In previous reports, we’ve looked at the performance of demand in destinations, with data from the European Union suggesting a stronger growth than initially expected – since the decrease in imports did not fully explain the trend in stocks.

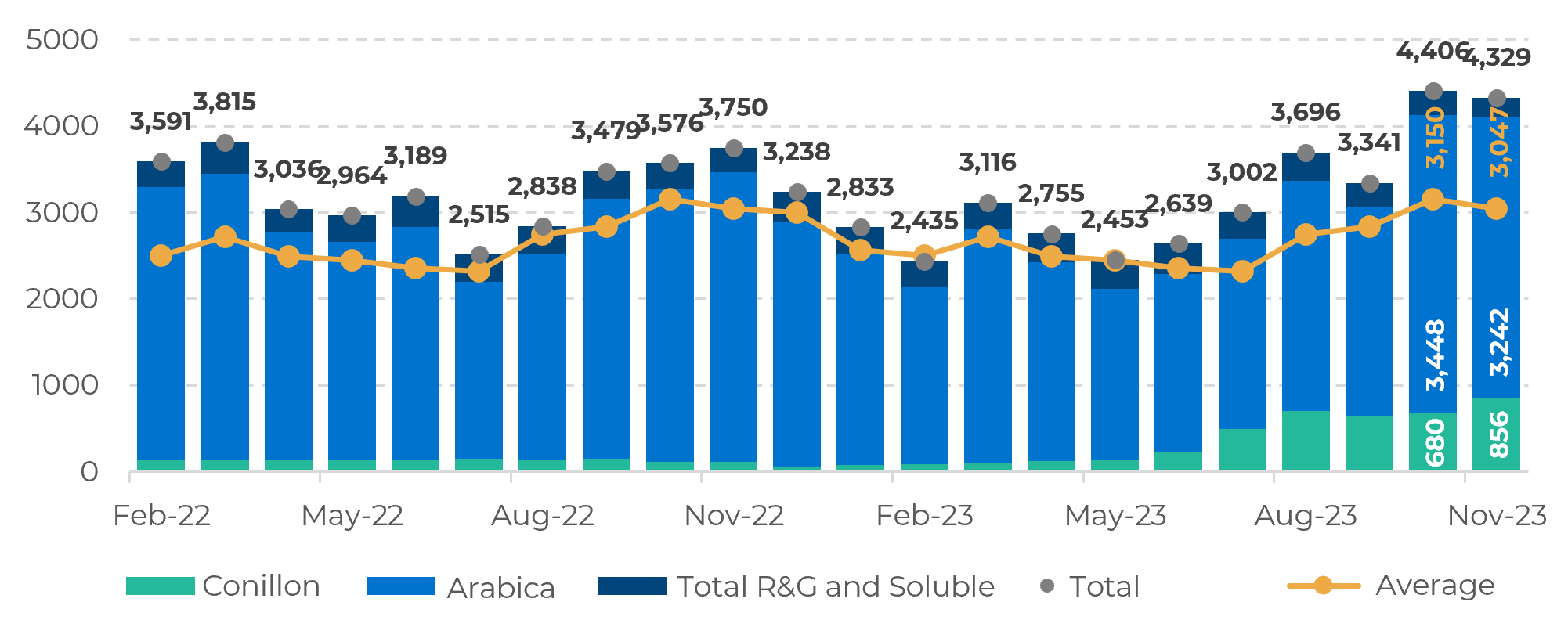

Still, that was a picture taken in the 22/23 cycle, and since then, Brazilian exports have increased, changing the landscape in destinations. Shipments reached 4.3M bags in November, with 3.2M bags of arabica and 856K bags of conilon (Figure 1).

The total has surpassed the average by 1.3M bags, nearly 42%. The move is explained by higher availability in the 23/24 Brazilian crop when compared to 22/23, as well as competitive prices from Brazil when compared to other origins.

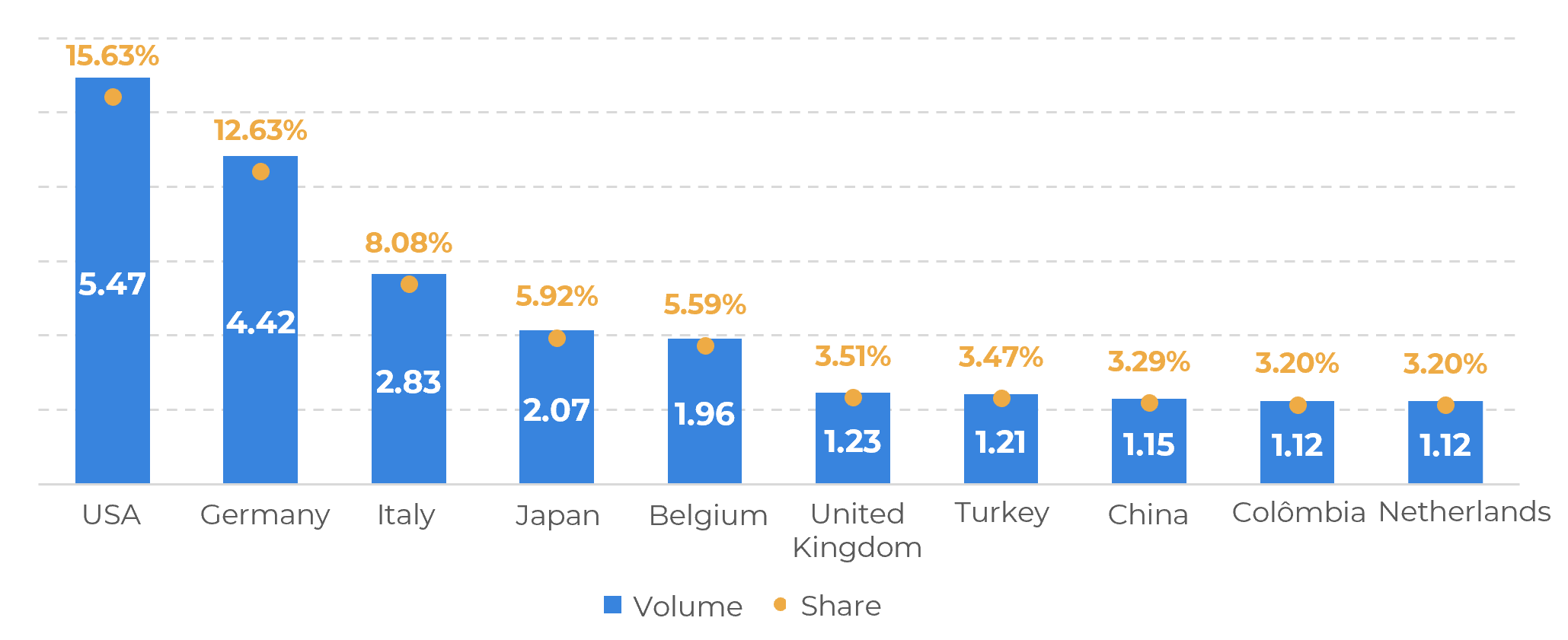

Considering the cumulative figure for 2023 (Jan-Nov), the USA has been the main destination for Brazilian coffee, at 5.47M bags, or 15.63% of the total (Figure 2). Germany and Italy follow in second and third places – although the EU as a whole has imported 14.73M bags from Brazil this year (down 14% YoY).