Weather remains on the cocoa market’s radar

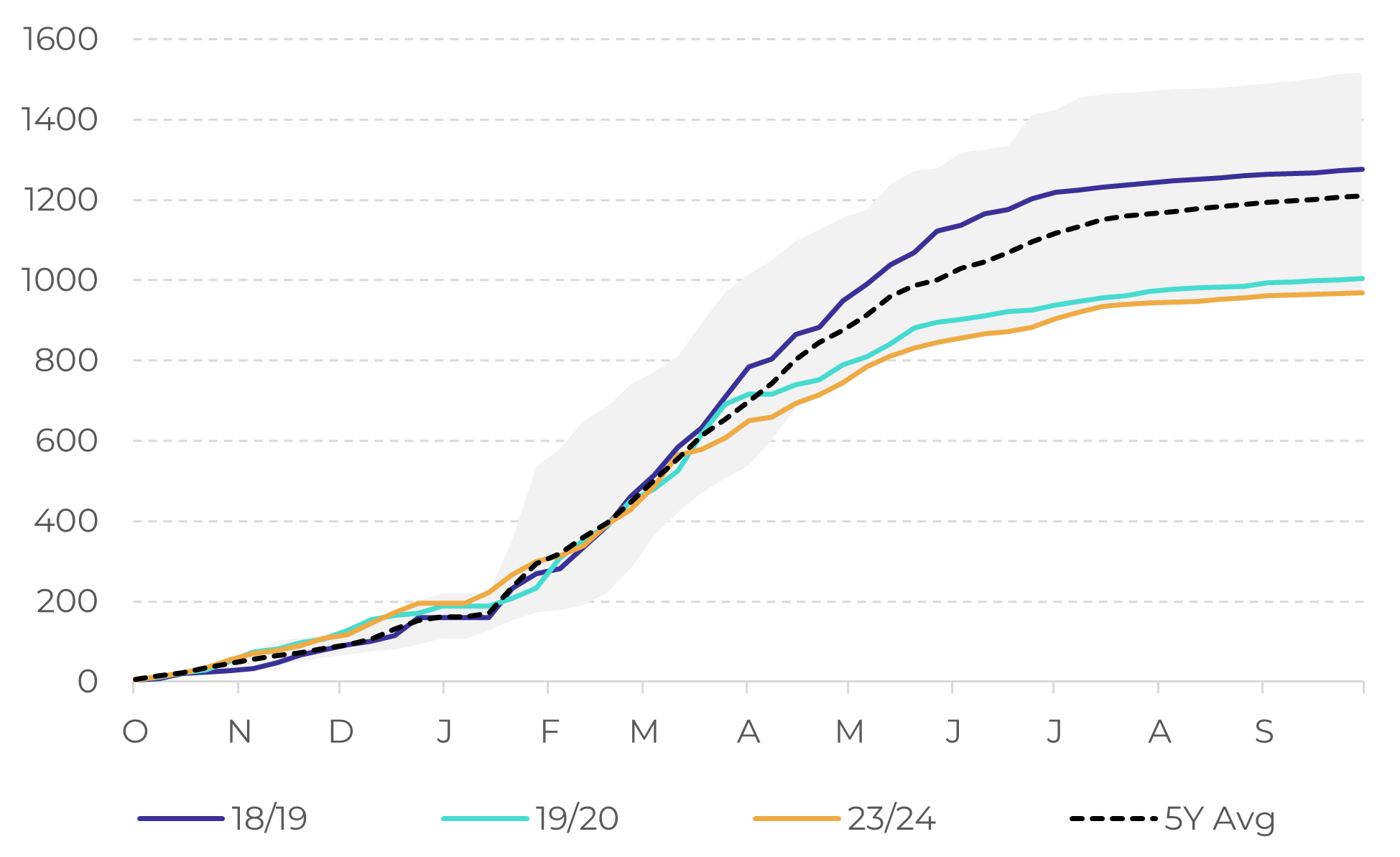

- In West Africa, cumulative rainfall in Ivory Coast and Ghana has exceeded last season’s levels and remains close to the historical average, supporting a partial recovery in production and reinforcing expectations of a surplus in 2025/26.

- Even so, the short term continues to demand attention, as some areas in these regions may experience below-average rainfall in the coming weeks at a critical time for fruit development and the flowering of the next main crop.

- In the medium and long term, the possibility of a transition from La Niña to an El Niño event between May and July keeps the weather on the radar, as the phenomenon could alter climate patterns in key commodity-producing regions.

- The analyzed evidence shows that El Niño’s effects on cocoa do not follow a single pattern, with distinct responses regarding rainfall, temperature, and production, suggesting that the final impact depends on the event’s intensity, its timing, and local conditions in each origin.

Weather remains on the cocoa market’s radar

Cocoa futures closed the week of April 10 at 3,246 USD/t in New York and 2,423 GBP/t in London. With no significant changes in fundamentals, the most recent market movements have been driven mainly by technical factors and the macroeconomic outlook, given the developments in the conflict between the US and Iran. Although the trend remains bearish, the cocoa market remains structurally sensitive, such that any shift in perception contributes to volatility.

In this context, the weather remains among the market’s key points of focus. More favorable weather conditions, especially regarding cumulative rainfall, are among the factors supporting the partial recovery of production in West Africa, the main cocoa-producing region. To date, Ivory Coast and Ghana have recorded cumulative rainfall in the current cycle above that observed in the same period of the previous crop year and close to the historical average. Combined with the expected reduction in grinding, this situation reinforces the outlook for a surplus in the 2025/26 season.

Nevertheless, given the characteristics of cocoa fruit development, a good amount of rainfall in the coming weeks remains important for the fruits that are still forming and will be harvested by the end of the mid-crop. Additionally, April and May correspond to the main flowering period that will give rise to the fruits of the 26/27 main crop, so favorable weather conditions will be important in determining both the volume and quality of the start of the next crop. In the short term, although weather forecasts involve some degree of uncertainty, models suggest that some areas of Ivory Coast may experience below-average rainfall over the next 14 days, which remains a point of concern for the market.

In the medium and long term, the weather also remains on the cocoa market’s radar. Statistical models point to the end of La Niña in 2026 and indicate an increased probability of an El Niño event beginning between May and July. The phenomenon tends to change global weather patterns, increasing the risk of drought, excessive rainfall, heat waves, and changes in storm and hurricane activity in key commodity-producing regions.

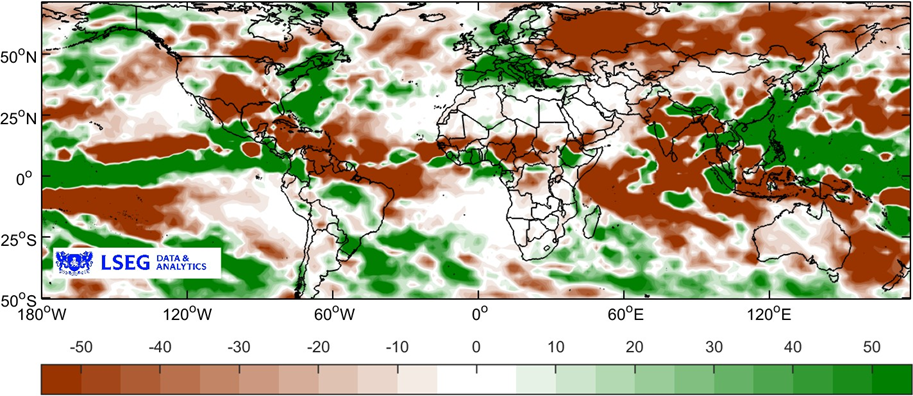

Regarding cocoa's main producing regions, the potential effects of El Niño vary depending on its intensity and the specific location analyzed. The phenomenon may lead to drier conditions in West and Central Africa, Central America, and northern Brazil, while simultaneously increasing rainfall in Peru, Ecuador, and parts of Africa. Regarding temperature, heat waves may occur more frequently in South America and Africa, among other regions. It is worth noting that, in some regions, especially in West Africa, the weather response to El Niño is not always direct and may be influenced by regional events.

El Niño precipitation anomalies | Jun-Aug (mm)

Source: LSEG

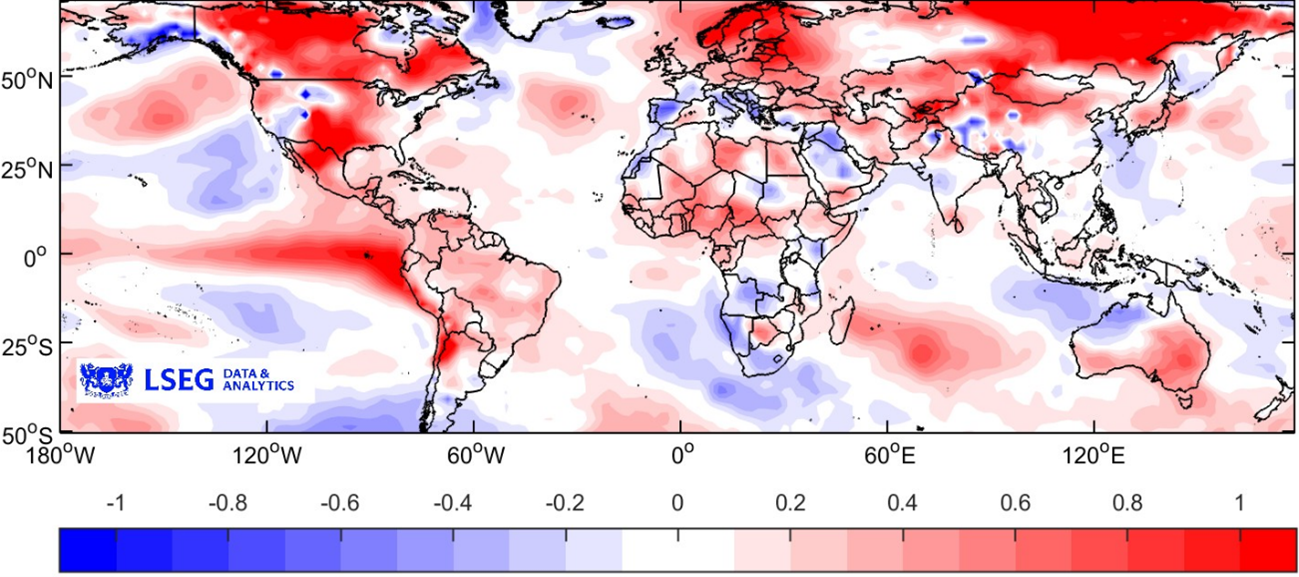

El Niño temperature anomalies | Jun-Aug (ºC)

Source: LSEG

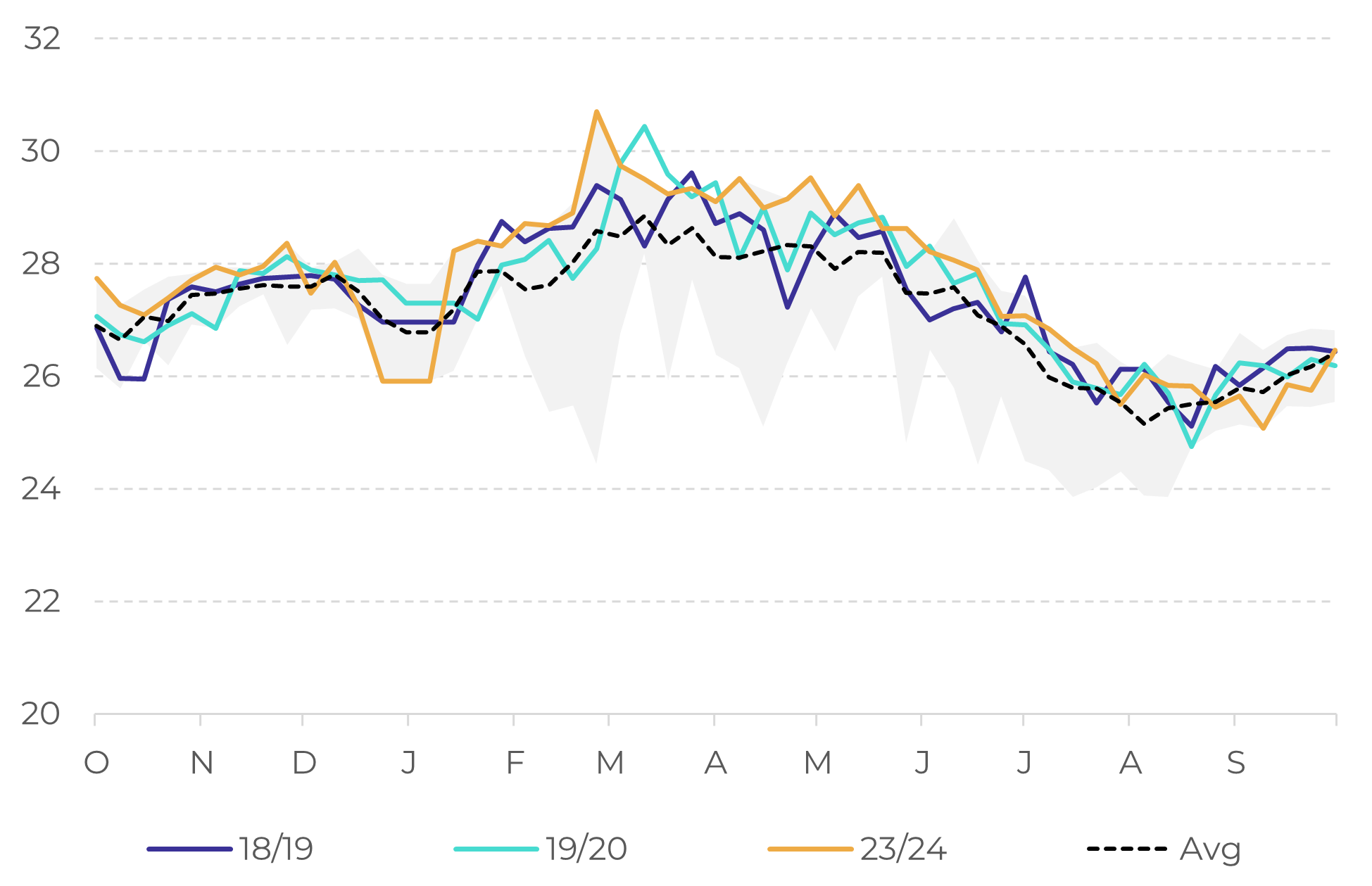

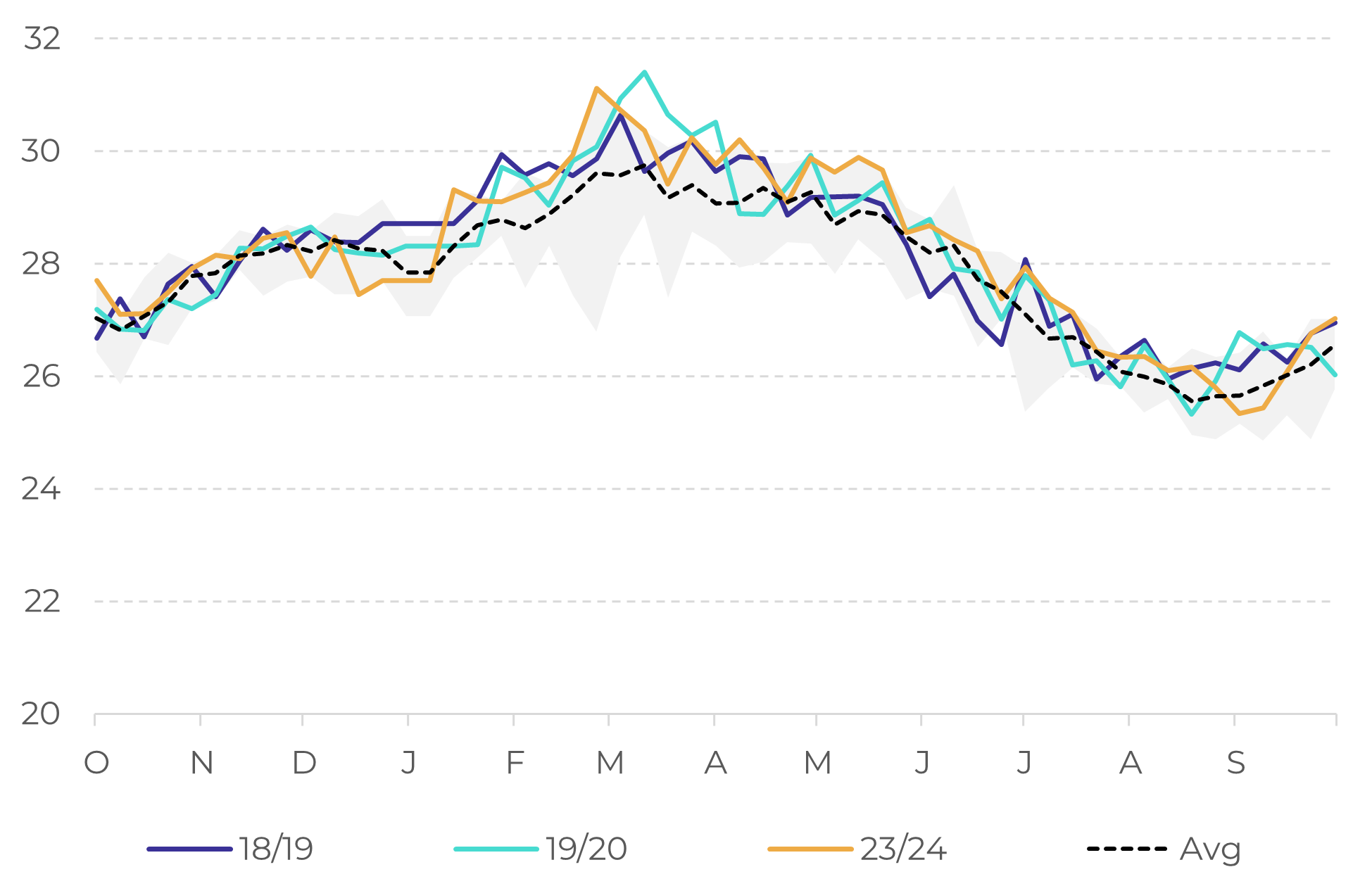

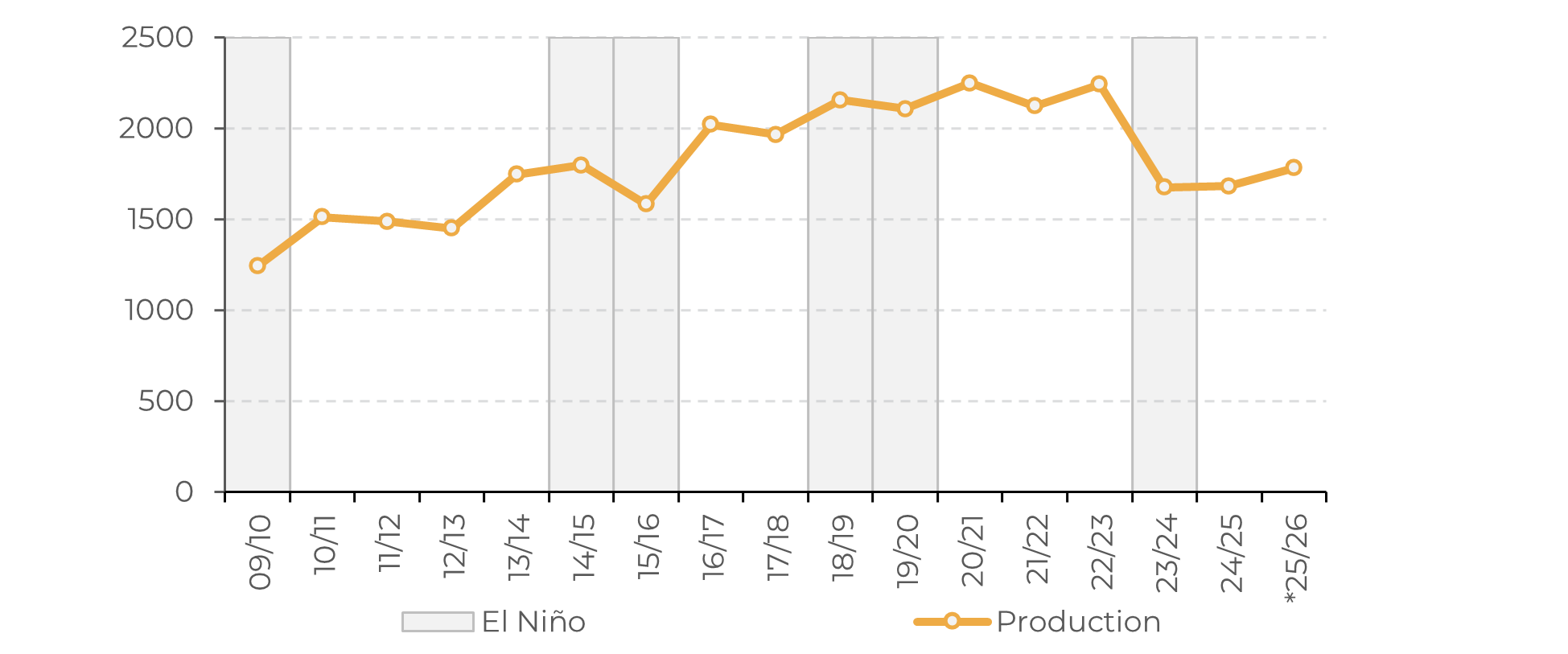

When examining the last three seasons during which El Niño occurred, cumulative precipitation in the main cocoa-producing regions does not indicate a single pattern across the origins analyzed. The results observed in Ivory Coast, Ghana, and Ecuador show that the phenomenon’s impacts on rainfall appear to depend on the event’s intensity, regional characteristics, and how precipitation is distributed throughout the season, rather than on a simple, generalized relationship with El Niño.

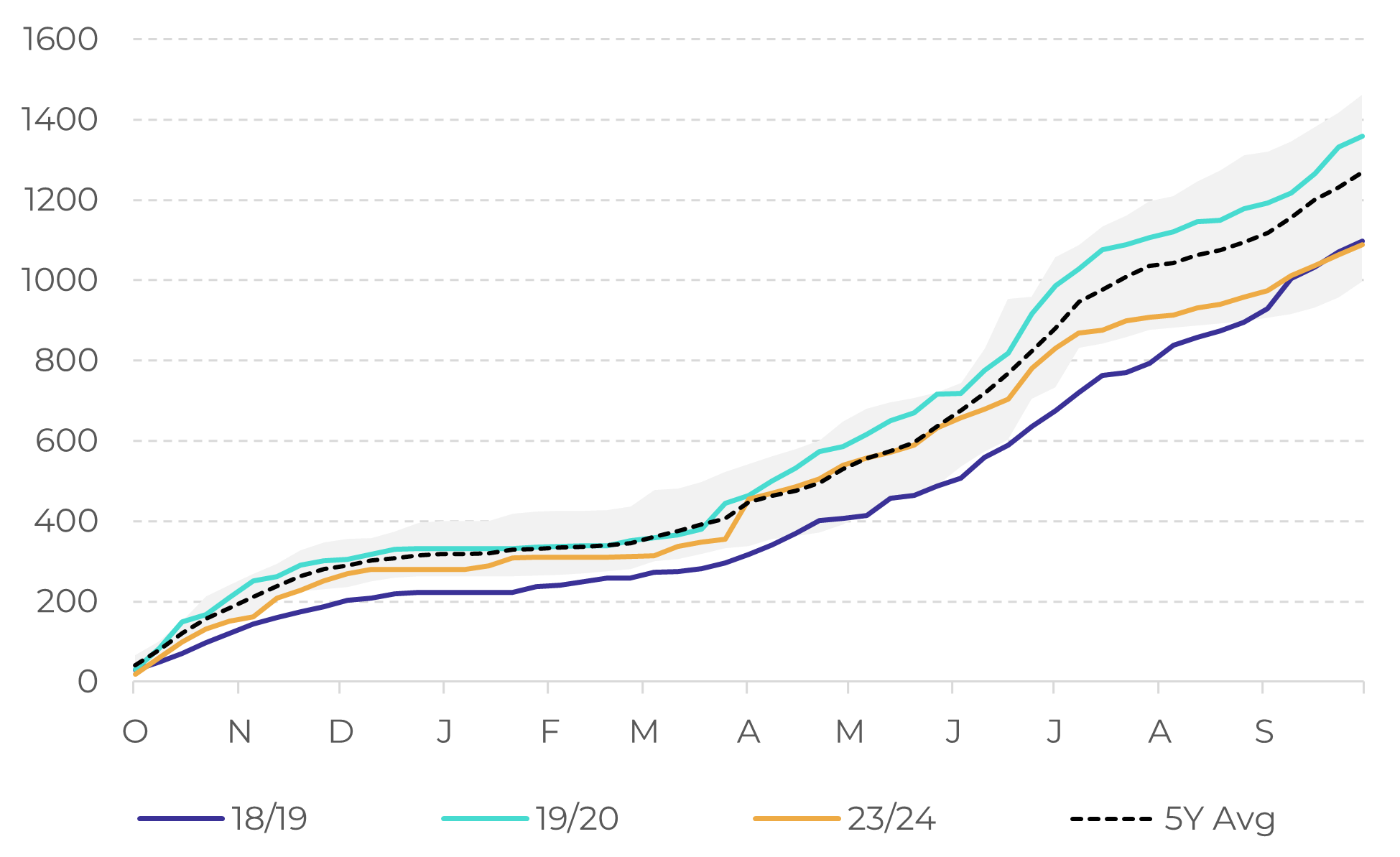

Ivory Coast – cumulative precipitation during El Niño years (mm)

* Weighted average by main producing regions

Source: CPC Gadas, Hedgepoint

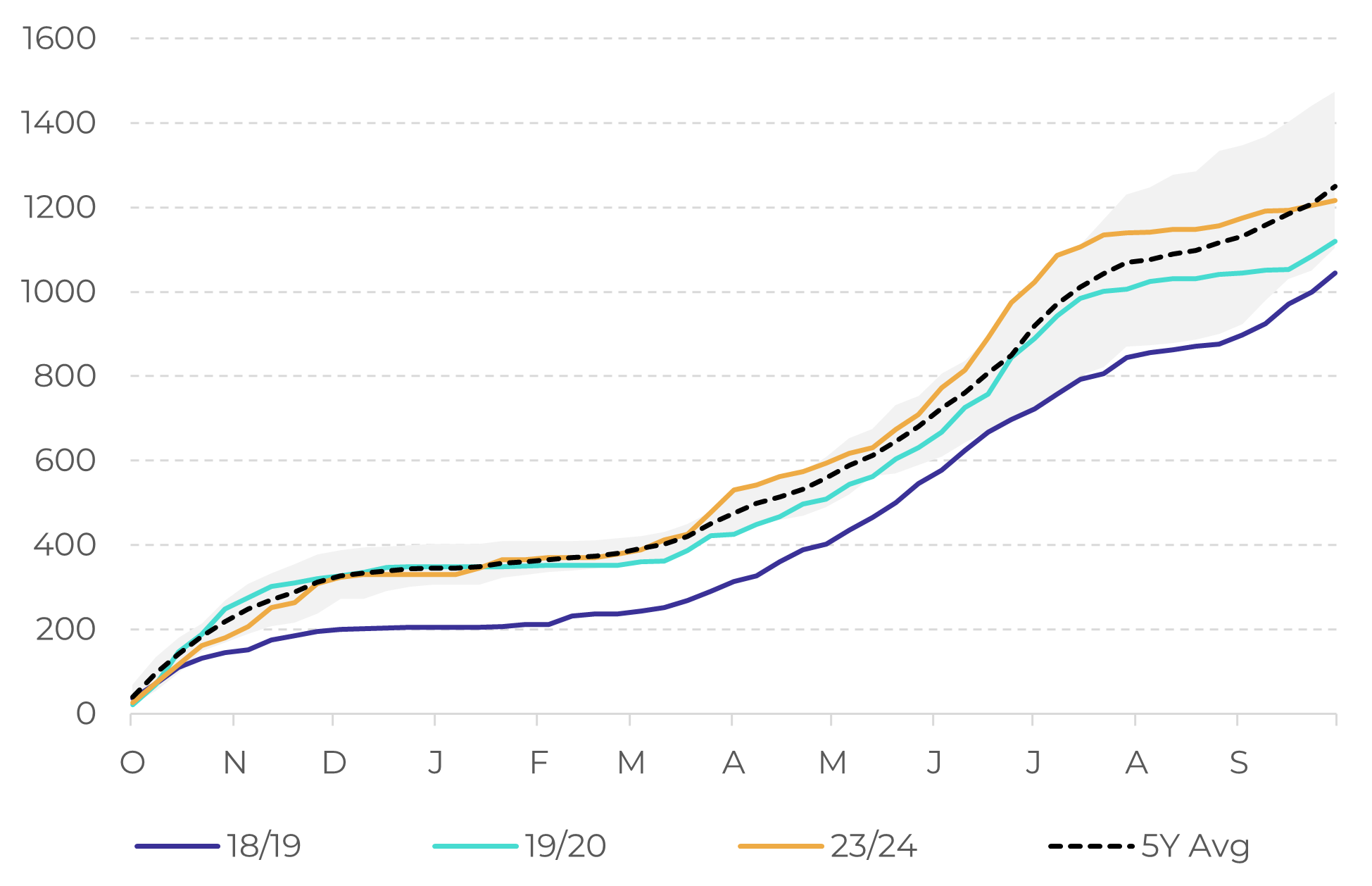

Ghana – cumulative precipitation during El Niño years (mm)

* Weighted average by main producing regions

Source: CPC Gadas, Hedgepoint

Ecuador – cumulative precipitation during El Niño years (mm)

* Weighted average by main producing regions

Source: CPC Gadas, Hedgepoint

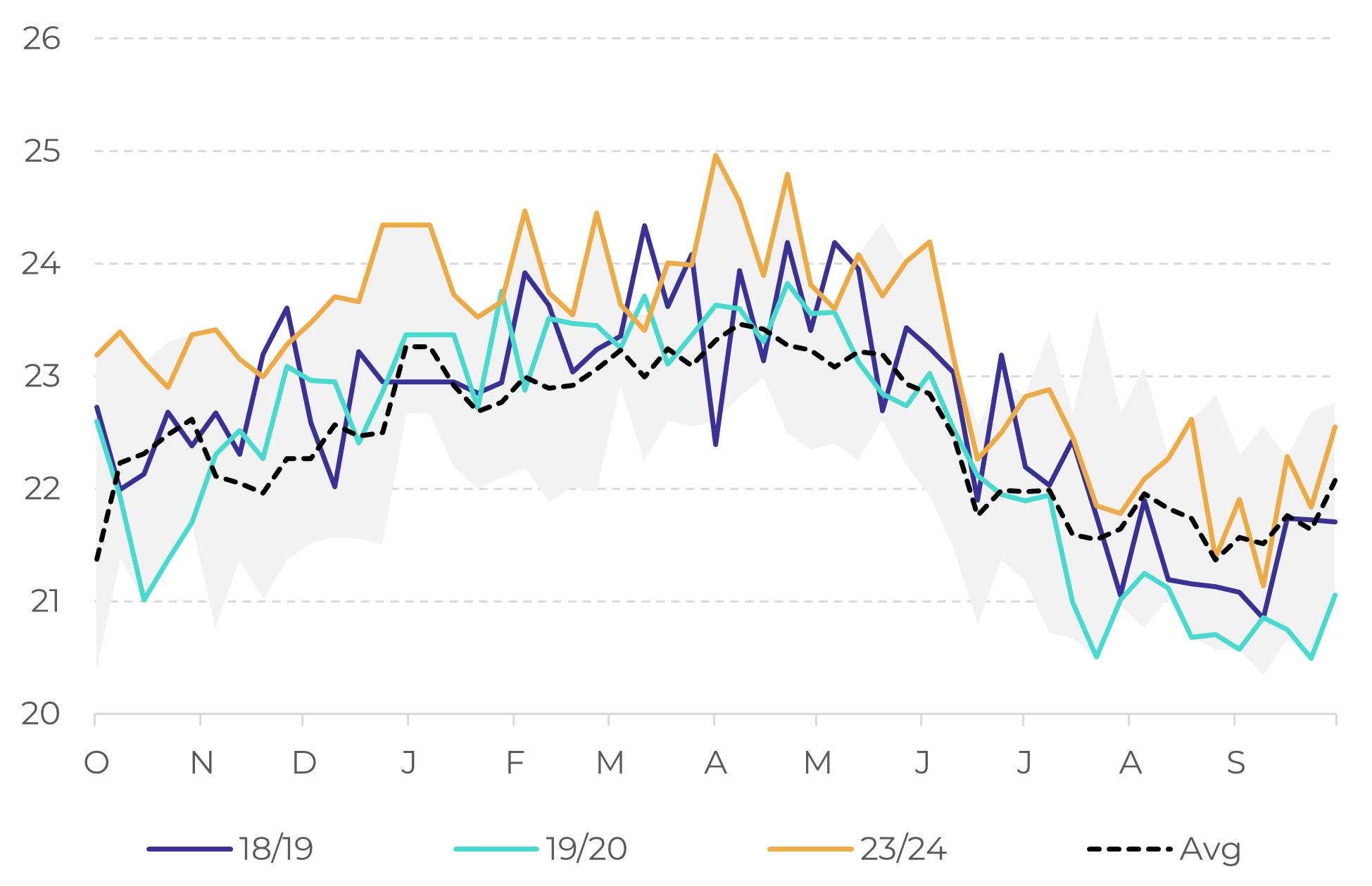

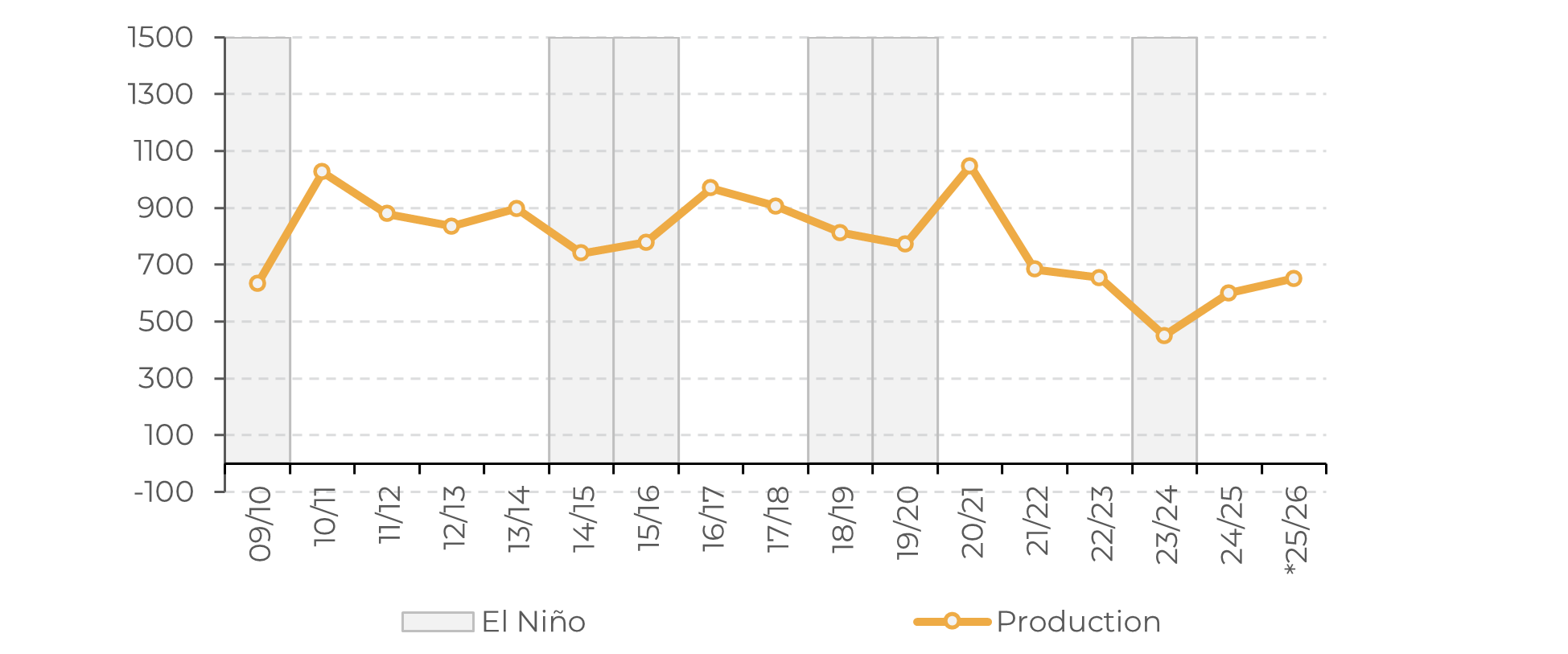

On the other hand, temperature data indicate a more consistent pattern. In recent El Niño-affected crops, Ivory Coast, Ghana, and Ecuador recorded, at different times, above-average temperatures, with the highest occurrence during the main flowering period (April - June). This behavior can intensify crop stress, especially when combined with reduced water availability.

Ivory Coast – average temperature during El Niño years (Cº)

* Weighted average by main producing regions

Source: CPC Gadas, Hedgepoint

Ghana – average temperature during El Niño years (Cº)

* Weighted average by main producing regions

Source: CPC Gadas, Hedgepoint

Ecuador – average temperature during El Niño years (Cº)

* Weighted average by main producing regions

Source: CPC Gadas, Hedgepoint

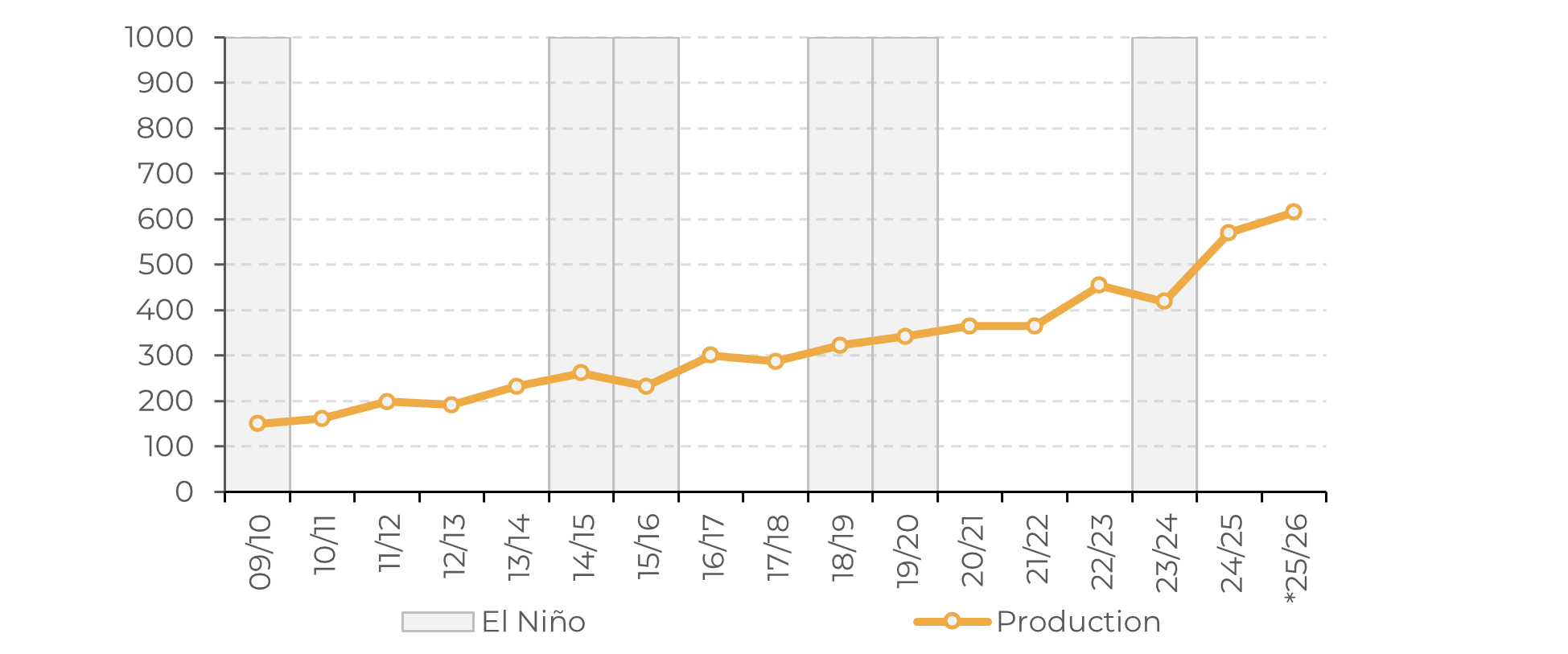

Furthermore, production response to the phenomenon does not appear to follow a single pattern, especially since it is a perennial crop. Some analyses suggests that production may react in a nonlinear and time-delayed manner, with losses in the current season of the event and possible positive effects in subsequent crops. This behavior may be related both to the reallocation of resources by the plants and to the phenomenon’s effects on rainfall distribution throughout the production cycle.

Ivory Coast: cocoa production by crop (‘000 tons)

Source: USDA, ICCO, FAOSAT, Hedgepoint

Ghana: cocoa production by crop (‘000 tons)

Source: USDA, ICCO, FAOSAT, Hedgepoint

Ecuador: cocoa production by crop (‘000 tons)

Source: USDA, ICCO, FAOSAT, Hedgepoint

In this regard, production data suggest that, in some seasons, there was a recovery in the cycles following the events, consistent with the hypothesis of lagged effects of the phenomenon on the crop. Nevertheless, this pattern is not uniform across countries and seasons, reinforcing the notion that the yield response to El Niño likely depends on the interaction between local climate, the phenological calendar, and the specific agronomic conditions of each region.

In general, El Niño tends to be associated with lower crop yields, as it leads to higher temperatures and, in certain contexts, also increases rainfall variability. However, its effects on cocoa do not follow a single pattern. The magnitude of the impacts depends on the intensity of the phenomenon, the timing of its occurrence throughout the crop cycle, and its interactions with critical phases of crop development, such as flowering and fruit development. Thus, the final effect on production can vary significantly between origins and seasons.

In Summary

Cocoa futures continued to fluctuate mainly due to technical factors and the macroeconomic environment, in a market that remains sensitive and volatile. At the same time, the weather remains a point of focus, as more favorable rainfall conditions in West Africa have been supporting a partial recovery in production and reinforcing the outlook for a surplus in 25/26. However, the market remains vigilant in the short term, given the risk of below-average rainfall in parts of Ivory Coast, and in the medium and long term, with the increasing likelihood of an El Niño event. Although the phenomenon’s effects on rainfall do not show a uniform pattern across the origins analyzed, temperature data show a more consistent trend of above-average values, especially during the flowering period. Additionally, studies suggest that the impacts of El Niño on cocoa production may vary and be time-lagged, depending on the event’s intensity, the timing of its occurrence, and the specific conditions of each origin.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.