Coffee Market Call Highlights

US new tariffs could bring inflationary pressure

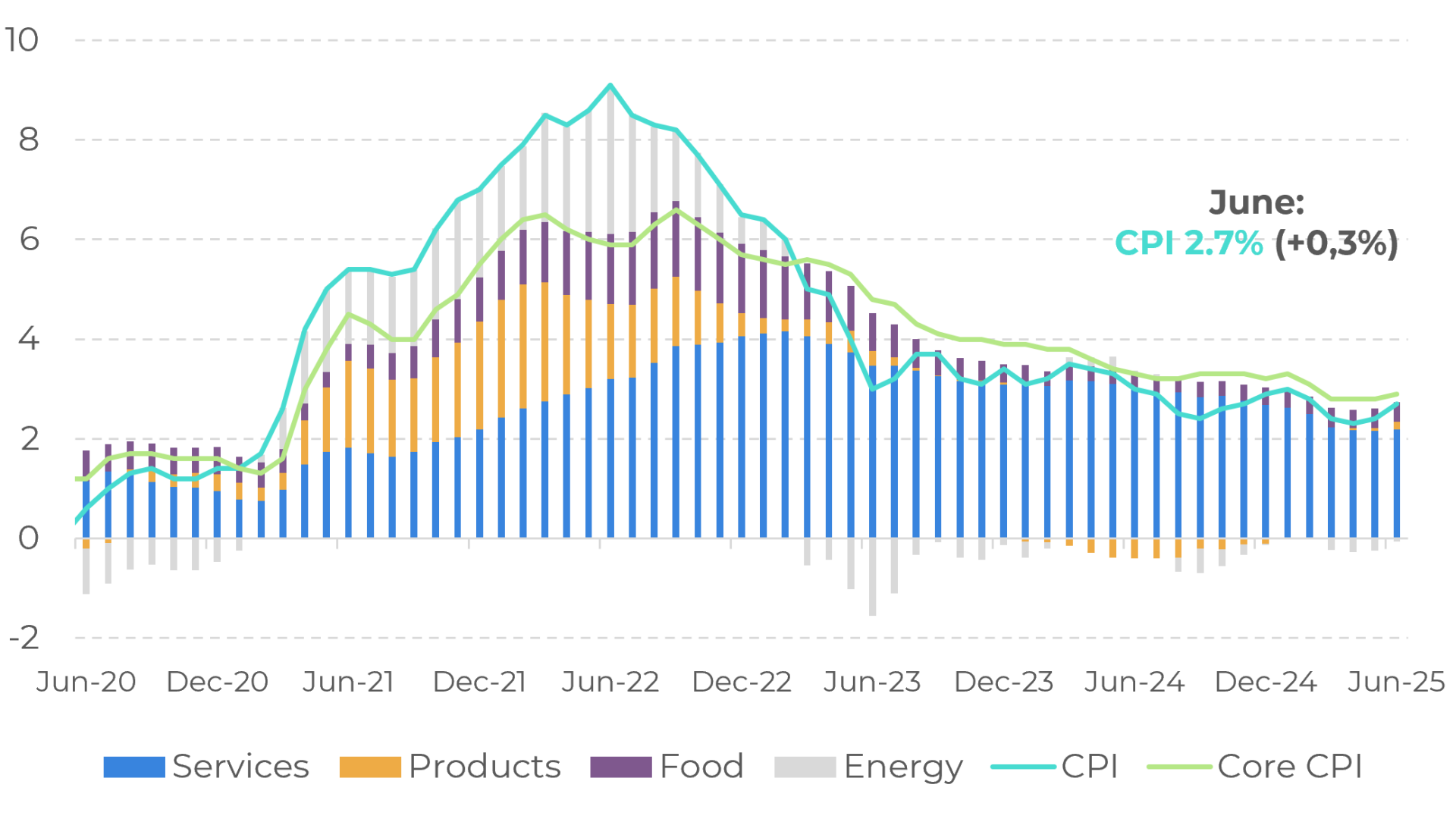

US Consumer Price Index (YoY %)

Source: US Buerau of Labor Statistics, Bloomberg

Although in line with expectations, the CPI increased by 0.3% in June, bringing the 12-month inflation rate to 2.7%, above the Fed's 2% target. Some analysts point out that part of the movement was due to the effect of tariffs, and they expect further growth in the coming months. Last Friday (01) update on US nonfarm payroll data also worried the market, as not only were July figures below market expectation, but June and May figures were also revised down.

A weakening US economy could put pressure on Trump’s trade policy and influence future Fed decisions. If the tariffs on coffee indeed come into effect, they could hamper demand.

US Payrolls (‘000 positions)

Source: US Buerau of Labor Statistics,; LSEG

US coffee imports were on recovery, but tariffs could change the scenario

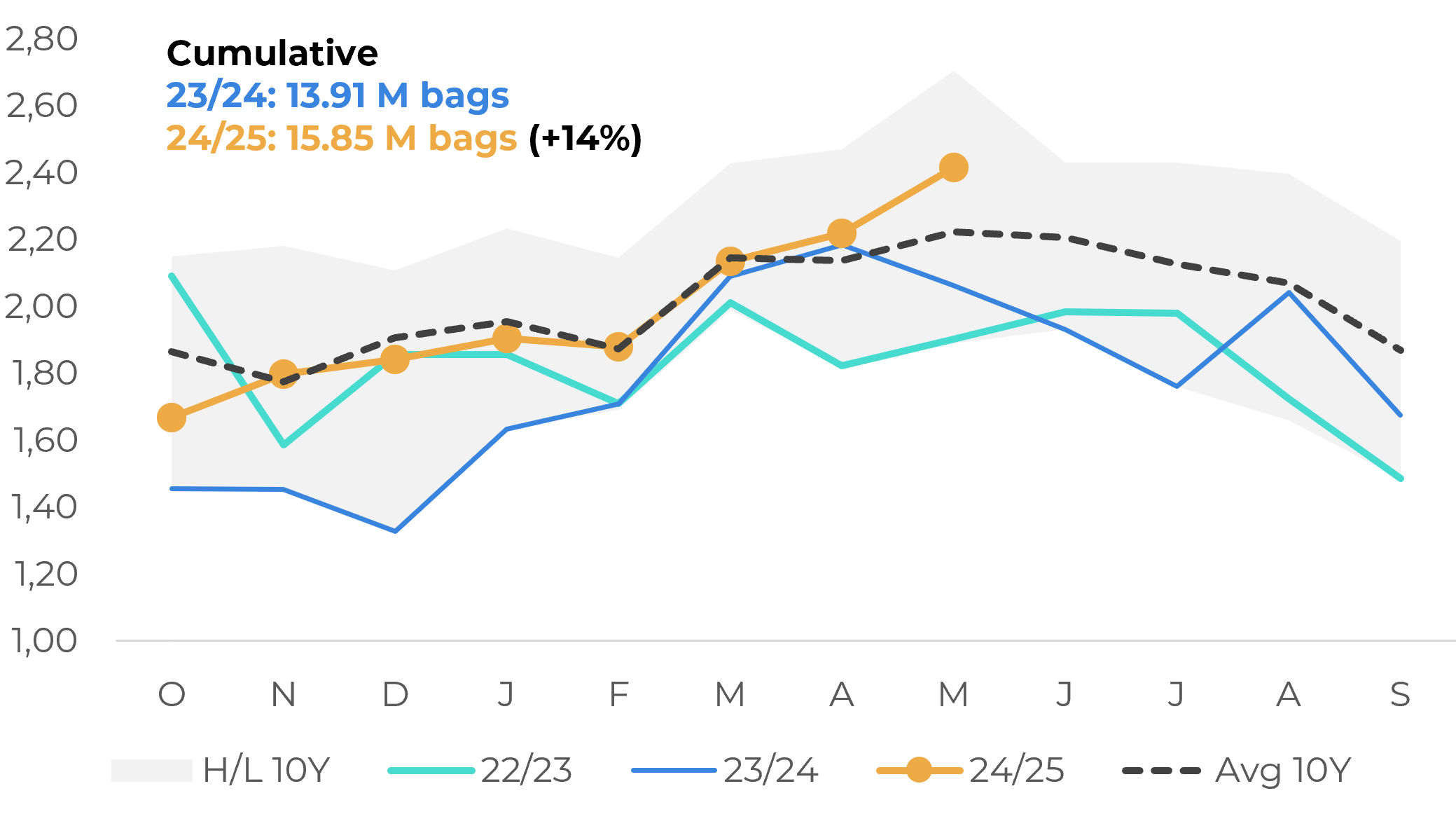

US: Coffee Net Imports (M bags)

Source: US. International Trade Commission, Hedgepoint

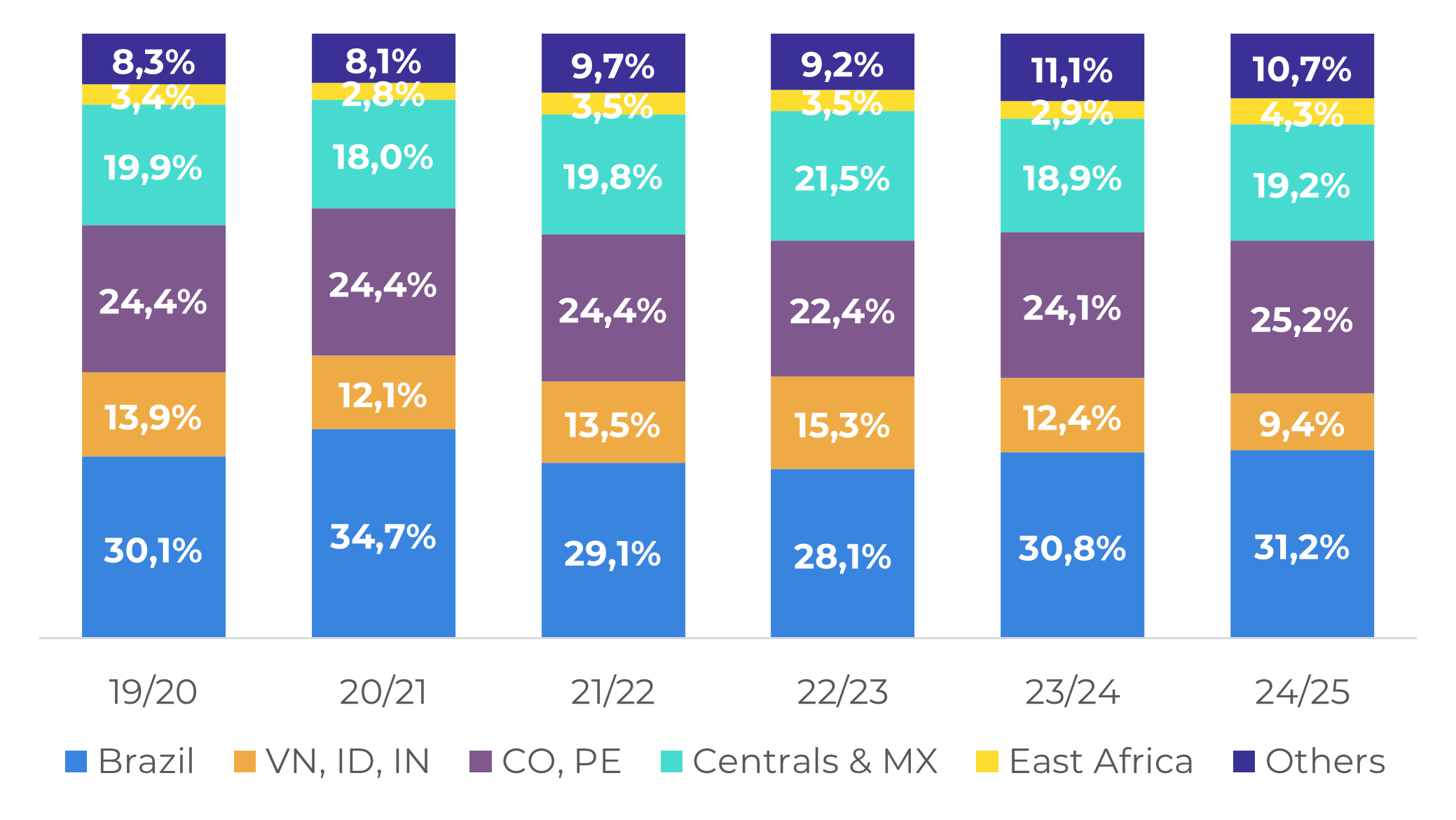

As mentioned before, Brazilian beans account for around 30% of all US coffee imports, so a 50% tariff would further increase prices, which are already at record levels, and could potentially harm demand. Although US importers could source coffee from other countries, Brazil currently has the highest availability (especially of Arabica), and as the largest producer, the US will likely need to rely on Brazil's production to meet its current demand.

US: Coffee Imports by Region/Country (% of total)

Source: US. International Trade Commission, Hedgepoint

Brazil’s 25/26 harvest is in its final stage

Despite the end of the harvest, sales in the physical market continue to be sluggish, with higher coffee availability. Many farmers have chosen to stay out of the market in recent months due to a price drop driven by harvest-related supply pressure. This has led to lower-than-average sales by farmers. With new concerns emerging around US’ trade policy, these conditions may persist.

Arabica Differentials (c/lb)

Source: LSEG, Safras & Mercado

Weather should be monitored closely in other origins

Most of the other coffee-producing countries are now on their development period for the 25/26 season. In Asia, Vietnam is expected to have a recovery in production, given higher investments and positive weather conditions, despite a drier July. Production in Central American countries are also expected to be similar or slightly higher than in 24/25, due to better weather prospects, with an ENSO-neutral scenario. However, we could further decrease Colombia production, given excessive rainfall during the flowering period.

Global Balance and Price Behavior

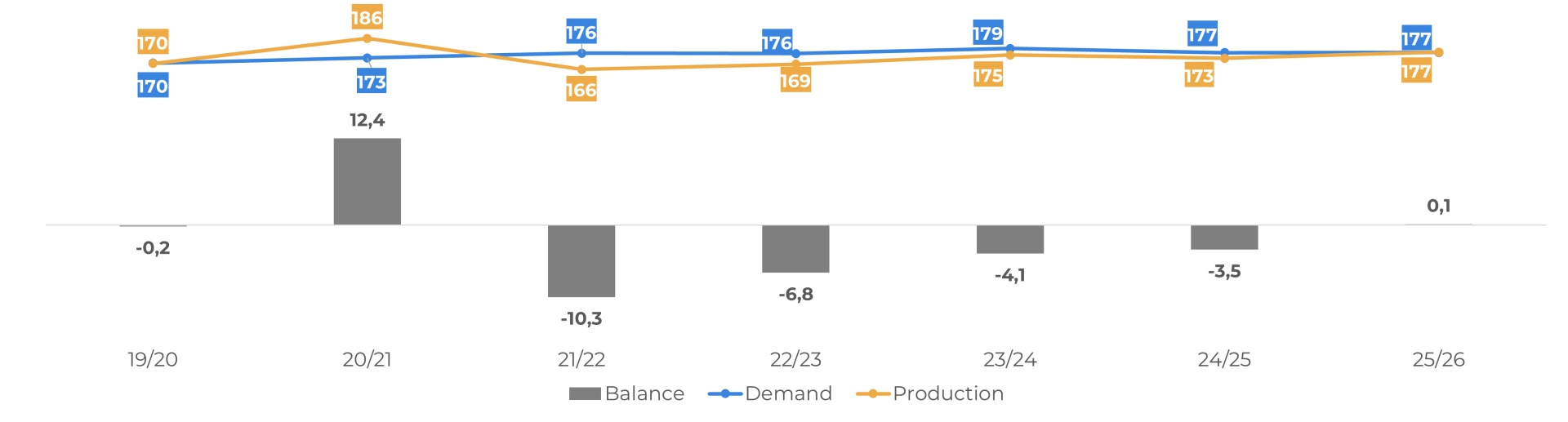

Global Supply and Demand for Coffee (M bags)

Source: Hedgepoint

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

livea.coda@hedgepointglobal.com