Higher risk reduces new sales, triggering differentials and spreads

- Since February, the coffee market has remained subdued amid rising global risks following the escalation of the U.S.–Iran conflict. With the 25/26 harvest concluded in many producing countries, farmers are assessing the geopolitical impacts on the coffee market and have been refraining from selling substantial new lots.

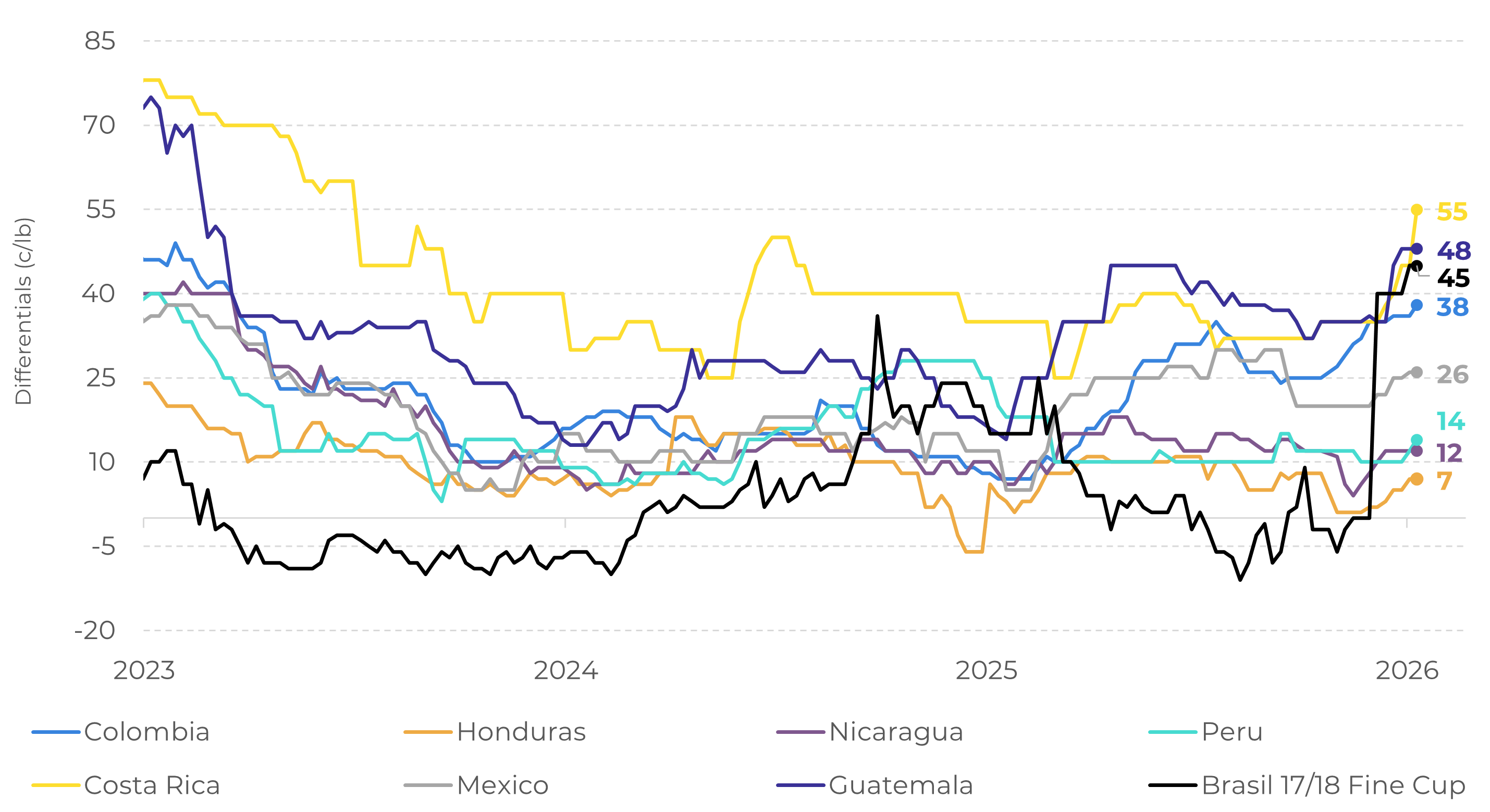

- In Brazil, farmers have been increasingly reluctant to sell since the end of 2025, affecting both Brazilian coffee exports and differentials, especially after disruptions to maritime routes in the Red Sea. Arabica 17/18 fine cup, which had been trading at a discount earlier this year, is now quoted at a premium of over 40 cents/lb.

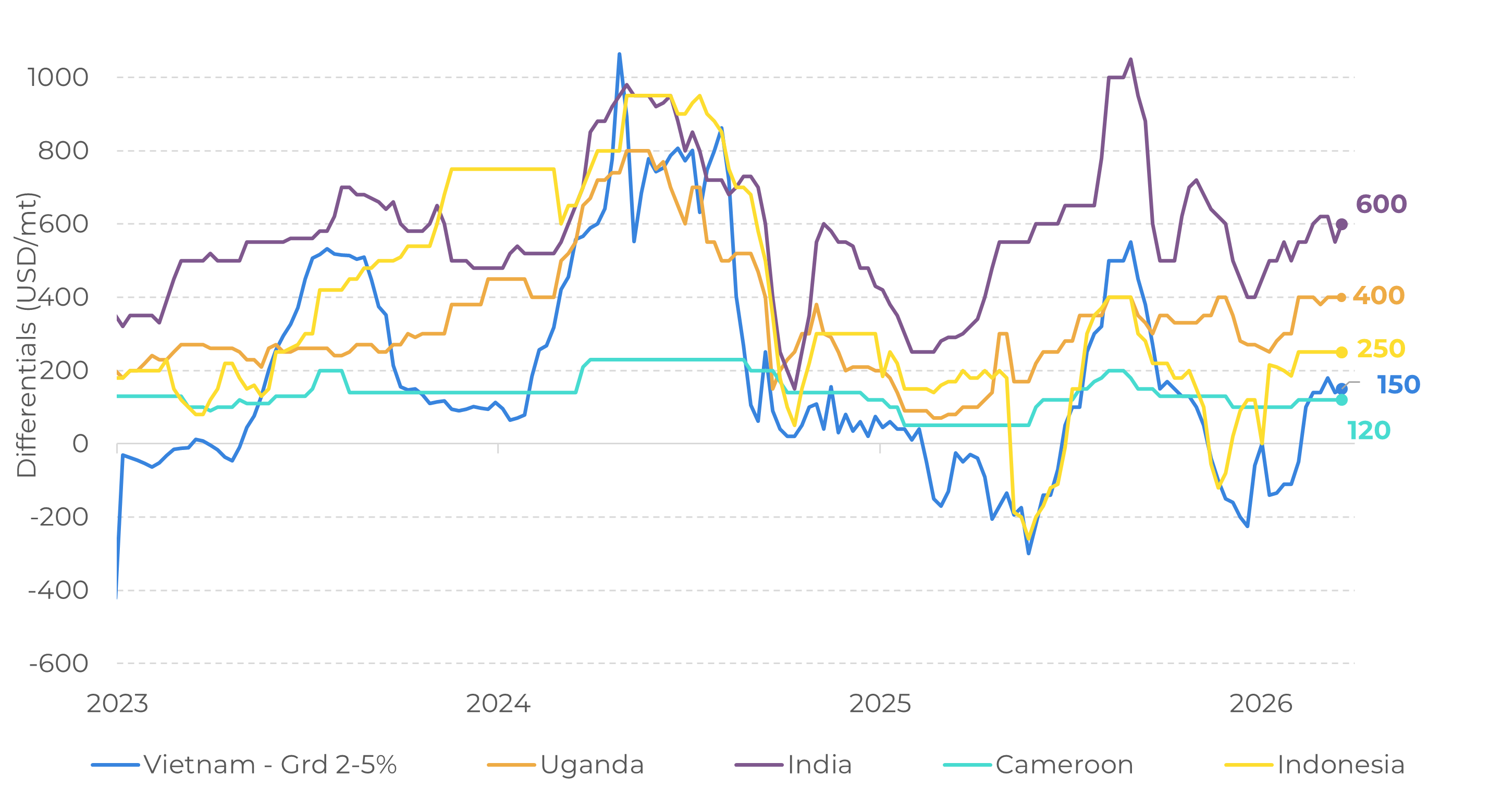

- Other origins are also experiencing rising differentials amid growing concerns over short‑term supply. Arabica and Robusta futures spreads are reflecting these supply-side worries as well.

- At the same time, changes in the macroeconomic environment – marked by higher bond yields and reduced expectations of interest rate cuts in major economies – along with the continuation of an inverted coffee market, may influence import behavior in destination markets and delay stock recovery in the coming months.

Higher risk reduces new sales, triggering differentials and spreads

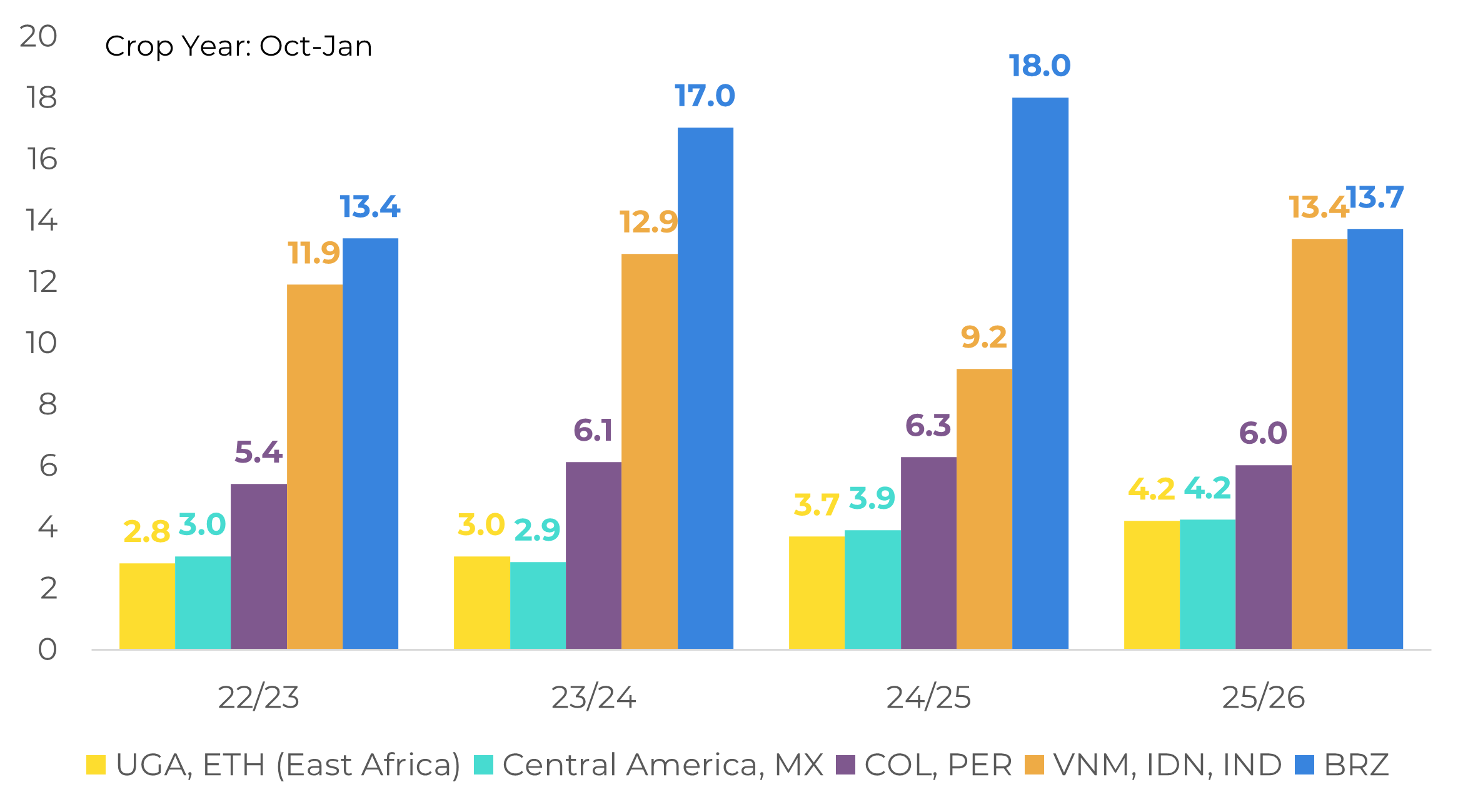

Total Coffee Exports in Main Coffee Regions (M bags)

Source: Cecafé, Vietnam Customs, FNC, UCDA, ICO

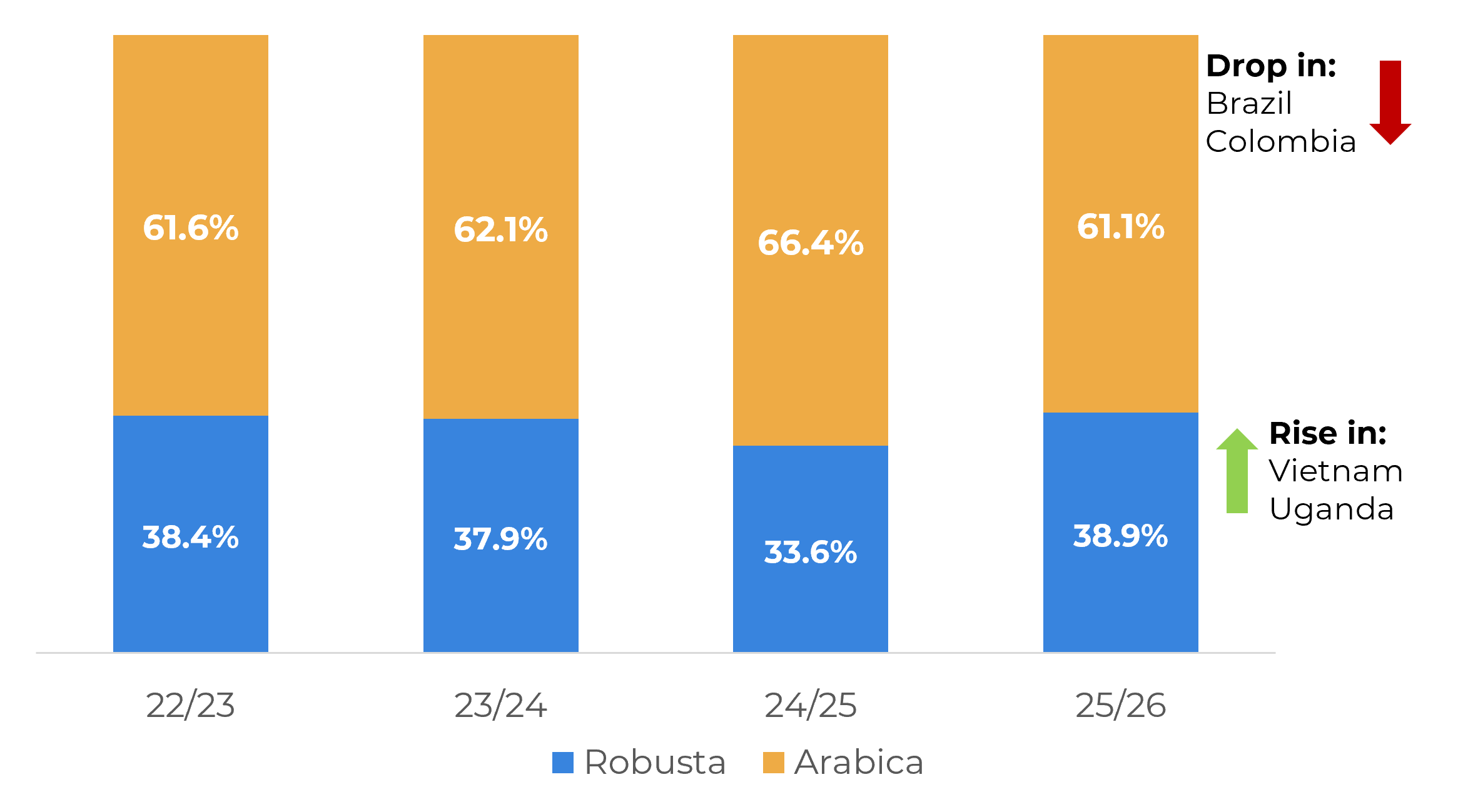

Share of World Green Coffee Exports by Type (%)

Source: ICO

These developments are already raising market concerns and influencing spreads and differentials, particularly as Brazilian farmers continue to sell less coffee than in previous years – reflected in lower export volumes in 2026 – while Colombian exports have also declined due to lower production and a stronger peso. Differentials for both Arabica and Robusta are now higher than at the start of the year, with the most notable shift seen in Brazilian Arabica 17/18 fine cup. After trading at a discount earlier this year, it is now quoted at a premium of over 40 cents/lb. Brazilian farmers remain well capitalized and show little interest in selling carry over stocks.

Arabica differentials (c/lb)

Source: LSEG, Safras & Mercado

Robusta differentials (c/lb)

Source: LSEG

While the medium to long term outlook still points to lower prices amid expectations of a record Brazilian crop, the market structure remains in backwardation, signaling near-term tightness . Front month spreads, which had been narrowing in early 2026, are once again widening, underscoring the market’s sensitivity to supply conditions amid persistent macroeconomic risks. The U.S.–Iran conflict has added inflationary pressures via higher energy prices, complicating inflation anchoring and reshaping monetary policy expectations in major importing economies such as the U.S. and the EU.

It is also important to recall that destination markets have significantly reduced coffee inventories – not only due to supply constraints in recent seasons, but also because of higher financial costs in the post pandemic environment of elevated interest rates. Higher coffee prices in recent years increased working capital requirements, prompting many importers to rely on short term supply while leaving inventories concentrated in producing countries. Although monetary policy began to ease in 2025, interest rates remain high, and renewed geopolitical tensions in the Middle East have dampened expectations of further easing. Combined with an inverted coffee market, this dynamic may reinforce stockholding in origins and lean inventories in consuming regions. At the same time, the prospect of a record Brazilian crop in the coming months allows roasters to continue operating on a hand to mouth buying basis, reinforcing this purchasing model.

As a result, while coffee supply may remain physically available in producing countries, it is less likely to flow smoothly toward consumption hubs. This implies that the market will remain highly sensitive not only to supply disruptions – whether at origin or along logistics routes – but also to any unexpected surge in demand. Therefore, while prices may continue to trend lower overall, the risk of renewed rallies should not be overlooked.

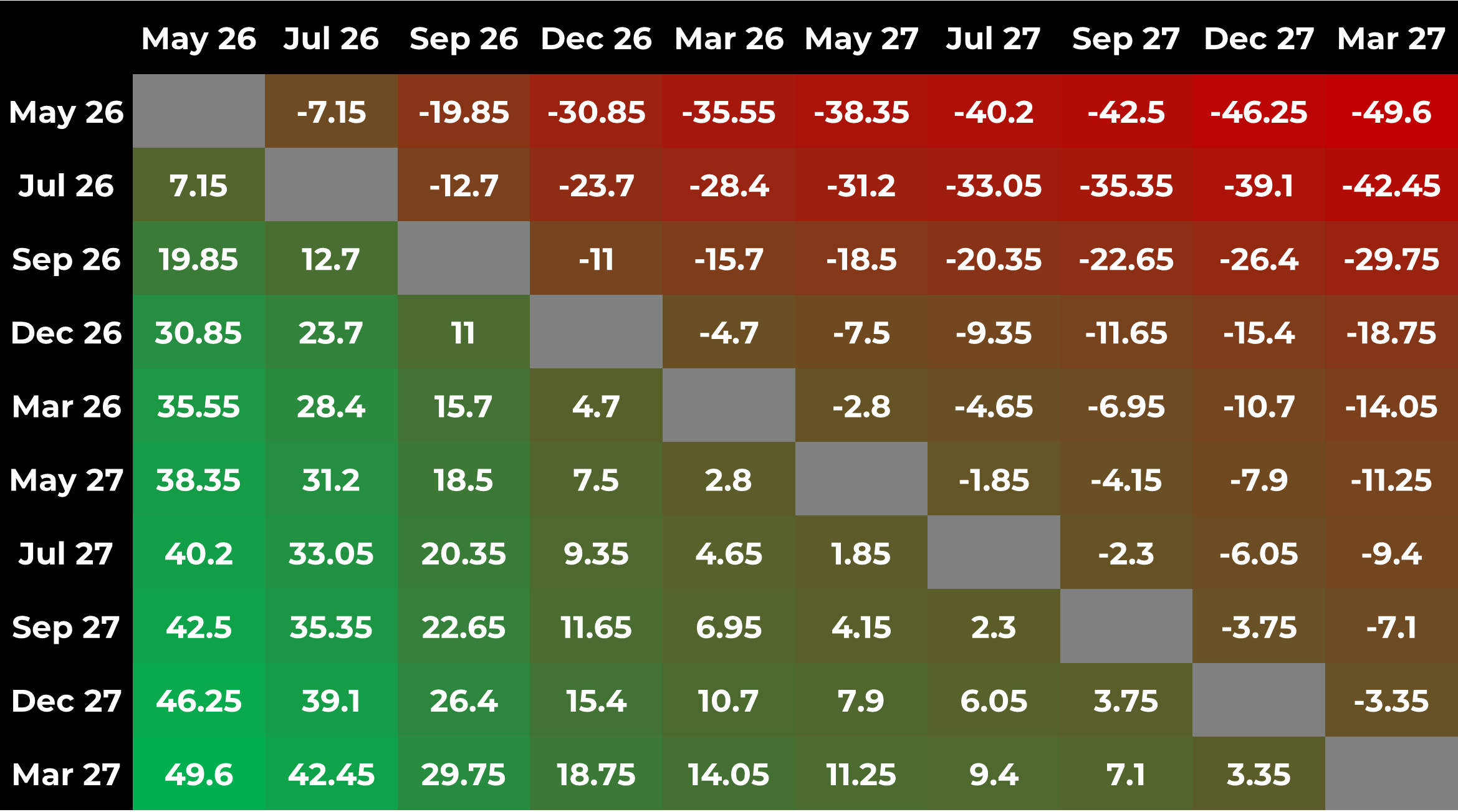

Arabica: Spread Matrix (c/lb)

Source: LSEG, Hedgepoint

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.