The coffee rollercoaster: Is there a change in fundamentals?

- Arabica coffee prices had a stellar rally on Monday, 06, hitting their fourth-largest daily gain on record in the prior session, nearing 360 c/lb. Robusta prices also followed the trend, with volatility for both varieties increasing substantially.

- Prices have then reverted part of the gains but continued to be highly volatile throughout the past few days, with strong intra-day variations.

- However, there has been little change in fundamentals. While the delay in the harvest in Brazil and the El Niño supported prices, the momentum was amplified by funds' positions and short coverings.

- As destinations remain with limited stocks and farmers selling in Brazil remain lower than in previous years, the market will likely remain sensitive to any supply-related news.

The coffee rollercoaster: Is there a change in fundamentals?

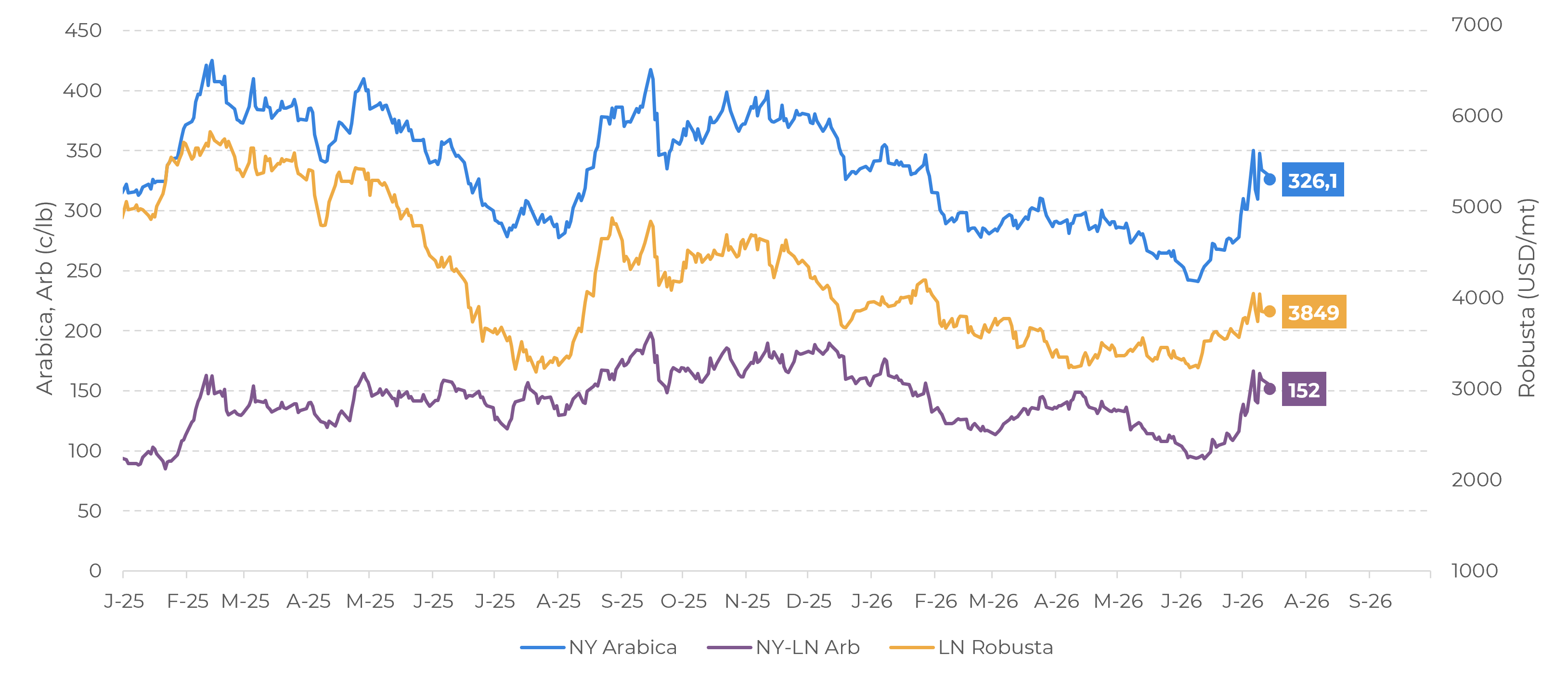

LN-Robusta (USD/mt), NY-Arabica and Arbitrage (c/lb)

Source: LSEG

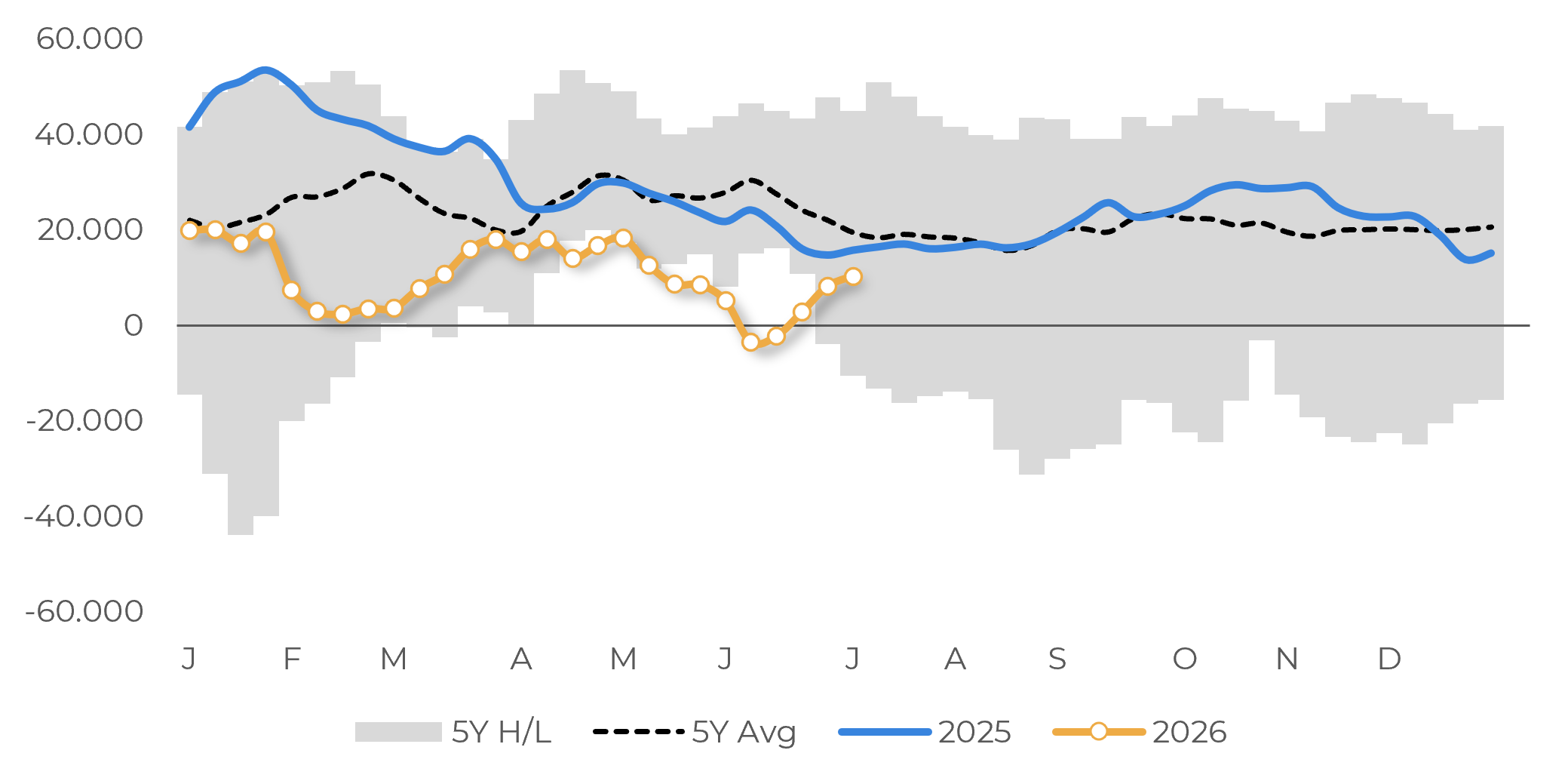

Prices then plunged over the following two days before staging another sharp reversal on Thursday, as volatility remained elevated with significant intraday swings. While market fundamentals provide some bullish support, recent price action appears to have been driven primarily by technical factors and funds positioning. CFTC data from July 7 showed an increase in speculative funds' net long positions in recent days.

As Arabica futures broke through key resistance levels and long-term moving averages in early July, fresh buying interest emerged. At the same time, the Intercontinental Exchange (ICE) increased margin requirements for coffee futures. This reduced market liquidity and prompted many commodity funds to adjust or close positions, contributing to exaggerated one-way price moves. As prices rose and margin requirements increased, margin calls triggered additional short-covering activity, further pushing prices higher in an environment where algorithmic trading amplified market reactions.

Fundamentals, on the other hand, have had little change in the past weeks, but have also been contributing to market volatility, especially with an increase in the short to medium-term risk. While the El Niño has increased the risk for many producing countries in 26/27 and potentially to 27/28, stocks in most destinations have still not recovered, making the market more sensitive to any potential changes in supply. Meanwhile, ICE-certified stocks continue to decrease and, although ICE stocks are only a small part of global coffee stocks, they have become an important proxy in recent months, particularly as inventories have become more concentrated at origin, especially in Brazil. This short-term supply concern has also been reflected in the September–December Arabica spread.

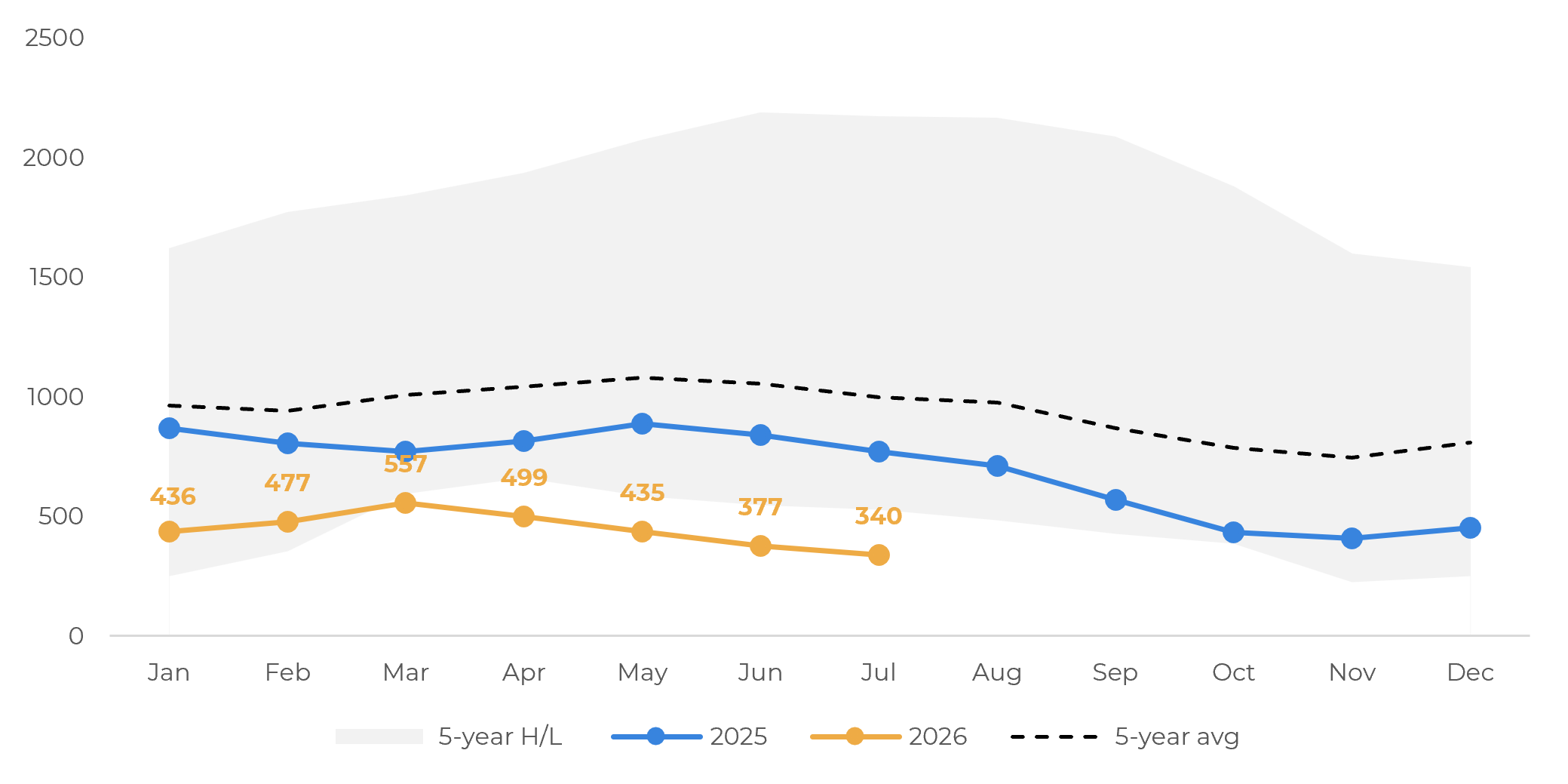

In July alone, Arabica certified stocks declined by more than 32,000 bags, bringing the year-to-date reduction to over 110,000 bags. As some market participants have relied on certified stocks to meet delivery obligations, inventories at origin have tightened due to the seasonal low point in supply, while elevated differentials have continued to discourage certification. Brazil, in particular, has significantly reduced its participation in the certification process since last year as a result of historically high differentials. Even though differentials have softened more recently with the advance of the harvest, certification activity has yet to gain meaningful traction.

Arabica: Speculative Funds Position (lots)

Source: CFTC

Arabica: ICE Certified Stocks (lots)

Source: ICE

Regarding the Brazilian harvest, weather conditions have become more favorable for fieldwork despite rainfall reported in some regions over the past few days. However, due to the persistent rains recorded in June, the 2026/27 Arabica harvest remains behind schedule, with approximately 48% of the crop harvested as of last week, compared with the five-year average of 53%. Robusta harvesting is also slightly lagging, reaching 78% versus the historical average of 81% (see report here).

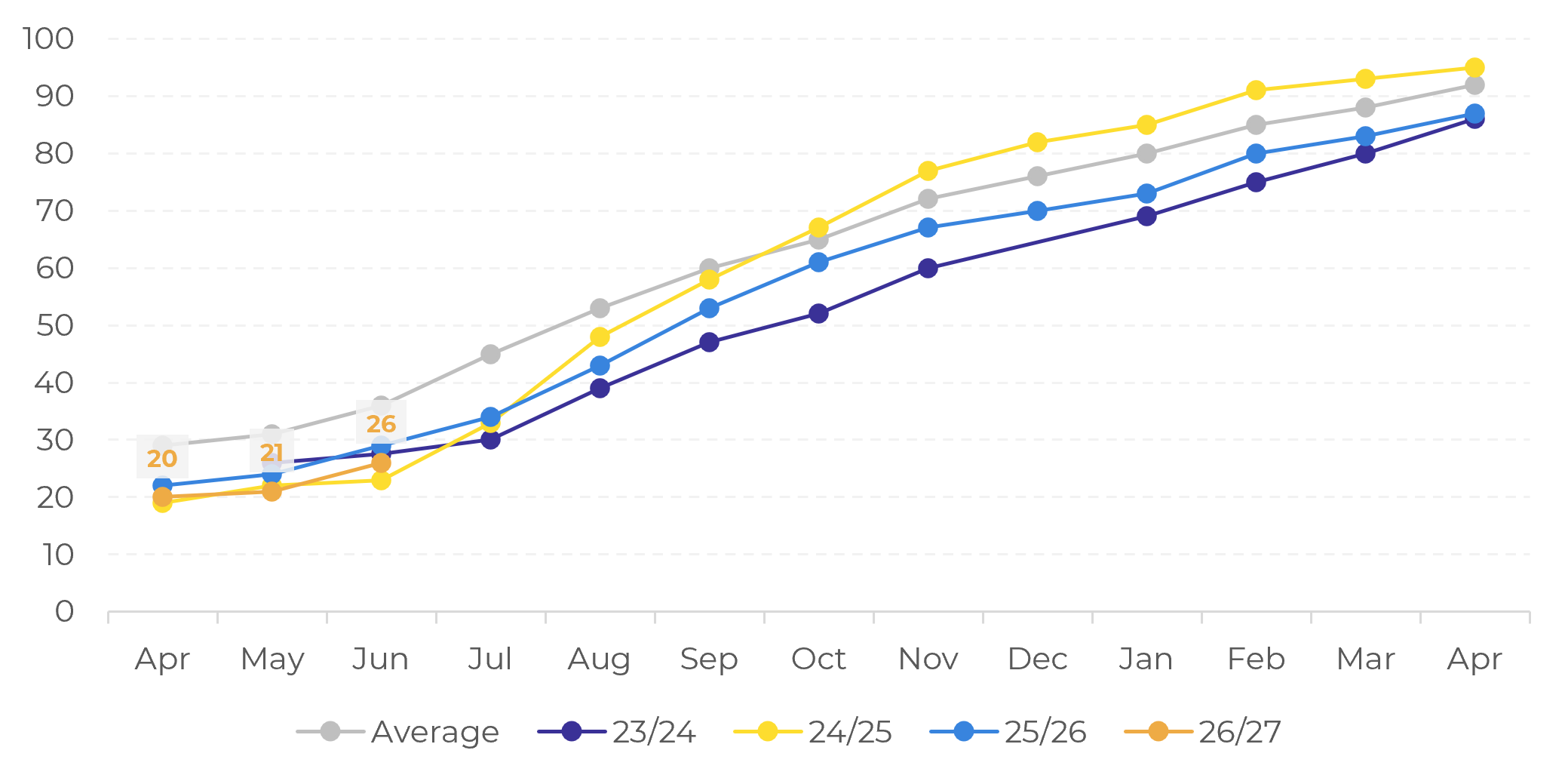

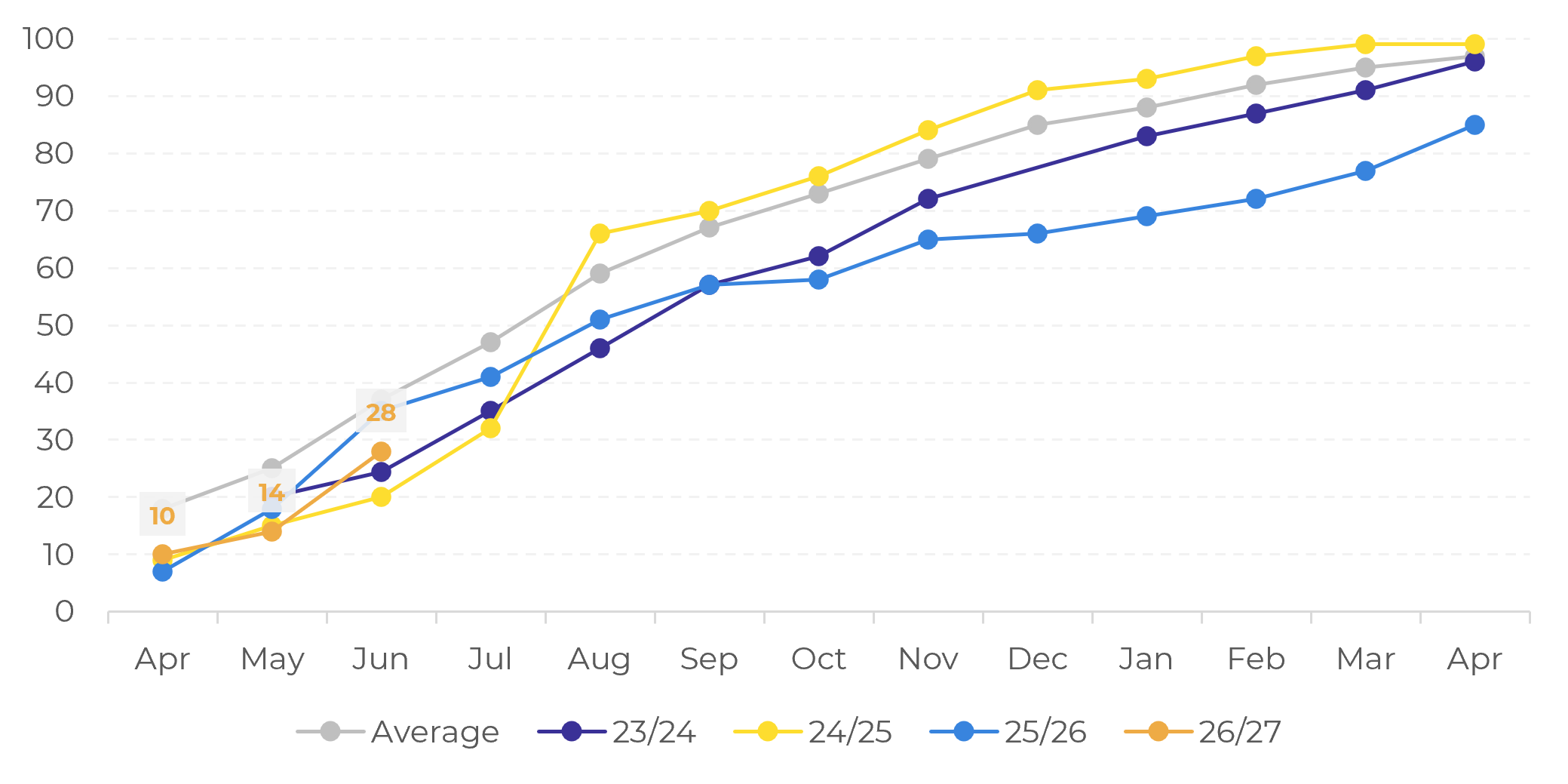

Farmer selling in Brazil also remains below expectations for this stage of the season. Although additional sales were reported last week as prices strengthened and harvest activity approached its peak, larger volumes were expected to reach the market. According to the latest data, producer sales for the 2026/27 crop stood at 26% of expected production in June, well below the five-year average of 36%. Arabica sales reached 26% of the crop, while Robusta sales stood at 28%, both below their respective historical averages of 36% and 37%.

Overall, while there has been no major shift in market fundamentals, the balance of risks continues to point toward potential supply constraints in the short to medium term. With liquidity remaining thin, any supply-related developments could trigger heightened price volatility, potentially amplified by fund activity. In the coming days, market participants will be closely monitoring Brazil's export data, scheduled for release this week, as well as the USDA estimates expected next week.

Brazil: Arabica Farmer Selling (% of total)

Source: Safras & Mercado

Brazil: Robusta Farmer Selling (% of total)

Source: Safras & Mercado

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

carolina.franca@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.