A volatile month for coffee: Arabica and Robusta hit 3-month highs in August

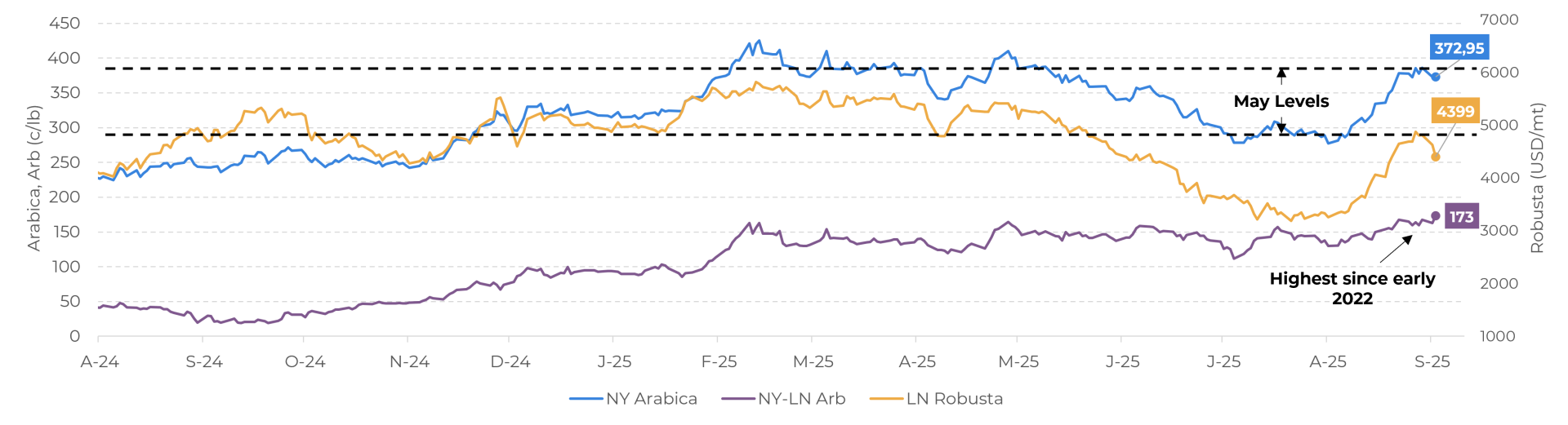

- Coffee market remained highly volatile in August, with significant fluctuations in Arabica and Robusta futures prices after the first week of the month. Nearest-term contracts for both varieties reached a three-month high in recent days, approaching levels seen in early May.

- Prices have not only been supported by fundamentals, but by speculative buying, specially after the drop in arabica certified stocks in August, as US roasters are trying to secure supply after the 50% tariff on Brazilian beans. The CFTC report from Friday, August 29, showed a light increase in funs long positioning in August.

- A lower 25/26 Arabica crop in Brazil, and the development of the 26/27 season in the country and the 25/26 season in Vietnam also continue to bring volatility to prices.

- In Vietnam, Typhoon Kajiki contributed to overall market instability in recent days. However, no impact was recorded in coffee-producing areas, which are currently in the final development stage of the 25/26 season.

- In Brazil, the 26/27 season is in its development phase, with heightened attention on weather conditions. Unfavorable climatic developments pose a potential risk to the Arabica crop, which has already faced challenges in recent years. Brazilian farmers also continue holding back on sales as they wait for the major blooms of the 26/27 season.

A volatile month for coffee: Arabica and Robusta hit 3-month highs in August

LN-Robusta (USD/mt), NY-Arabica and Arbitrage (c/lb)

Source: LSEG

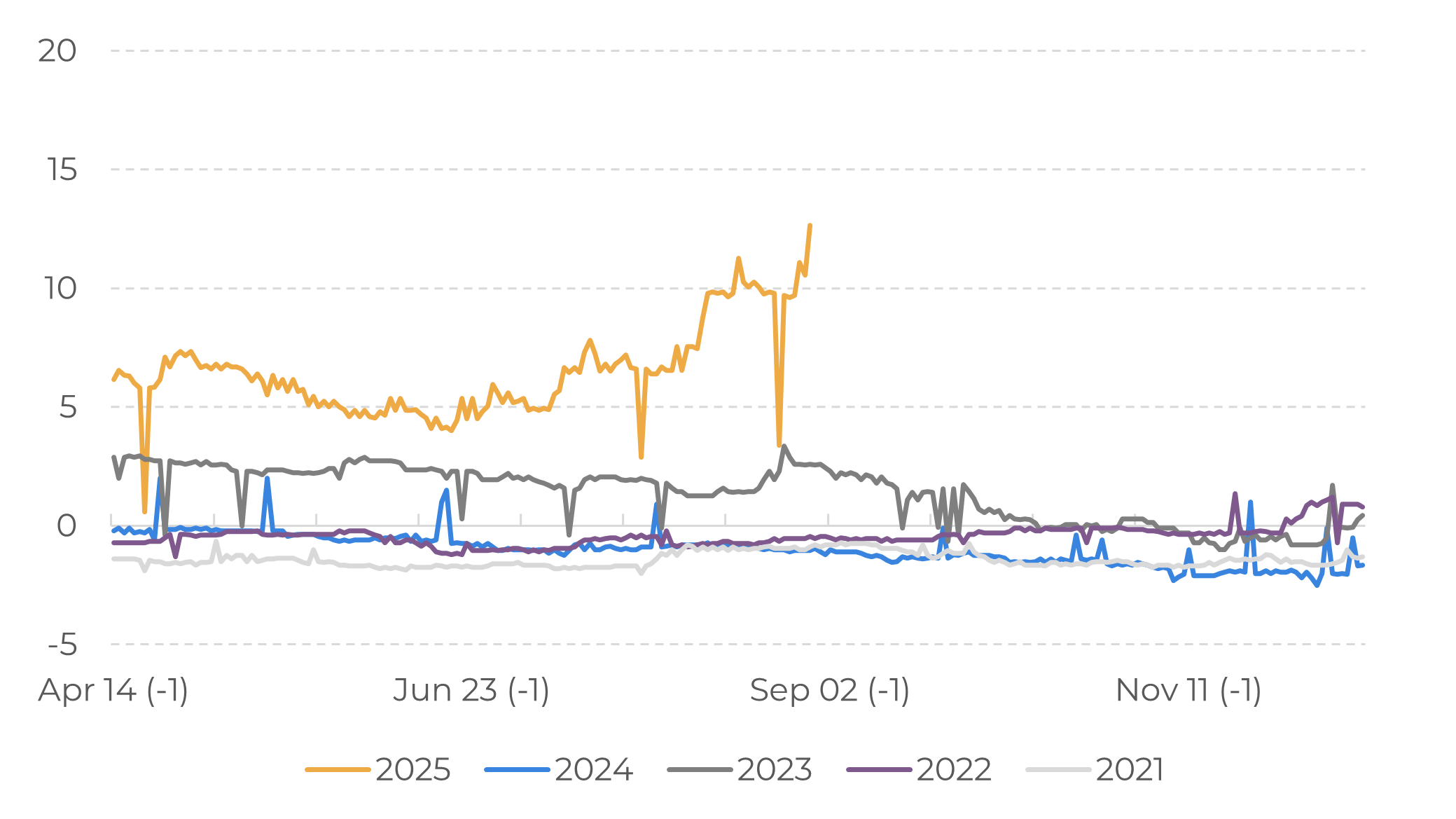

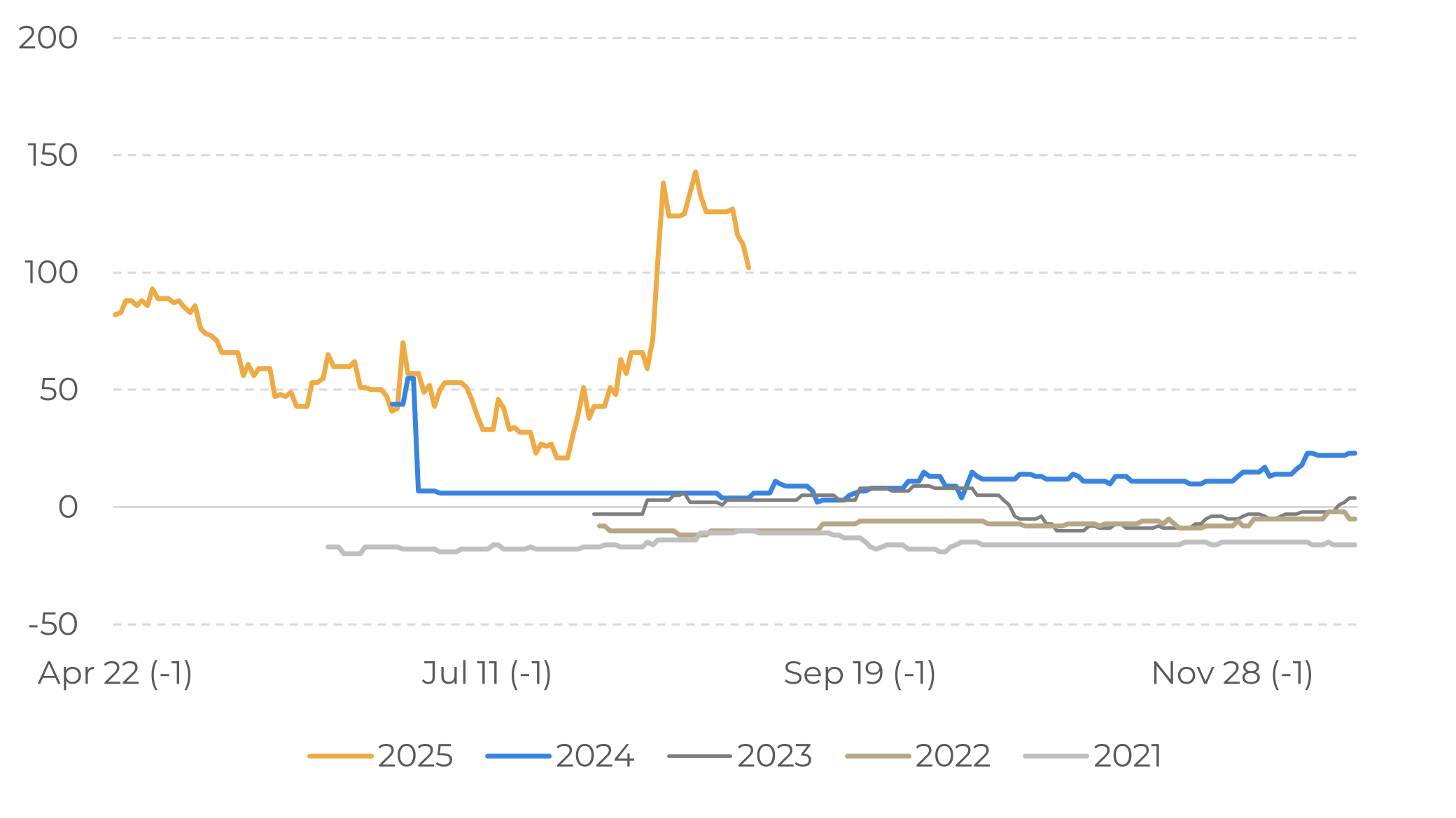

Reflecting these concerns, the spread for near-term Arabica contracts has increased, particularly for the December/25 vs. March/26 contracts. The Robusta November/25 and January/26 spread also increased in August, despite a setback last week, reflecting near-term supply concerns. Despite the large production of this variety in Brazil and in Indonesia in the 25/26 season, Brazilian farmers still remain distant from the market, redirecting more sales to the domestic industry. Meanwhile, supplies in Indonesia are scarcer than at the beginning of the season.

Arabica: December/25 and March/26 spread (c/lb)

Source: LSEG

Robusta: November/25 and January/26 spread (USD/mt)

Source: LSEG

Meanwhile, the availability of Vietnam's Robusta remains low. In a recent development, some traders have been looking for Brazilian and Indonesian beans to fulfill their contracts. At the end of August, Typhoon Kajiki also hit the country. While the typhoon hopefully did not damage coffee-growing regions, it contributed to market instability last month as Vietnam is currently in the 25/26 season development phase. Additionally, demand for Robusta could increase in the coming months due to current arbitrage levels and fears of an Arabica shortage. As previously mentioned, Arabica certified stock has dropped amid a lack of selling interest from Brazilian farmers while most other origins are in their off-season.

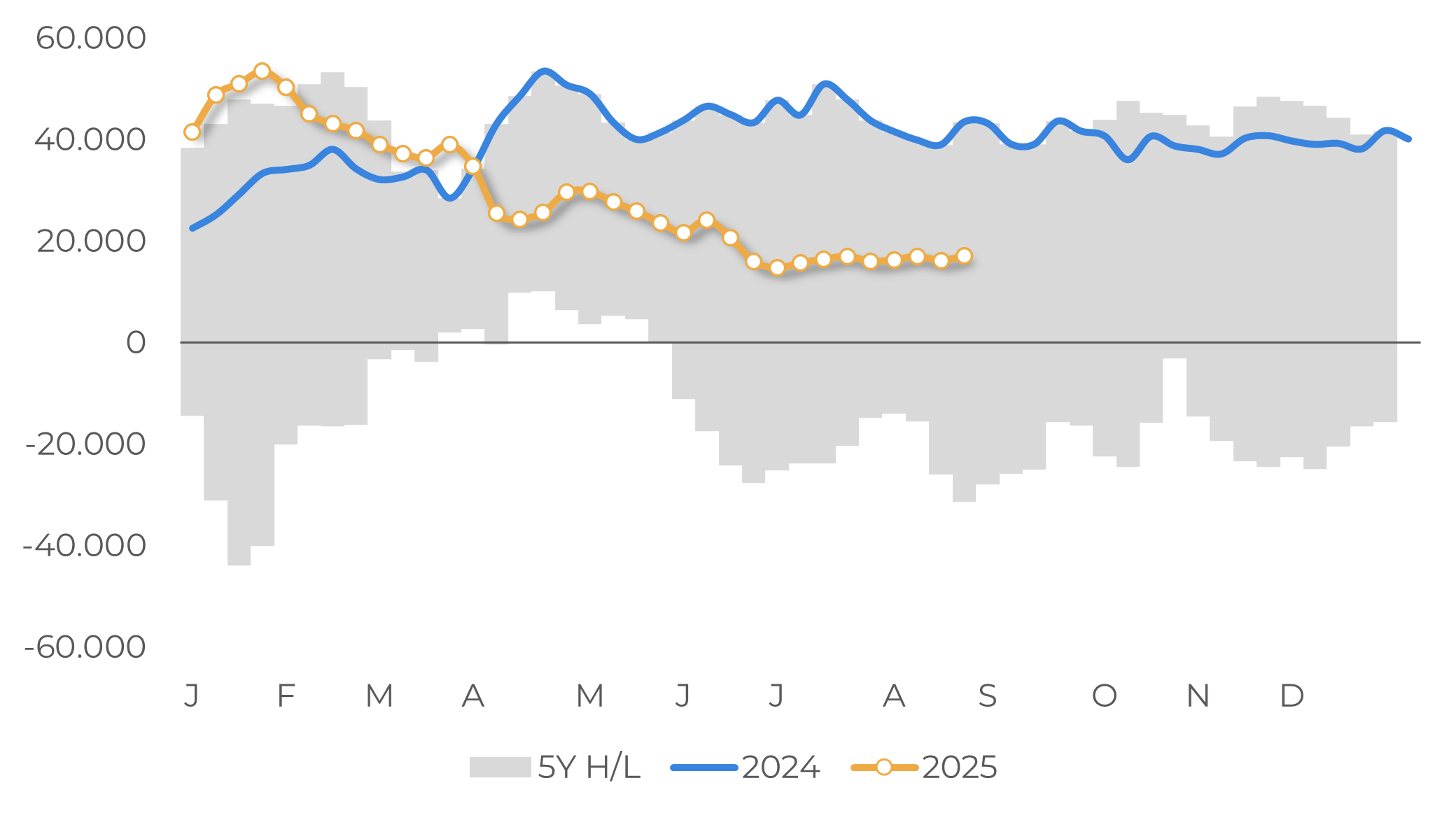

These fundamentals also prompted speculative buying last week. Arabica funds increased their net long positions, and Robusta speculative funds went from net short to net long positions in the latest COT report, which also contributed to the price hike. As we head into the development of the 26/27 season in Brazil, we may see more activity from funds in the coming weeks depending on the country's weather forecast, as unfavorable climatic developments pose a potential risk to the 26/27 cycle.

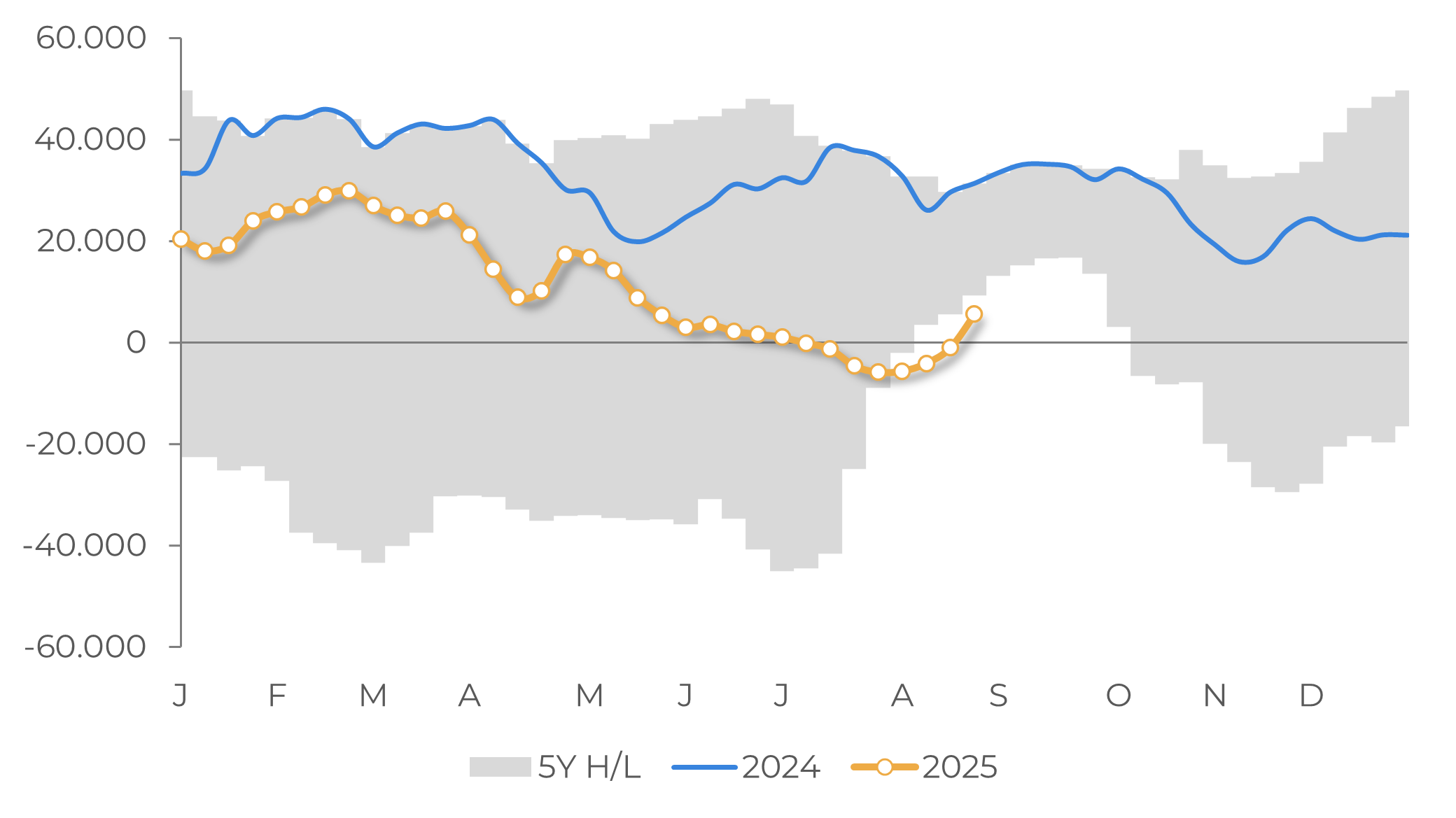

CFTC: Arabica Speculative Net Funds Position (lots)

Source: CFTC

ICE: Robusta Speculative Net Funds Position (lots)

Source: ICE

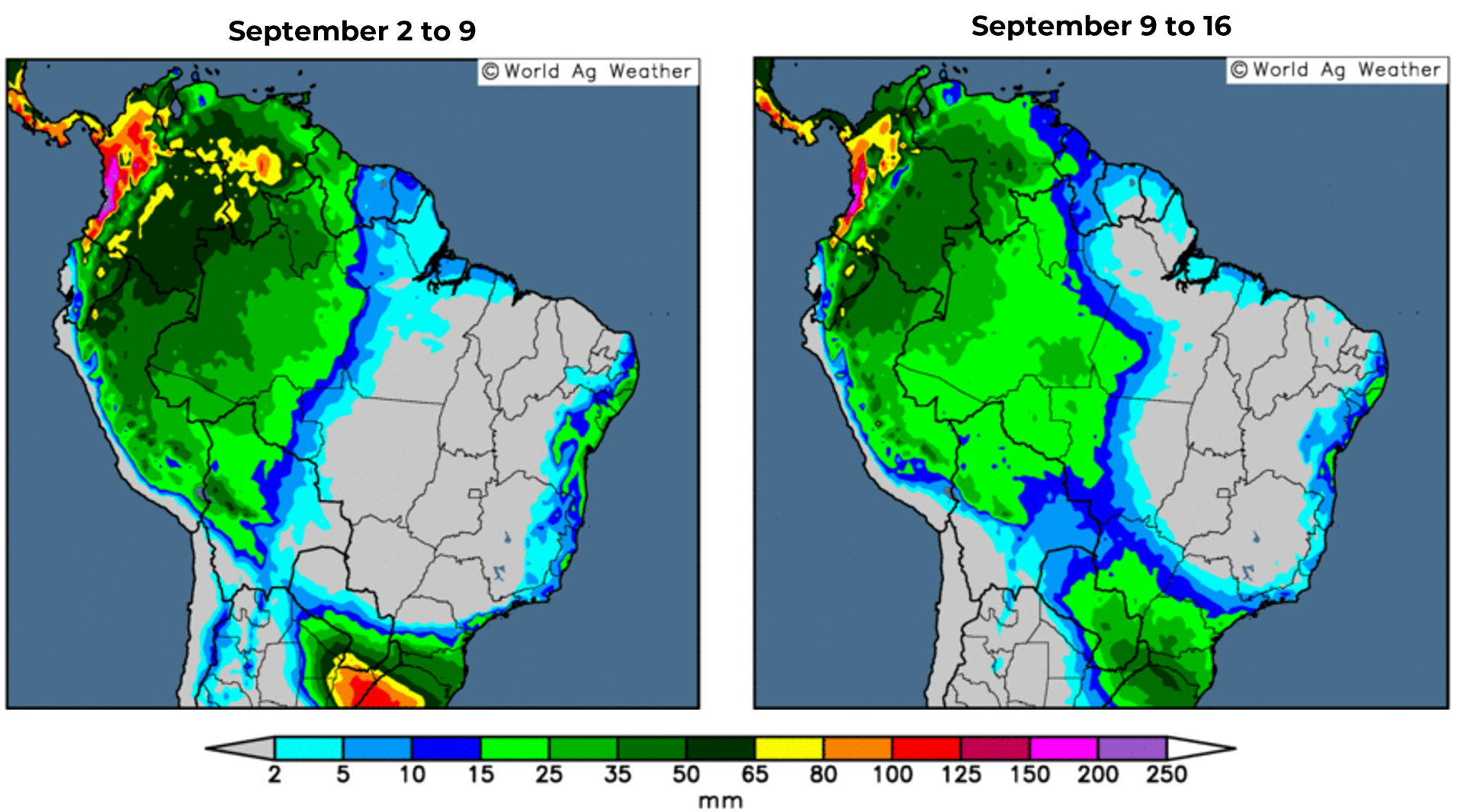

Over the next two weeks, dry conditions with below-average rainfall are expected in most Arabica coffee-producing regions in Brazil. Currently, a larger volume of rain is necessary to induce major blooms in Arabica areas for the 26/27 season. In Conilon areas, rainfall was recorded in Espírito Santo, and favorable weather is forecasted for the coming weeks. Higher rainfall in these regions will promote new blooms and is essential for setting flowers that have already opened.

Brazil Weather forecast for next 14 days – European Model (mm)

Source: World AG Weather

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

luiz.silverio@hedgepointglobal.com