September Coffee Market Call Highlights

This analysis summarizes the main points discussed in the Coffee Market Call on September 25. The main topics discussed were:

- US tariffs: impacts and perspectives for coffee;

- Imports in other destinations;

- Brazil’s 25/26 crop update and 26/27 outlook

- Weather continues to be monitored in other origins

- Global balance and perspectives.

US tariffs: impacts and perspectives for coffee

Tariffs have not only impacted the

coffee sector, but US economy in general, leading to a persistent inflation In

the country, which, together with current weaker US job market, led to Fed

first rate cut of the year in September. With this the target range for its

main lending rate at 4% - 4.25%. Fed officials also indicated the possibility

of two more quarter-point rate cuts this year. The perception rising risk and

instability in the US economy and the decrease of interest rate led to a

weakness in the dollar in 2026. In Brazil, this movement was reinforced by the

increase in the interest rate differential between Brazil and the US.

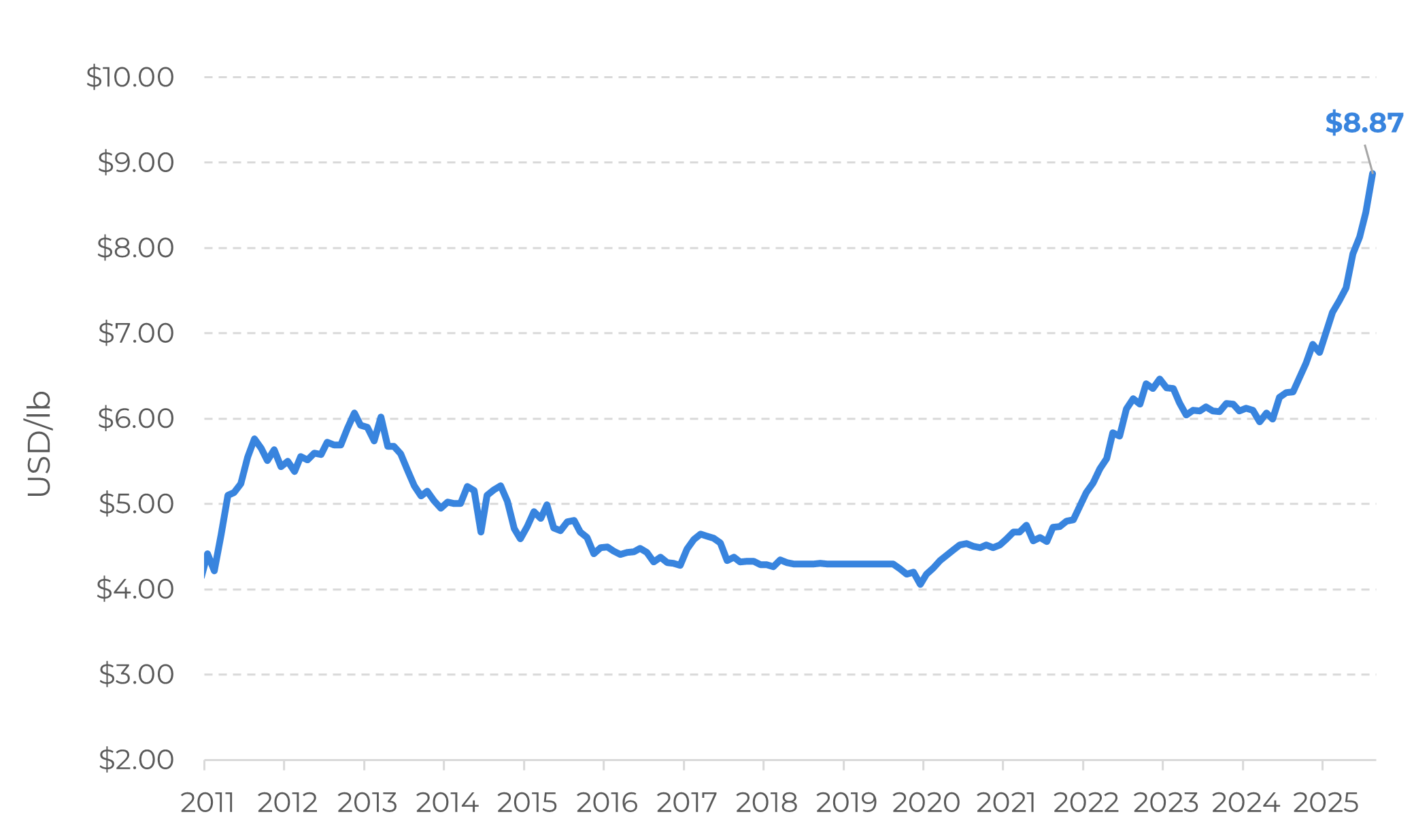

US: Coffee Retail Price (USD/lb)

Source: US Buerau of Labor Statistics

Specific for the coffee market, tariffs have also already changed some aspects, such as US trade flows and stocks, beyond its effect in prices volatility. Although the current meeting between Trump and Lula this week is bringing hope for a possible end to the US tariffs on Brazilian beans, the effects of tariffs are still reflecting in the market.

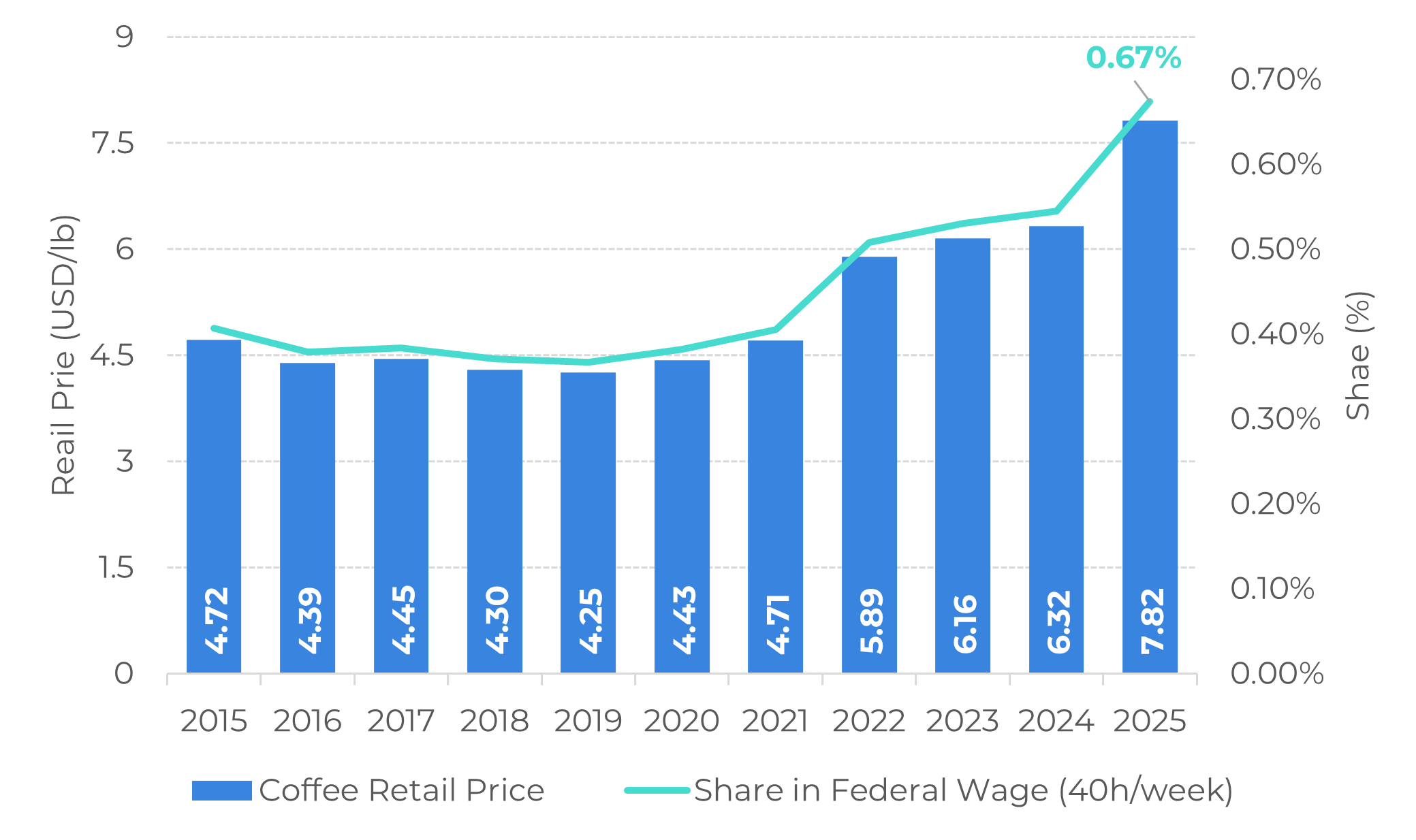

Since the end of 2024, US retail prices have increased, a trend felt globally, but the decreased of US stocks and tariffs are likely to lead to further hikes. Although coffee represents a small portion of wages (based on the federal minimum wage with a 40-hour workweek), given the scenario of higher American inflation and a cooler jobs market, a possible drop in demand, or at least a change in consumer habits, is not out of the picture.

US: Coffee Retail Price (USD/lb) and Minimum Wage vs. Coffee Price Ratio (%)

Source: US Buerau of Labor Statistics

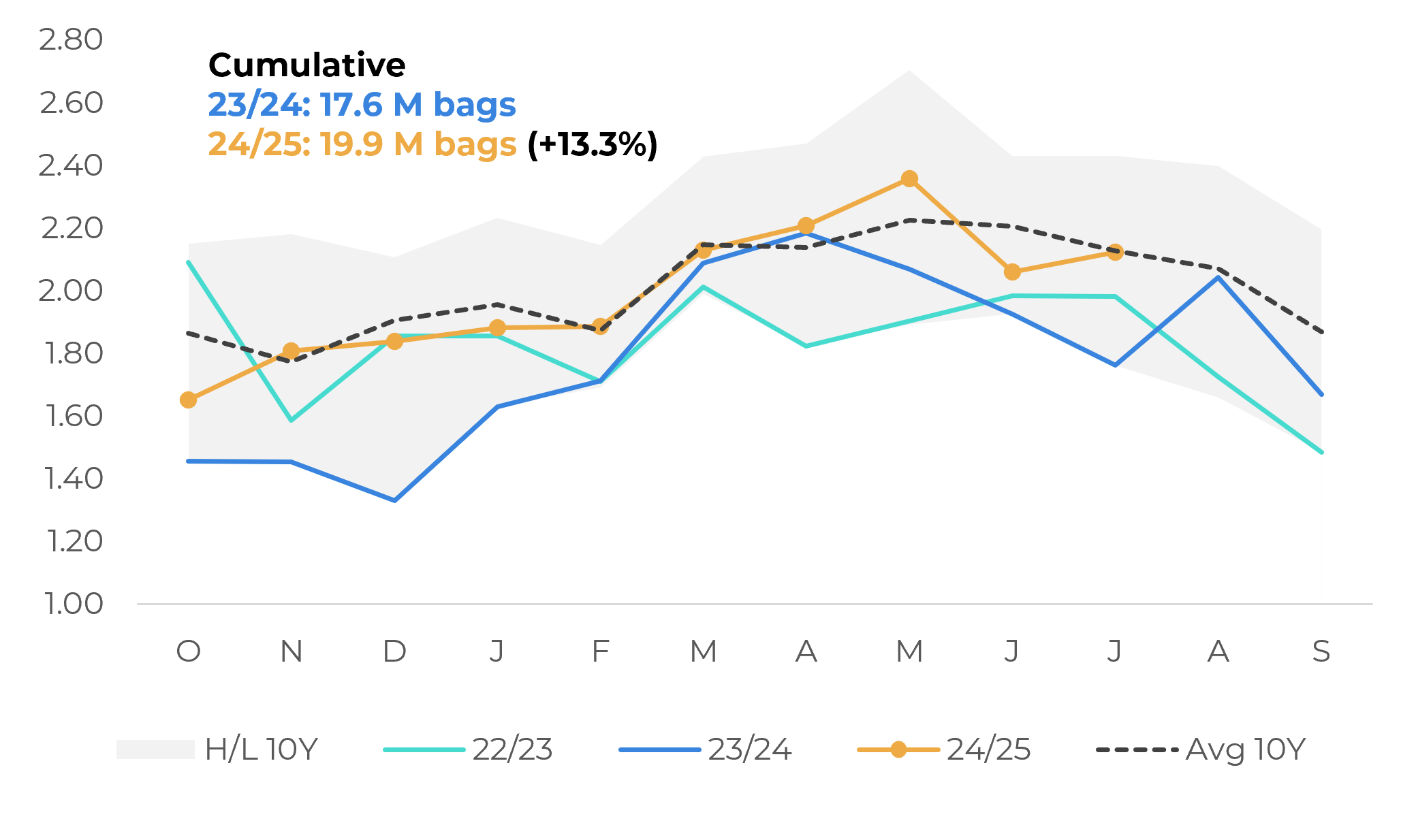

There is also the expectation of US

imports to decrease from August on. While cumulative figures in 24/25 are

higher than 22/23 and 23/24, there could be a drop after tariffs were

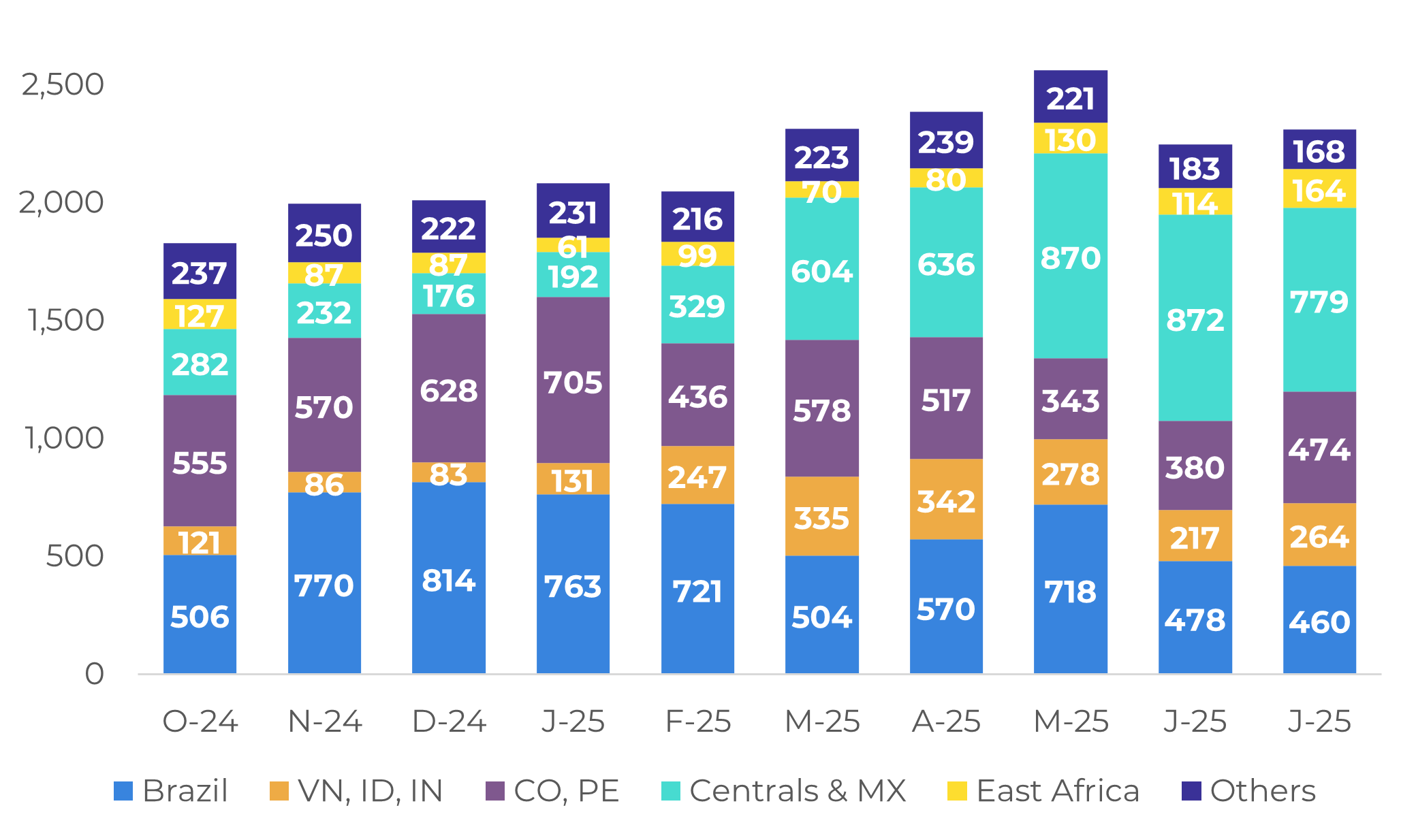

implemented. Tariffs are also expected to affect the share of each origin in US

imports. While Brazil figures were decreasing in June and July, this was mainly

due to low availability in the market, but we have yet to see the impact of

tariffs in the next months. Cecafé data also showed a sharp 46% decrease in

Brazilian exports to the US in August. Meanwhile, we are likely to see rising

imports from Colombia, Central America and Mexico, albeit limited, due to the

off-season.

Current differentials and uncertainty in the market have also decrease Brazilian farmers interest in certified coffee, leading to a decrease in stocks. In US ports, although Brazil’s participation is lower than in EU ports, current tariffs also led to a reduction of this origin participation, but an increase in Central American and Mexican coffee certified stocks.

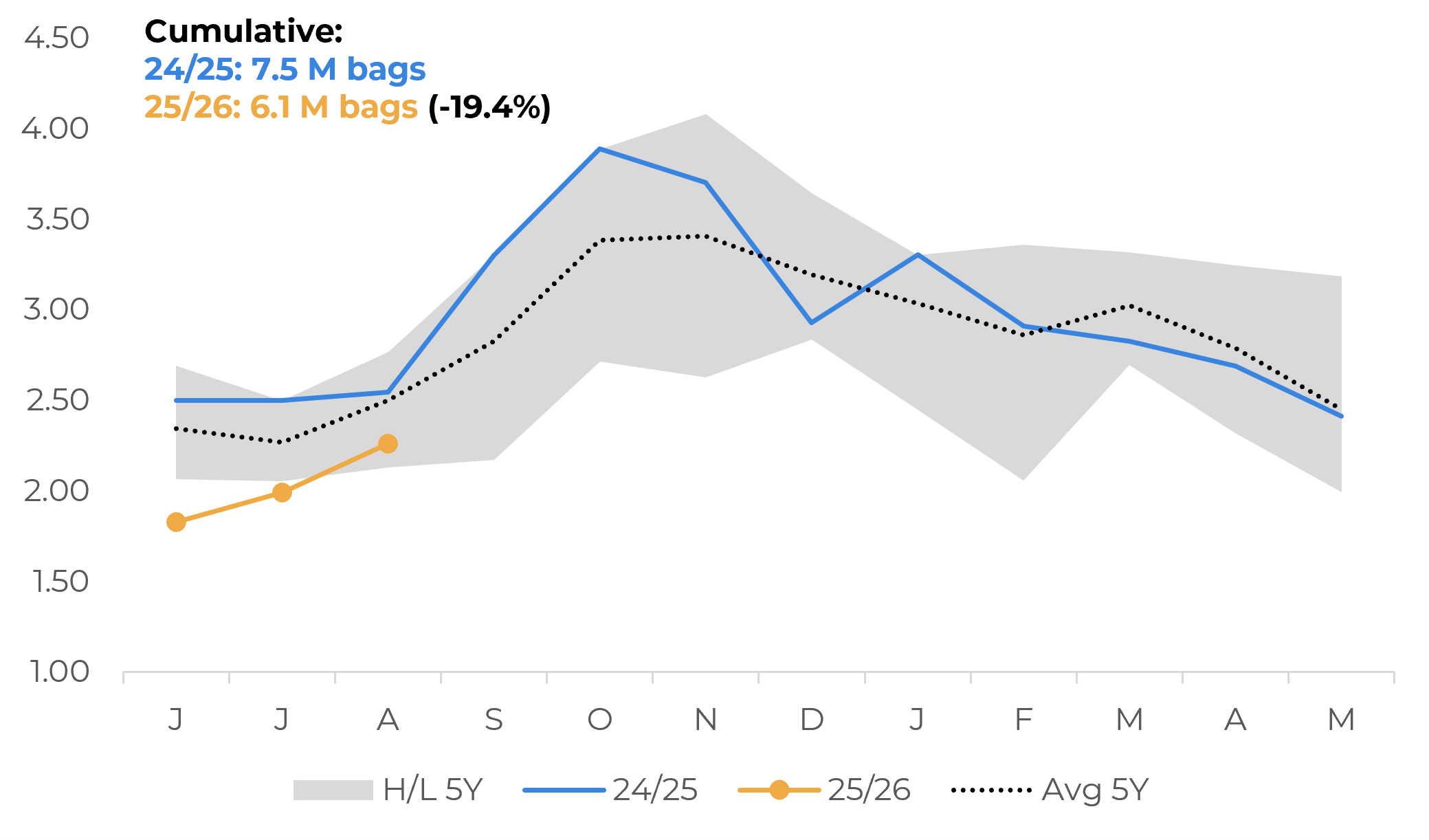

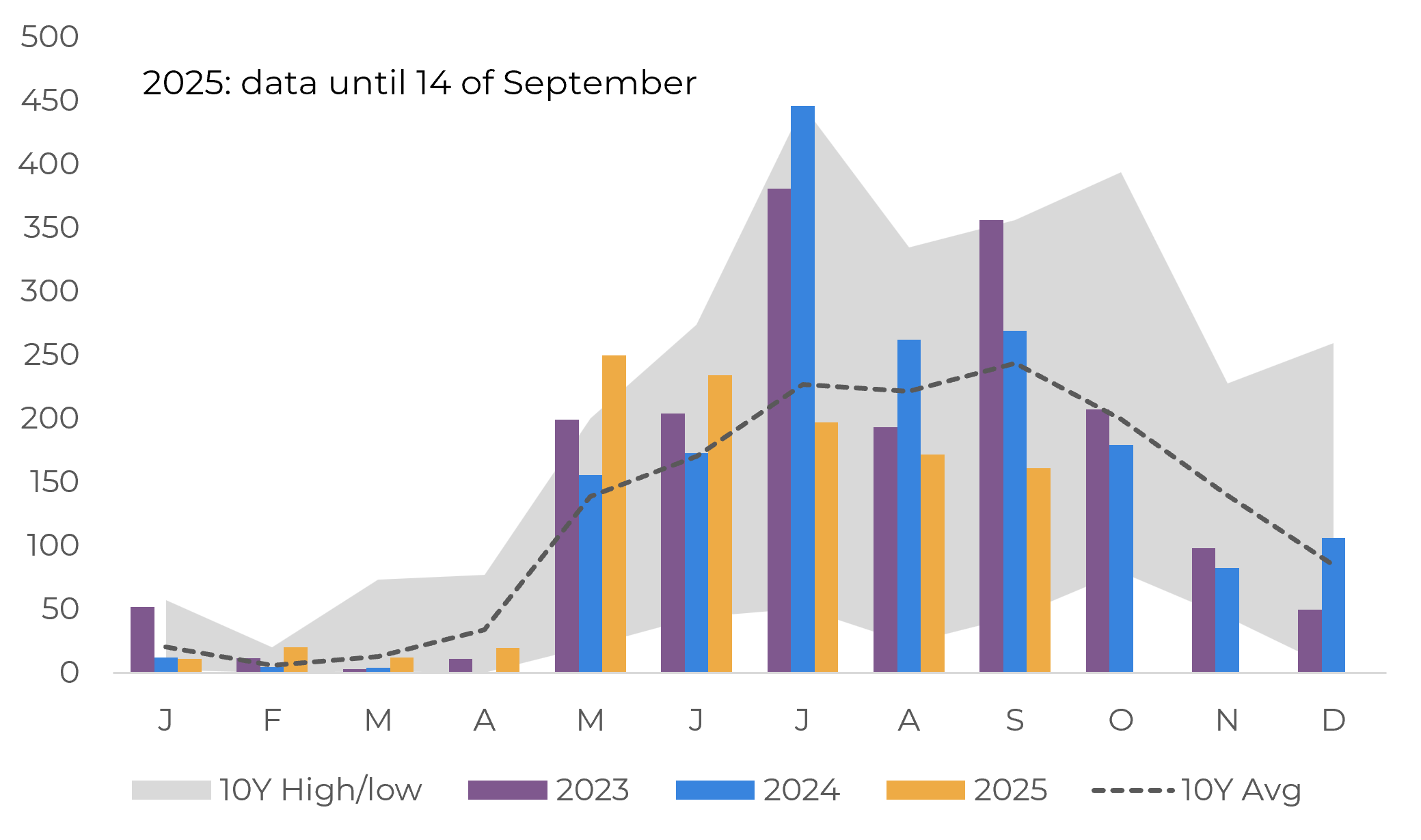

US: Coffee Net Imports (M bags)

Source: US. International Trade Commission

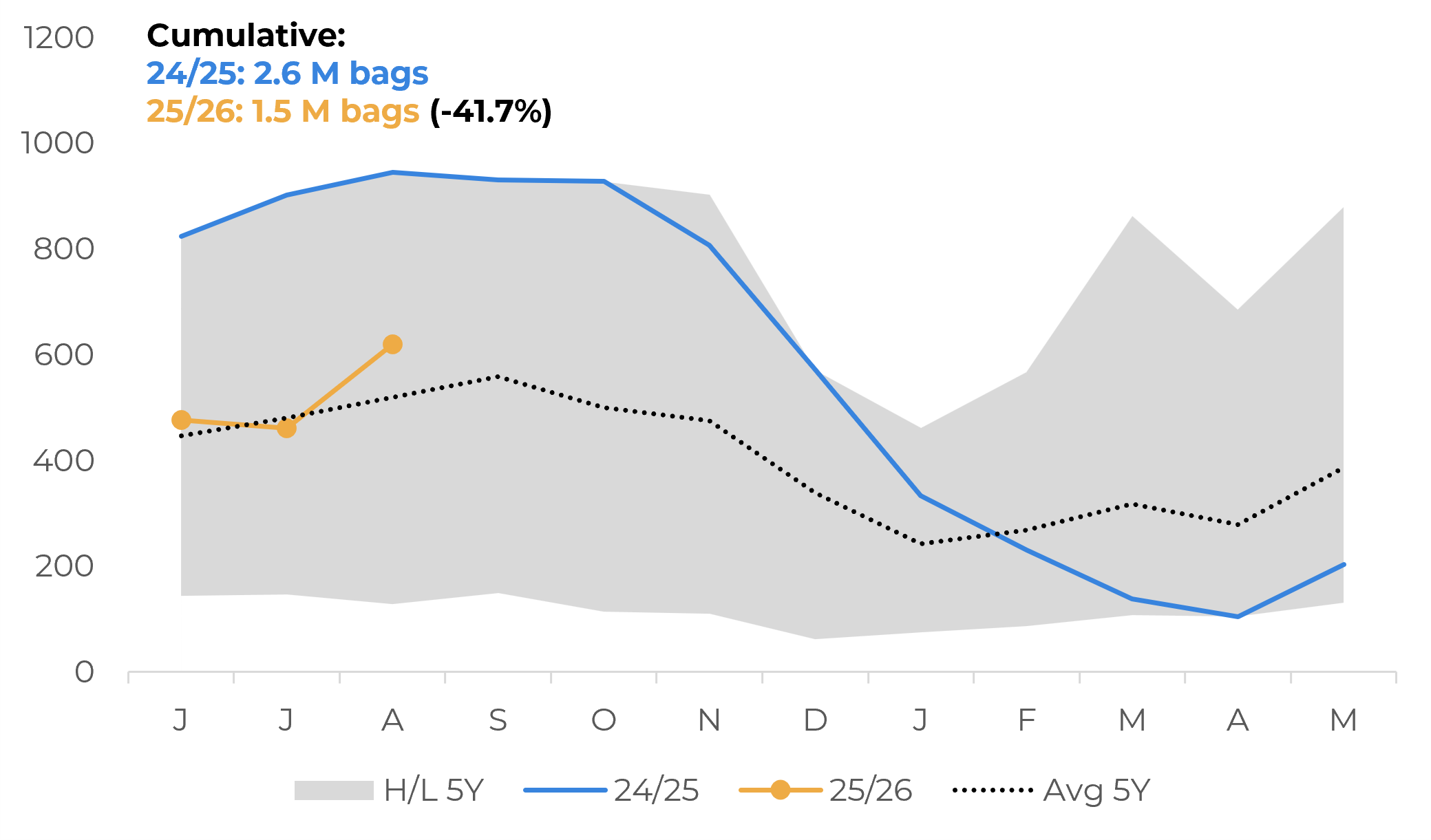

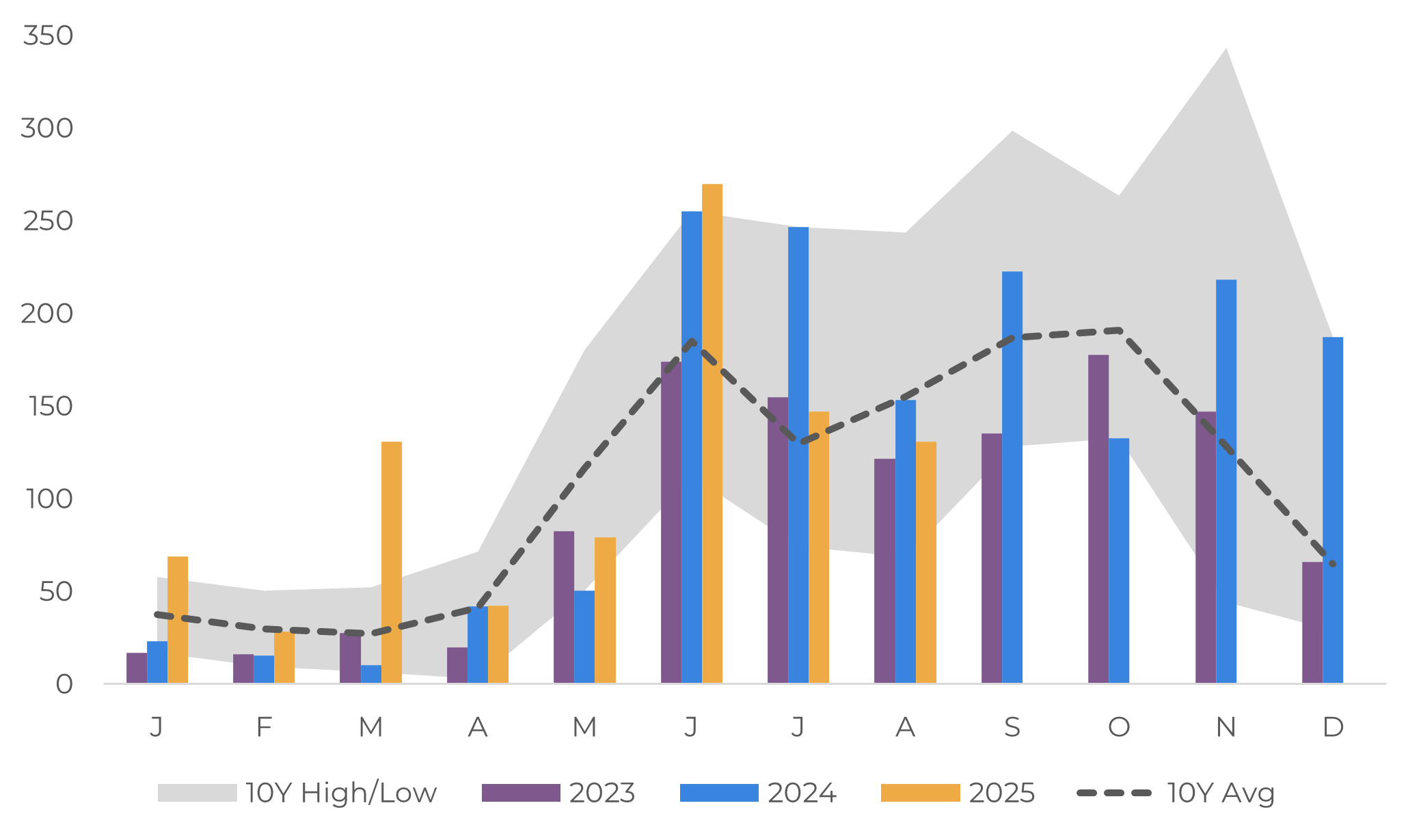

US: Green Coffee Imports by Origin (‘000 bags)

Source: US. International Trade Commission

Imports in other destinations

Beyond US, in Europe, cumulative net imports point to a stability from 23/24 levels for now, but weekly import data from September indicates that the trend is still for more sluggish imports in 2025. With EUDR now postponed again, roasters in EU have more time to buy coffee. On the other hand, disappearance also shows a resilience, compared to 23/24.

However, in Japan (another traditional coffee market) 24/25 cumulative net imports figures still show a drop compared to 23/24 and the average. In this sense, even with Japanese stocks at low levels, disappearance also shows a similar trend.

Brazil’s 25/26 crop update and 26/27 outlook

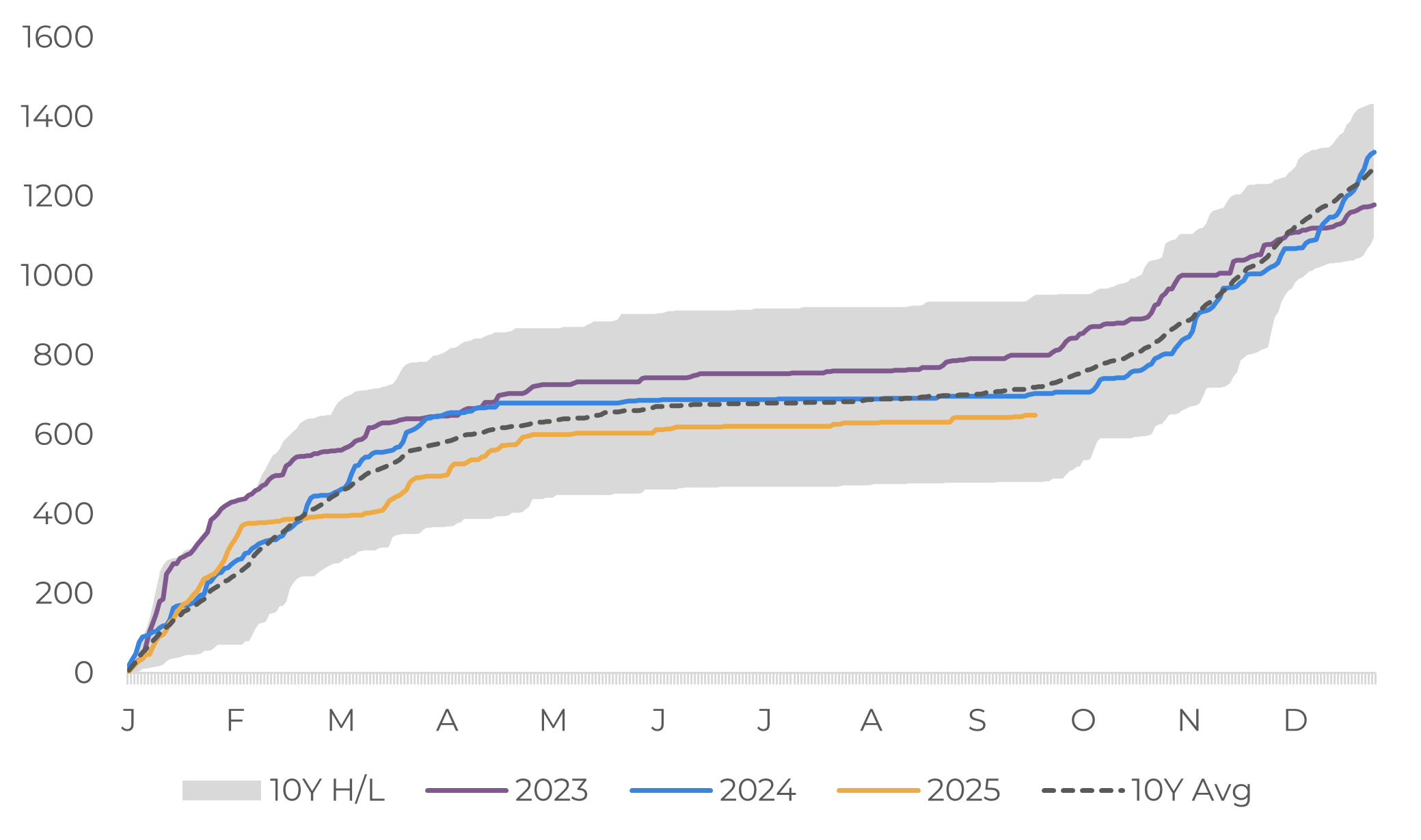

Brazil: Green Arabica Exports (M bags)

Source: Cecafe

For the 26/27 Brazilian crop development, weather in Arabica areas is still a risk for 26/27. While the flower of the 26/27 season already bloomed in Conilon areas and weather is more favorable, Arabica areas started to register higher volume of rains only this week. The blooms could happen in the next days and should allow for a first estimate of the 26/27 season potential. However, after the flowering, the continuation of the rainfall will be necessary for flower setting and bean filling. In this sense, the recent update from NOAA about a higher probability of a La Niña from October to December this year brings some risks to coffee development in part of the Brazilian areas.

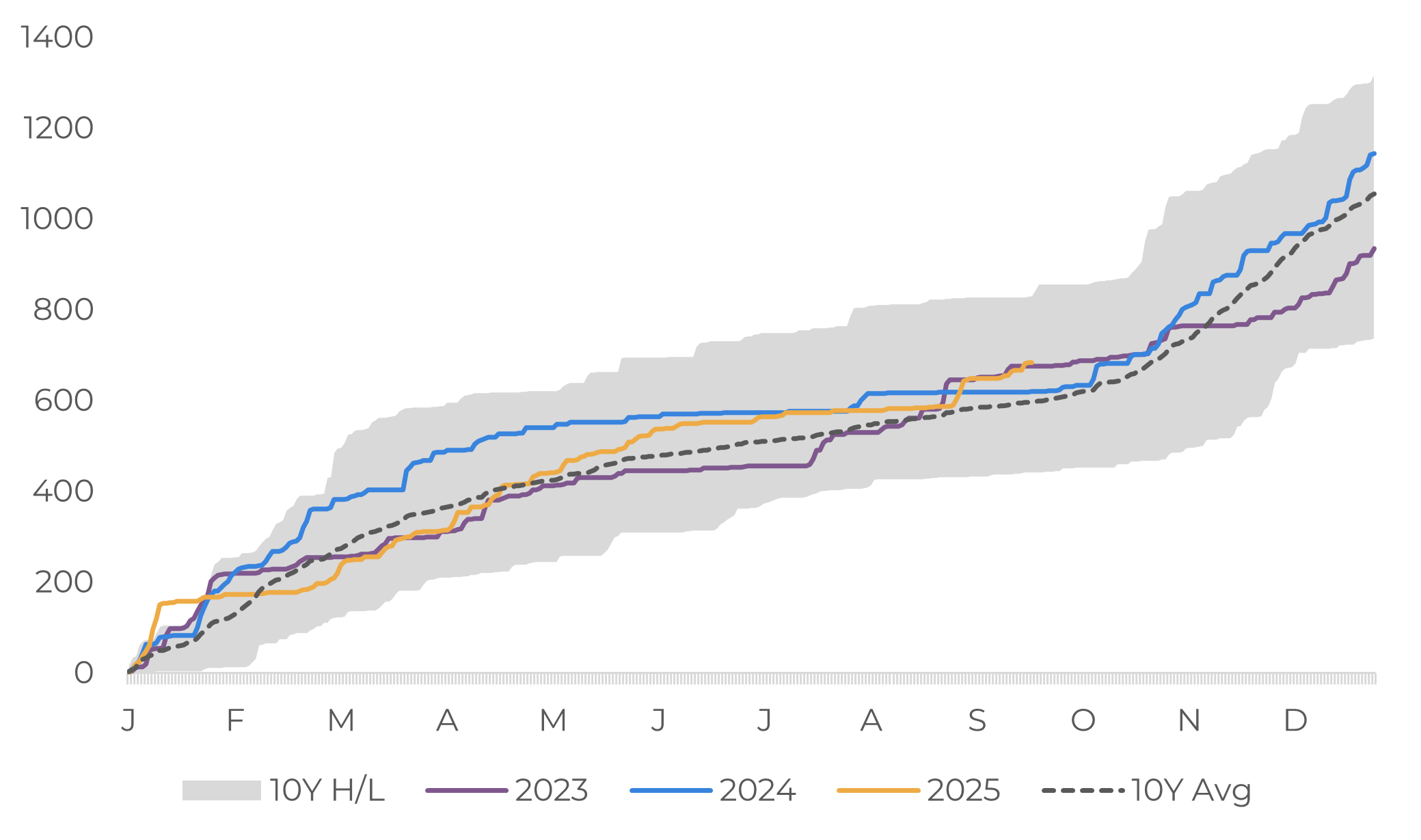

Brazil: Exports of Green Conilon ('000 bags)

Source: Cecafé

Cumulative Rainfall in Minas Gerais Coffee Areas (mm)

Source: Somar, Bloomberg

Cumulative Rainfall in Espírito Santo Coffee Areas (mm)

Source: Somar, Bloomberg

Weather continues to be monitored in other origins

Although rainfall in Vietnam has been below average in recent months, development of the 25/26 season is still going well, with our estimate of 29.4 M bags for the country unchanged. The harvest is expected to begin at the end of October.

Last month's rains in Indonesia disrupted the end of the harvest, but they also improved the crop conditions for the next cycle

In Arabica areas, Central American countries saw a more favorable weather in the 25/26 crop development. But excessive rains in Colombia are expected to decrease the potential for 25/26.

Vietnam: Cumulative Precipitation in Central Highlands (mm)

Source: Gadas, CPC

Honduras: Cumulative Precipitation (mm)

Source: Gadas, CPC

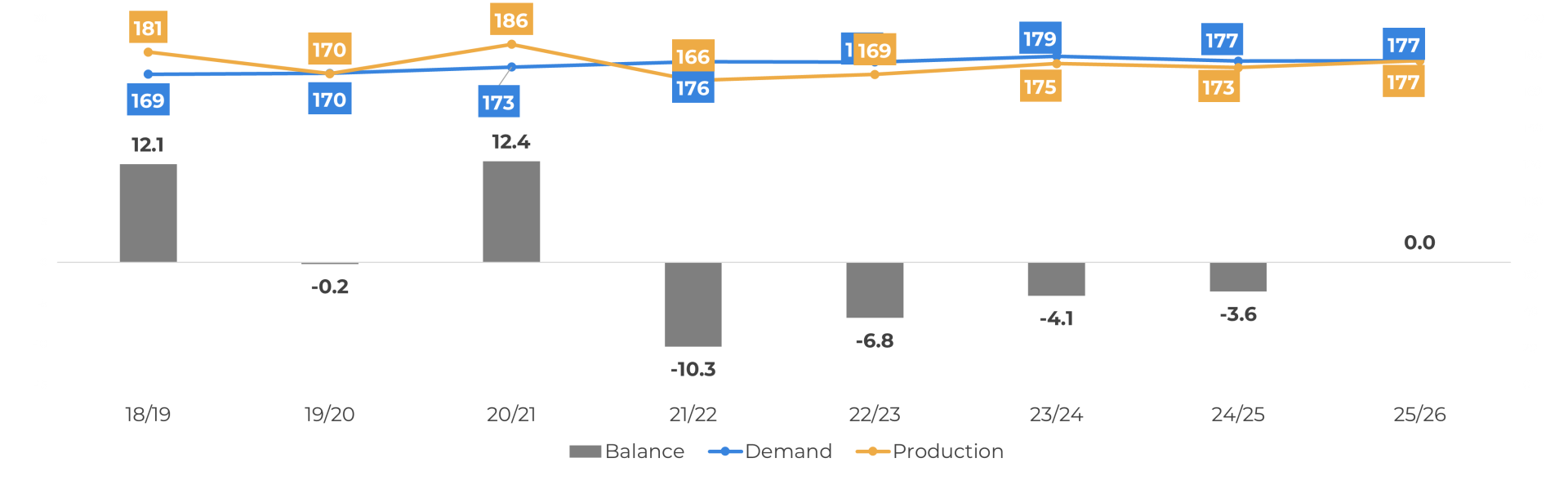

Global balance and perspectives

It was projected a drop in demand in 24/25, given higher prices, but with production lower than expected in Brazil and Vietnam, leading to a deficit. In 25/26, there is an expectation of higher supply, especially due to Robusta output. Demand, however, is expected to remain flat given current uncertainties. These figures will be revised as we reach more clarity in the next months.

Given the current trend in net import and stocks figures in destinations, we expect final stocks to continue to be pressured in the next cycle. Current financial costs, higher interest rates and prices also discourage stock formation. In origins, we might see a recovery in Robusta producers and in Brazil, especially considering the tariffs effect in Brazilian exports in 2025.

As for prices, the past few months have been marked by sharp fluctuations. Current market uncertainties, lower overall stock levels, logistical challenges, and Brazil's and other origins' development stage will likely keep prices sensitive to any change in outlook and volatile. Conversely, the trend for arbitrage is clearer, with Robusta prices favoring its use in demand.

Source: Hedgepoint

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

thais.italiani@hedgepointglobal.com

Disclaimer

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.