Live with Experts – Coffee Market Highlights

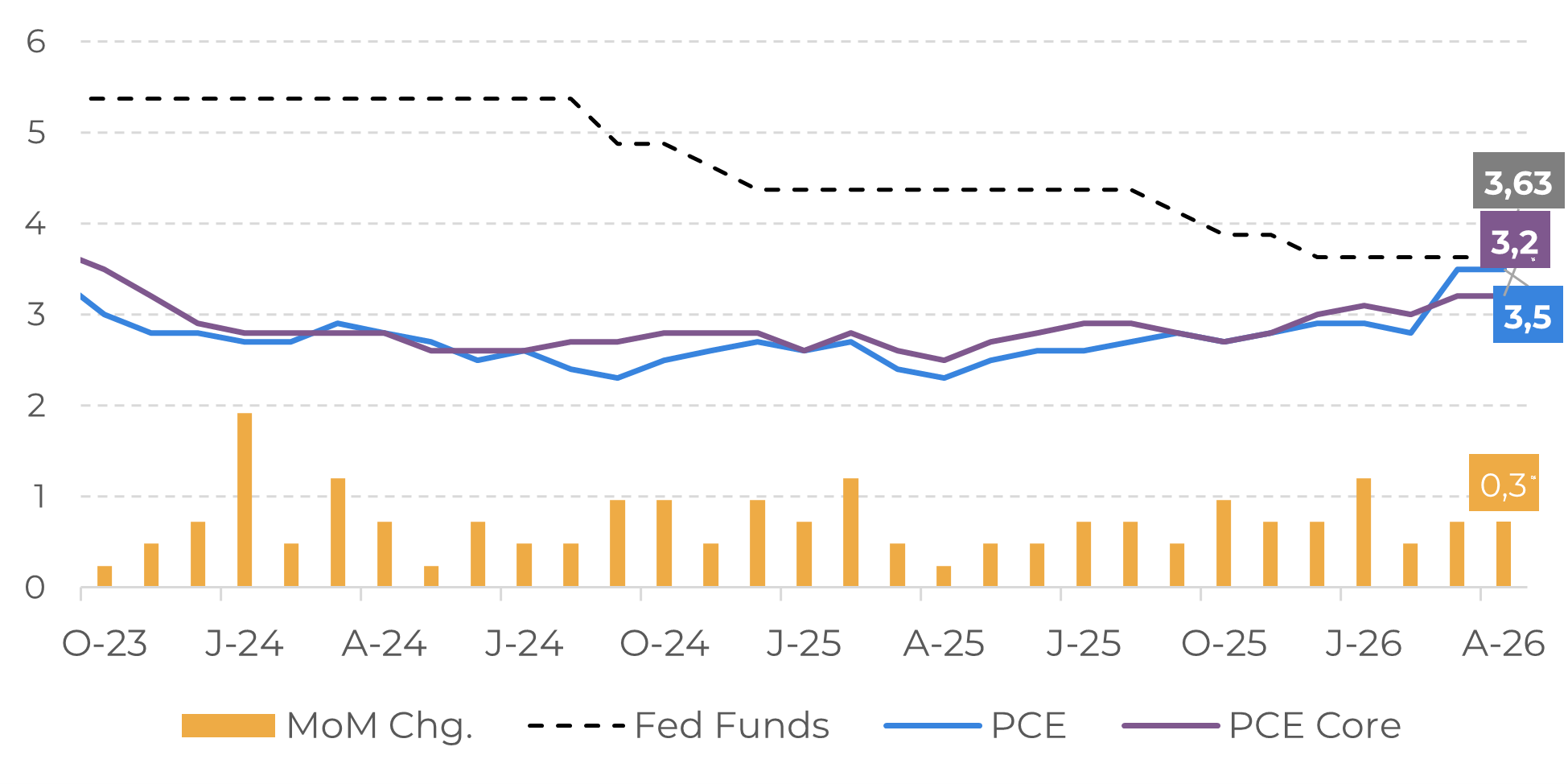

Macroeconomic and price overview

Fed Funds, PCE, and PCE Core

Source: LSEG

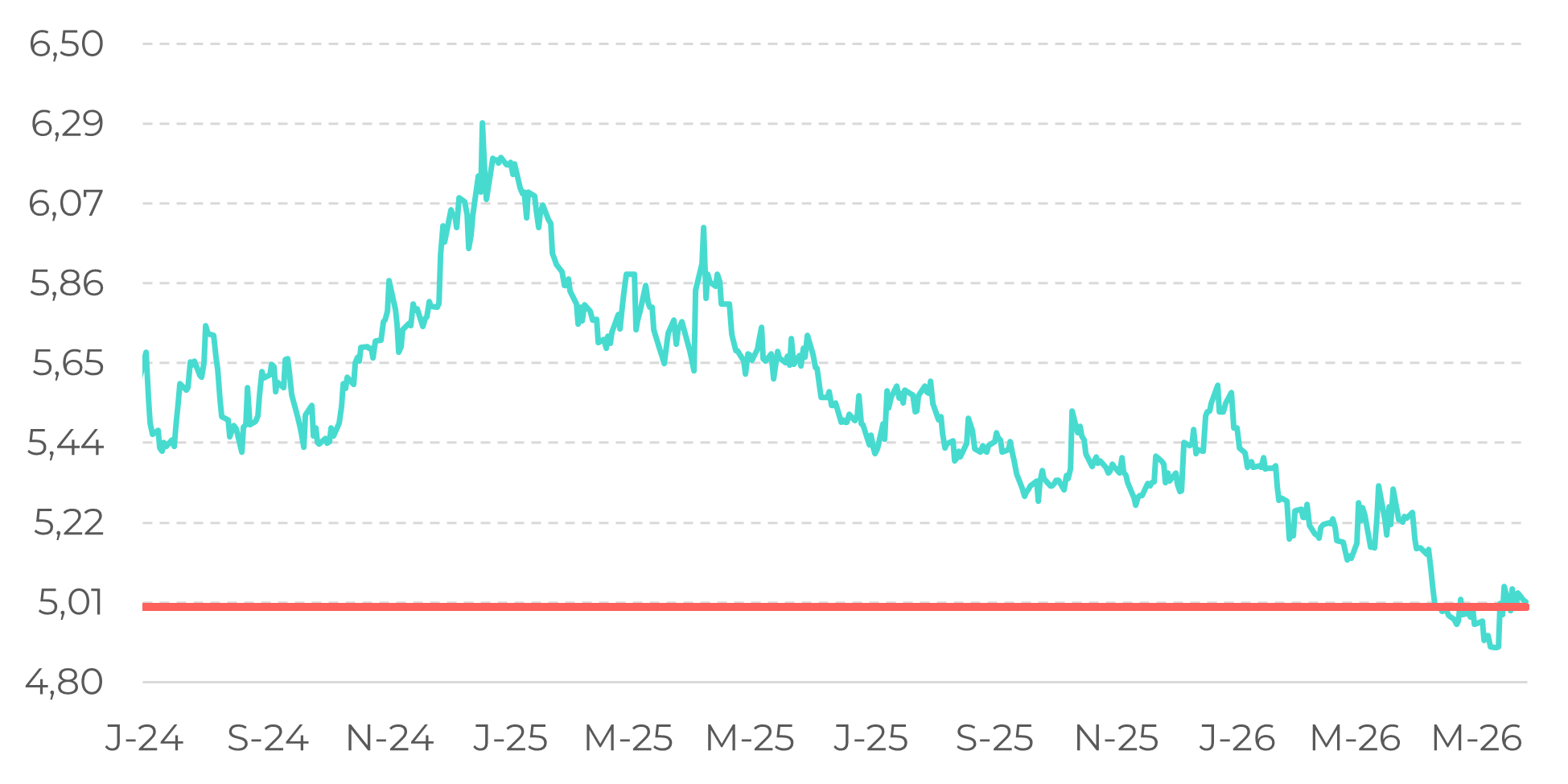

BRL at its highest levels in 2-years

Source: LSEG

For coffee, another point of attention in the BRL valuation in 2026, which is also potentially impacting Brazilian coffee exports, as farmers now receive less for shipments. Although possible changes in US policy could reduce the rate differential with Brazil, the BRL is still benefiting from the carry trade and foreign investment in Brazil, operating at its highest value in years.

Regarding coffee prices, a record crop in Brazil in the 26/27 season puts downward pressure on prices. But the short-term low availability in other origins and lower farmer selling in Brazil is capping part of the movement. The worries over the El Niño could also limit bearish momentum. However, if supply from Brazil becomes more comfortable in the market, corrections are expected.

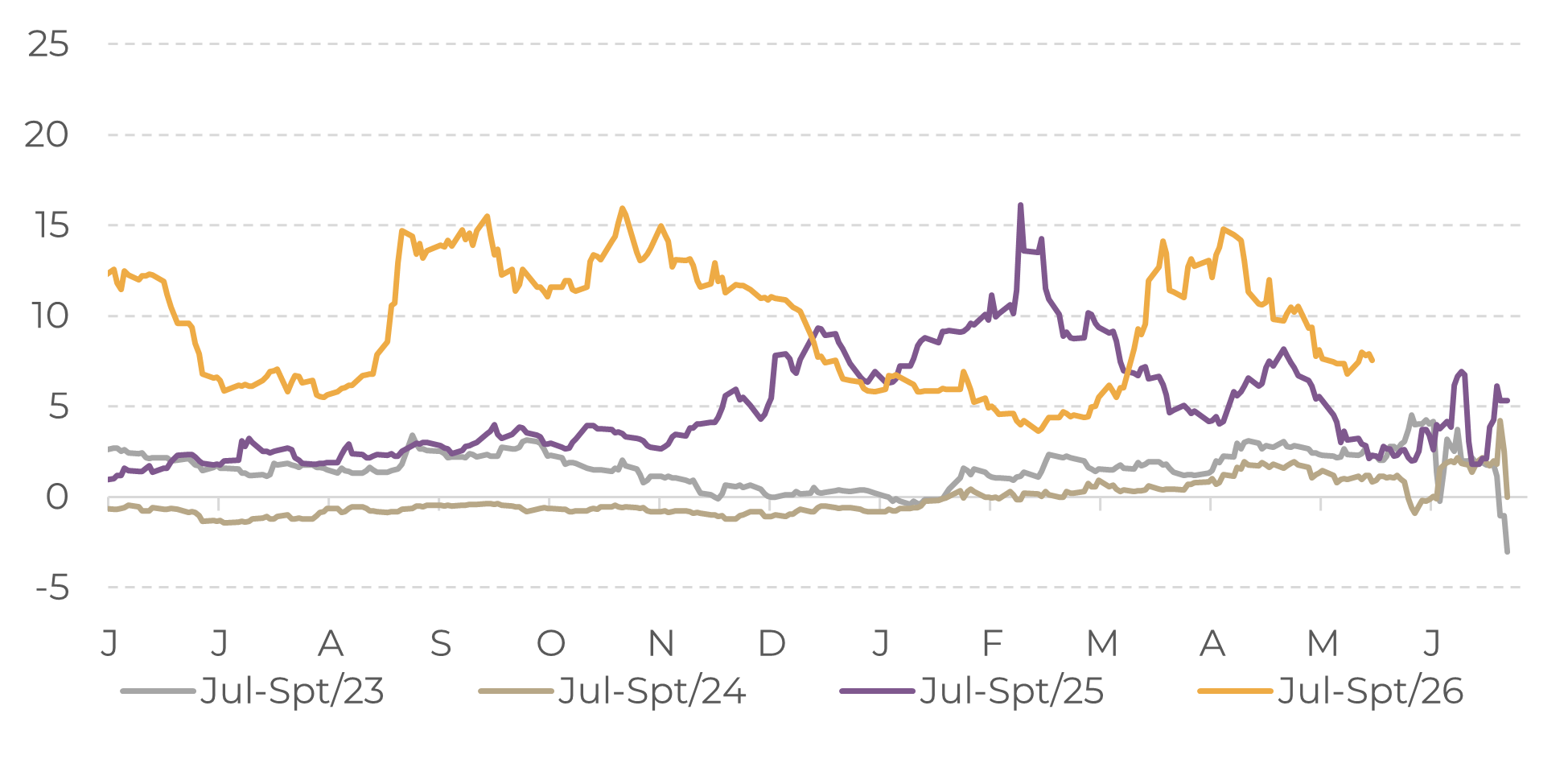

Arabica: July-September Spread (c/lb)

Source: LSEG

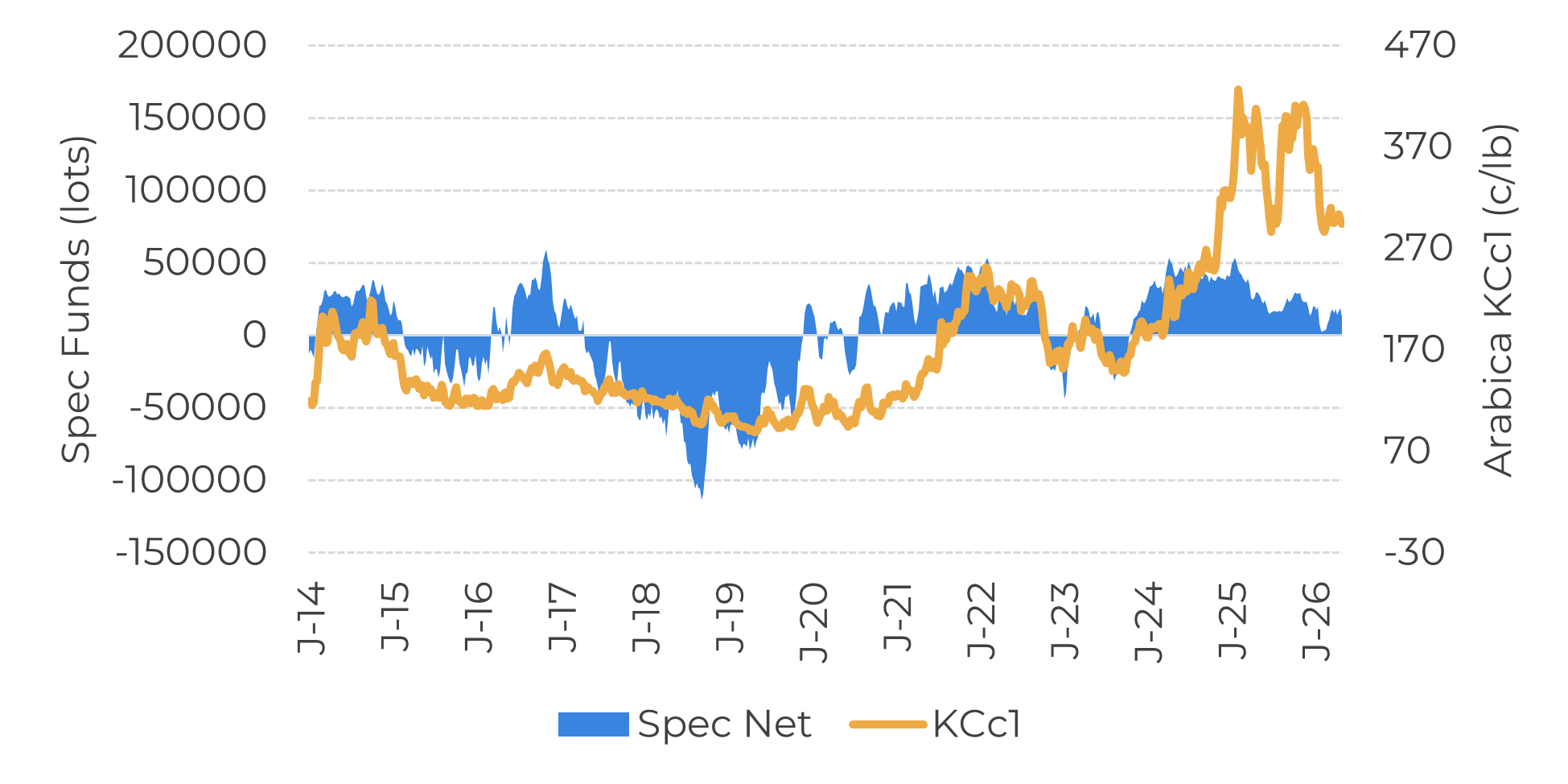

Arabica: Speculative Funds Net Position (lots) and First contract (c/lb)

Source: CFTC

Looking at spreads, Arabica July-September still indicates an inverted market, although levels are lower than in previous months. Higher spread levels also increase financial costs and can impact stock recovery in destinations, as it is more expensive to build stocks.

On the other hand, funds are showing a more bearish market. While net speculative funds' position is still long, they have trimmed their net position in recent months, in light of the substantial Brazilian crop in 26/27. This shift in position also occurred at a time when open interest was increasing, signaling a slightly bearish trend. For funds to go short, however, the supply needs to be more comfortable.

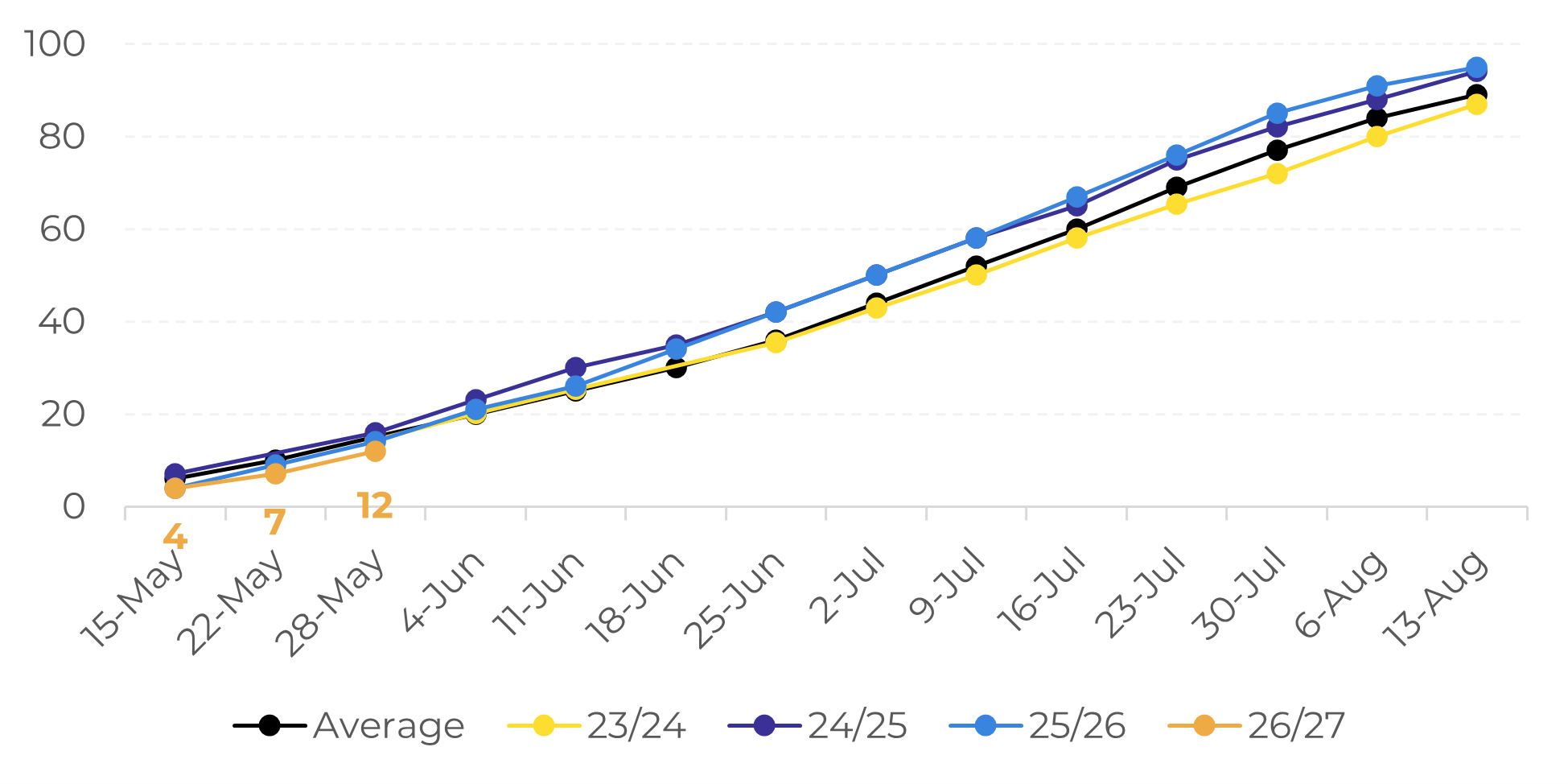

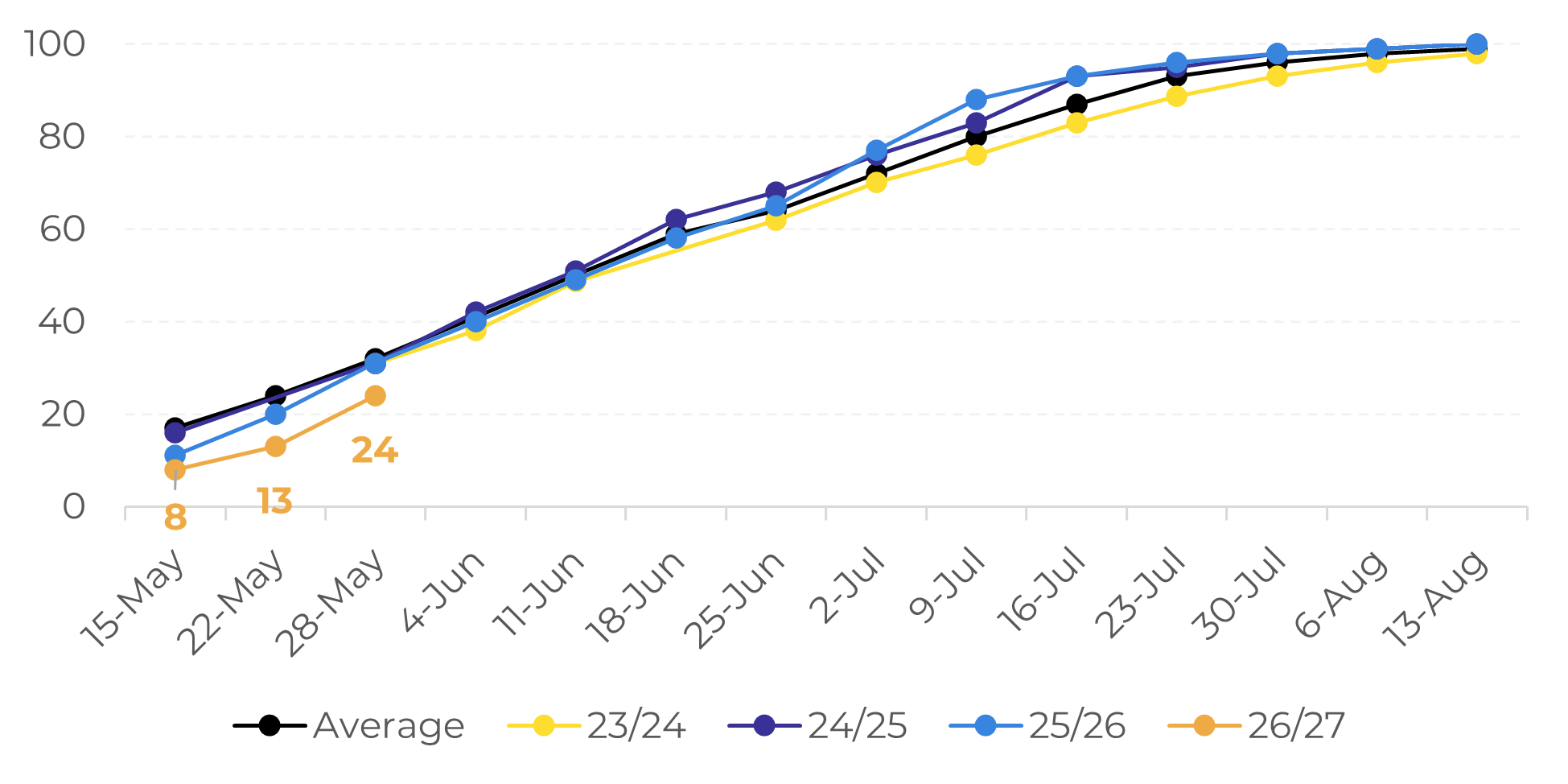

Brazilian 26/27 harvest to gain pace

Due to delays in 2025 flowering and the record coffee volume in 26/27, the harvest pace is behind previous cycles. For now, reports show an increase in screen size and good cup quality, although more definitive figures will only come after June, when harvest is expected to gain pace, given the current volume of green beans.

Brazil: Arabica Harvest Rate (% of total)

Source: Safras & Mercado

Brazil: Conilon/Robusta Harvest Rate (% of total)

Source: Safras & Mercado

Despite the proximity to the harvest, farmers refrained from selling large volumes of coffee, with commercialization in the country below that of previous years. Forward sales for the new season are also below average levels, especially as future prices continue below those from the physical market. This has also been reflected in 25/26 export figures, although the US tariffs also impacted the Brazilian[LC1.1] shipments early in the season.

Other origins’ availability is tight

As most Arabica origins are now in their off-season, with stocks decreasing and farmers waiting for better prices, differentials started to increase. In Brazil, although lower than in early 2026, differentials are still high. In Colombia, not only the 25/26 season has a decrease from 24/25, but a stronger peso has also been limiting exports from the country and supporting differentials.

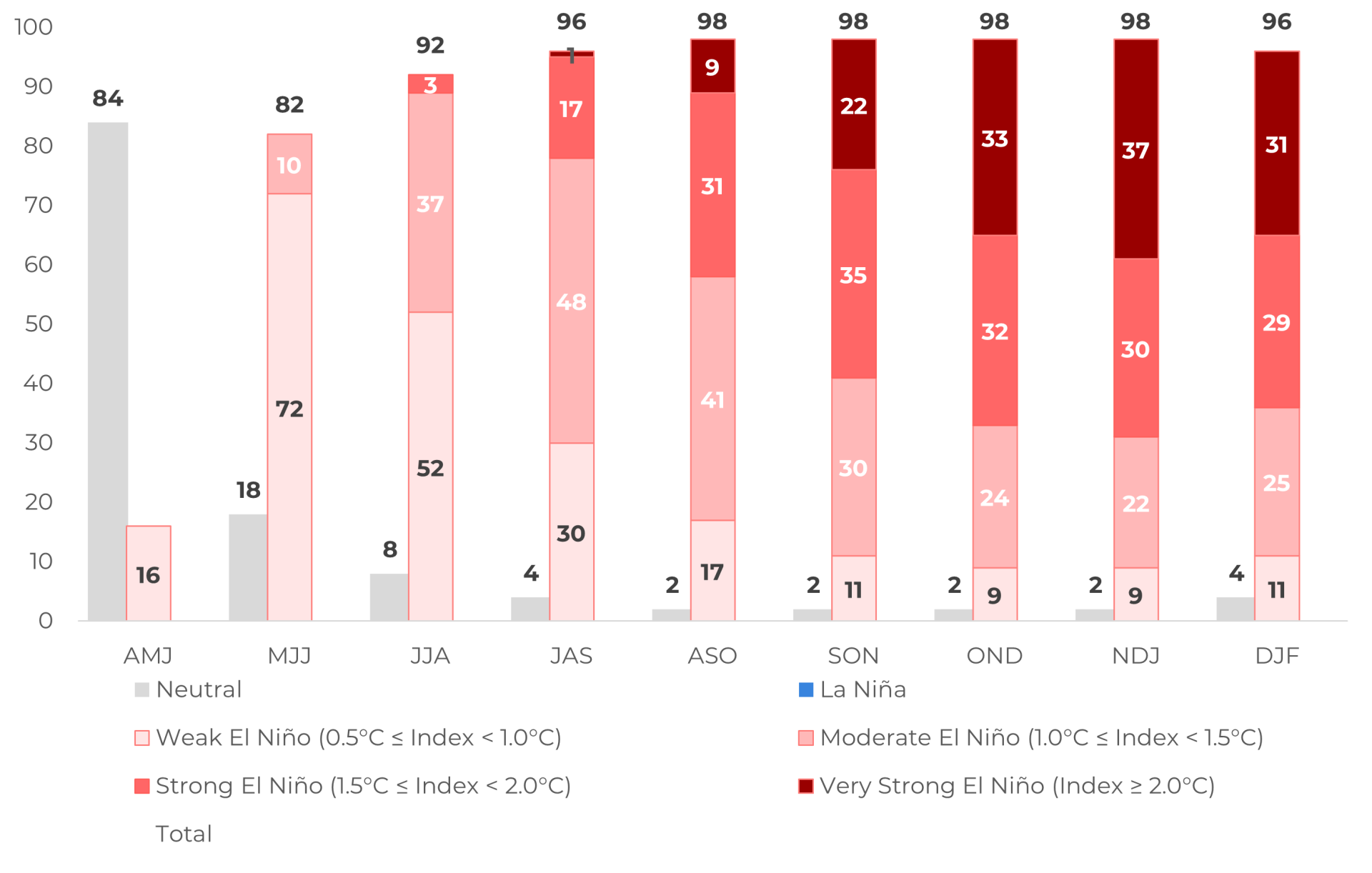

El Niño poses a risk to the supply

Official NOAA ENSO Probabilities and Strength (May 2026, %)

Source: NOAA

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.