Sep 29

Coffee Weekly Report - 2023 09 29

Back to main blog page

- Recent rains in Brazil may trigger a second flowering in early October for the 24/25 crop. Also, October marks the start of the 23/24 global cycle and the main harvest for many washed arabica origins.

- Latin American coffee-producing countries struggle to regain pre-19/20 production levels due to climatic and economic challenges. We anticipate a modest recovery of 700k bags in the 23/24 cycle, with Colombia as main driver.

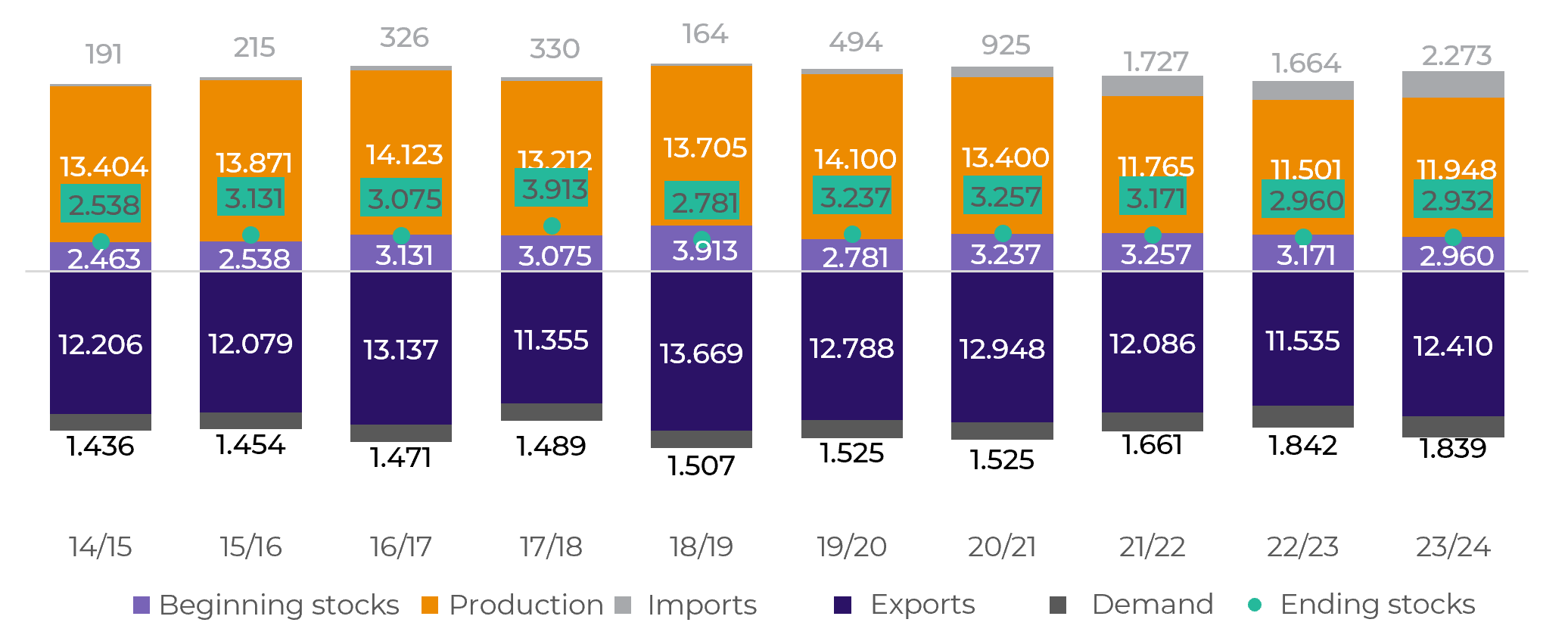

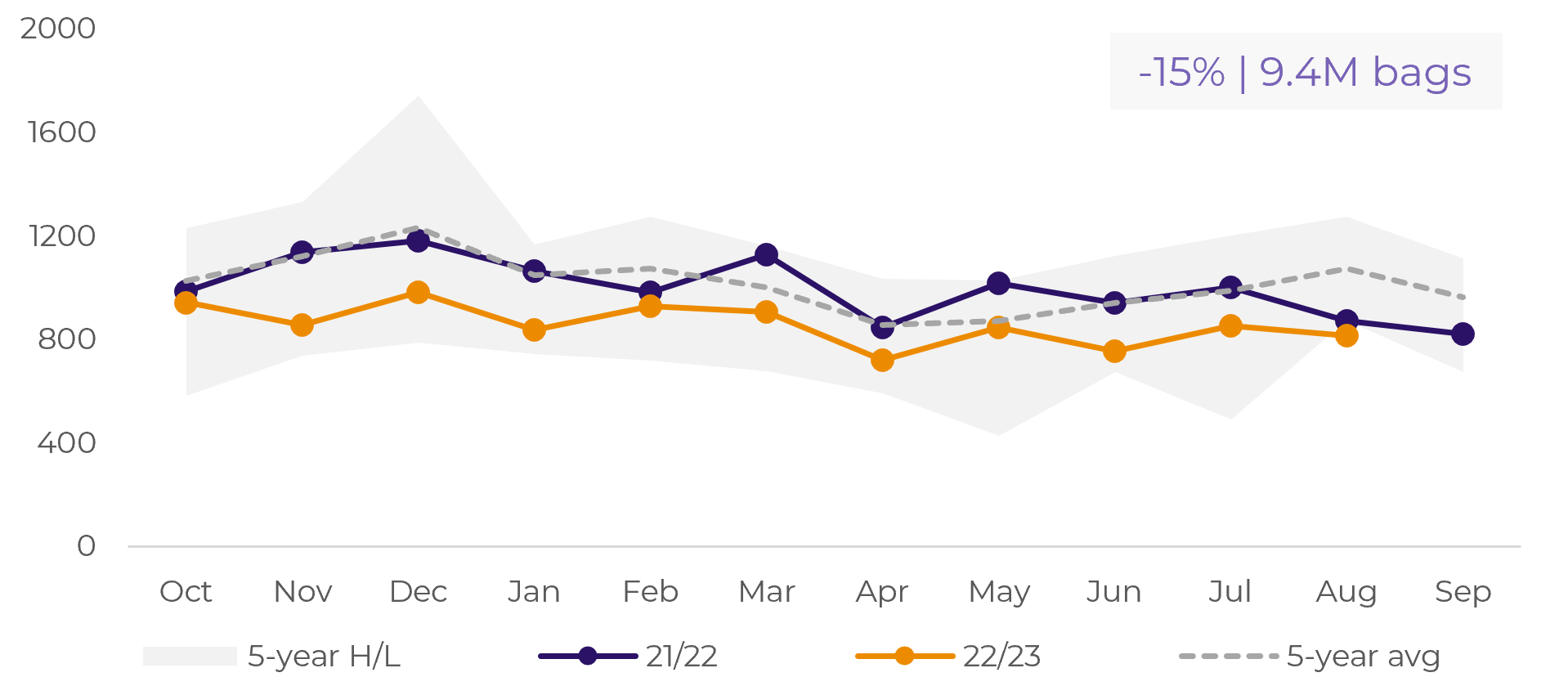

- Depletion of initial stocks for 23/24 may lead Colombia to increase imports in the cycle starting in October. Exports may recover in 23/24 but are expected to remain below previous records.

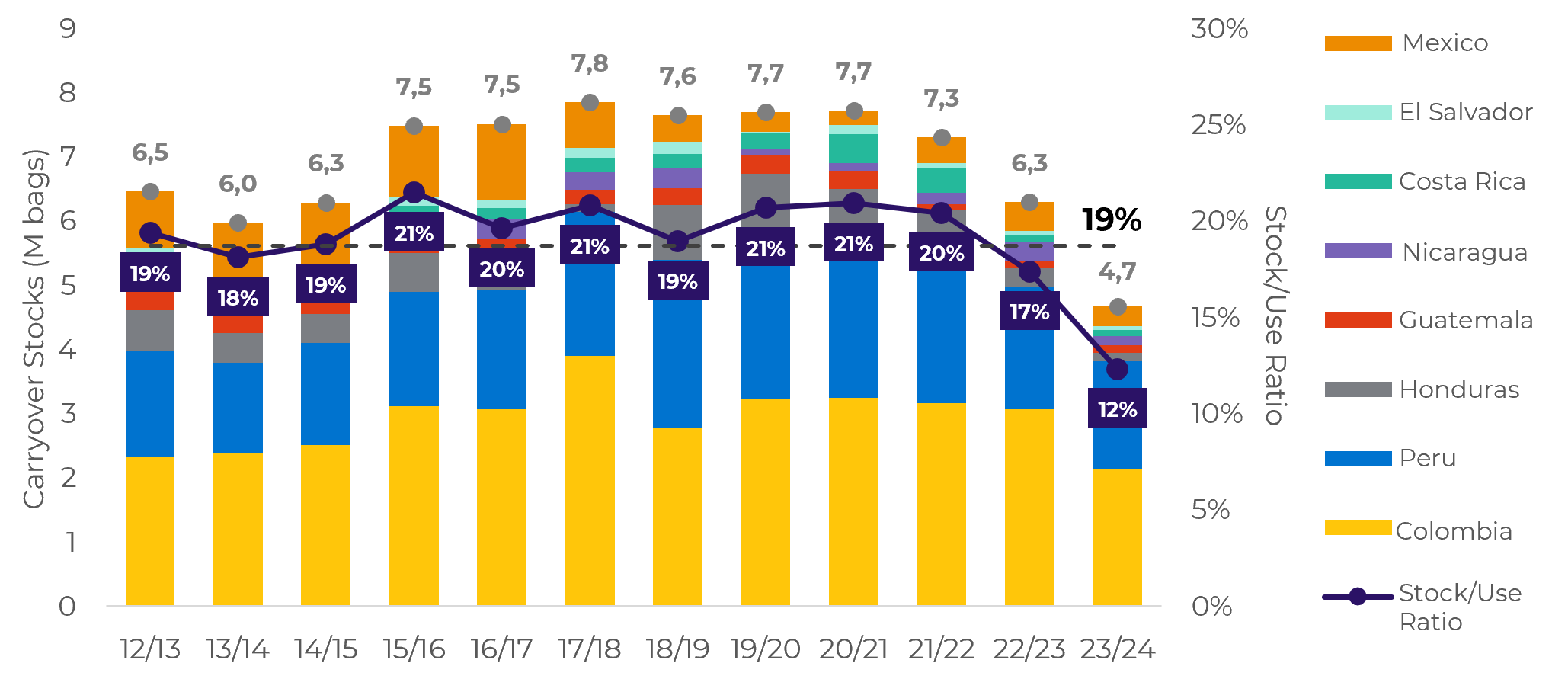

- Stocks have been depleting over the last four years, reaching the lowest result in recent history. In 23/24, the stock-to-use ratio is expected to fall to 12%, below the historical average of 19%.

Washed arabica coffee challenges

Coffee prices were back on the downtrend this week, with the 145 c/lb support level being an important marker for the first week of October, especially as the recent rains are likely to trigger a second flowering in Brazil, in areas that only registered the first one at the end of August.

Still, besides the 24/25 crop growth in Brazil, October marks the beginning of the 23/24 global cycle, and the main harvest for most washed arabica origins.

Latin American coffee-producing countries posted a record production in 18/19, and after the setback in 19/20, they have struggled to regain previous production levels due to climatic and economic impact. We anticipate a recovery of only 700 thousand bags in the 23/24 cycle, with a larger contribution from Colombia, given the climatic conditions, especially in the southern region of the country.

With the depletion of initial stocks for 23/24 and the expectation of limited production growth, we estimate that Colombia is likely to experience an increase in imports in the cycle starting in October. Consequently, exports may recover in 23/24 but remain below the records set in previous years.

Image 1: Supply & Demand – Colombia (‘000 bags)

Source: hEDGEpoint

Image 2: Exports – Colombia (‘000 bags)

Source: FNCC

It’s also important to highlight the results from farmer selling data in Brazil, indicating that while liquidity has improved when compared to August, this crop’s sold volume is still below the average expected for the period.

This perspective of higher stocks going into the last quarter of the year – when other arabica origins begin their harvest – also weighs down on prices.

Differently from the past week, forecast models are now starting to deviate: the American model suggests near-zero rainfall levels over most coffee areas – except for regions in Sul de Minas and Zona da Mata – whereas the European model already shows a slightly more optimistic view.

Still, rains must follow through to maintain the optimum NDVI levels seen so far, and also to lower the likelihood of pests. For instance, broca: Dry conditions may boost coffee borer beetle activity, with higher temperatures speeding their life cycles, particularly in densely planted lower-altitude areas.

Image 3: Carryover stocks and Stock-to-Use Ratio

Source: hEDGEpoint

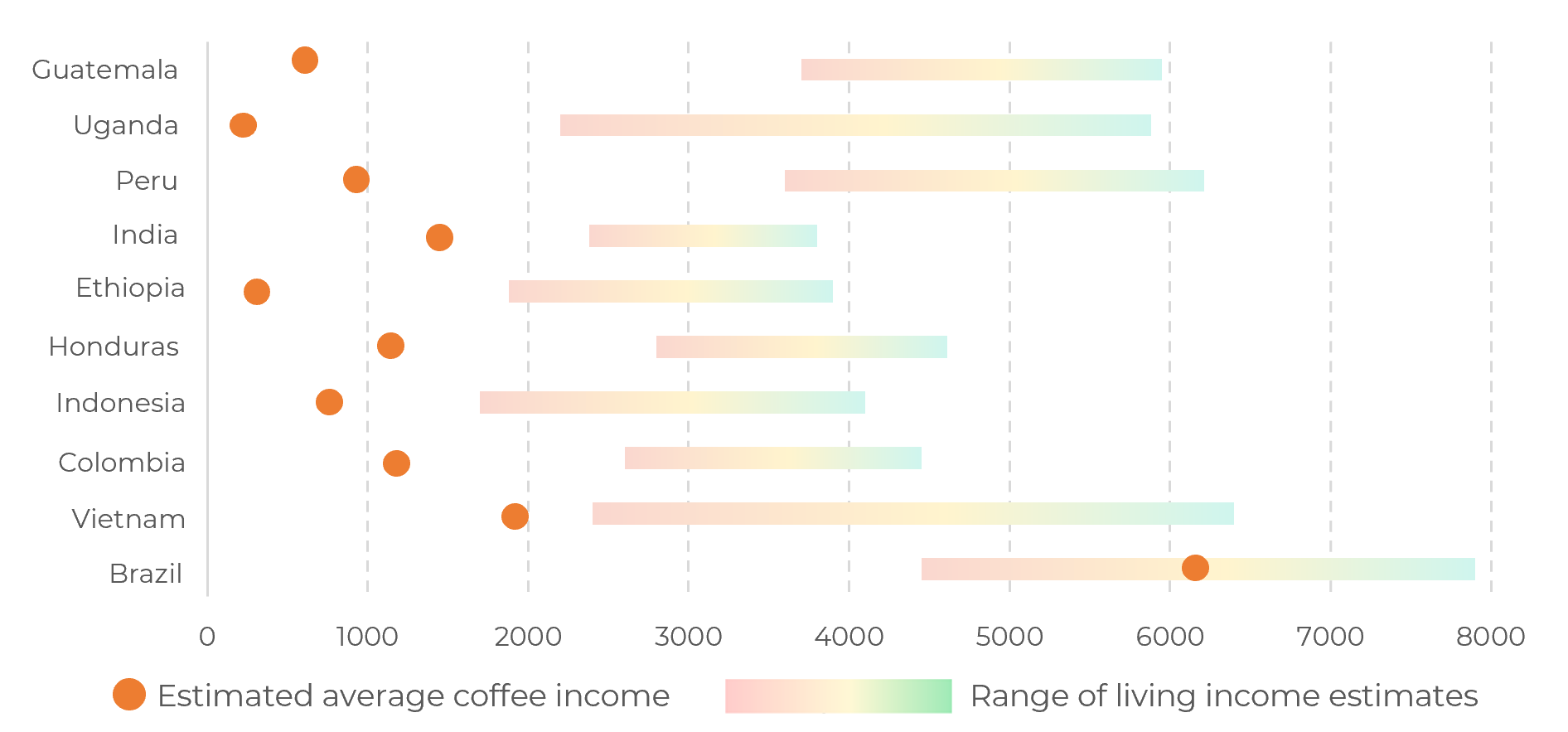

Image 4: Country living income – Coffee income (US$/household per year)

Source: Coffee Barometer, Cordes, K. and Sagan, M. (2021)

In Summary

Coffee prices slid this week, aiming for the crucial 145 c/lb support by early October. Recent rains in Brazil may trigger a second flowering, impacting the 24/25 crop.

October also initiates the global 23/24 cycle, fundamental for most washed arabica origins. Latin American producers, after a record 18/19, struggled to recover from 19/20 setbacks.

A modest 700k bag increase is expected in the 23/24 cycle, mainly driven by Colombia. Depleted stocks and global demand could strain the stock-to-use ratio, dropping to 12% (below the 19% historical average). Climate and disinvestment have hampered production in Central America, Colombia, and Mexico.

Weekly Report — Coffee

Written by Natália Gandolphi

natalia.gandolphi@hedgepointglobal.com

natalia.gandolphi@hedgepointglobal.com

Reviewed by Victor Arduin

victor.arduin@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.

To continue using the Hedgepoint HUB, please review and accept the updated terms.