Live with Experts: Key Highlights for the Cocoa Market

Live with Experts: Key Highlights for the Cocoa Market

The cocoa market remains volatile, reflecting a combination of macroeconomic uncertainties, adjustments in global supply and demand flows, and looming climate risks. In this context, this analysis aims to consolidate the main points discussed during the Live with Experts: Cocoa, held on April 29, bringing together highlights of the macroeconomic view, cocoa supply and demand dynamics, weather factors, and the global market balance, in order to contextualize recent price movements and the associated risks.

Macroeconomic Outlook

The recent macroeconomic environment has been strongly influenced by the escalation of the conflict between the US and Iran, which has raised the global risk premium and caused a crisis in the energy sector. Disruptions in the Strait of Hormuz and increased insecurity in the Red Sea have reduced traffic through strategic routes such as the Suez Canal, driving up freight and insurance costs and affecting global logistics. This scenario is putting pressure on energy and fertilizer costs, especially nitrogen-based fertilizers, increasing inflationary risks.

In the US, inflation already rose in March and reinforced fears of stagflation, while in Europe, which is more sensitive to the conflict’s impact on the energy sector, inflation may exceed 3% in the second quarter, accompanied by a decline in consumer confidence and a repricing of expectations regarding the ECB’s monetary policy. For the cocoa market, the impacts are indirect, linked mainly to rising logistics and energy costs, adding volatility to a market that is already sensitive.

Cocoa Imports and Demand

On the demand side, Asia showed positive signs, particularly Malaysia, where grinding volume increased by 8.7% in the first quarter of 2026, above expectations, temporarily supporting international prices in mid-April. This trend was reflected in a 5.2% increase in Asian grinding, a region that accounts for about 23% of global processing.

However, this was offset by significant weakness in Europe, which put downward pressure on prices, where processing fell 7.8% over the same period, reflecting historically low net imports between December and January, despite some recovery in February and March. In the US, net beans imports remain above the previous cycle, with a larger share from Ecuador beans , in addition to a sharp increase in imports of paste and butter, which may have reduced the need for local processing and contributed to the 3.8% decline in grinding in the first quarter. In Brazil, the industry faces additional challenges due to import restrictions, changes in the drawback system, and regulatory uncertainties, amid a 0.8% decline in milling in 1Q26.

Supply and Weather

On the supply side, considering the crop calendar, major producers are in a critical phase between the mid-crop and flowering, which will give rise to the main 26/27 season. In Ivory Coast, despite better weather conditions than in the previous cycle, the short term still requires monitoring. The 25/26 production estimate was revised downward by 1,753 kt due to the likely early closure of the crop from October to September.

Regarding trade flows, the increase in the farmgate price last season, followed by a correction in international prices, caused a slowdown in the country’s sales and adjustments in export flows. Consequently, the government of Ivory Coast, as well as Ghana, which also faced these issues, took several measures to normalize trade, including bringing forward the mid-crop. Between February and March, following the reduction in the farmgate price and the adoption of the other measures, we project a gradual recovery in exports, which is expected to converge toward levels close to the historical average in subsequent periods.

In Ghana, production estimates remain around 650 kt, with exports expected to improve following government measures. In Ecuador, cumulative precipitation is above the previous cycle, with production estimated around 615 kt and exports close to the historical average.

In the medium and long term, the increased likelihood of an El Niño event beginning in the second half of the first half of the year is one of the market’s key concerns. Projections indicate that the event could extend through the end of 2026 and into early 2027, raising risks for agricultural commodities amid potential record-breaking temperatures, particularly during critical phases of the cocoa cycle, such as the development of the main 26/27 crop and the flowering that will give rise to the 26/27 mid-crop.

An analysis of previous seasons influenced by El Niño shows that there is no direct or uniform relationship between the phenomenon and rainfall volume or production, with varying responses by region, time-lagged effects, and potential impacts ranging from negative outcomes to subsequent positive adjustments, reflecting the perennial nature of the crop and its interaction with regional weather factors. In general, El Niño is associated with increased production risk, requiring continuous monitoring in the coming months.

Global Balance and Prices

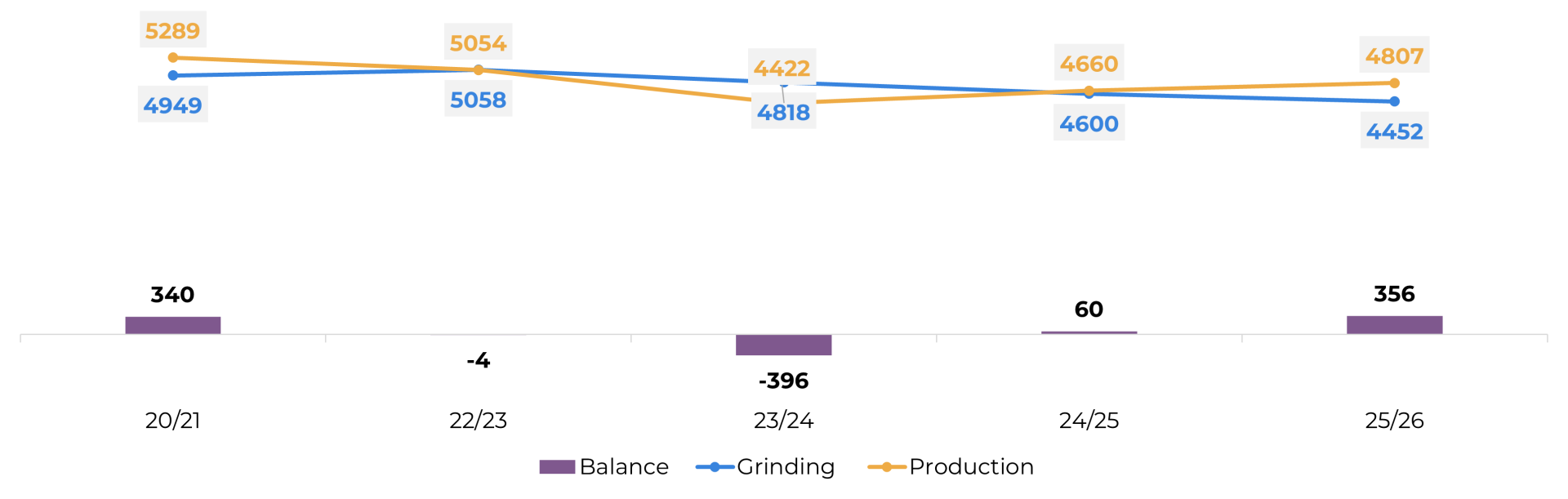

For the 2025/26 crop year, our global balance indicates an estimated surplus of approximately 356 kt, slightly lower than the previous projection. This result stems not from strong supply growth, but from a partial recovery in production combined with a decline in demand.

Global Supply and Demand for Cocoa (‘000 tons)

Source: ICCO, Hedgepoint

Despite the expected surplus, the market remains highly sensitive, as even minor changes in any of the fundamentals could significantly alter this balance. In the short term, a bearish bias prevails, with prices consolidating and significant influence from technical factors and the expiration of the nearest contracts. Still, part of the market is betting on more favorable demand data in the coming quarter, supported by a more intense price adjustment and some signs in net imports from major markets, which could influence sentiment in the medium term.

In Summary

The recent macroeconomic environment remains marked by the escalation of the conflict between the US and Iran, which has raised the global risk premium and put pressure on the energy sector, directly impacting logistics costs, freight rates, insurance, and inputs such as nitrogen fertilizers. This context reinforces inflationary risks, with a recent rise in U.S. inflation and fears of stagflation, while Europe, more sensitive to energy price fluctuations, faces the prospect of inflation above 3% in the second quarter, deteriorating consumer confidence, and a tightening of monetary policy. For the cocoa market, the effects are indirect, mainly through rising costs and greater volatility in an already fragile scenario.

On the fundamentals side, demand showed mixed behavior: Asia showed positive signs, with a recovery in grinding in Malaysia and the region, while Europe and the US recorded a decline, possibly reflecting weaker imports and a greater influx of byproducts; in Brazil, regulatory uncertainties and import restrictions put pressure on grinding. On the supply side, major producers are navigating a critical phase of the cycle in terms of the harvest calendar, with ad hoc revisions, adjustments to export flows, and a possible gradual normalization of sales in West Africa. In the medium and long term, the growing likelihood of an El Niño event increases production risks, particularly due to higher temperatures during sensitive phases of the cycle. In this context, the 25/26 global balance points to an estimated surplus around 356 kt, supported by a partial recovery in supply and a decline in demand, but the market remains sensitive, with a bearish bias in the short term and heightened attention to any changes in fundamentals.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.