Global demand for cocoa remains under pressure at the end of 2025

- Cocoa prices fell for another week after the release of grind data for the fourth quarter of 2025.

- In Europe, the sharp decline in grinding in Q4 reinforced the reading of weakened demand in an environment still marked by high prices.

- North America showed greater resilience, supported by steady imports and Ecuador's increased share of US purchases.

- In Asia, the decline in grinding was below market estimates, with a highlight being Malaysia, one of the main processing regions in the area.

- Despite the still bearish bias, technical indicators suggest the likelihood of occasional corrections and greater volatility.

Global demand for cocoa remains under pressure at the end of 2025

Cocoa contracts closed on Friday, January 16, at USD 5,076/t in New York and GBP 3,712/t in London, accumulating another week of declines after hitting their lowest levels in two years. Following the technical adjustments observed in the previous analysis, the recent movement is set against the backdrop of the release of fourth-quarter 2025 grinding results in the main processing regions, which reinforced the perception of weakening demand.

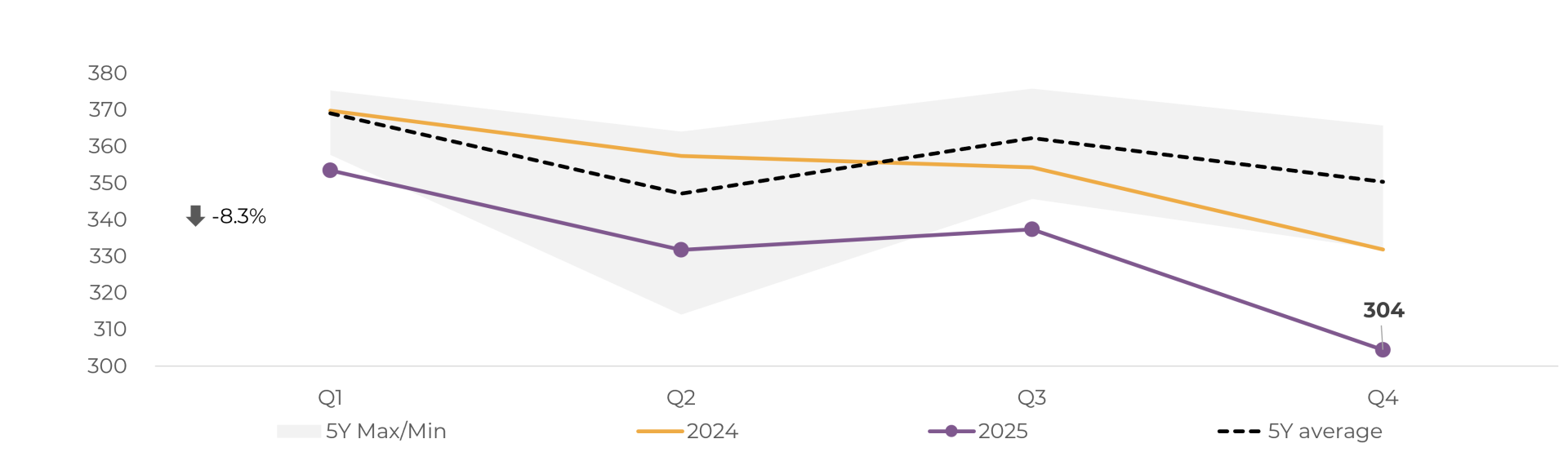

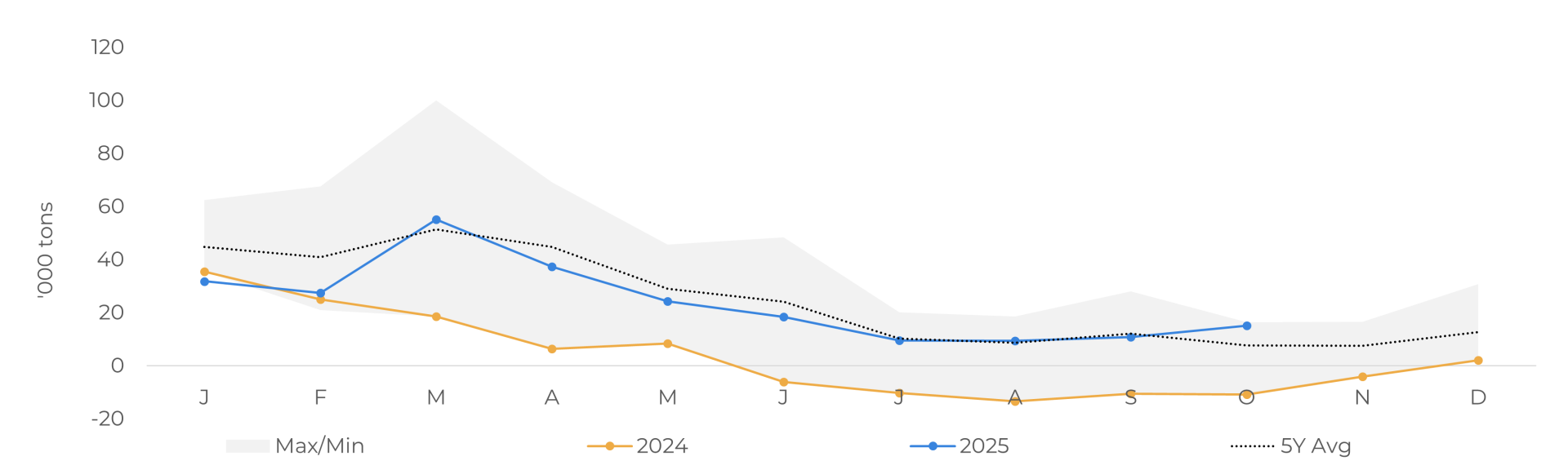

In Europe, the world's largest cocoa processing hub, data from the European Cocoa Association (ECA) showed an 8.3% drop in fourth-quarter grinding compared to the same period last year, ending 2025 with a cumulative decline of 6.1%. With both results above market estimates and reinforcing the reading of still weak demand, cocoa prices reached lows of USD 4,839 in New York and GBP 3,572/t during the January 15 session.

Cocoa grinding: Europe (‘000 tons)

Source: European Cocoa Association

The scenario aligns with our estimates. When tracking regional trade flows, net cocoa bean imports declined by 5.6% in 2025. Looking specifically at the fourth quarter, the decline was 8.9% compared to the same period last year, after a 6.4% increase in the previous quarter.

EU: net cocoa beans imports ('000 tons)

Souce: European Commission

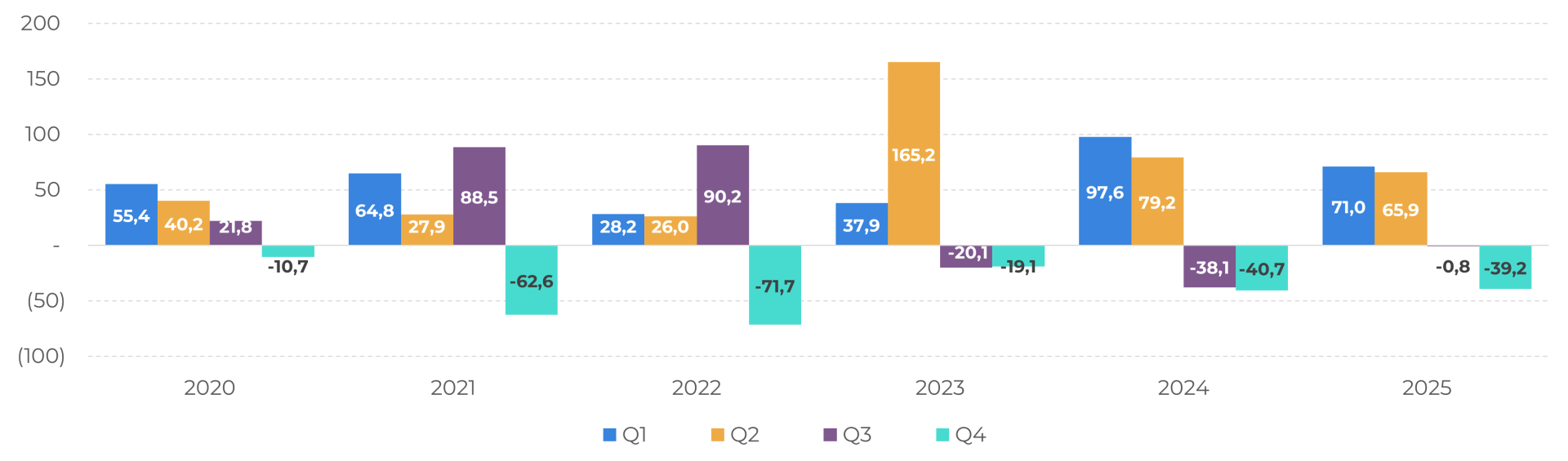

Although these movements cannot be interpreted as a direct impact on grinding, given the relevant role of stocks in this analysis, they reinforce an environment marked by high prices and supply constraints throughout the year. This scenario becomes even more evident when observing stock flows throughout the second half of the year.

EU: quarterly stock flows (‘000 tons)

Souce: European Commission, Hedgepoint

Historically, the third quarter showed a positive restocking flow, a pattern that breaks down starting in 2023, when Q3 begins to record net inventory outflows. In 2025, although the third quarter flow remained negative, the higher inflow of imports during the period helped to reduce the intensity of this outflow, partially easing the pressure on stocks, although without restoring the historical pattern. In this context, high price levels continue to limit the capacity for inventory replenishment and keep grinding more sensitive to the availability of raw materials, prolonging an environment of caution on the demand side.

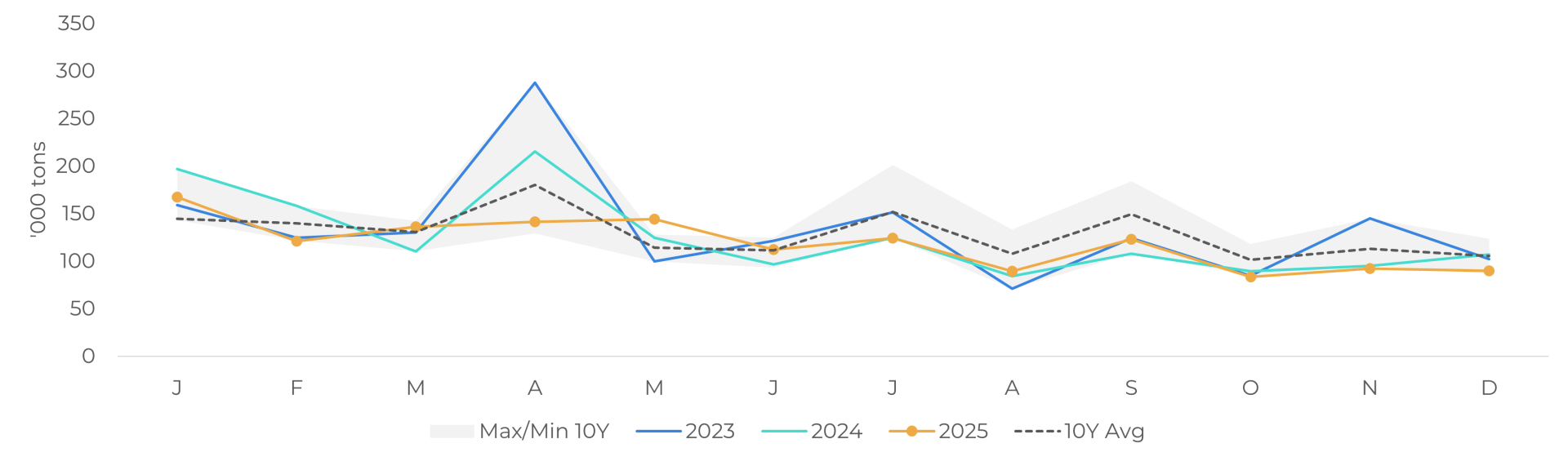

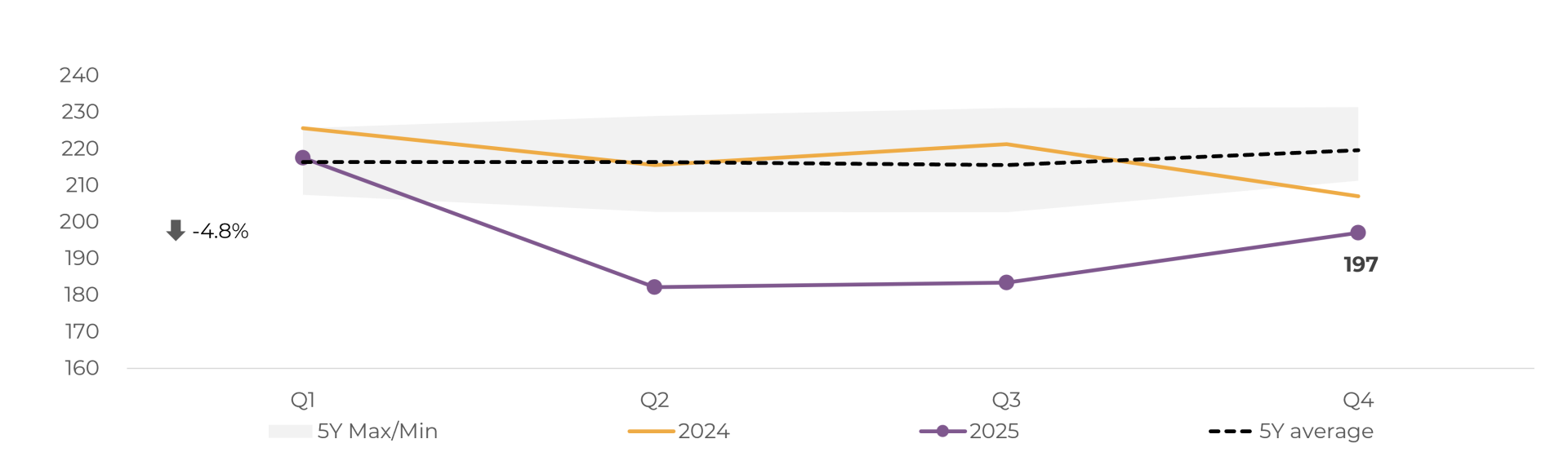

In contrast to this scenario, data from the National Confectioners Association (NCA) indicate that grinding in North America advanced 0.35% compared to the same period in 2024. In the United States, net cocoa imports remained steady throughout the year, totaling 238.7 kt through October, compared to only 42.5 kt in the same period in 2024.

Cocoa grinding: North America (‘000 tons)

Source: : National Confectioners Association

US: net cocoa beans imports (‘000 tons)

Source: United States International Trade Commission (USITC)

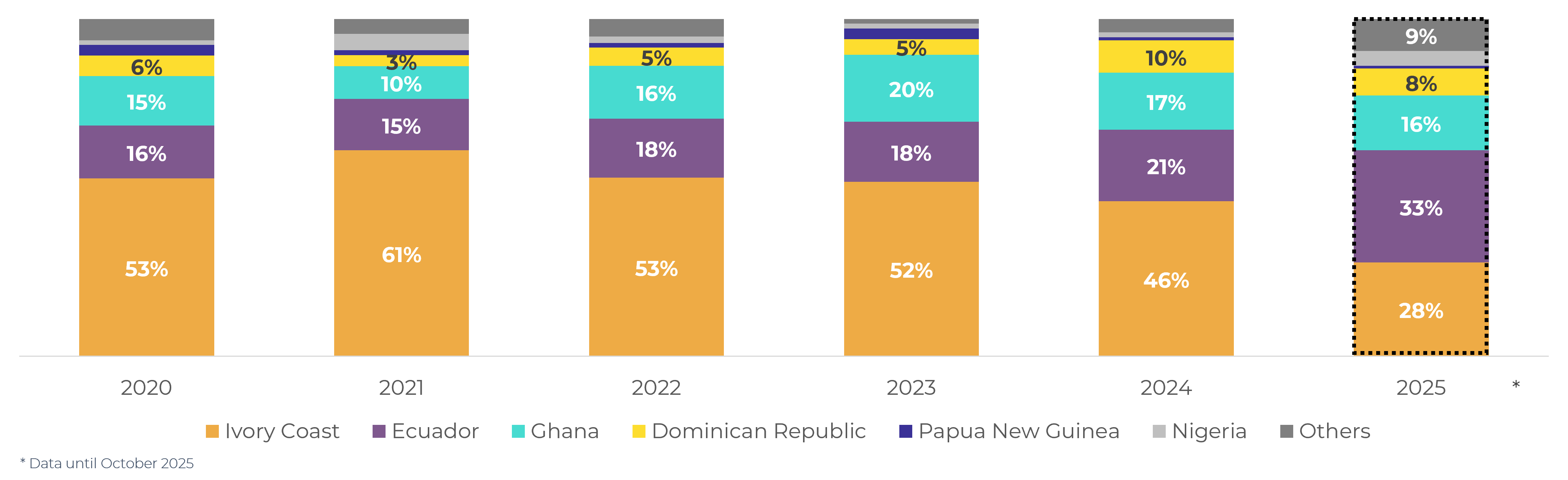

When analyzing US imports by origin, part of the explanation for the higher import volumes becomes clear. From the start of 2025 to October, Ecuador accounted for 33% of imports, while Ivory Coast's share fell from 46% in 2024 to 28%. This movement reflects stronger exports from Ecuador, associated with more competitive price differentials in the US market. The dynamics of the differentials indicate that, while African cocoa premiums remain high, Ecuadorian cocoa has relatively lower prices and an arbitrage that favors the direction of flows to the US, contributing to a relatively more favorable environment compared to the European market. In addition, agreements regarding US tariffs may also have contributed to this change in trade flows.

US: cocoa beans imports by origin (%)

Source: United States International Trade Commission (USITC)

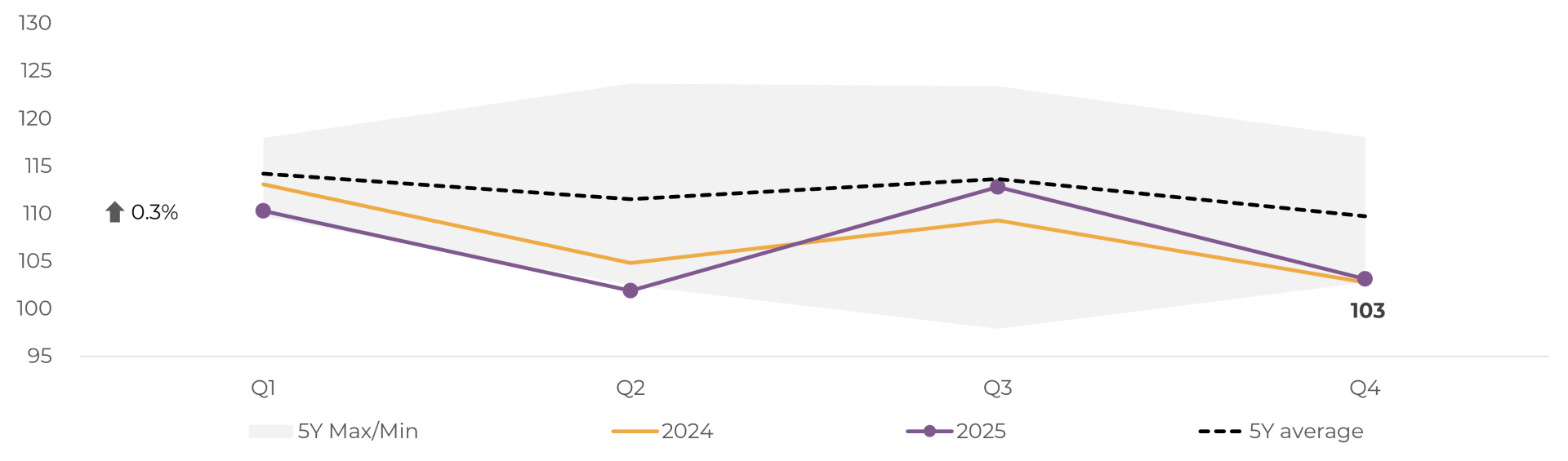

Finally, when analyzing Asian demand, data released by the Cocoa Association of Asia (CAA) indicated a 4.82% drop in grinding in the fourth quarter of 2025 compared to the same period last year, a result below market estimates. This performance partly reflected the downturn observed in Malaysia, one of the main cocoa processing regions in Asia, where grinding fell 6.8% in the fourth quarter of 2025 compared to the previous year, also below market expectations, as reported by the Malaysian Cocoa Board (MCB) and the Cocoa Manufacturers Association (CMG). This data, added to the NCA figures, contributed to the slight recovery observed in the session on Friday, January 16, since the results were released after the market closed on the 15th. The NCA data was published on the afternoon of the 15th, while the CAA data was released on the morning of the 16th.

Cocoa grinding: Asia (‘000 tons)

Source: Cocoa Association of Asia

Overall, the market remains bearish, supported by signs of weakening demand in the main processing regions and the prospect of better production results for the 2025/26 cycle. In line with this environment, the latest positioning data indicate an increase in net short positions in New York and London, reflecting a market that continues to operate cautiously.

Still, from a technical perspective, the Relative Strength Index (RSI) remains close to the oversold zone in both markets. In this context, any changes in the market environment, such as positioning adjustments, technical factors, or changes in weather conditions in producing regions, could trigger corrective movements or greater price volatility in the short term, without, however, signaling a structural change in the still bearish bias for now.

In Summary

Cocoa prices ended another week down, pressured by the release of fourth quarter 2025 grind results, which reinforced the perception of weakening demand in the main processing regions. In Europe, the decline in grinding was more intense than expected, in a context of tight inventory flows and historically high prices, which kept demand sensitive to the availability of raw materials. In Asia, the decline in grinding, partly influenced by Malaysia's performance, although below market estimates, also contributed to the negative reading on the global demand side.

In contrast, North America showed greater resilience, with a slight increase in grinding and robust net imports throughout 2025, sustained mainly by Ecuador's greater share, which offered more competitive prices compared to African origins. Even so, the market remains bearish, supported both by demand fundamentals and expectations of better production results in the 2025/26 cycle. From a technical point of view, the RSI close to the oversold zone suggests a limit to further declines in the short term, opening space for possible correction movements or greater volatility, with no signs of a structural trend change for now.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.