The bears have arrived: Arabica coffee prices already 12.9% down in 2026

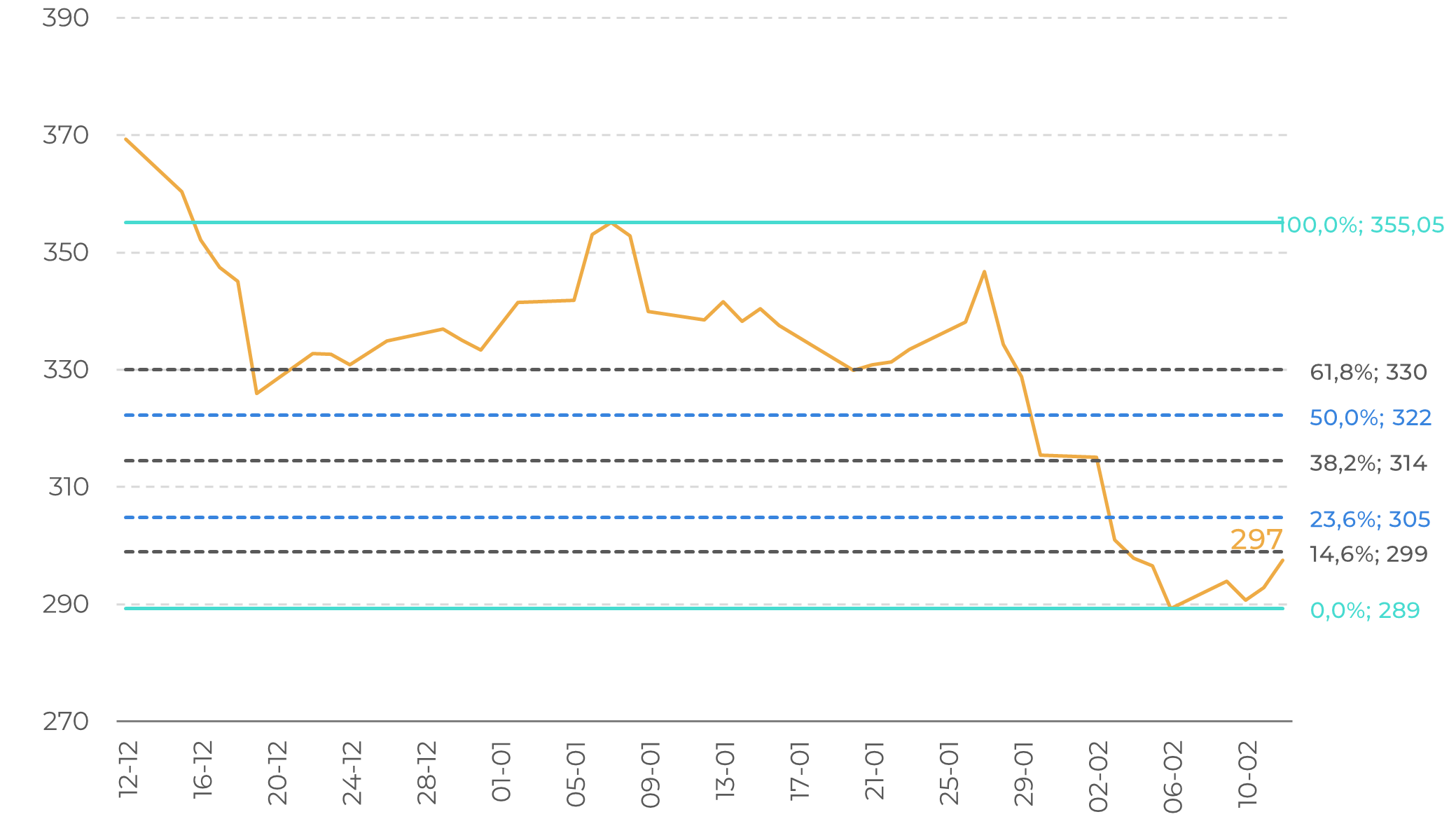

- Arabica coffee futures have dropped sharply over the past two weeks, pressured by technical selloffs and expectations of a bumper Brazilian crop in the 2026/27 season.

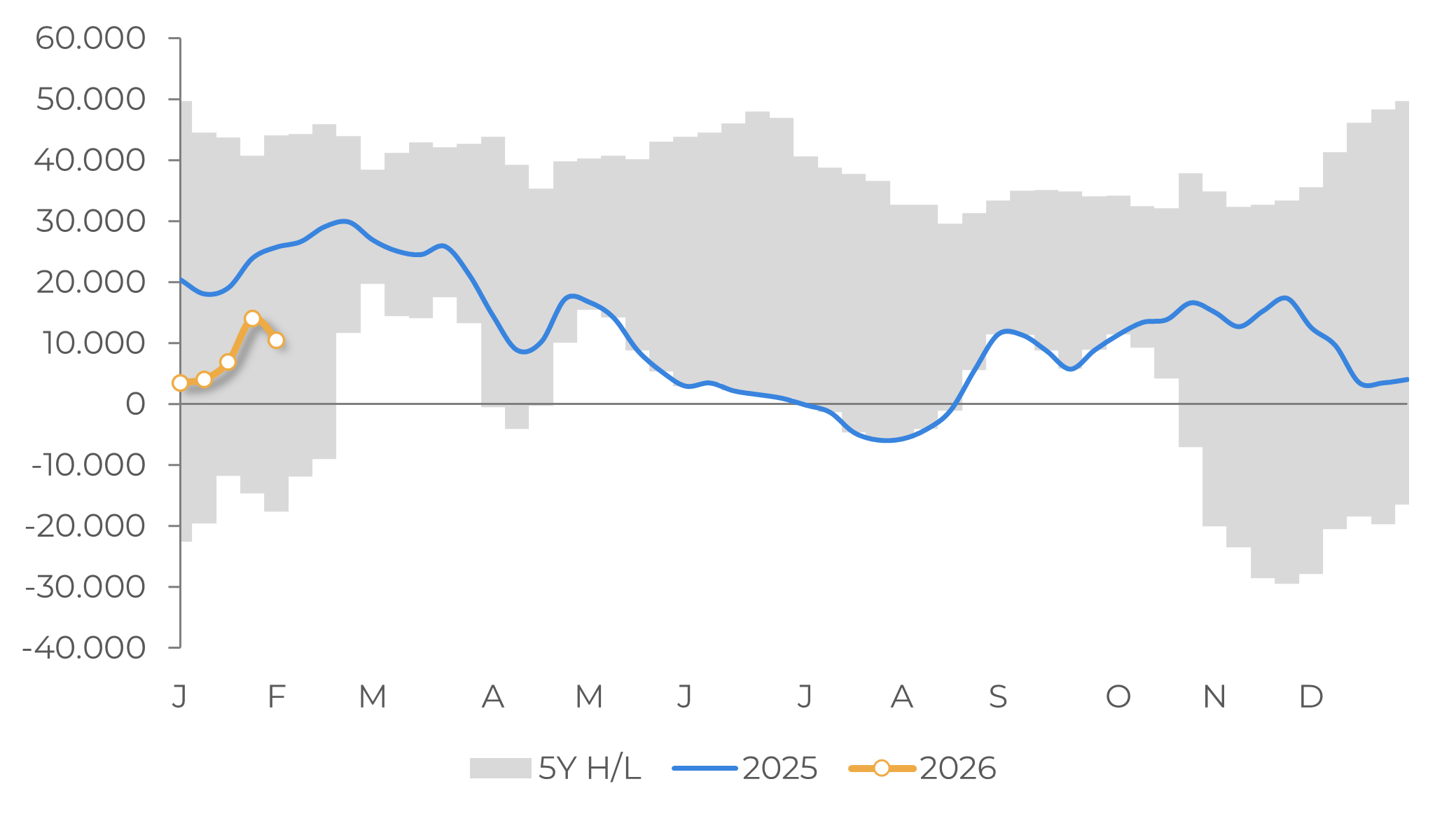

- The latest CFTC report highlights a shift in market sentiment, with speculative funds trimming their long positions.

- Although the market rebounded slightly this week, supported by the March contract options expiry, the overall outlook remains bearish, with the May contract likely to test key support levels in the coming days.

- Coffee-growing regions in Brazil have received abundant rainfall in early 2026, supporting the bean-filling phase and underpinning prospects for strong production in the next cycle. Many market participants are pointing to the possibility of a record crop.

- The recent price drop has prompted selling activity in the Brazilian market. However, volumes remain limited. The latest export data also show declining shipments, reflecting reduced farmer selling over recent months.

The bears have arrived: Arabica coffee prices already 12.9% down in 2026

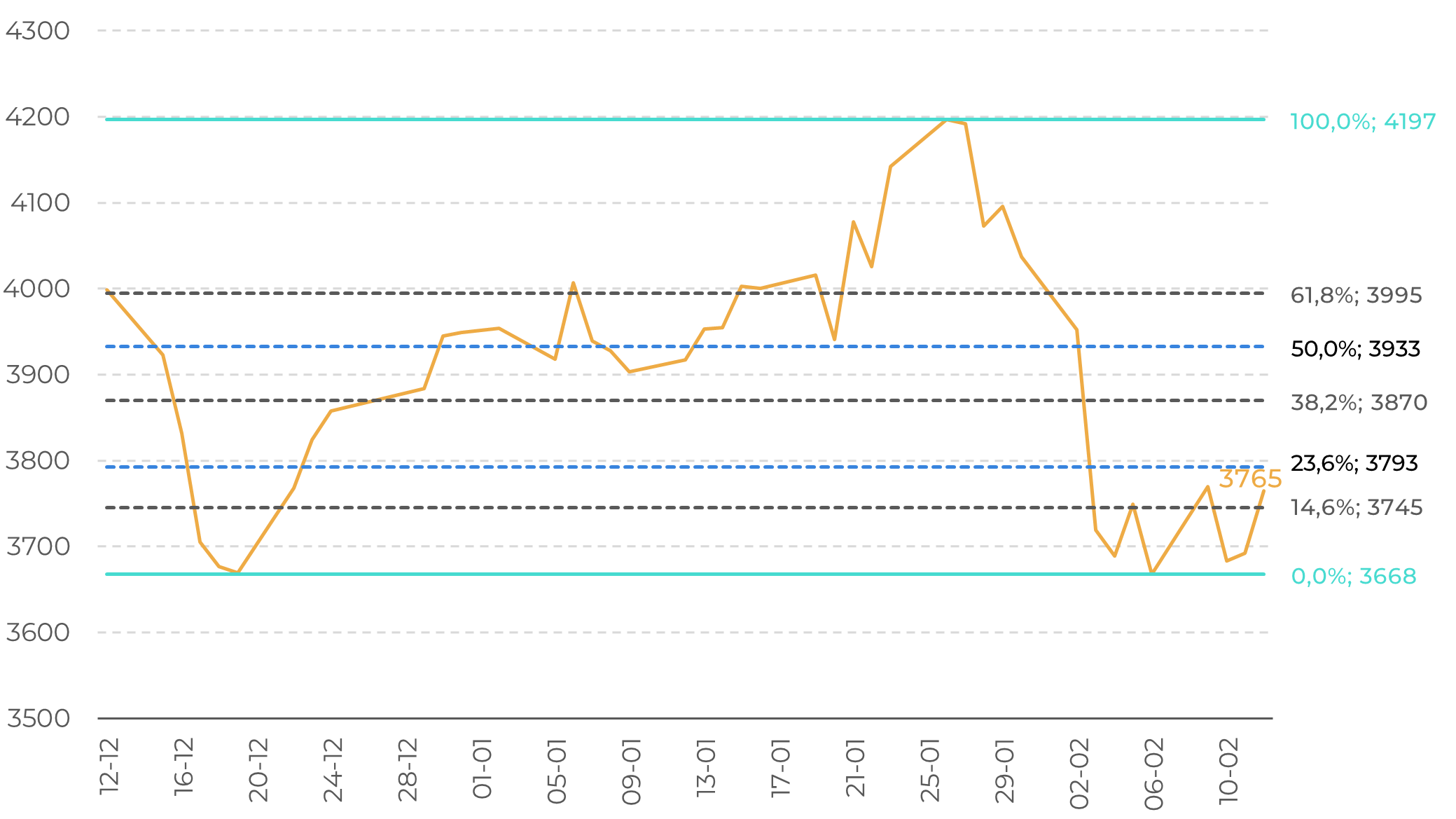

Robusta future prices have also followed a similar pattern , with prices still in a bearish trend but showing a short rebound. It’s also interesting to note that, for the variety, prices have also been supported by limited supply in Southeast Asia. While Indonesia is in its offseason, farmers in Vietnam are refraining from selling, driving differentials up (see our report). There is also the expectation of increased demand for this variety in 2026, as Robusta’s prices are more competitive than Arabica’s, with higher prices in past months expected to impact consumer habits in most destinations, such as US.

Arabica Future (2nd contract) and Fibonacci Retracements Levels (c/lb)

Source: LSEG

Robusta Future (2nd contract) and Fibonacci Retracements Levels (USD/mt)

Source: LSEG

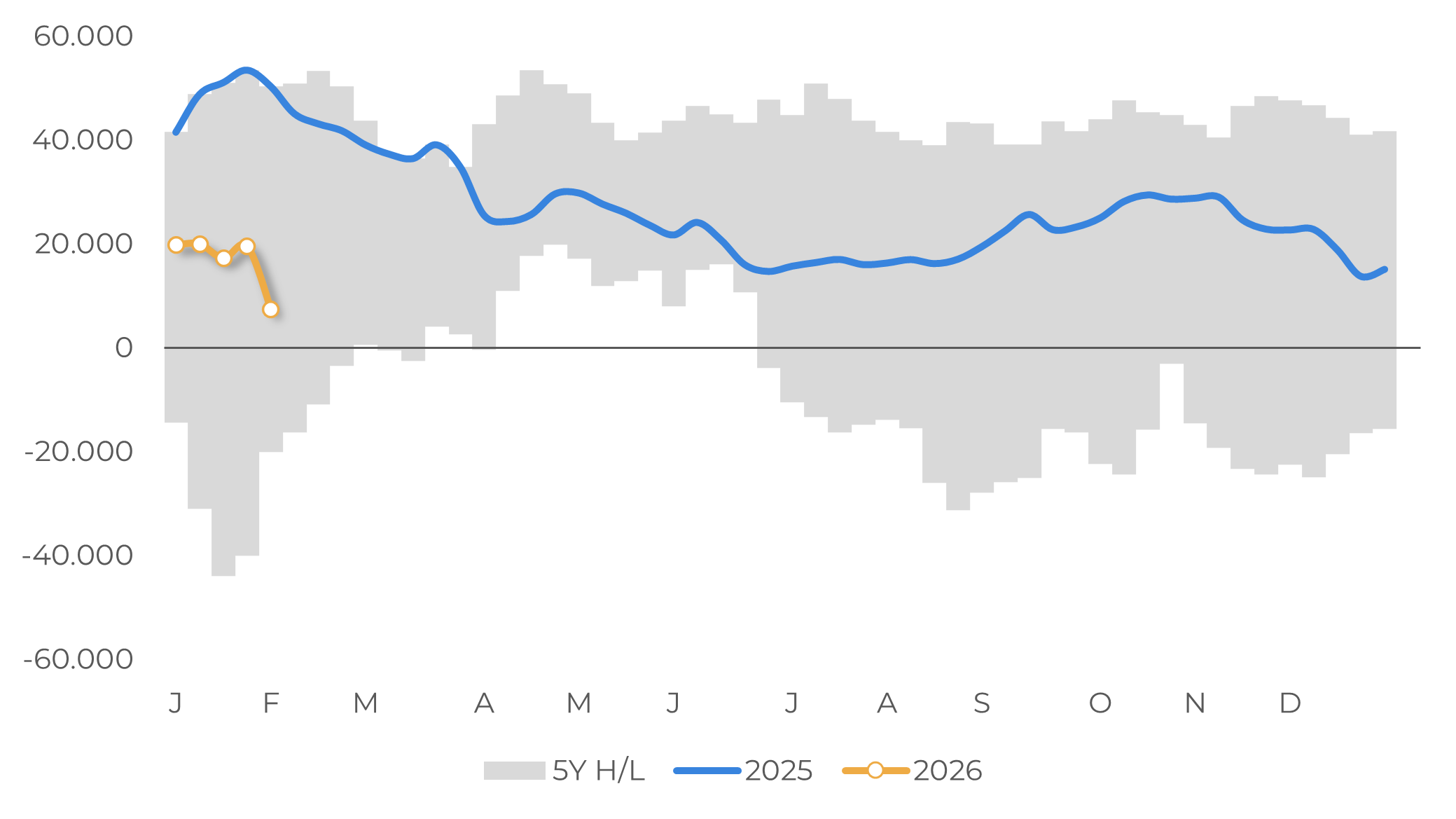

Another point of attention is changes in speculative funds positions. The coffee market’s selloff intensified sharply in February, marking a clear acceleration of a correction that had been unfolding for months. While speculative investors had already been reducing long exposure amid growing expectations of improved global supply in 2026, the move became disorderly after Brazil’s crop outlook shifted decisively more bearish this year, as many companies are now pointing to a record crop in the country. Coffee-growing regions have received abundant rainfall since January, supporting the bean-filling phase and underpinning prospects for strong production in the next cycle. More recently, Conab (the Brazilian National Supply Company) reported a record crop of 66.2 M bags, and although their figures are typically below market projections, they still indicate a trend in Brazilian production.

Positioning data shows that February’s price decline was driven particularly by aggressive liquidation of existing longs. The latest CFTC Commitments of Traders report showed a sharp weekly drop in non commercial net long positions in ICE Arabica, as funds simultaneously exited longs and added shorts, one of the largest positioning adjustments in months.

In the physical market, the recent drop in Arabica and Robusta prices has also prompted selling activity in Brazil in early February. However, sales volumes remain limited, as farmers are well capitalized and are waiting for a clearer view of price direction. In this context, it is also important to highlight that lower farmer selling in recent months is still reflected in the country’s exports. According to Cecafé, total coffee exports reached 2.78 million bags in January, down 30.8% year over year. According to Márcio Ferreira, Cecafé’s president, falling prices and the depreciation of the U.S. dollar since the end of 2025 have contributed to this movement.

Arabica : CFTC Speculative Funds Net Positions (lots)

Source: CFTC

Robusta : ICE Speculative Funds Net Positions (lots)

Source: ICE

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.