Coffee Outlook 2026 Highlights

This analysis summarises the key points that were discussed at the Coffee Outlook 2026 event on 25 February.

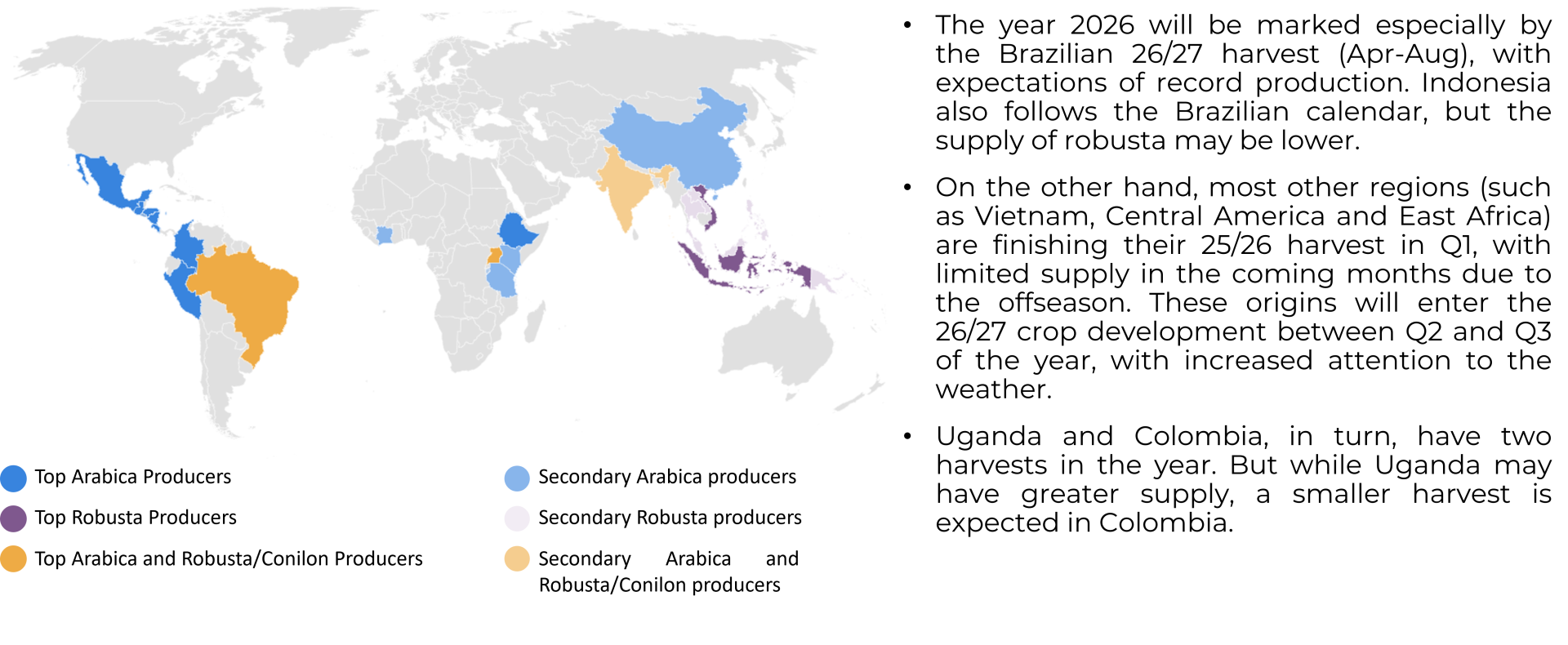

Coffee Market Overview in 2026

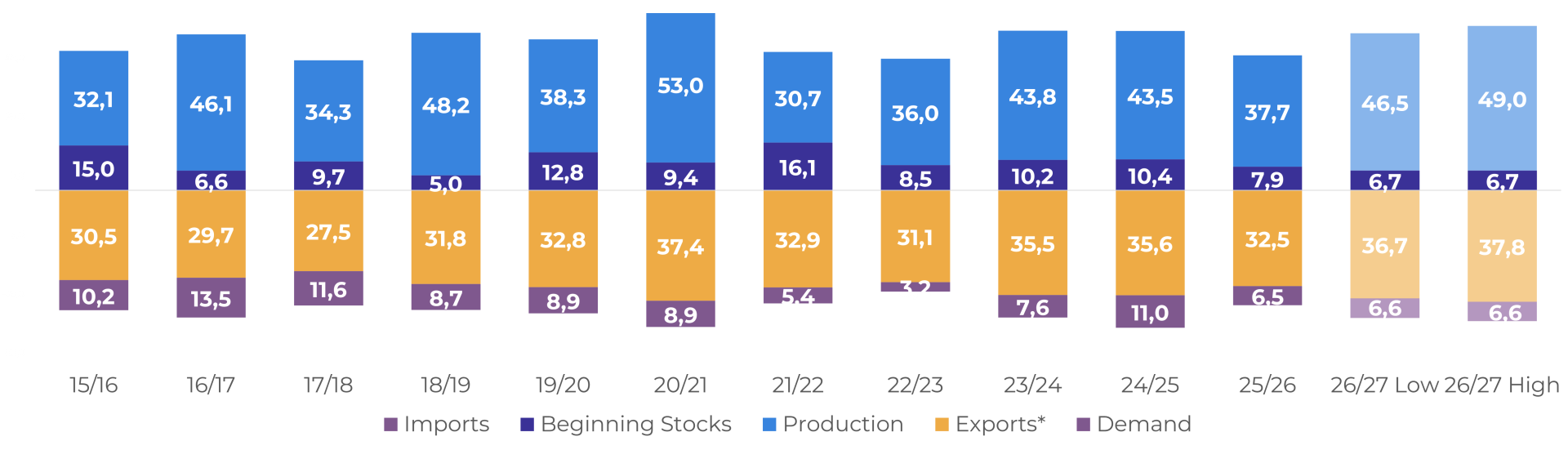

Brazilian 26/27 Season

Despite the delay, rains arrived at the right time in 2025 in Arabica regions, allowing for good blooms in coffee fields. Although productivity remains uneven, a bulk crop is expected, also supported by increased area. As for 2026, rain has been constant and abundant, likely helping in processing yields.

In this sense, depending on the final processing yield, production could reach between 46.5 M and 49 M bags in 26/27. This would also support an increase in exports, particularly given that global stocks are still low and destinations are likely to seek to replenish them during the higher Brazilian season.

As for domestic demand, current arbitrage levels still favor a higher use of Conilon in Brazil, with Arabica domestic demand likely continuing lower than in the 24/25 season.

Brazil: Arabica Supply and Demand (M bags)

Source: Hedgepoint

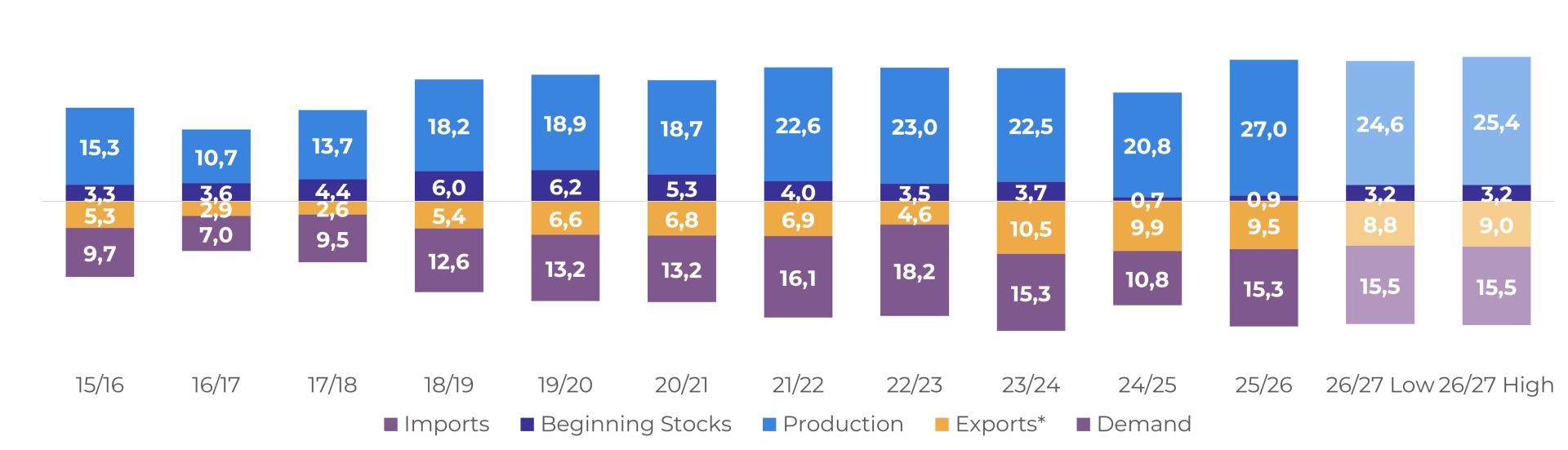

As for Conilion, although yields were expected to drop due to the record production in 25/26, area increases in past years, and good weather should help production to remain high (above previous years), supporting a small increase in domestic demand – in expectation of lower prices in the coming months.

Exports could also remain high, as global stocks have been depleted and the level of arbitrage favours the consumption of Robusta. Conversely, the use of Conilon in Brazilian domestic blends could offset some of this movement.

Brazil: Conilon/Robusta Supply and Demand (M bags)

Source: Hedgepoint

Since 2025 Brazilian roasters have moved back to a higher Conilon blend, as Arabica had a greater valuation. The movement is also expected to continue in 2026, even with an increase in Arabica supply. Retail prices are also expected to drop slightly in the year, which could prompt a demand recovery.

Destinations Outlook

Consumer prices have been increasing since 2021, but had a stronger hike in 2025. Coffee could become cheaper in 2026, but prices may continue above pre-pandemic levels.

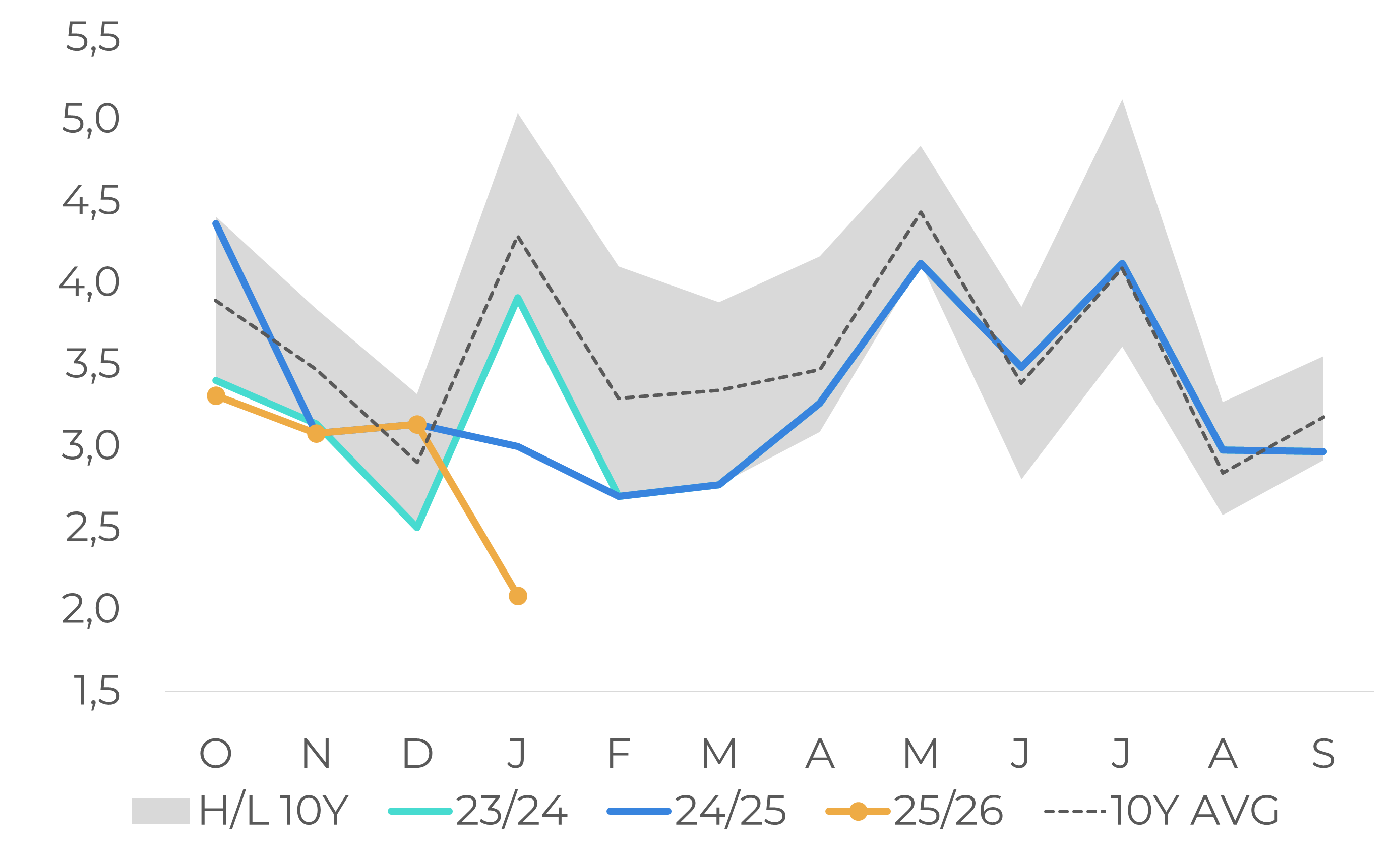

For the U.S., prices affect mostly consumer habits, with likely lasting changes in the country, with reports from major companies in the sector indicate that Americans started to drink more coffee at home. Despite remaining below the 10-year average, the 24/25 U.S. season saw a recovery in net imports, underscoring market resilience amid higher prices, though with shifts in consumption patterns. In 25/26, net imports started at a low pace, likely due to tariffs on Brazilian beans, but lower price prospects and the removal of tariffs could support a rebound.

For the EU, higher prices impacted import demand in the 24/25 season. Despite stocks remaining at low levels, EU net import figures for the 24/25 and 25/26 seasons impacted the disappearance/apparent consumption figures. However, higher supply (and lower prices) in 2026 could lead to a recovery for the remainder of the 25/26 season.

U.S. Coffee Net Imports (M bags)

Source: U.S. International Trade Commission

EU Net Imports (M bags)

Source: European Commission

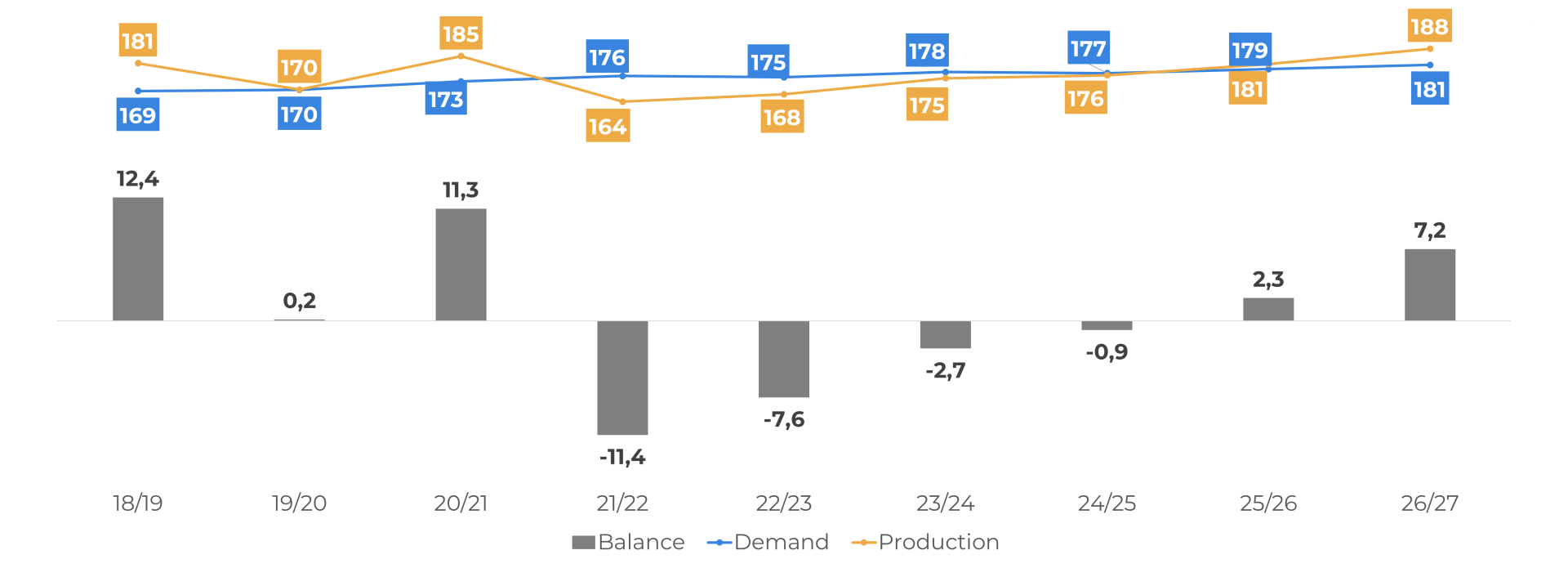

Global Balance And Prices

We expect a surplus in the season given the expectation of an increase in supply in Brazil in 26/27. However, it is important to remember that most other origins are only just entering the development stage of the 26/27 season, and the size of the surplus next season will depend heavily on the weather.

Global Coffee Balance (M bags)

Source: Hedgepoint

Higher production in the 26/27 season would favour a recovery in stocks. However, inventories were depleted in the previous season and will remain a cause for concern, even with an increase in volume.

Overall, prices of Arabica and Robusta have fallen considerably since the end of 2025, and the outlook is bearish due to the prospect of a record crop in Brazil. However, prices are likely to remain volatile as stock levels are low and farmers are selling at a slow pace, particularly in Brazil, Colombia and Vietnam. Any supply shock will lead to further volatility.

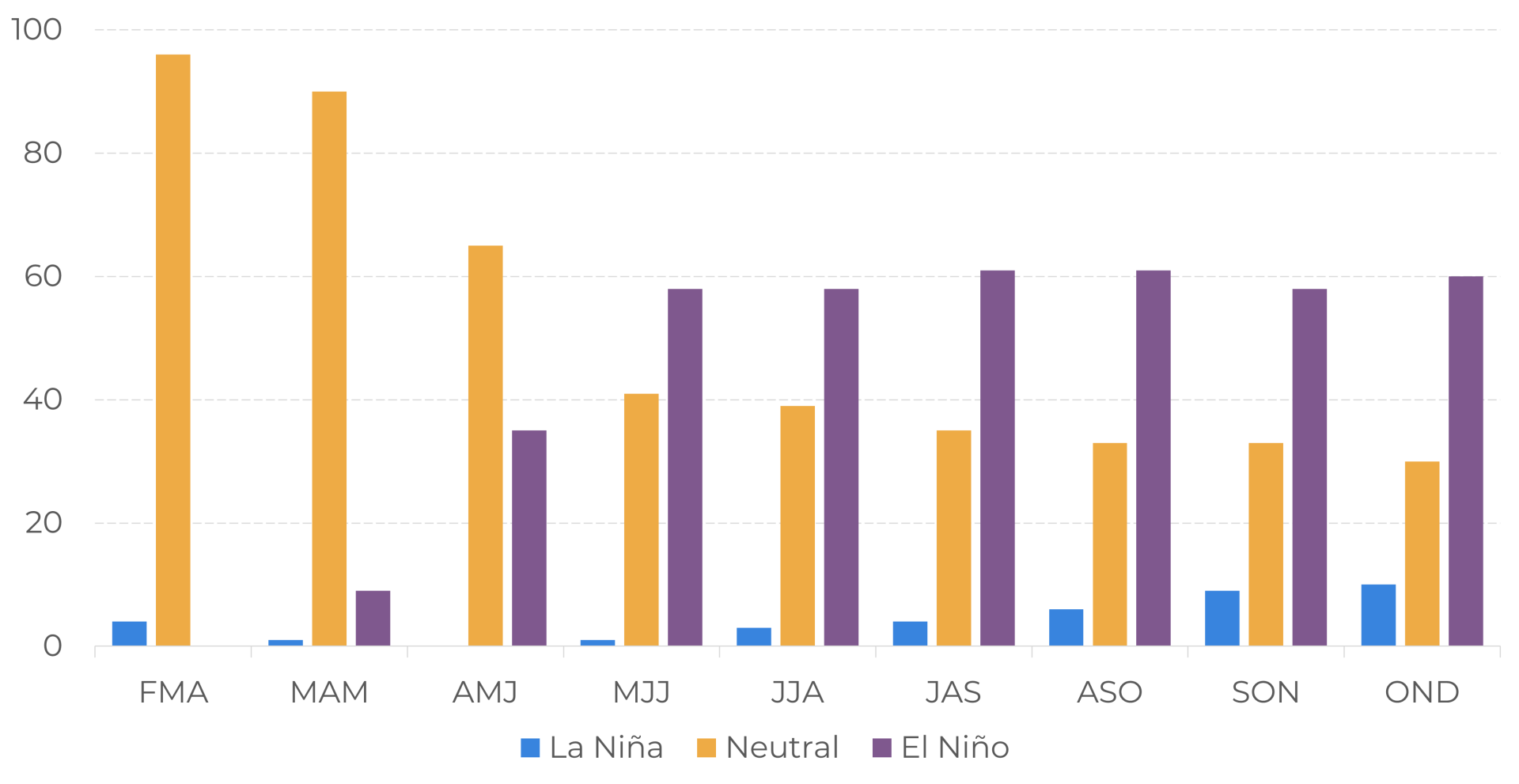

IRI ENSO Forecast (%)

Source: International Research Institute for Climate and Society

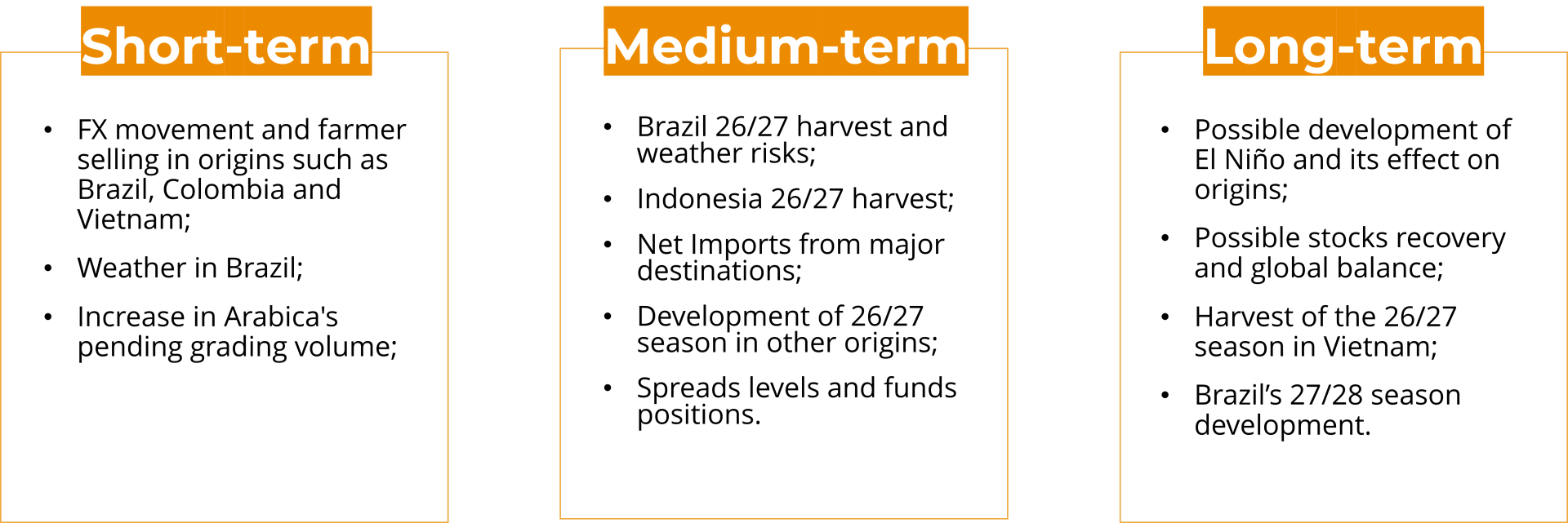

What to look out for in 2026

Source: Hedgepoint

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

livea.coda@hedgepointglobal.com