Live with Experts – Coffee Market Highlights

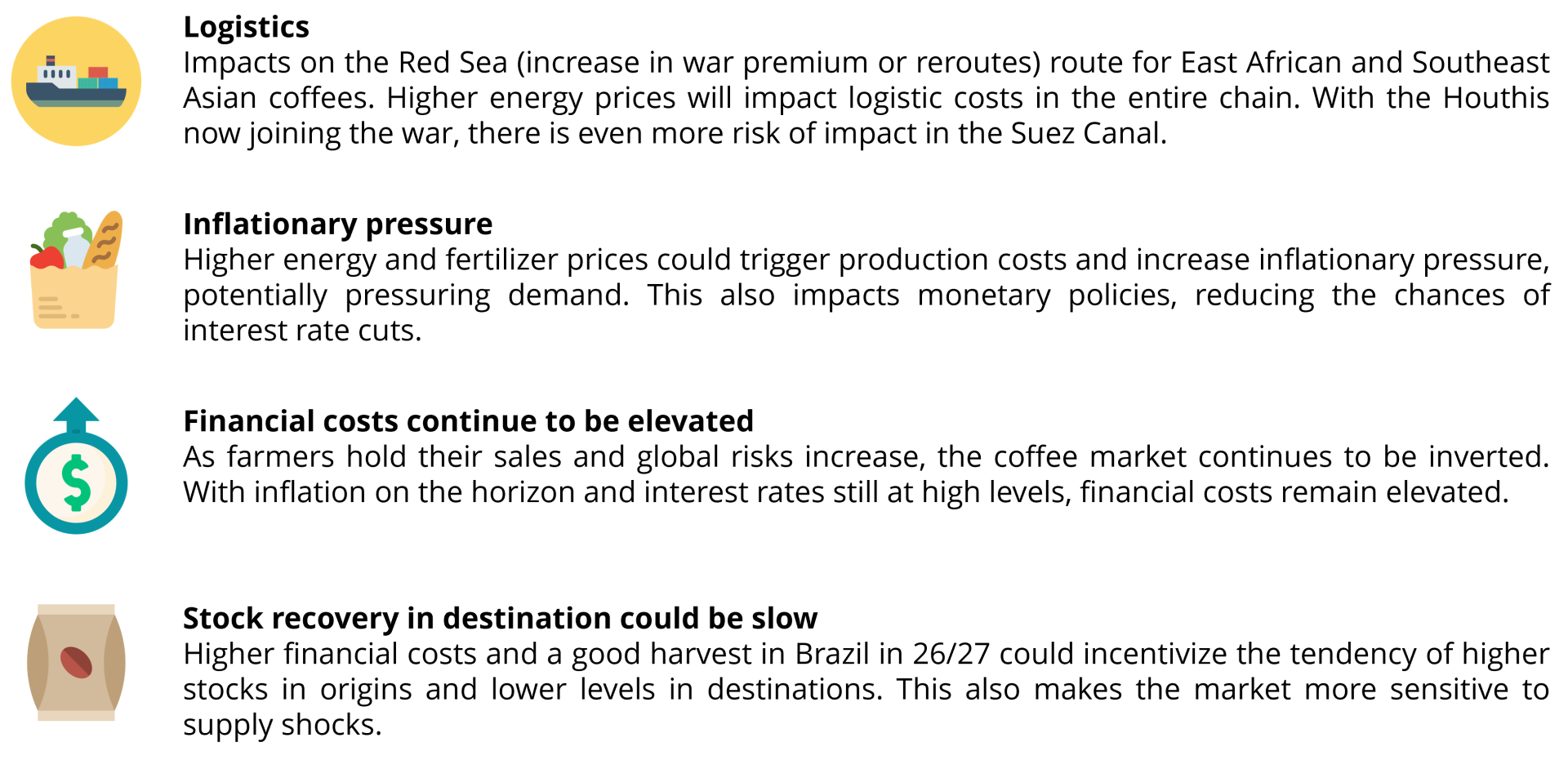

U.S.-Iran war impacts global markets

As the conflict is prolonged, inflationary pressures also increase, with growing fears of stagflation. U.S. yields have also grown since early this year and are more sensitive to new inflation indicators and possible changes to the Fed’s monetary policies, as this scenario could leave less space for central banks to cut interest rates.

U.S.-Iran Conflict: The main impacts for coffee

Source: Hedgepoint

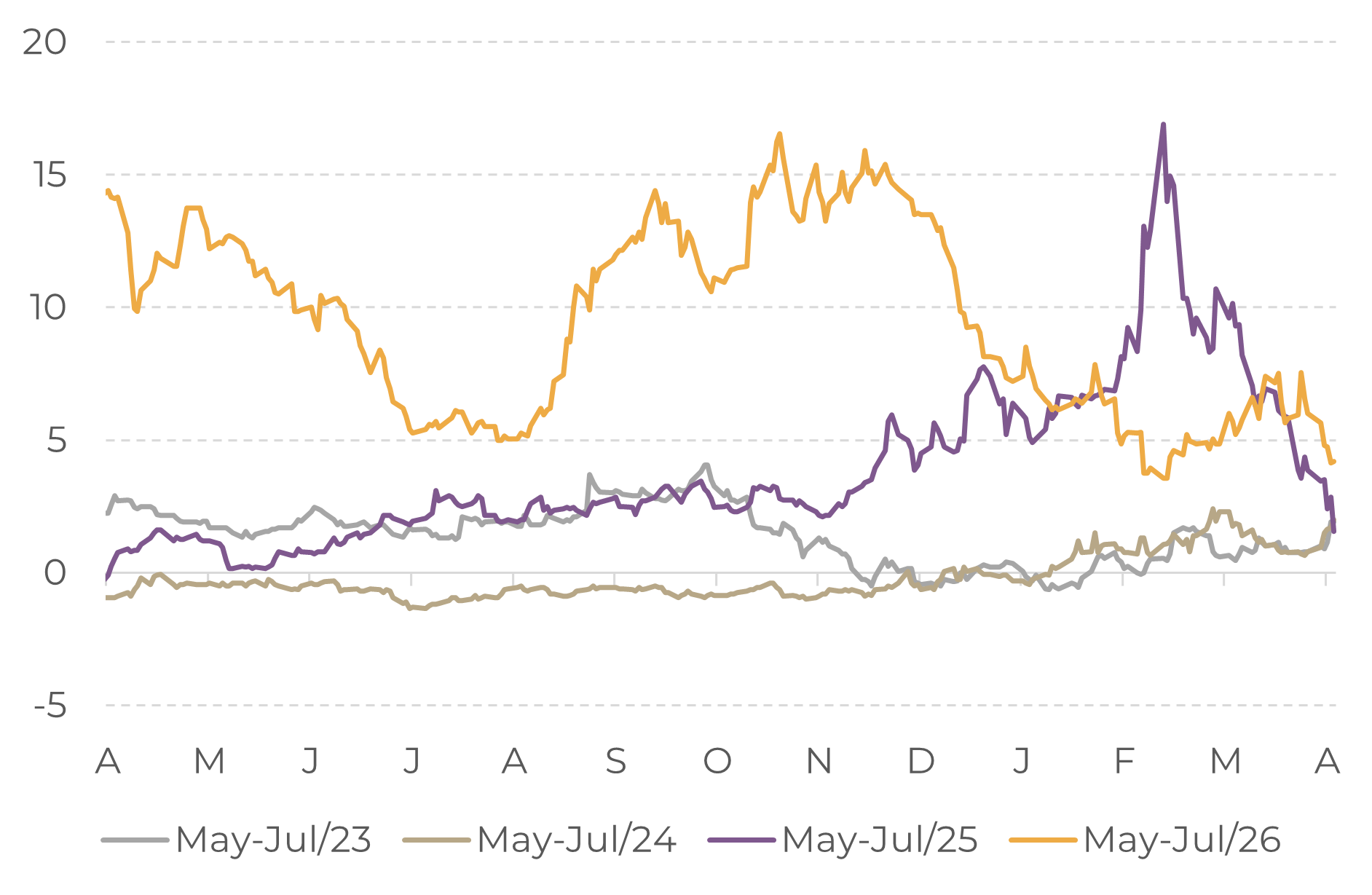

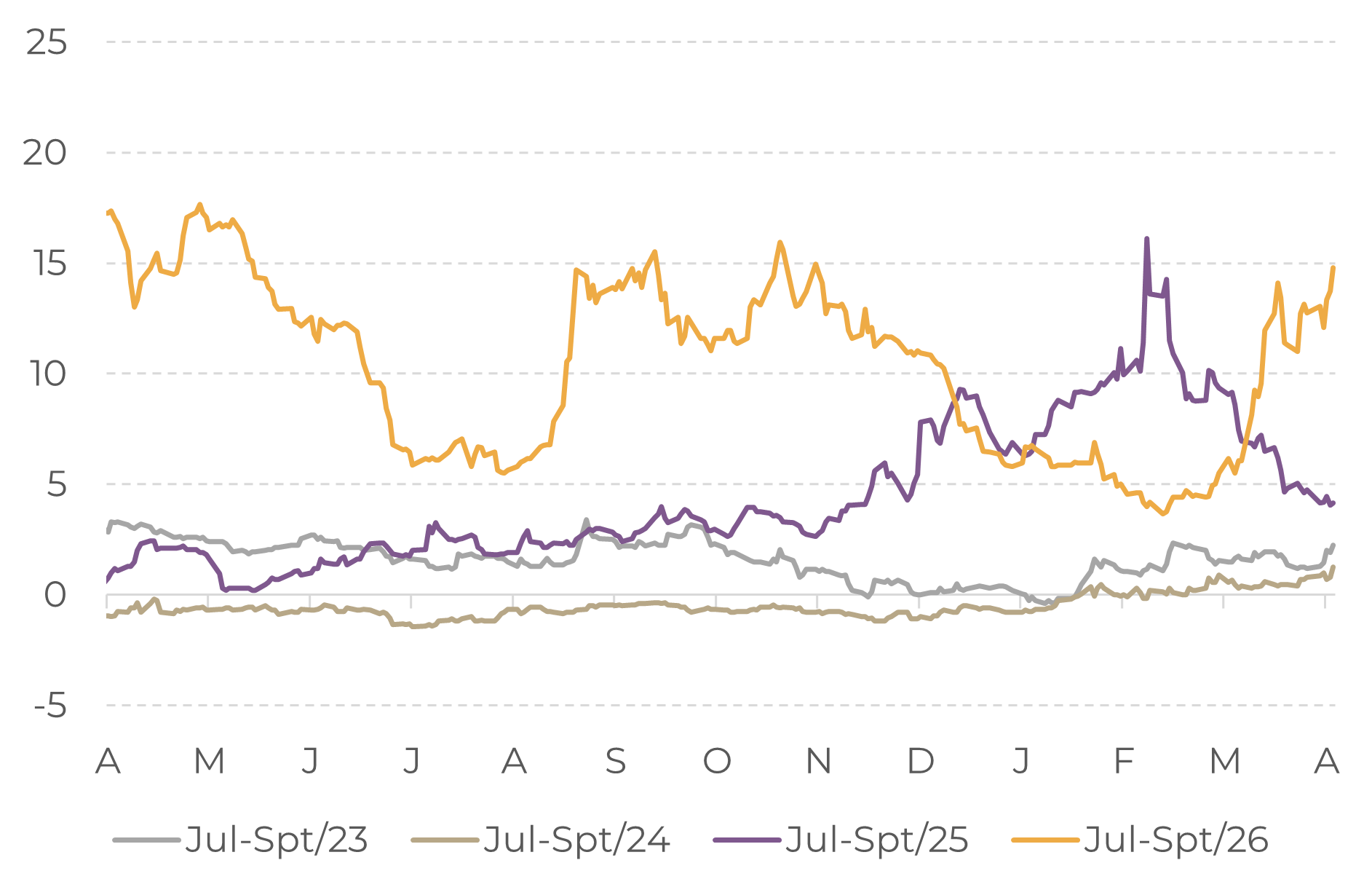

Market structure could impact stock recovery

After a sharp drop early this year, spreads for near-term contracts increased, especially the July-September one, reflecting the worries over short-term supply, as farmers continue to hold new coffee sales, especially in Brazil.

This has also been reflected in differentials as the 25/26 harvest is now completed in other key origins and, with no additional harvest-related cash needs, farmers and exporters are reassessing the risks posed by rising production and logistics costs, with sales tepid.

Meanwhile, as the world focuses on Brazil, farmers still hold their sales, triggering differentials early this year. Normally, at this time of the year, Brazilian farmers would be selling more coffee, raising doubts about farmers’ willingness to sell.

Arabica: May-July Spread (c/lb)

Source: LSEG

Arabica: July-September Spread (c/lb)

Source: LSEG

Higher financial costs and Brazilian farmers being less active in the past months have also reflected in imports and stocks figures, especially in the EU. The European Union net imports have decreased considerably in 24/25 and 25/26, due to an increase in re-export, higher coffee prices, and carry costs, besides a decrease in selling appetite by farmers. This has also contributed to a decrease in ECF stocks, and, with the current inverted market, this trend is likely to continue

In other destinations, however, the scenario is a little more hopeful. Although U.S imports were affected by tariffs in 2025, January figures point to a recovery in 2026, especially with an expected record crop in Brazil. Asian countries, on the other hand, are showing higher import figures in 25/26. However, the current market structure could still limit stockpiling in these countries.

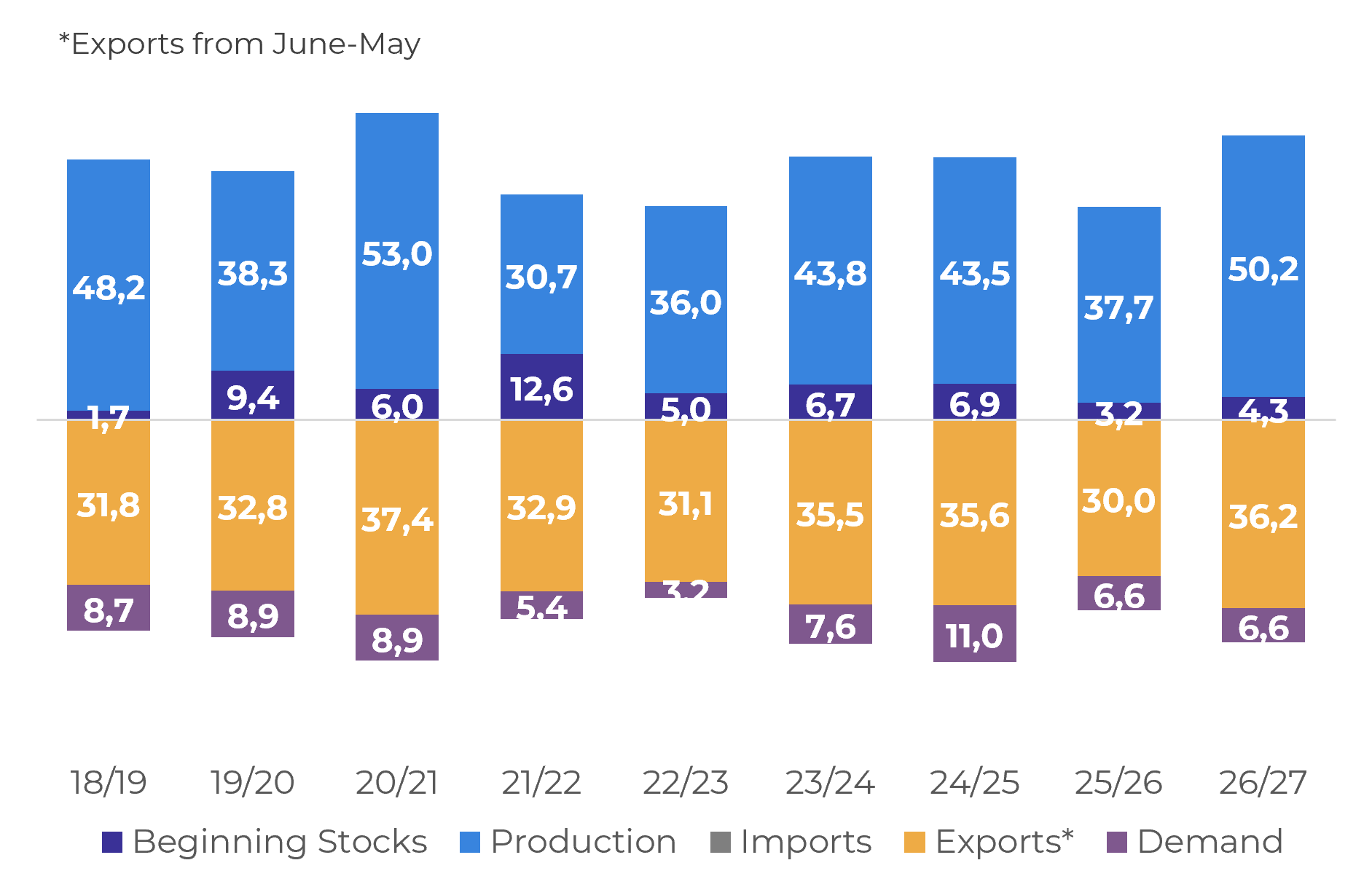

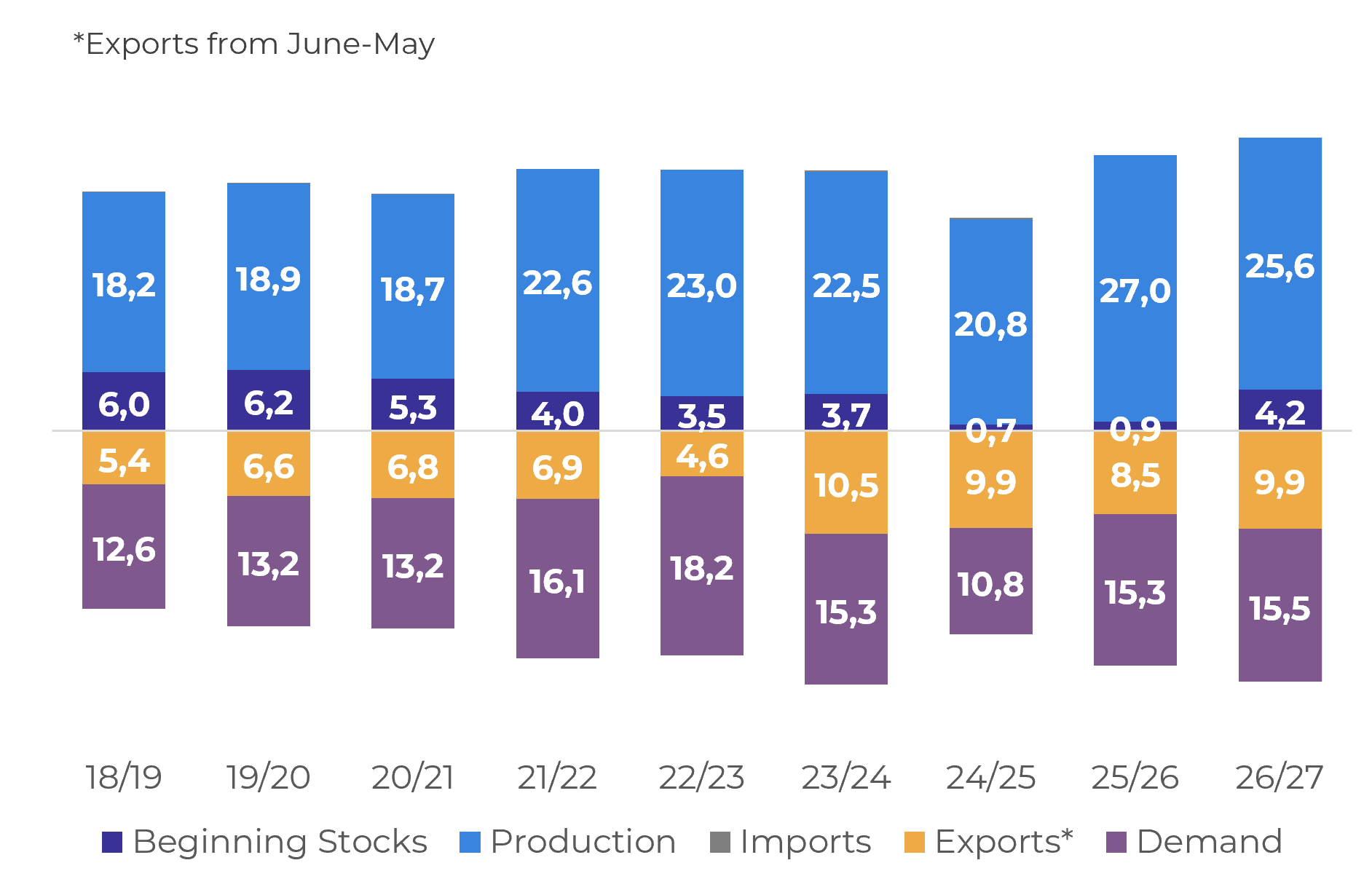

All eyes on the 26/27 Brazilian season

In the past months, a good volume of precipitation was recorded in all coffee-producing regions, contributing to the beans’ filling, which will likely reflect in an increase in processing yields. Favorable weather and an increase in investments (and area) in the past years will lead to higher production in the country in 26/27, driven by a recovery in Arabica production and still good figures in Conilon.

Brazil: Arabica Supply and Demand (M bags)

Source: Hedgepoint

European Union cumulative disappearance (M bags)

Source: Hedgepoint

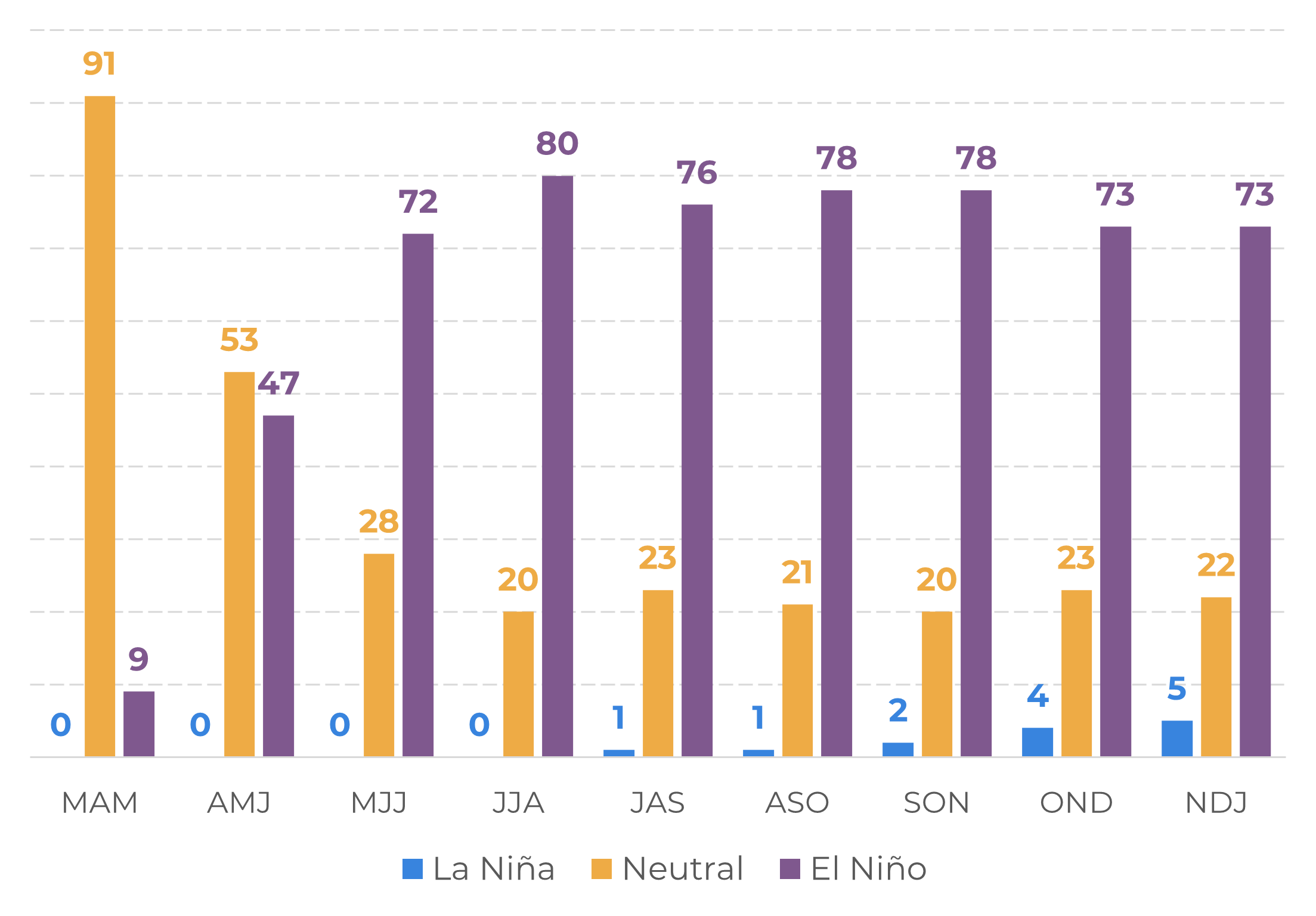

El Niño increases risks for other origins

The chances of a La Niño in May-June have risen, likely extending until early 2027. The major impacts for coffee regions are:

• Central America: It can reduce hurricane activity and rain, even leading to drought in some regions. Also, temperatures could increase significantly.

• Southeast Asia: It can increase hurricane activity in the Pacific and bring storms to Vietnam and part of Indonesia but can also bring drought to the southeast of the country.

• East Africa: It can bring floods in the south of Ethiopia. In the northern part of the country and in Uganda, it can cause drought. Temperatures also tend to increase.

Official IRI ENSO Probabilities (March 2026, %)

Source: International Research Institute for Climate and Society

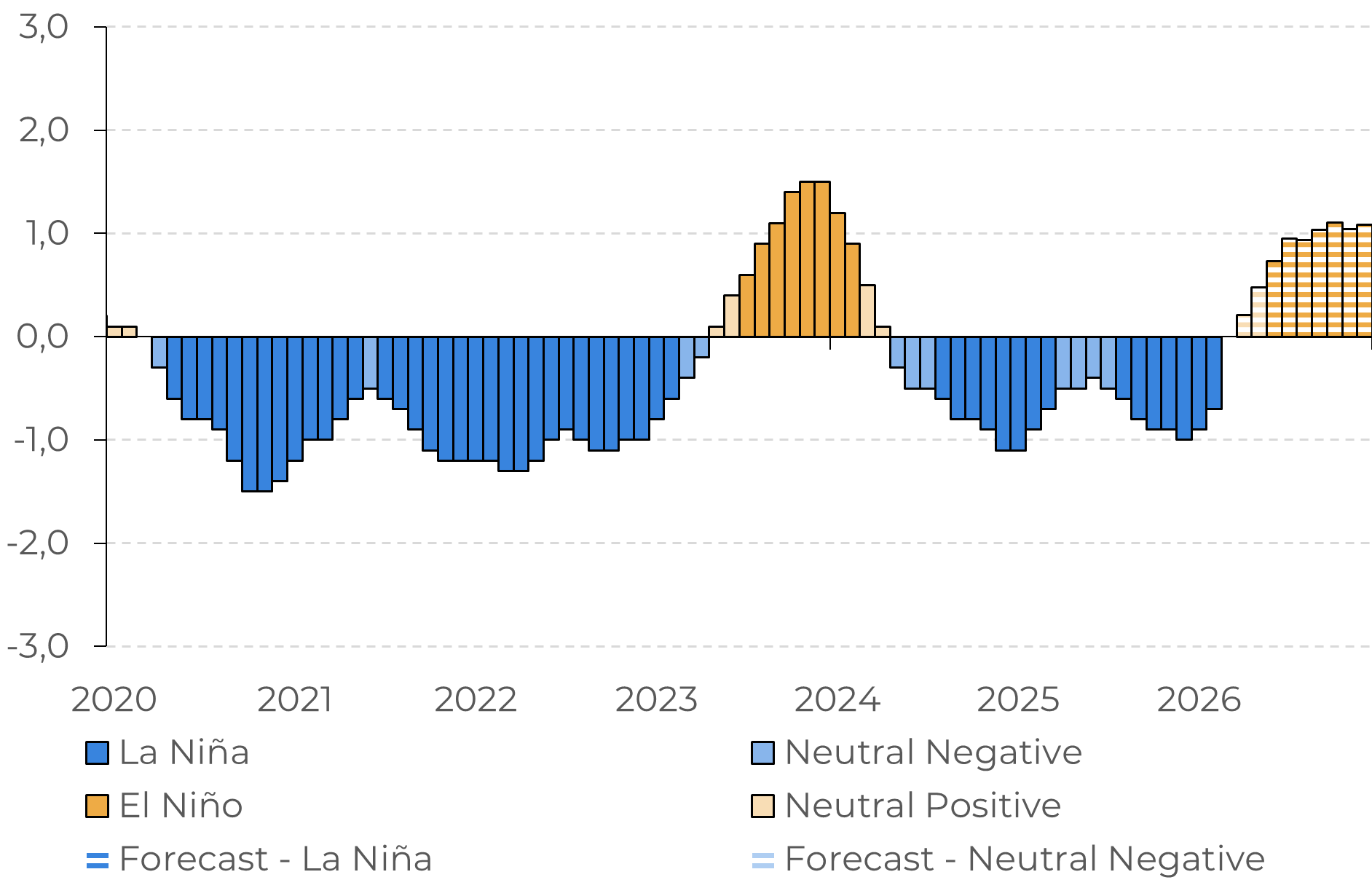

Forecasted Sea Surface Temperature Anomalies (in ºC) in the Nino 3.4 Region

Source: International Research Institute for Climate and Society

Current models also point to a significant increase in the Pacific temperatures at the end of 2026, which could translate into a strong event in this period. This is especially significant as, aside from Indonesia, all other producers are in their main development period for the 26/27, with weather playing a key role in production figures and global surplus. A strong El Niño could affect trade flows.

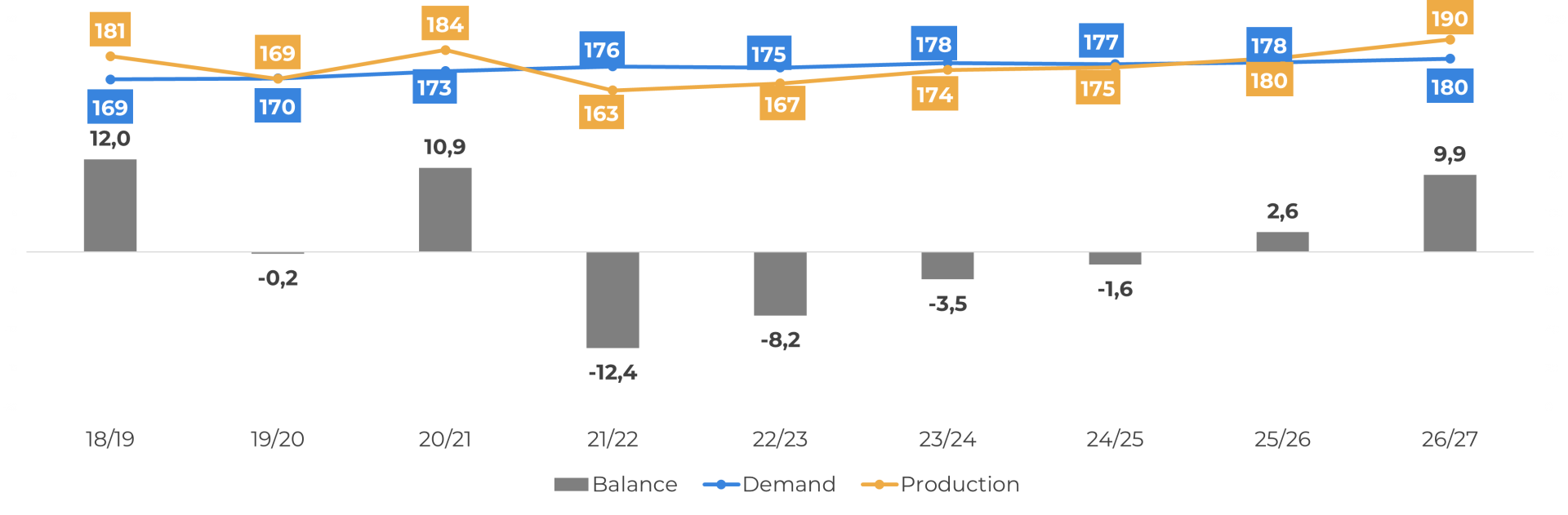

Global balance and summary

After a few seasons in a tight scenario, coffee balance could finally see a significant surplus in 26/27, mainly due to the record crop in Brazil. However, it is important to note that, with other origins in the development period, the size of this surplus could change. We are also taking a more conservative approach regarding demand.

Hedgepoint: Global Coffee Supply and Demand (M bags)

Source: Hedgepoint

With this, the landscape for prices is bearish, but not without volatility. The record crop in Brazil is expected to put downward pressure on prices. However, some key points in the market could lead to periods of upside:

• Low farmer selling and high differentials.

• An inverted market and high financial costs make prices more sensitive to changes in supply.

• Low stocks in destinations may trigger a price hike as buyers enter the market.

• El Niño could affect production.

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

carolina.franca@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.