The Middle East conflict escalation: what about the cocoa market?

- The escalation of the conflict in the Middle East has heightened geopolitical risk and impacted the energy market, with Brent crude oil reaching its highest levels since 2022.

- The disruption of the Strait of Hormuz and reduced traffic in the Suez Canal have increased global logistics costs and widened risk premiums on freight and marine insurance.

- This heightened uncertainty tends to strengthen the dollar and increase inflationary pressures, driving up the cost of energy, fertilizers, and other inputs critical to agricultural production.

- For the cocoa market, the direct impacts on trade routes are limited, as about 80% of cocoa by-products and approximately 70% of cocoa beans imported by the European Union originate in West Africa and use unaffected Atlantic routes.

- The most significant effects on the sector tend to occur indirectly, through higher freight costs, vessel availability, and potential adjustments to trade flows in the medium term, keeping the cocoa market sensitive and subject to greater volatility.

The Middle East conflict escalation: what about the cocoa market?

On February 28, tensions in the Middle East entered a new phase. Coordinated attacks by the U.S. and Israel against strategic regions in Iran triggered retaliation from the country and intensified the conflict, amplifying the impacts on the global economy and trade. With the escalation, several neighboring countries hosting U.S. bases or energy assets became directly or indirectly involved, such as Iraq, Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, and Bahrain. Additionally, drone incidents and missile activities also affected areas near Lebanon, Syria, and Azerbaijan, highlighting the regional nature of the escalation.

The first impacts were observed in the energy market. The disruption of the Strait of Hormuz, which accounts for about one-fifth of global oil and LNG flows, and the reduction in maritime traffic through the Suez Canal due to insecurity in the Red Sea directly affect commercial energy flows. Additionally, production cuts by Saudi Arabia and other OPEC members contributed to the critical situation, driving Brent oil prices to their highest levels since 2022 during the March 9 trading session.

President Donald Trump’s statement that the conflict was nearing an end, and the easing of sanctions on Russian oil, the world’s second-largest exporter, helped reverse some of the gains in prices. In addition, on Wednesday, March 11, the International Energy Agency (IEA) recommended the release of 400 million barrels of oil to curb the rise in the energy market. Even so, the situation remains critical. What the agency describes as the largest disruption to oil supplies in history, coupled with the intensification of attacks in recent days, continues to put pressure on prices.

The conflict involved some of the key players in the Middle East energy market and disrupted strategic shipping routes, driving up geopolitical risk premiums in energy, freight, and currency markets. As a result, the regional military conflict began to generate economic and commercial impacts on a global scale, affecting the commodities market as well. In this context, this analysis aims to discuss the potential impacts of the conflict’s escalation on the cocoa market, assessing possible developments for a market that is already highly volatile.

From a broader macroeconomic perspective, a scenario of greater uncertainty tends to favor the dollar, which could improve commodity returns for producers and stimulate sales in the medium term. On the other hand, this same context of uncertainty may also intensify inflationary pressure, raising costs and risks throughout the commodity chain, including cocoa, and contributing to higher price levels.

In this regard, another relevant point is that rising oil prices and dollar volatility tend to put pressure on production costs, making not only the fuel used on farms more expensive but also inputs such as fertilizers and pesticides, reflecting higher energy and logistics costs. In addition, a disruption in the Strait of Hormuz could affect global fertilizer trade, as major Gulf producers rely on this route to transport a significant portion of the world’s supply.

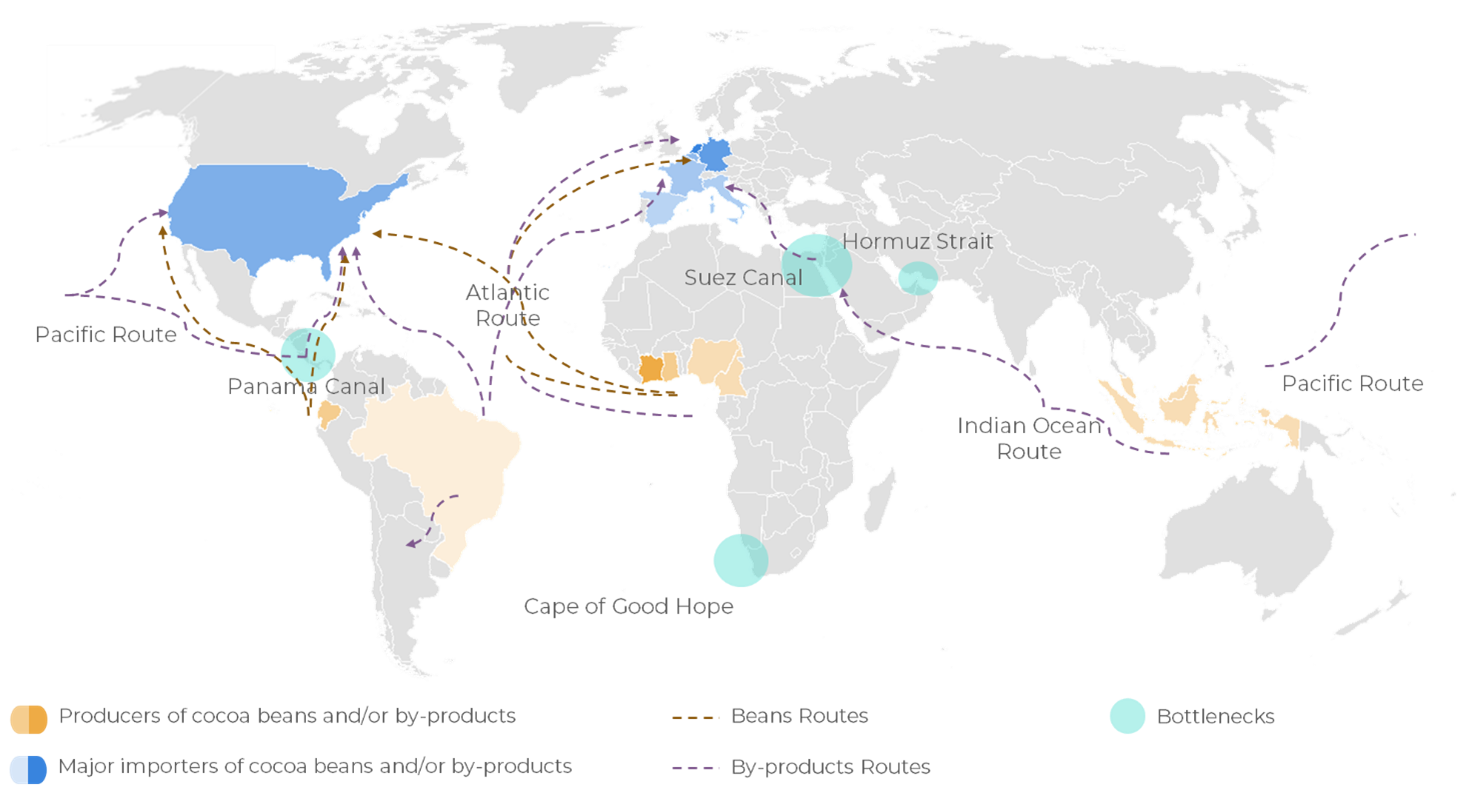

Looking at the issue from a logistical perspective and evaluating the main global maritime routes, several critical points stand out, three of which are particularly relevant in the current context. As mentioned earlier, the Strait of Hormuz, which is directly impacted, the Suez Canal, where traffic has decreased due to insecurity in the Red Sea, and the Cape of Good Hope, which has become a longer alternative route due to the conflict.

Major maritime routes in the cocoa market

Source: Hedgepoint

For the cocoa market, the impacts tend to be indirect, as none of the routes used by major producers and importers of cocoa beans and by-products have been directly affected. The main exception is the route used by Malaysia and Indonesia to export cocoa powder and cocoa butter to Europe. Even so, the impact is limited, since, on average, about 80% of the European Union’s imports of these by-products originate in West Africa, whose Atlantic route remains unchanged. It is also worth noting that about 70% of the cocoa beans imported by the European Union also originate in West Africa.

Thus, the indirect effects are more closely linked to rising freight costs and global logistics dynamics, particularly regarding vessel availability and the cost of marine insurance, depending on the duration of this escalation of the conflict. In this context, we are also monitoring the possibility of changes in trade flows in the medium term, particularly in the North American market, should rising logistics costs begin to significantly influence competitiveness among origins, while also considering limitations related to product quality.

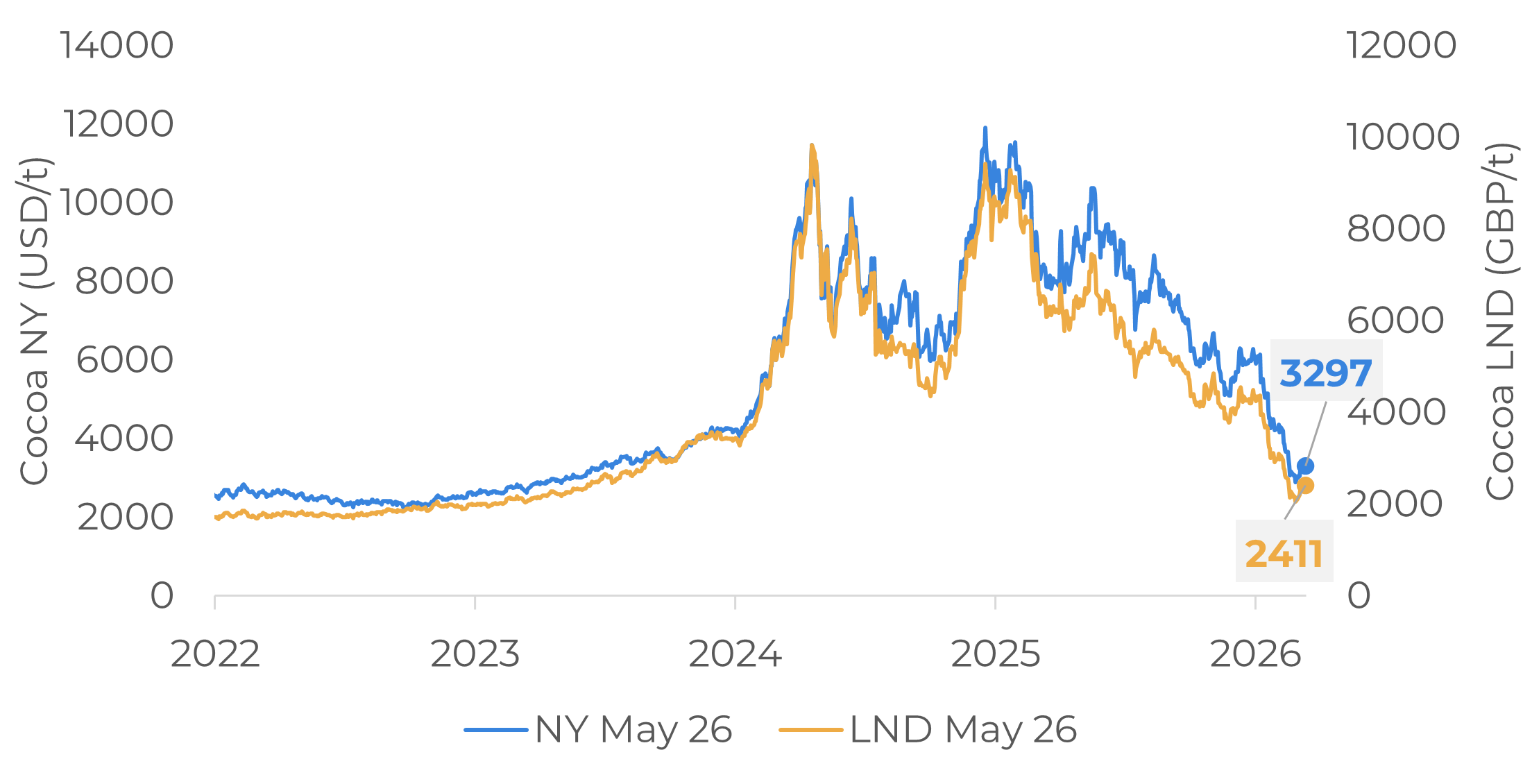

Finally, it is worth noting that the cocoa market is already sensitive due to factors discussed in recent analyses, and that the conflict in the Middle East is likely to sustain volatility in this market. In this scenario, cocoa prices closed on Friday, March 13, with a weekly gain of 2.14% in New York and 4.54% in London.

Cocoa Prices in New York and London

Source: LSEG

In Summary

The escalation of tensions in the Middle East following the attacks on February 28 has amplified the geopolitical impacts on energy, logistics, and global markets. The disruption of the Strait of Hormuz and reduced traffic in the Suez Canal have raised risk premiums in the energy market, contributing to the recent rise in oil prices and greater macroeconomic uncertainty. This scenario is putting pressure on energy, logistics, and agricultural costs, particularly through rising fertilizer and input prices. For the cocoa market, direct impacts on trade routes are limited, as the main flows between West Africa and Europe remain unchanged, but indirect effects may arise through freight rates, marine insurance, and global logistics dynamics. In a market already sensitive to structural and technical factors, this environment of uncertainty tends to sustain price volatility.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.