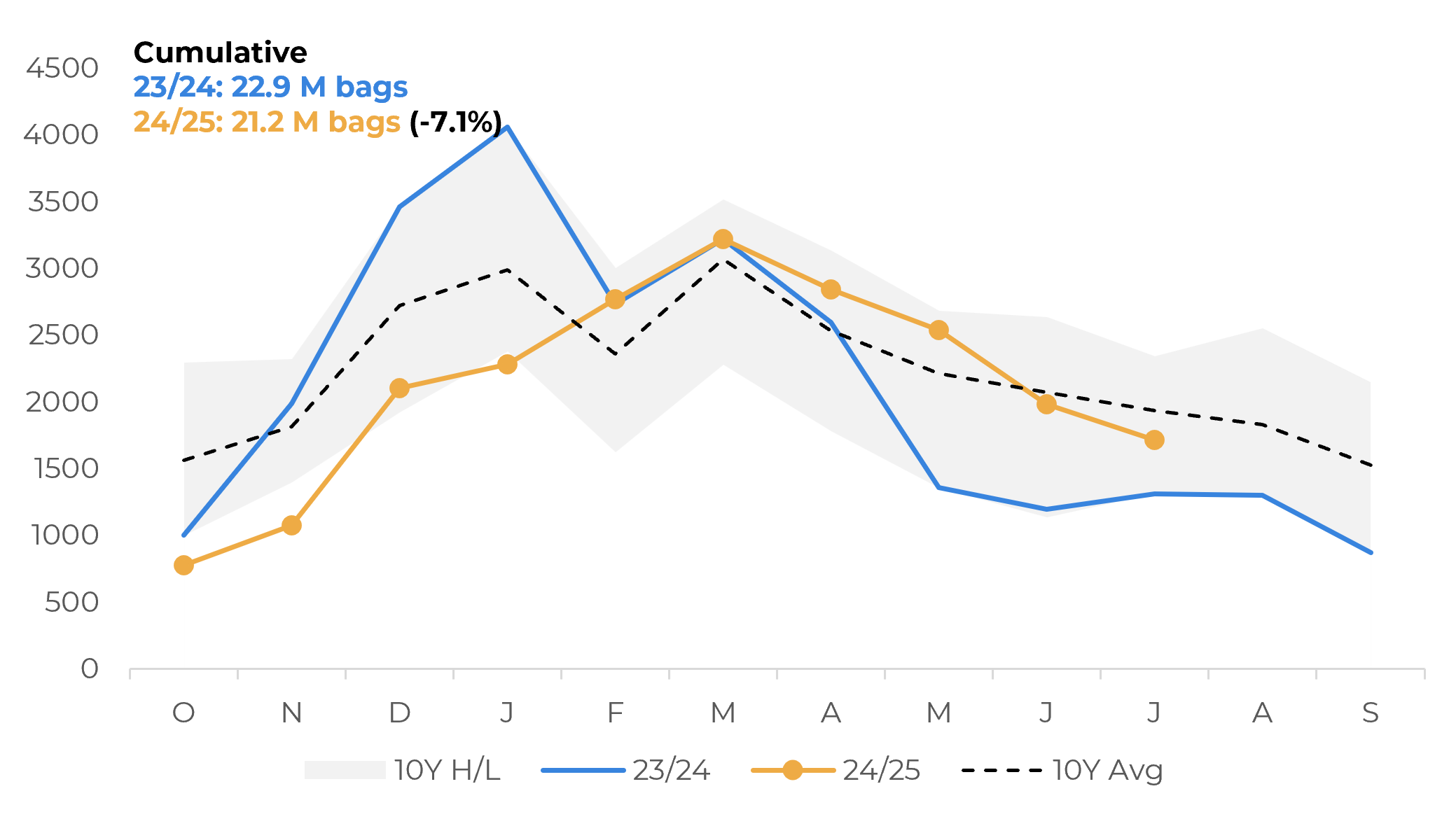

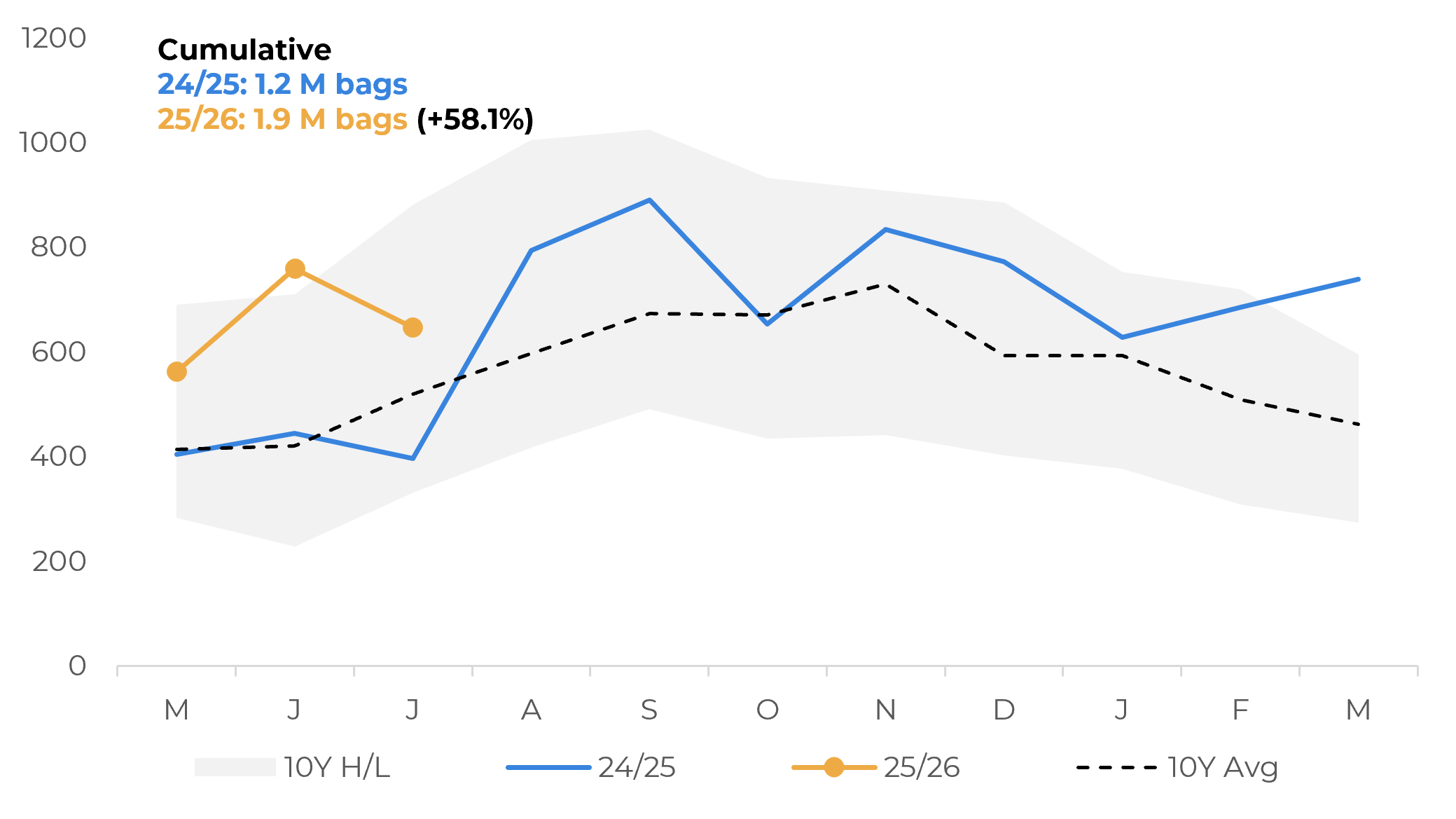

Vietnam and Indonesia exports rise in 2025, but trade slow down

- Vietnam and Indonesia exports rose in the first half of 2025. For Vietnam, the volume was slightly below the 10-year average in some months, but still higher than the same period of 2024. In Indonesia, exports kept a strong performance, with shipments above 24/25 and the 10 –year average levels.

- Exports were mainly favored by the lack of Brazilian offer, as sales of the Latin American country remain sluggishly, and more competitive Asian differentials in the past moths. In the case of Indonesia, a higher production in 25/26 also favored shipments.

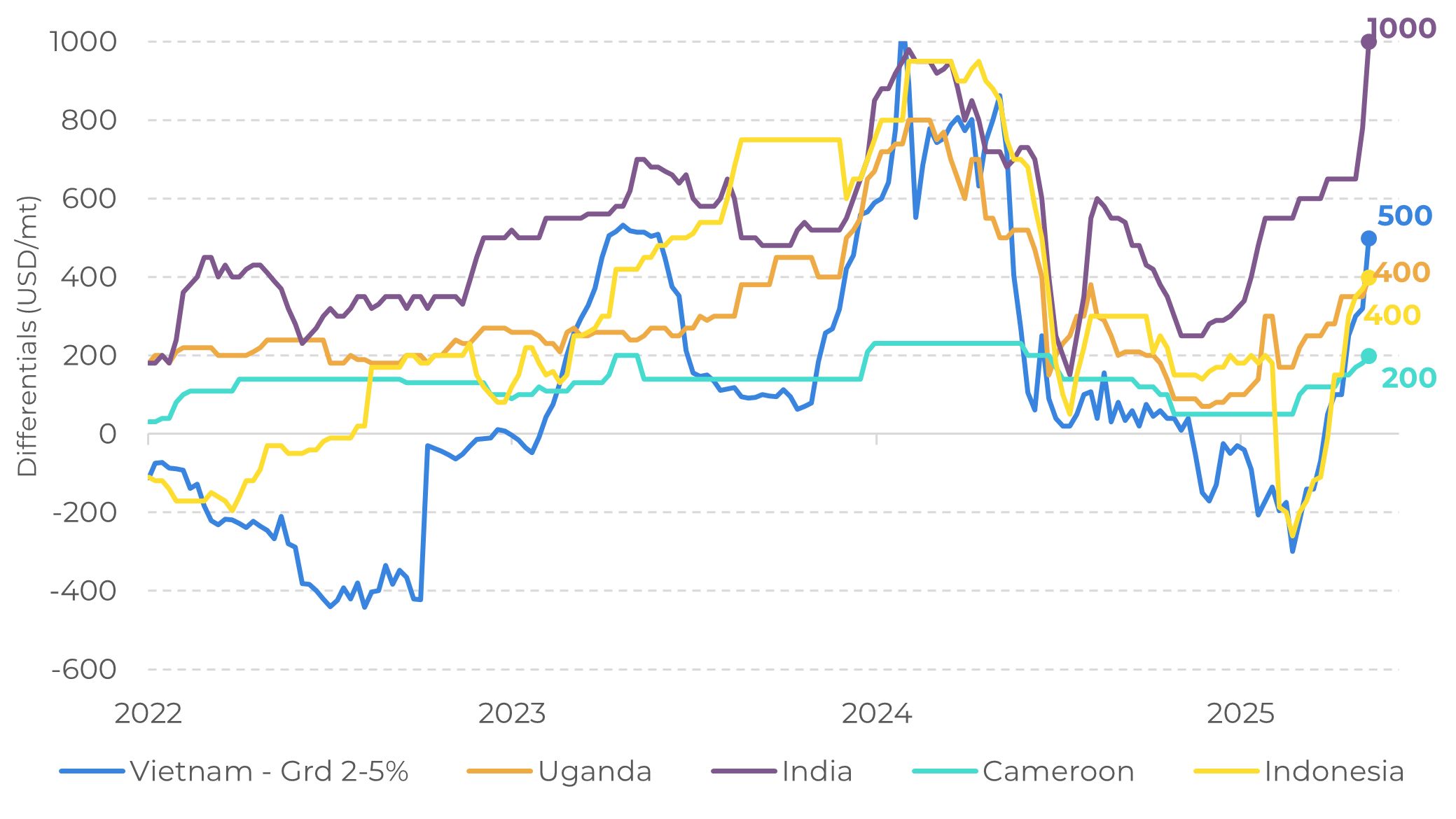

- However, according to some market reports, trade in Asia is now muted due to lower stocks and weaker demand. Vietnamese and Indonesia differentials have remained supported in recent days.

- Market also continues to monitor the development of Brazil-US relations. As the 50% tariff takes effect in Brazilian coffee shipments starting this week, trade between the two countries has halted, boosting future prices.

Vietnam and Indonesia exports rise in 2025, but trade slow down

Vietnam: Coffee Exports (000’ bags)

Source: LSEG, ICO

Indonesia: Coffee Exports (000’ bags)

Source: LSEG, ICO

In Indonesia, farmers have already sold a significant portion of their 25/26 inventory and are waiting for higher prices before selling the remainder, also supporting differentials. The country has also experienced intense rainfall in recent weeks. Although no major losses were reported, the rains disrupted the end of the harvest and slowed trade. Conversely, reports of a decrease in demand for Asian coffees have also emerged. This could reflect both the recent changes in differentials and the expectation of increased Brazilian Conilon availability in the second half of the year, as Brazil's 25/26 harvest is nearly finished.

The global market has also been paying close attention to Brazil-US relations. With the 50% tariff on Brazilian coffee taking effect this week, trade between the two countries has reportedly halted. While coffee loaded in Brazil before the August 6 tariff deadline is expected to enter the U.S. without paying the tariff if it arrives by October 6, new trades are unlikely to occur between the two countries in the short term.

This has supported prices, especially Arabica's. In this sense, the September contract surpassed 300 cents per pound this Friday. A cold front reaching Brazil in the coming days also supported the futures. Prices are likely to remain volatile in the coming months due to uncertainties regarding the medium- and long-term impacts on the global coffee supply chain.

Robusta Differentials (USD/mt)

Source: LSEG

Vietnam: Cumulative Precipitation in Central Highlands (mm)

Source: Gadas/CPC

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.