Cocoa market: key highlights from Outlook 2026

- Even with the expectation of a surplus in the 2025/26 season, the global balance remains sensitive to changes in fundamentals, which could keep volatility high in the cocoa market.

- Recent trade problems in Ivory Coast and Ghana, associated with farmgate prices, have affected export flows and may continue to influence the availability of beans in the short term.

- The possible occurrence of El Niño in the second half of 2026 may affect the 26/27 crop development, with the potential to bring drier conditions to West Africa and greater disease pressure in Ecuador, depending on the intensity of the phenomenon.

- Despite the recent recovery in prices, the prevailing market trend is still bearish. However, technical indicators suggest room for short-term adjustments, which may favor technical recoveries and keep market volatility high.

Cocoa market: key highlights from Outlook 2026

Cocoa futures closed slightly higher on Friday, March 6, compared to the previous session. Unlike previous weeks, prices rose 11.8% in New York and 12.6% in London on a weekly basis. In the absence of significant changes in market fundamentals, recent movements are mainly attributed to technical factors, a topic previously discussed during Hedgepoint Outlook 2026 regarding the cocoa market, held in February 27. In this analysis, we present the main topics covered in the event, along with the latest market updates.

Demand is still under pressure

The data indicates a weakening in the main markets. In the European Union, the largest cocoa processing region, beans imports fell 12.1% in the first three months of the 25/26 season compared to the same period in the previous cycle. Although this movement cannot be interpreted in isolation as a direct reflection of grinding, due to the relevant role of stocks, it reinforces an environment still marked by high prices and supply constraints. This scenario contributed to an 8.9% drop in grinding in the region in the fourth quarter of 2025.

In the United States, another important consumer and processor of the commodity, the recent dynamics have been different. Total net cocoa imports, including beans and by-products, increased at the beginning of the 25/26 crop and returned to near historical average levels. Part of this movement is associated with increased cocoa purchases from Ecuador, which has benefited from more competitive differentials and favorable arbitrage conditions compared to African origins.

Even with this relatively resilient behavior in the United States, global demand may remain under pressure throughout the remainder of the 25/26 season and possibly also at the beginning of the next cycle. A significant portion of the industry purchased cocoa at historically high prices, which continues to put pressure on production costs and keep consumer prices at high levels. This environment has also led to portfolio adjustments and product reformulations adopted by the industry as a way to adapt to the high price scenario.

Partial recovery in supply

Weather conditions in the main producing countries have been closely monitored. In Ivory Coast, the world's largest producer, the weather scenario so far is better than that observed in the same period of the previous season, with cumulative rainfall close to average. Still, the lack of rain in the coming weeks may influence the volume and quality of the 25/26 mid-crop. The current production estimate for the country is around 1.78 million tons.

In Ghana, cumulative rainfall is above average, raising concerns about possible impacts on the harvest and disease pressure, factors that are being monitored. The country's production is estimated at approximately 650 kt for the current season.

In Ecuador, the world's third-largest producer, cumulative rainfall remains below the historical average, although it is above the levels observed in the same period of the previous cycle. The country has stood out for its increased production in recent years, and for the current cycle, we expect production to be around 615 kt.

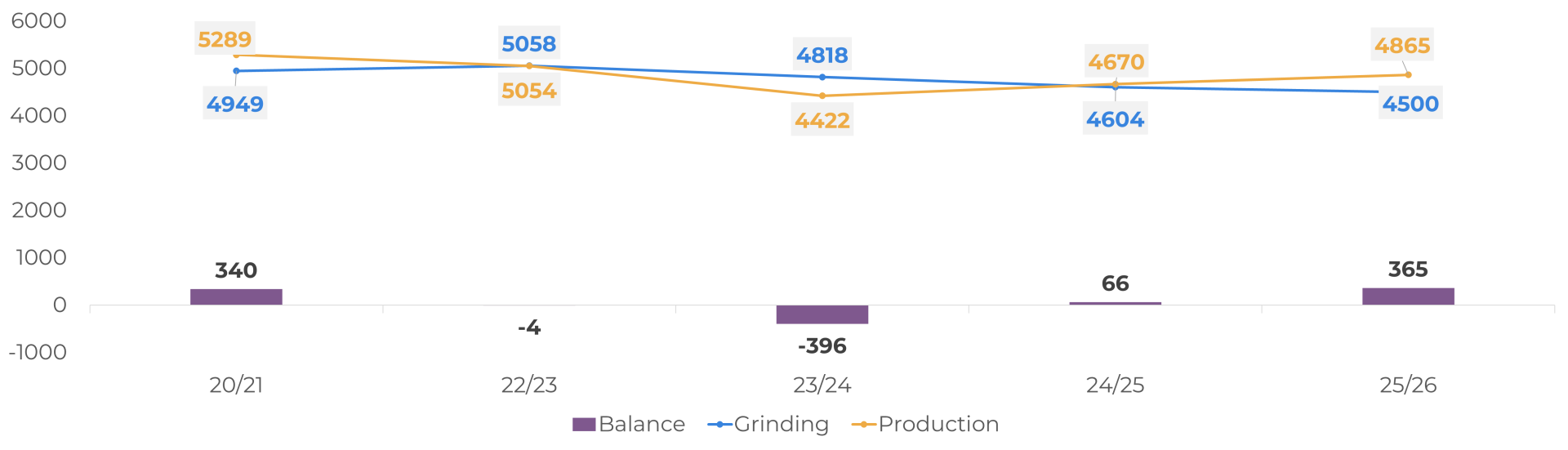

Global balance

Based on this scenario, the current estimate points to a global surplus of around 365 kt in the 25/26 season, resulting from a partial recovery in production (+4.2%) combined with a decline in demand (-3.0%). Even so, despite the expected surplus, the balance remains relatively sensitive, so that any change in fundamentals could have a significant impact on the cocoa market balance and contribute to market volatility.

Global Supply and Demand for Cocoa (‘000 tons)

Source: ICCO, Hedgepoint

Points of attention for 2026

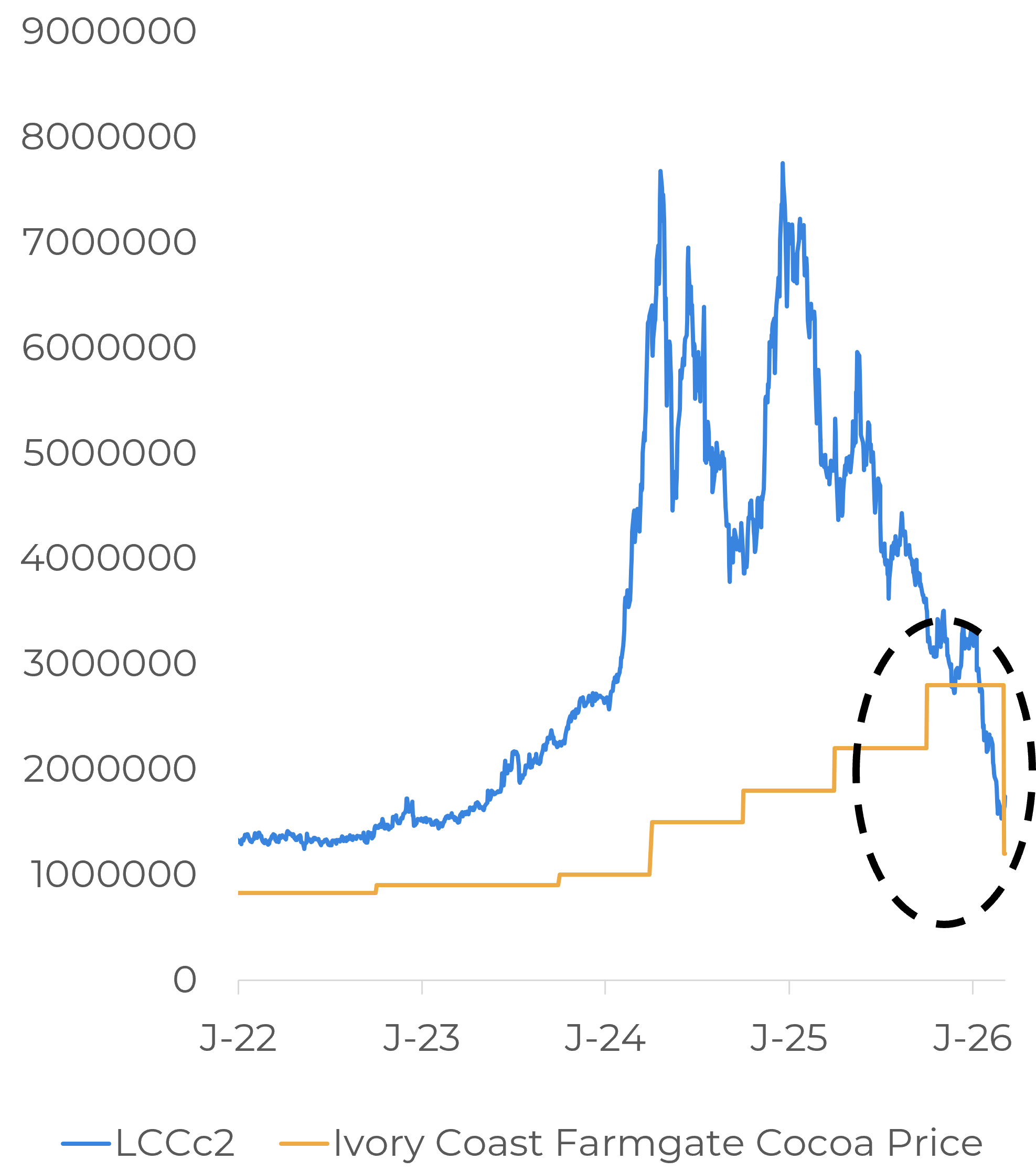

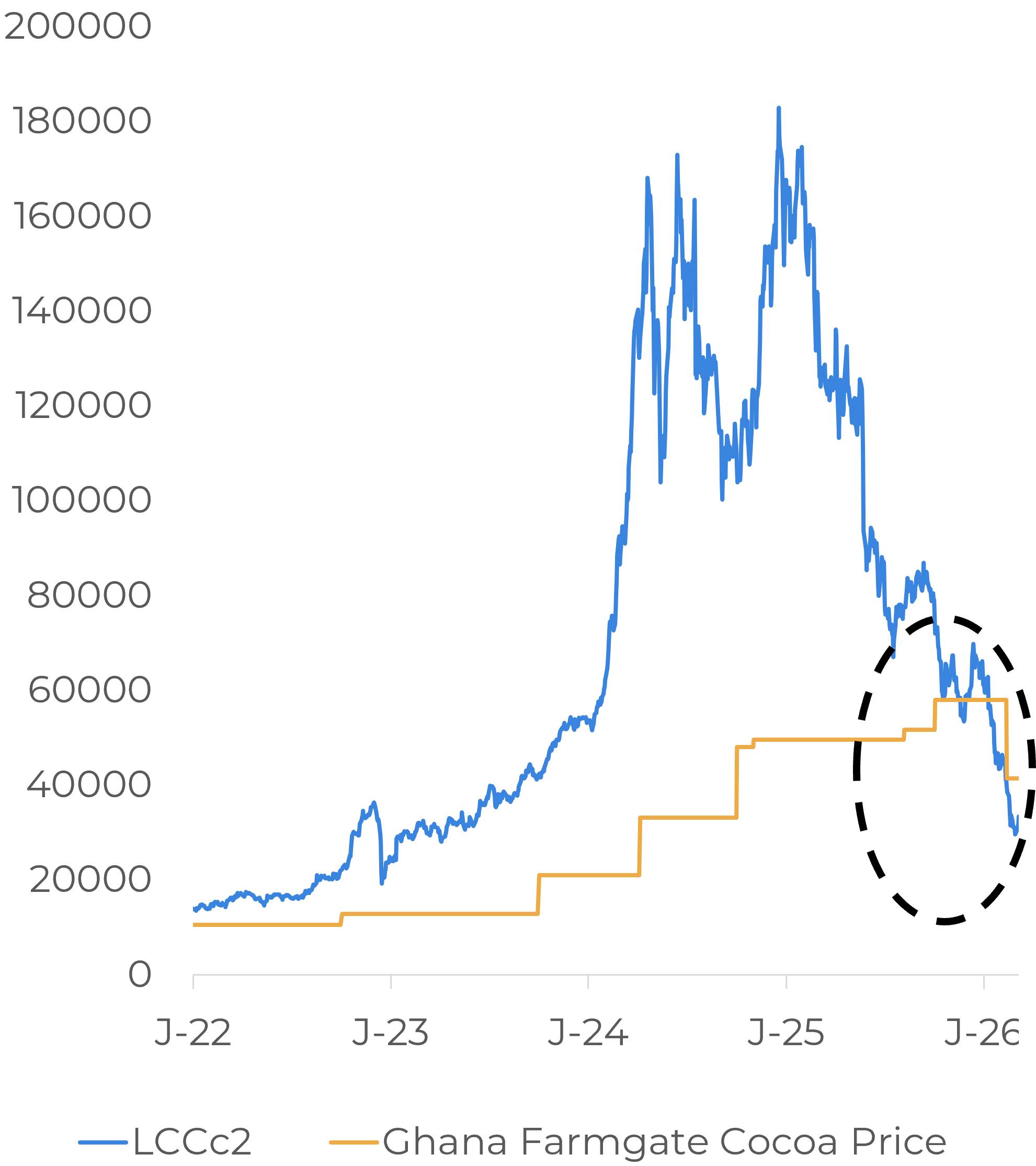

Farmgate prices has been an important factor in understanding the recent problems in trade flows from Ivory Coast and Ghana. With futures falling, domestic prices set by regulators in both countries rose above market levels, which created difficulties in sales and affected the pace of exports. During Hedgepoint Outlook 2026, we expected Ivory Coast to cut the price paid to producers, a move that was confirmed this week. On Wednesday, March 4, the country announced a reduction of about 57% to 1,200 CFA francs per kg. Ghana had already made a similar adjustment earlier.

Ivory Coast reference prices (XOF/t)

Source: LSEG

Ghana reference prices (GHS/t)

Source: LSEG

In addition, Ivory Coast decided to bring forward the start of the mid-crop from April to March in an attempt to improve the marketing of remaining stocks from the main crop, at a time when the quality of some of the beans has also been a concern for the market. This move may contribute to the normalization of export flows starting this month, with possible impacts on trade flows, especially to the European market, the main destination for African beans. Depending on the pace of exports and production, this change may also lead to revisions in the country's estimates, as the anticipation of the mid-crop may influence the calendar for the next 26/27 season.

Another relevant point for the market in 2026 is the increased likelihood of an El Niño event in the second half of the year. Considering the crop calendar in the main producing countries, this period coincides with the development and start of the 26/27 main crop (Oct 2026 – Mar 2027), in addition to the flowering that will give rise to the mid-crop of the same cycle (Apr 2027 – Sep 2027). If confirmed and depending on its intensity, the phenomenon may bring hotter and drier conditions to West Africa, increasing the risk of water stress in crops, while in Ecuador it tends to cause increased rainfall and greater disease pressure.

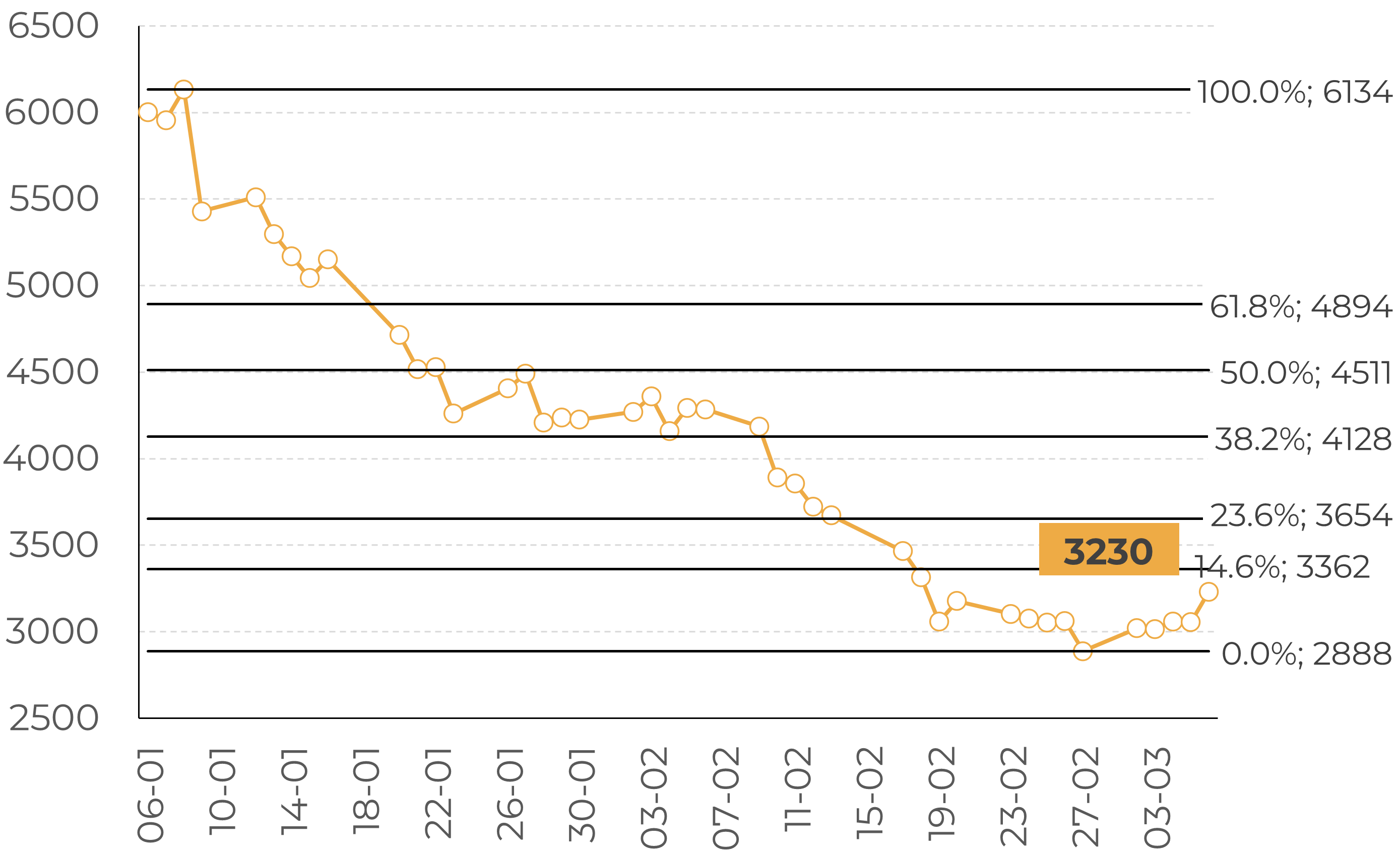

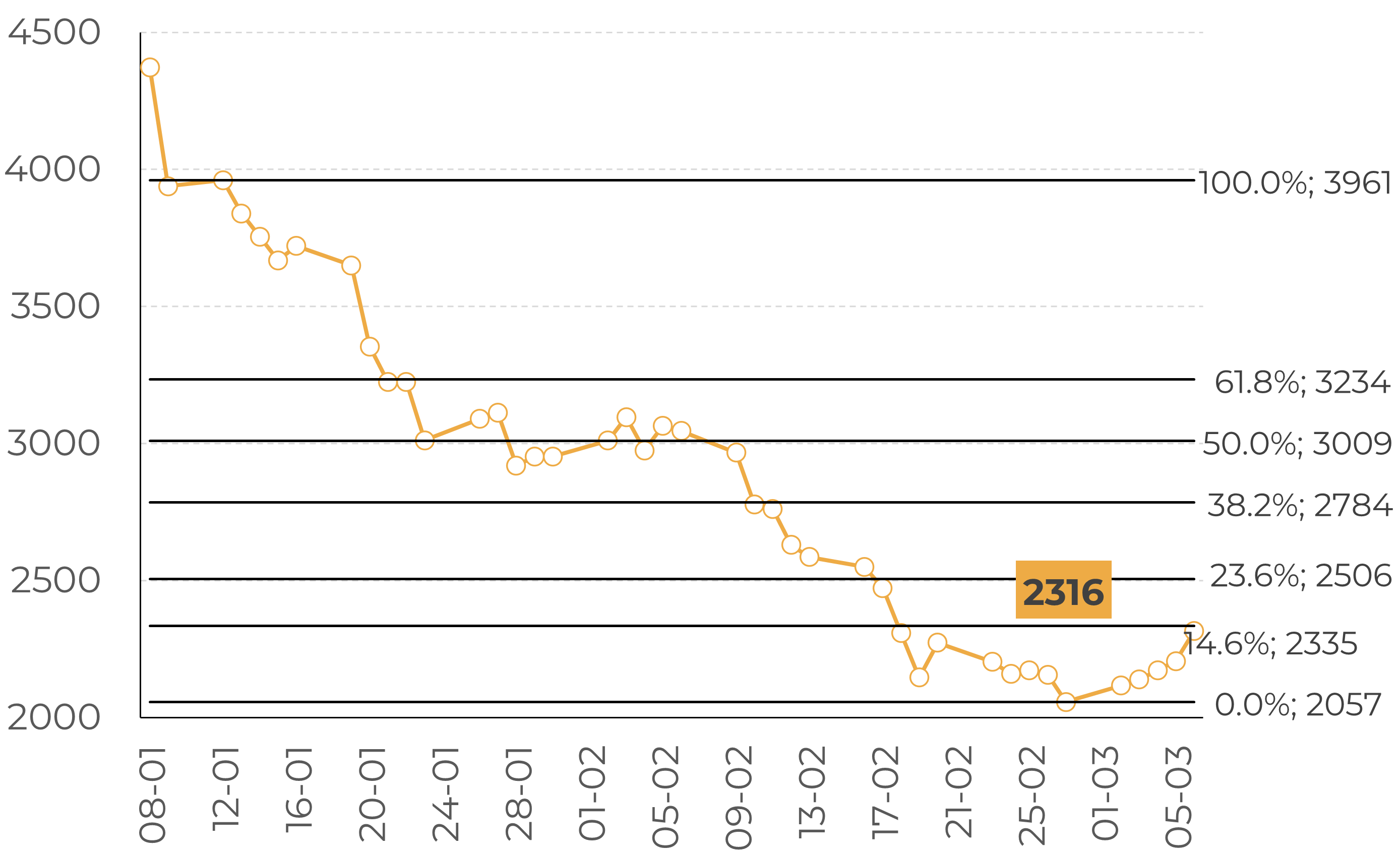

From a technical point of view, the market continues to reflect a bearish trend. The RSI in both markets, New York and London, remains close to oversold territory, which may open room for short-term adjustments, including profit-taking and short covering by funds. This movement may have contributed to the recovery observed throughout the week. In addition, the recent escalation of the conflict in the Middle East, which impacts the macroeconomic scenario and the global commodities market, may also have contributed to the behavior of prices. The impacts on the cocoa market, such as production cost, freight, logistics, and trade flows, will be addressed in the next analysis.

Cocoa – New York May 26: Fibonacci retracement levels (USD/t)

Source: LSEG

Cocoa – London May 26: Fibonacci retracement levels (GBP/t)

Source: LSEG

In Summary

Even with the prospect of a surplus for the 25/26 season, the cocoa market is likely to remain volatile in the short and medium term. The expectation of greater availability supports a downward trend for prices, but factors such as weather, technical adjustments, and decisions in the main origins continue to influence price behavior.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.