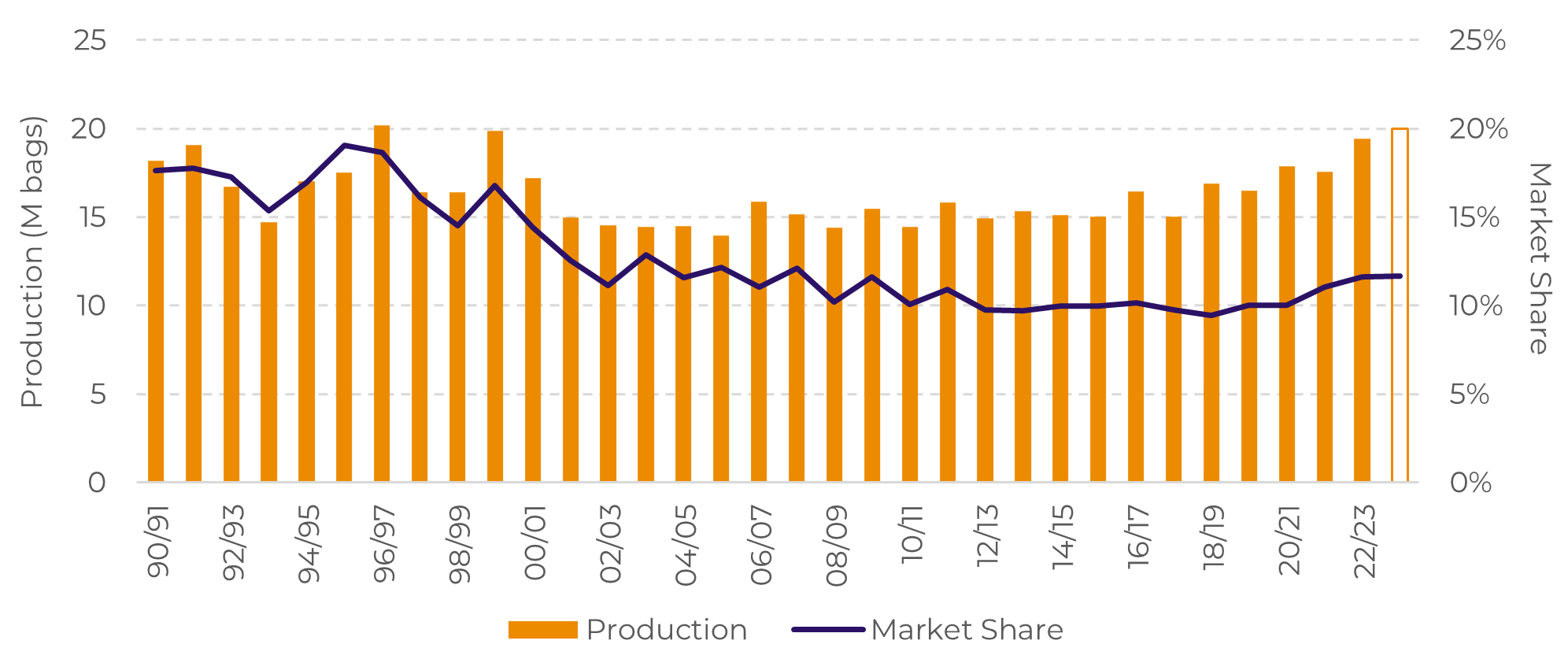

As we delve into the intricacies of the 23/24 coffee market cycle, it's imperative to grasp the evolving supply dynamics, particularly in Africa, which has witnessed a surge in prominence in recent years. In 1990, African nations contributed nearly 20% to the global coffee supply, but their share dwindled as Asian origins, notably Vietnam, gained prominence in both cultivation area and yield.

However, a pivotal shift occurred from the 16/17 cycle onwards, with African countries reclaiming lost market share, escalating from 9% in 16/17 to a notable 12% by 22/23. Projections for the 23/24 cycle are even more promising, anticipating a substantial upswing to 20 million bags, marking the highest level since the 96/97 cycle.

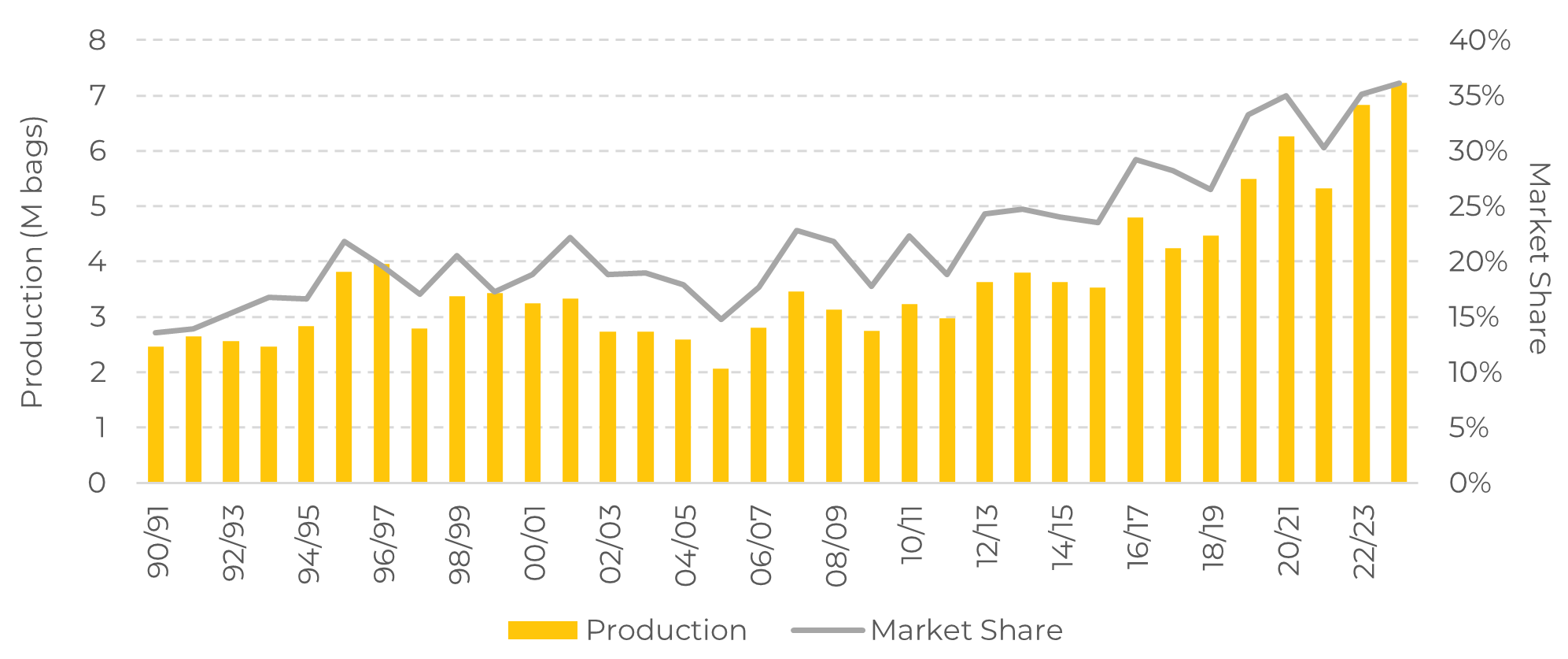

Beyond the conventional coffee-producing origins, such as Ethiopia, Uganda emerges as a standout player in this narrative. Remarkably, Uganda's market share within Africa skyrocketed from 14% in 90/91 to an impressive 35% in 22/23, underscoring its pivotal role in the evolving coffee landscape. This resurgence underscores Uganda's transformative journey, positioning it as a significant player and contributing to the broader recovery of African coffee on the global stage.