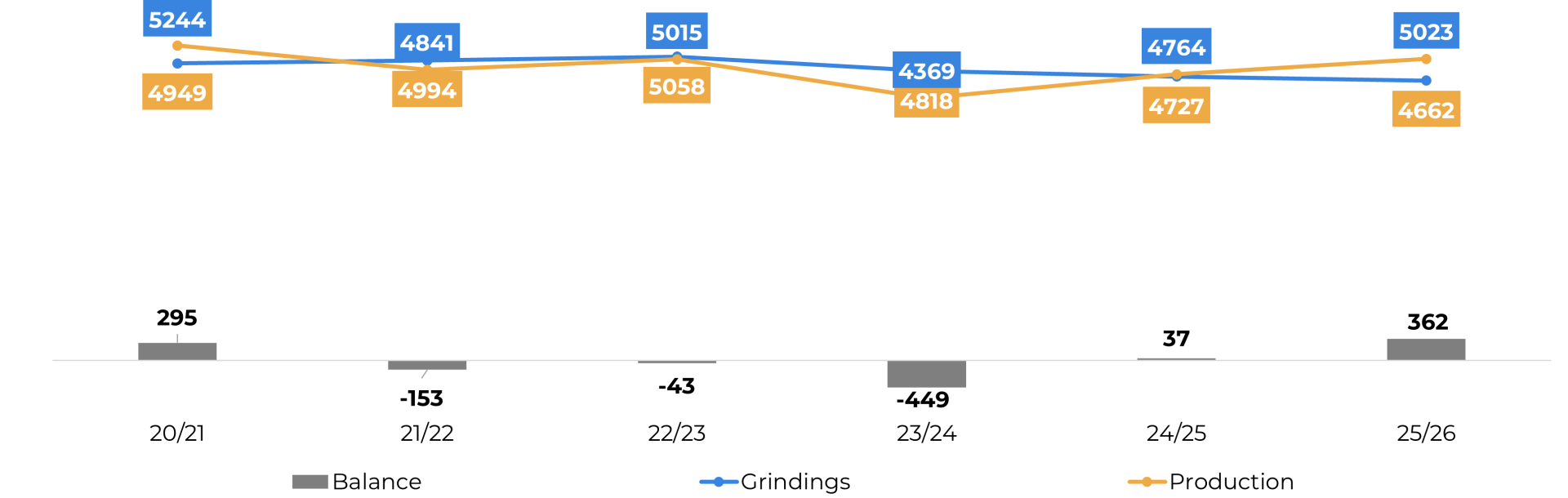

Spreads in London and New York turned negative for the first time in 2025, mainly reflecting expectations of a surplus in the 2025/26 crop. For the 2024/25 cycle, we project a surplus of around 37,000 tons, while for 2025/26 this figure may approach 360,000 tons, supported by better prospects in West Africa and production expansion in origins such as Ecuador. Even so, the global balance between current supply and demand remains tight, which keeps market volatility high and reinforces sensitivity to new weather, trade, and grinding data that can quickly change market sentiment

Global Supply and Demand for Cocoa (‘000 tons)

Source: ICCO, Hedgepoint

In Summary

The cocoa market ended the week with contracts accumulating declines of more than 10% after reaching their lowest level in a year. In the United States, the interest rate cut in September reflects inflationary pressure and the slowdown in the labor market, while in Europe, the ECB kept rates unchanged in an environment of relative stability. In this scenario, funds remain cautious, although recent movements have reflected not only technical factors but also the updating of prices paid to producers in Ghana and Ivory Coast, which stimulated a faster pace of deliveries and put pressure on prices.

Despite the high price environment, total net cocoa imports by the United States increased by almost 70% until July compared to the previous year, with Ecuador standing out, now accounting for 30% of almonds received. Europe, in turn, saw a decline in net imports, influenced by higher acquisition costs.

The technical outlook for the 2025/26 season indicates a possible surplus of around 360,000 tons, but the volume will depend on a balanced water regime in West Africa in the coming months. Even so, the current global balance remains tight, keeping the market sensitive to new data on weather, trade policy, and grinding.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

thais.italiani@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.