Coffee market waits for new fundamentals

- Coffee market has been, overall, slow in 2026, as most agents wait for new fundamentals. Agents continue to keep attention to the development of the 26/27 season in Brazil and the country’s supply in its offseason, as well as the trade in other origins.

- Weather in Brazil has been favorable to the development of the next cycle, albeit trade in the country is slow. Exports also continue at lower levels than in the 24/25 season.

- In other origins, trade has also been tepid, as farmers are not satisfied with current prices.

- These factors have contributed to still elevated spread levels between near-term contracts, especially for Arabica.

- May-July spread, however, has been decreasing in the recent days, reflecting the expectations of an increase in supply with the harvest in Brazil in mid-2026.

Coffee market waits for new fundamentals

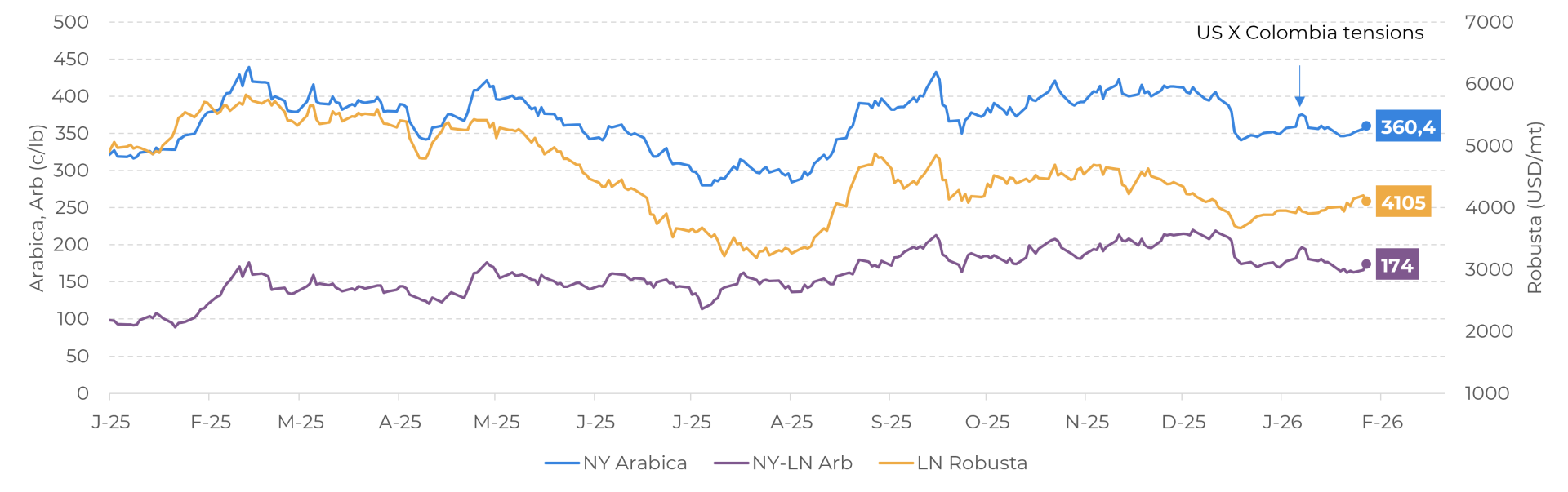

LN-Robusta (USD/mt), NY-Arabica and Arbitrage (c/lb) (1nd contract)

Source: LSEG

In Brazil, the weather has been mostly favorable for the development of the next cycle since last year. Despite the heat wave in the country at the end of 2025, rain has been more constant and helping in the bean-filling phase (see our report). There were reports of fruit dropping in certain Arabica regions, but in most cases, this has been associated with the high volume of coffee beans in trees and considered a normal behavior, likely not affecting the final production figures.

So, for now, our production estimates remain unchanged – ranging from 46.5 to 49.0 M bags of Arabica – although we will revisit these numbers between March and April, a period in which more accurate figures can be achieved.

For Conilon, storms hit Espírito Santo state (the largest producer) in the past days, bringing high volumes of rains. For now, there has been no report of negative impact on coffee production areas, but the weather should be monitored closely in the next months, as the plants are still in the bean-filling phase. As for Arabica, our production figures for Conilon will be updated between March and April.

A good production of Conilon and a higher output for Arabica could lead to a record crop in Brazil in 26/27 and tend to pressure down prices in the coming months. However, currently, low interest in new sales has kept some support for prices. Sales are at a slow pace as farmers are well capitalized and not interested in current prices. There has been some movement in the first week of 2026, when Arabica March/26 contract reached 382 c/lb, but domestic market has been muted since then, contributing to the relatively lower volatility in the market in the past days.

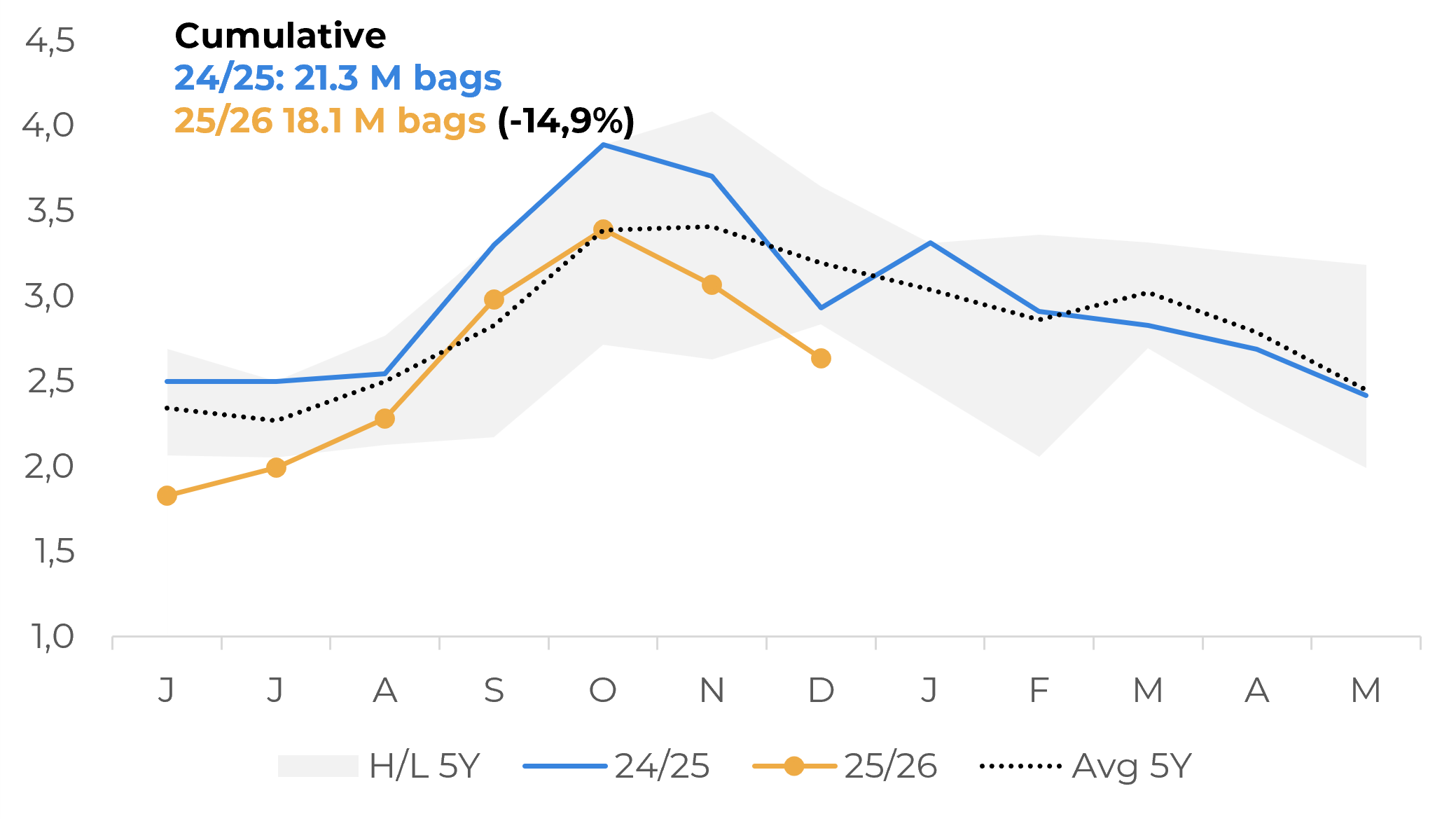

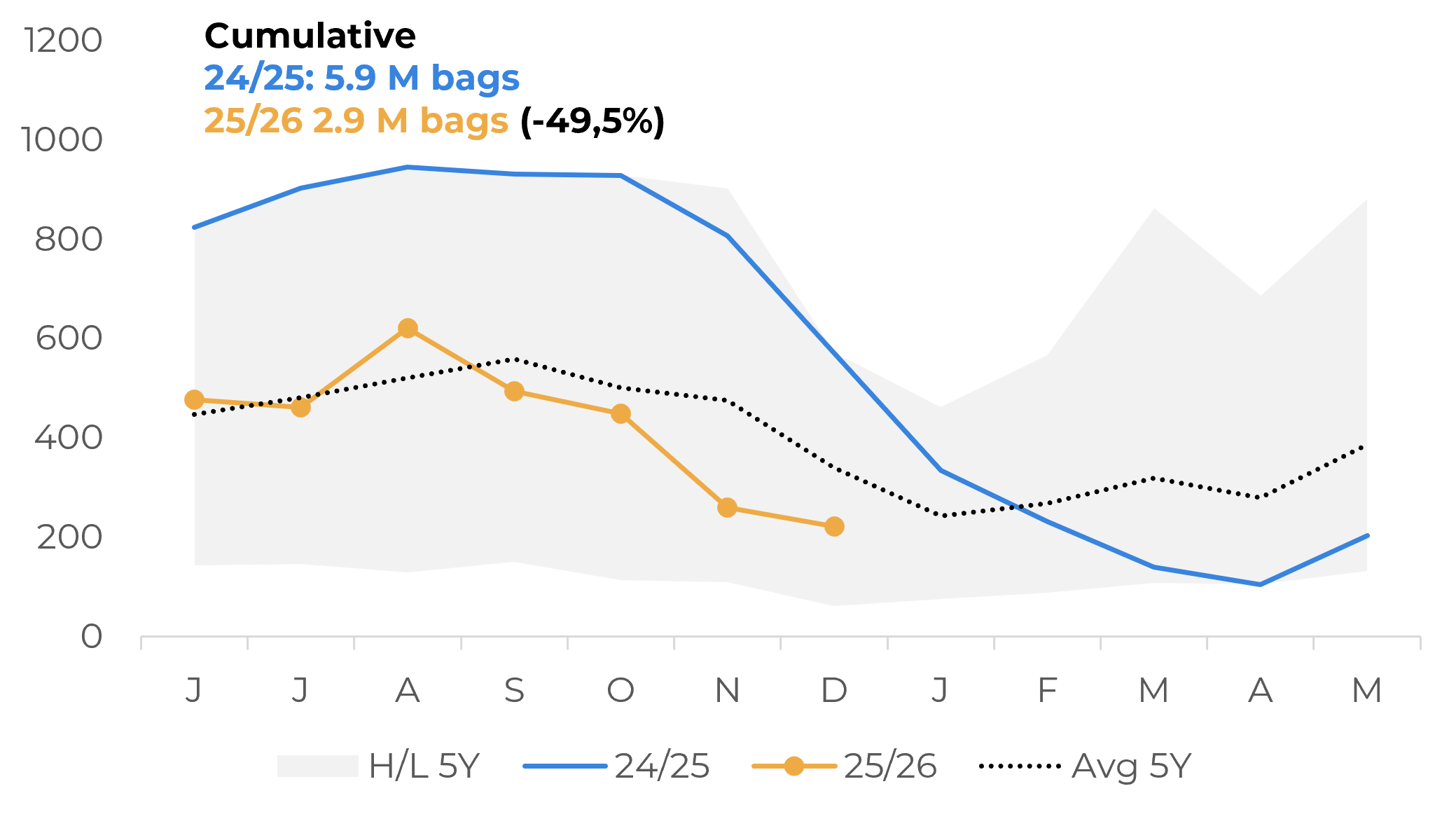

Brazil's exports from the 25/26 season of the country also continue to underperform compared to the last cycle. Toral shipments were at 3.13 M bags in December 2025, 20.2% lower than 2024, with a decrease of 10% in Arabica figures (2.63 M bags) and down 61.1% for Conilon (222.15 K bags). Beyond the slow pace in sales, the ongoing US tariffs on soluble coffee also contributed to the drop. Lower exports compared to the 24/25 cycle were also expected, given the record exports last season.

Brazil: Arabica Exports (M bags)

Source: Cecafé

Brazil: Conilon Exports (‘000 bags)

Source: Cecafé

Trade in other producer countries, such as Colombia, Vietnam, and Indonesia, has also been tepid. In Indonesia, supply is limited, as the country is in its offseason, with many farmers focused on the development of the 26/27 season. The current concerns over January weather impact in the next cycle, with some reports of cherries falling due to the high volume of rain, could also prompt producers to hold new sales.

In Vietnam, while many exporters are seeking to buy, farmers are still selling a low volume of beans from the 25/26 season, current being harvested. This reflects a decrease in values from early 2025, when domestic prices were above the 150.000 dongs due to the shortage of Robusta worldwide, while in 2026, coffee is being traded below the 100.000 dongs.

Lastly, in Colombia, there has also been rising concern over the impact of lower prices in trade, although this also reflects the valuation of the Colombian peso in the past months. In a statement, Germán Bahamón, general manager of the National Federation of Coffee Growers, Fedecafé, pointed that the appreciation of the peso has generated losses for producers and reduced the country’s bean competitiveness, impacting the sector. This could also prompt farmers to sell coffee at a slow pace in the next months, waiting for better prices, possibly limiting supply.

These current worries over short-term supply continue to be reflected in spreads between the near-term contracts for both varieties of coffee, but more particularly for Arabica’s. For instance, March/26 and May/26 spreads continued to an uptrend, close to the 19 c/lb in the past days. The offseason in Brazil and Indonesia, and lower interest of farmers around the world in new sales could keep some support into the Mach/26 and spreads elevated.

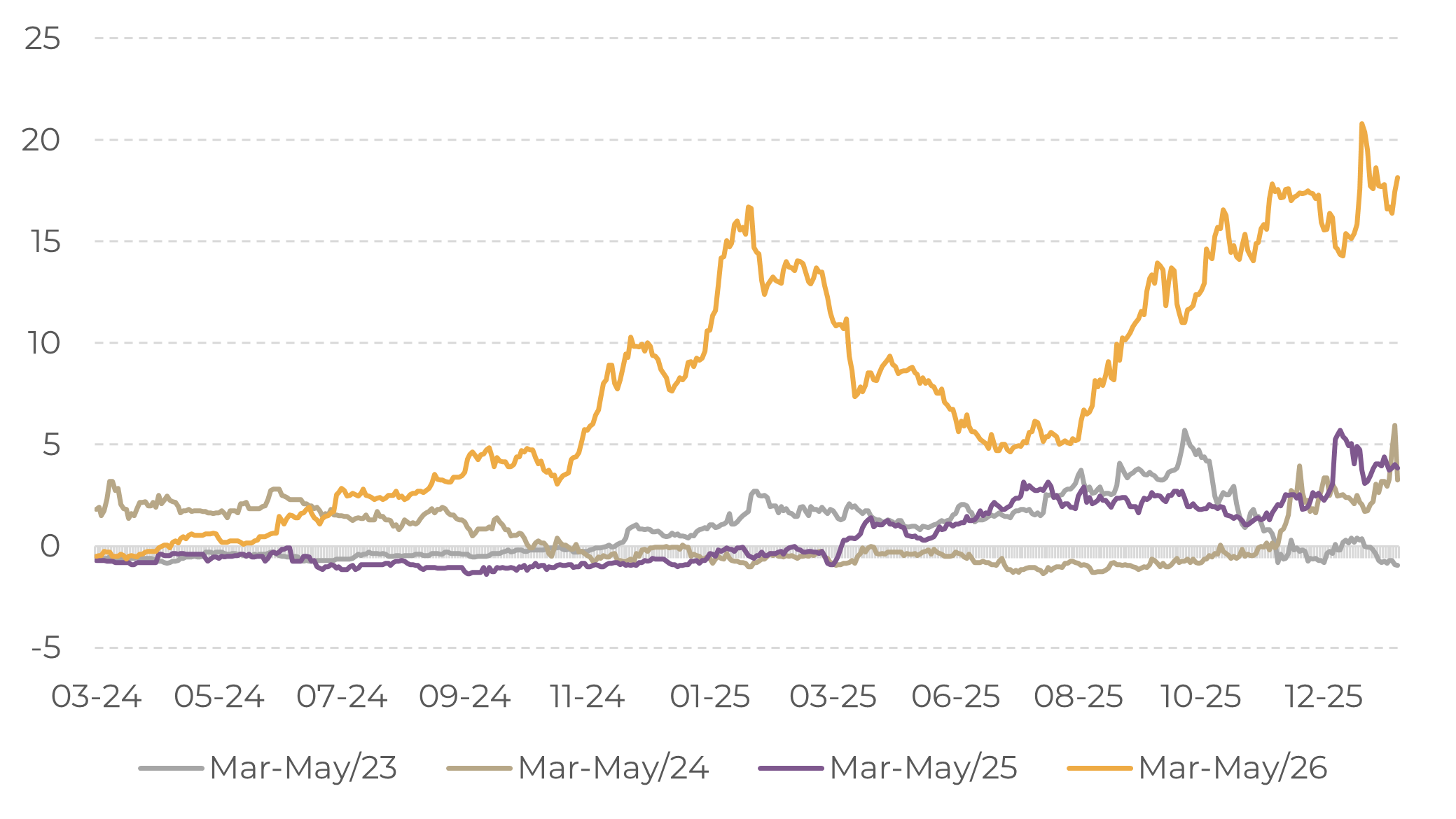

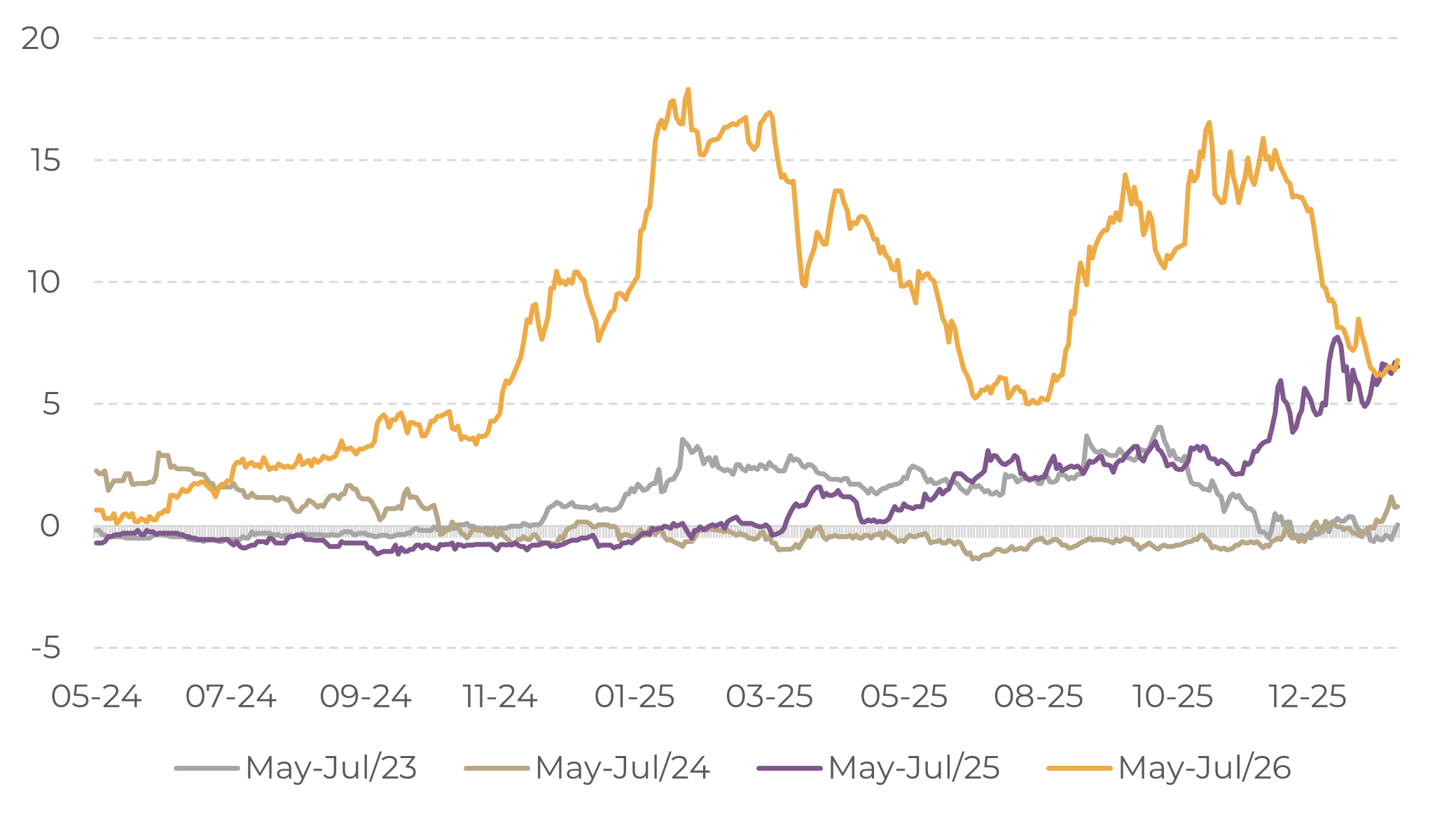

Meanwhile, the May-July spread, albeit still positive, has been decreasing in the past weeks, between 6-7 c/lb, reflecting the harvest of a larger crop in Brazil between Q2 and Q3 and expectations of an increase in supply. As farmers prepare to bring in a larger crop, they are likely to boost sales to cover harvest costs and increase storage capacity for the new beans, which could apply downward pressure on prices, especially on the July contract.

Arabica: March-May Spread (c/lb)

Source: LSEG

Arabica: May-July Spread (c/lb)

Source: LSEG

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

carolina.franca@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.