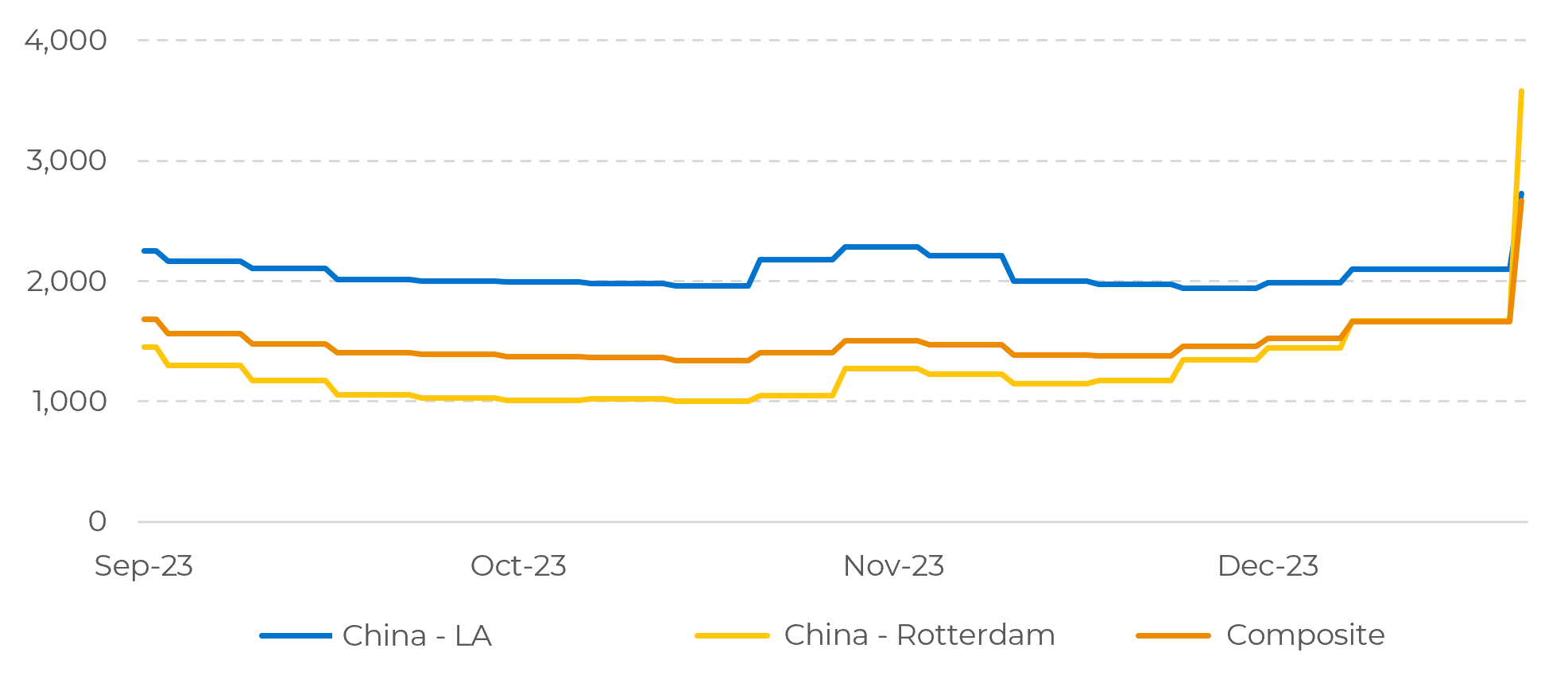

In the transpacific route, liner rates surged by 56% sequentially to $2,769 per 40-foot container in the week ended January 3. Spot-rate volatility affects liner operators directly, but also has a cascading effect in commodity markets, also impacting railroads, truckers, freight forwarders, and intermodal marketers.

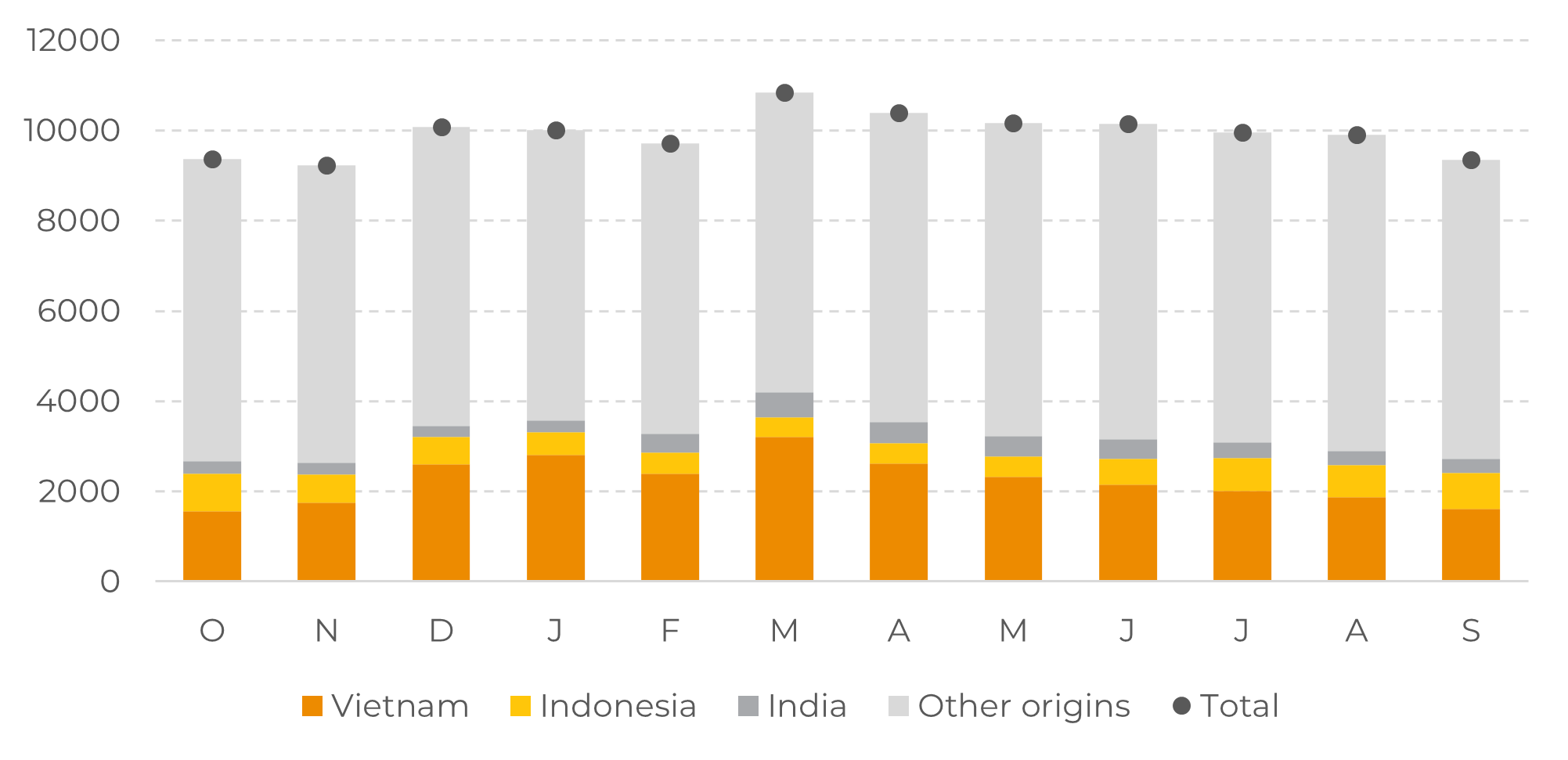

For coffee, the route affects mainly origins from Asia and Southeast Asia. Considering the three main exporters in the region (Vietnam, Indonesia, and India), roughly 36% of the first quarter global exports may be delayed – as the three countries represent approximately 11M bags from the 30.5M bags average that are exported during the first quarter of each year.

Further escalation of the conflict may add volatility to robusta prices, decreasing the NY-LN arbitrage. Additionally, other robusta-producing origins may see an increase in FOB differentials – such as Brazil and Uganda – as well as a trigger for higher exports in the first quarter, which would be supported by 23/24’s Brazil availability and the secondary harvest in Uganda.