A volatile week for coffee

- It was a volatile week for coffee prices. Until Wednesday (16), both Arabica and Robusta futures rose due to uncertainty surrounding the US's proposed 50% tariff on Brazilian goods. There were also reports of US roasters rushing to land Brazilian coffee in the country before the tariffs take effect.

- However, prices, especially Robustas', lost part of the support at the end of the week after Cecafé (the Brazilian Coffee Exporters Council) announced advanced trade talks with the U.S. government. It's also worth remembering that Robusta has greater availability due to a large crop in Brazil, and higher availability on Uganda and Indonesia.

- As Brazil remains the largest supplier of coffee to US, market volatility is expected to persist - at least until more concrete discussions surrounding tariffs take place

- Trade in Brazil continues to be sluggishly given current uncertainties, with farmer selling below average levels. Exports are also reflecting the lower farmer selling, as both Arabica and Robusta shipments are below previous season levels.

A volatile week for coffee

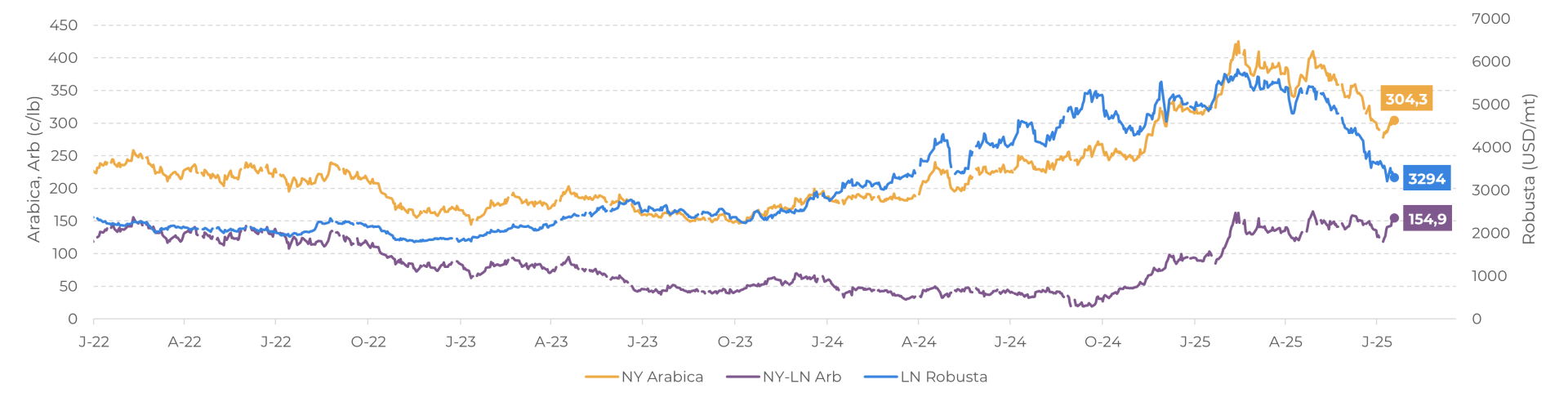

LN Robusta (USD/mt), Arabica and Arbitrage (c/lb)

Source: LSEG

This movement also reflected in rising Arabica futures in the past days, as Brazil has a larger availability of Arabica at the current time. With most other producers in their off-season, Brazil has taken a leading role in supply, pushing the September contract closer to the 310 c/lb level on Wednesday and Thursday.

Robusta futures rallied 8.8% on Monday, but prices lost support by the end of the week due to greater availability of the variety. This occurred after Marcos Matos, the chief executive of Cecafé, stated that the group is not considering a coffee supply break to the US. The Brazilian government and sector are also addressing the issue, with coffee taking center stage in ongoing talks about US tariffs.

Separately, since April, the National Coffee Association (NCA) of the US has been in talks with representatives of Trump’s administration. The goal is to include Brazilian coffee on the list of strategic products, which would exempt it from new tariffs. However, no agreements have been reached thus far.

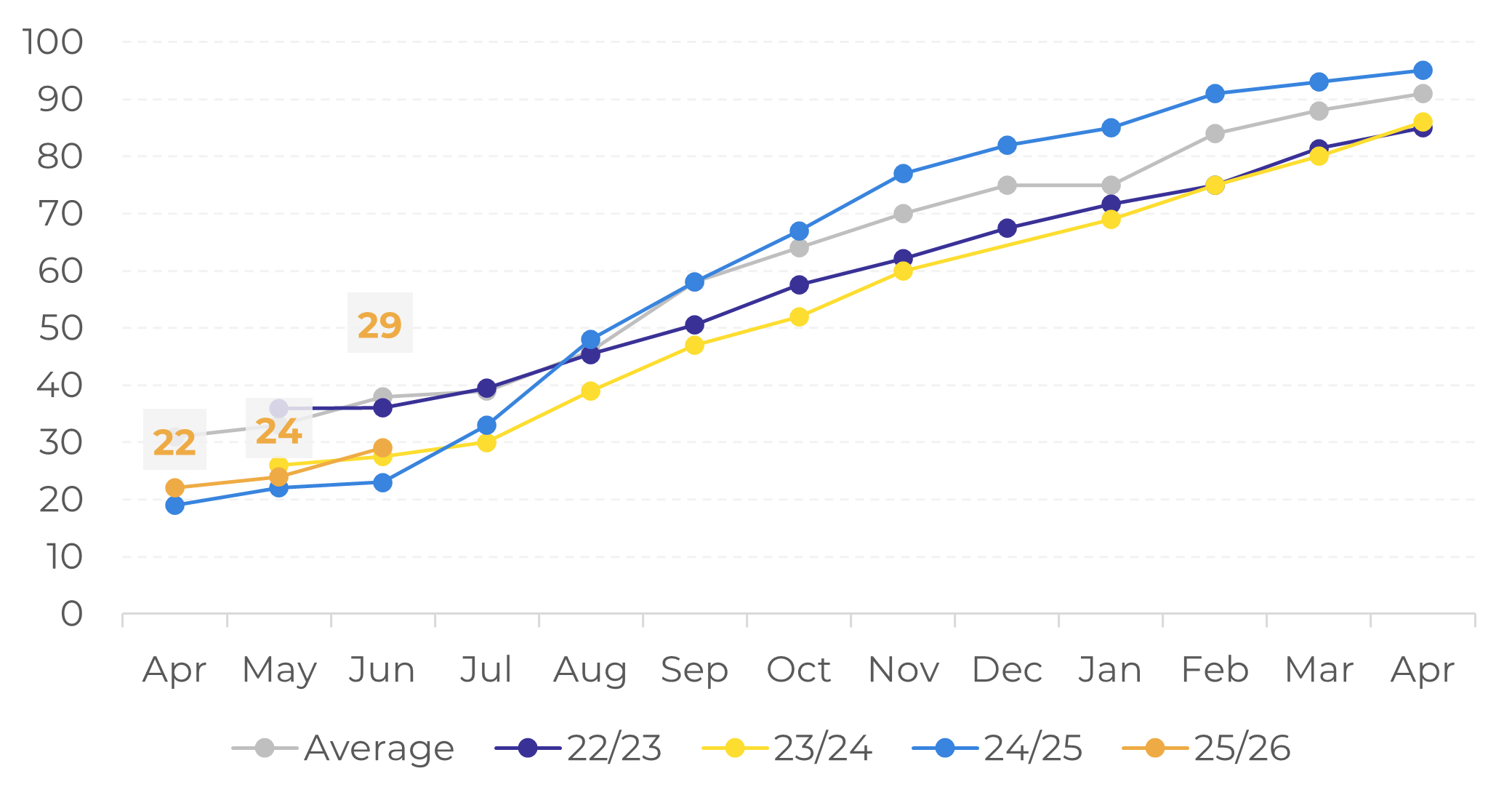

Brazil: Arabica Farmer Selling (% of total)

Source: Safras & Mercado

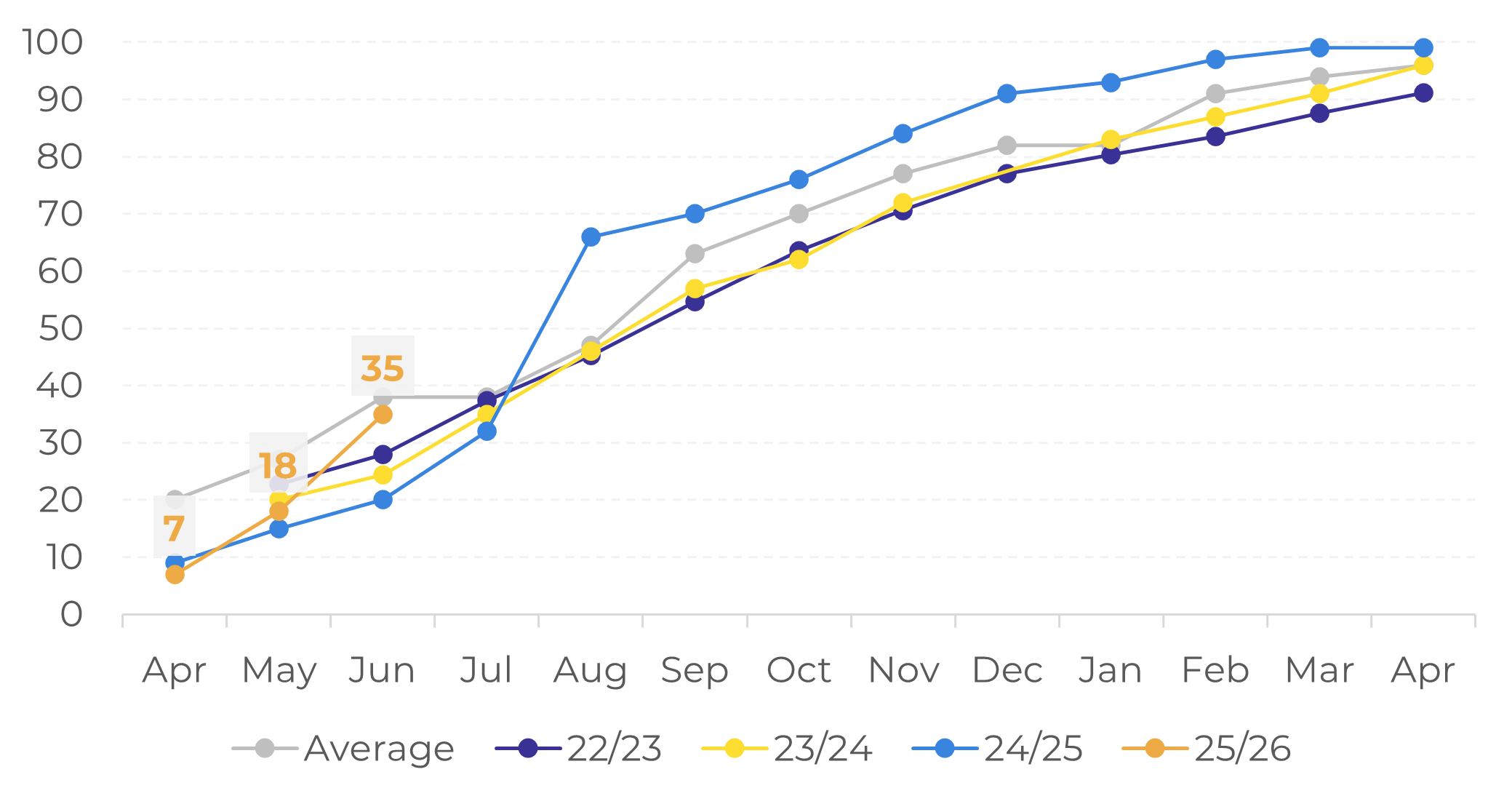

Brazil: Conilon/Robusta Farmer Selling (% of total)

Source: Safras & Mercado

Although there are no immediate weather risks and 77% of Brazil’s coffee harvest has already been completed, the ongoing uncertainty surrounding US tariffs and trade flows is likely to maintain market volatility. The current scenario is also slowing trade in Brazil. Many farmers have chosen to stay out of the market in recent months following a drop in prices driven by harvest-related supply pressure, leading to lower-than-average farmer sales. As of June, Arabica sales stood at 29%, while Robusta’s, at 35%, both below the average of 38% for the period. With new concerns emerging around trade policy, sluggish market conditions may continue.

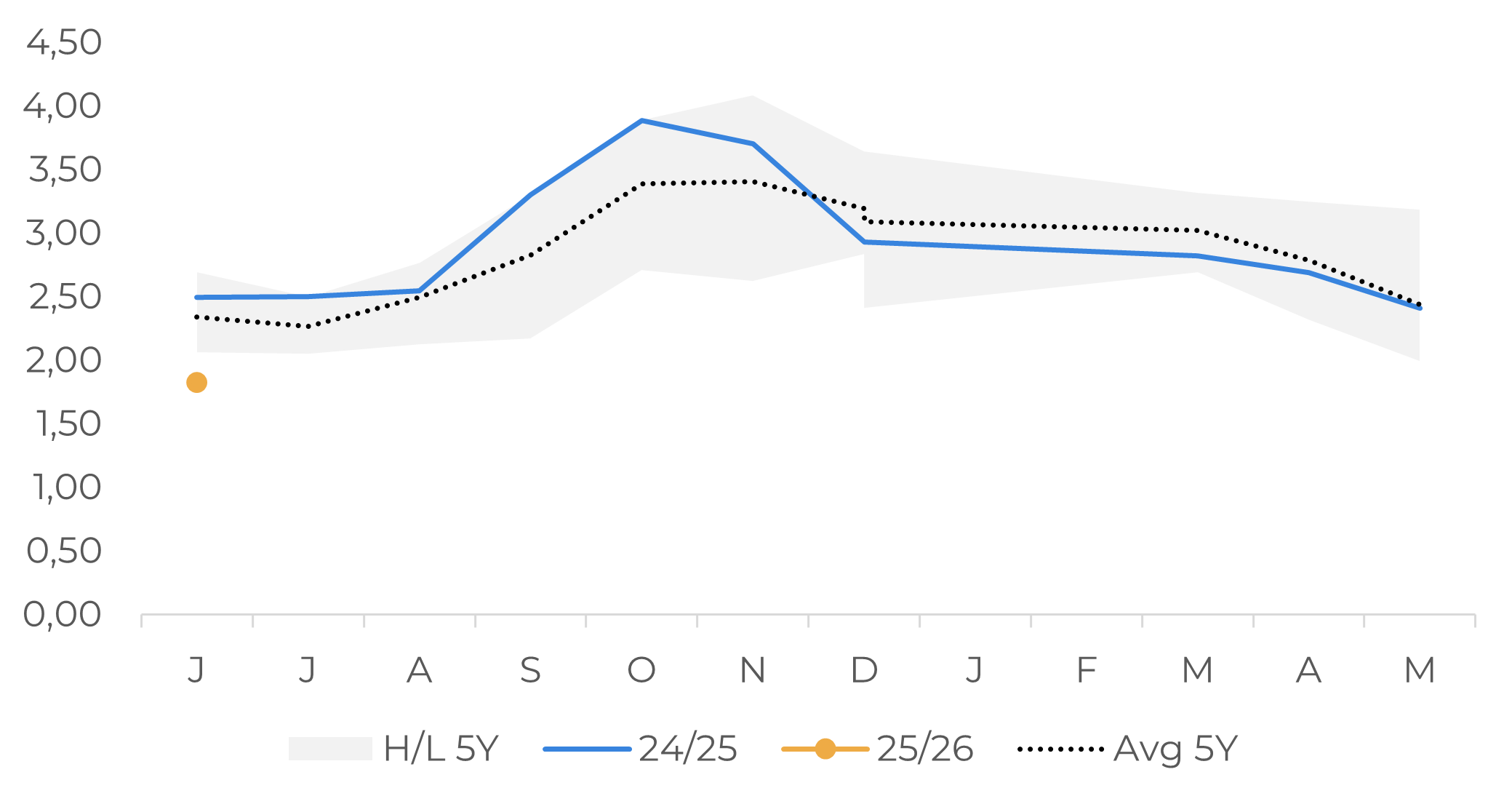

Lower farmer selling was also reflected in Brazil’s shipments. Arabica exports in June reached only 1.8 million bags, which is 26.9% less than in the same period in 2024 and below the five-year average. While the 476.3 thousand bags of Robusta shipped in June were above average, exports remained 42.2% lower year-over-year.

Brazil: Arabica Green Exports (M bags)

Source: Cecafé

Brazil: Conilon/Robusta Green Exports (M bags)

Source: Cecafé

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

thais.italiani@hedgepointglobal.com