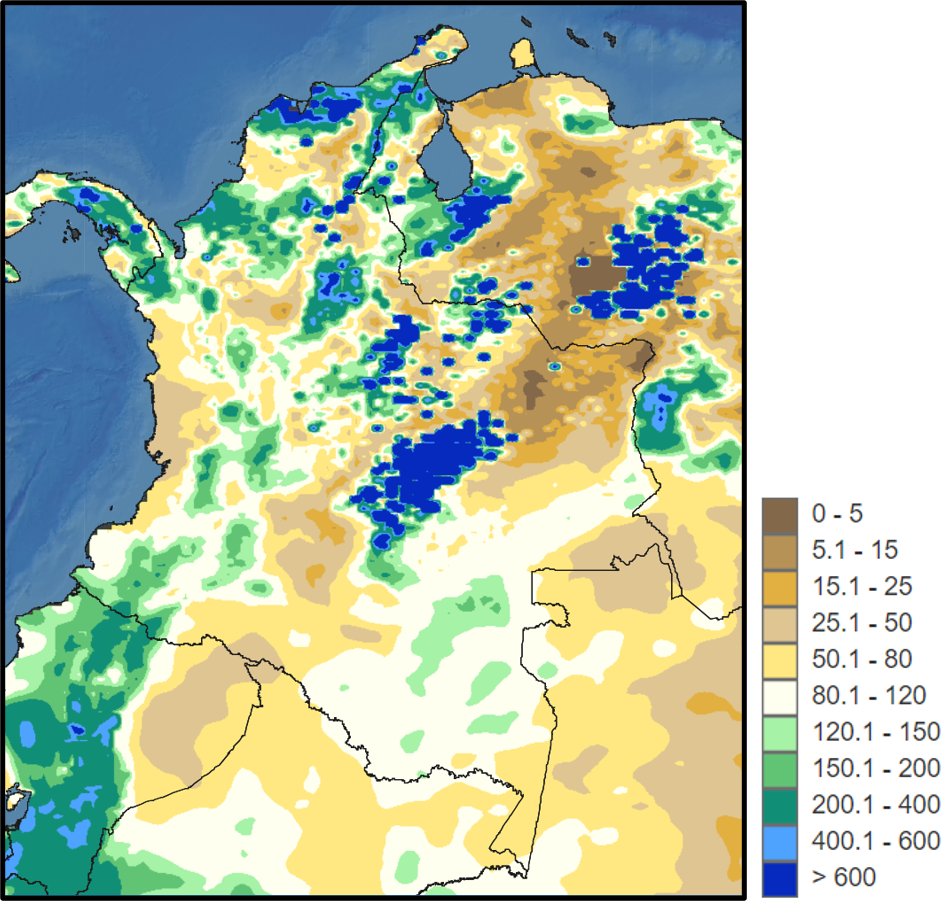

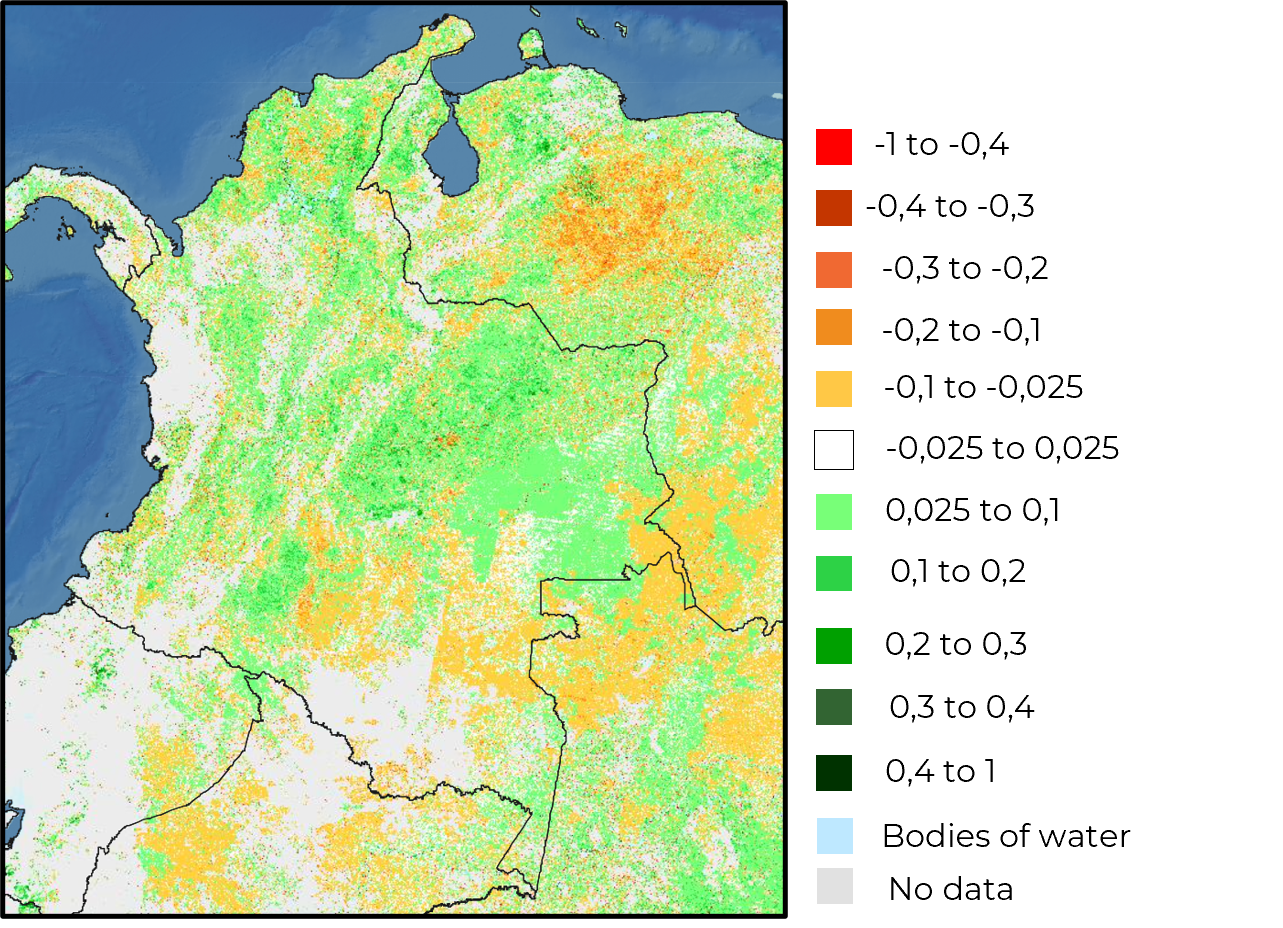

The weather has improved in Colombia, but not uniformly. While some regions are reporting favorable vegetation indices, adequate precipitation, and suitable temperatures, this trend does not cover all coffee-growing areas (Figures 1 and 2).

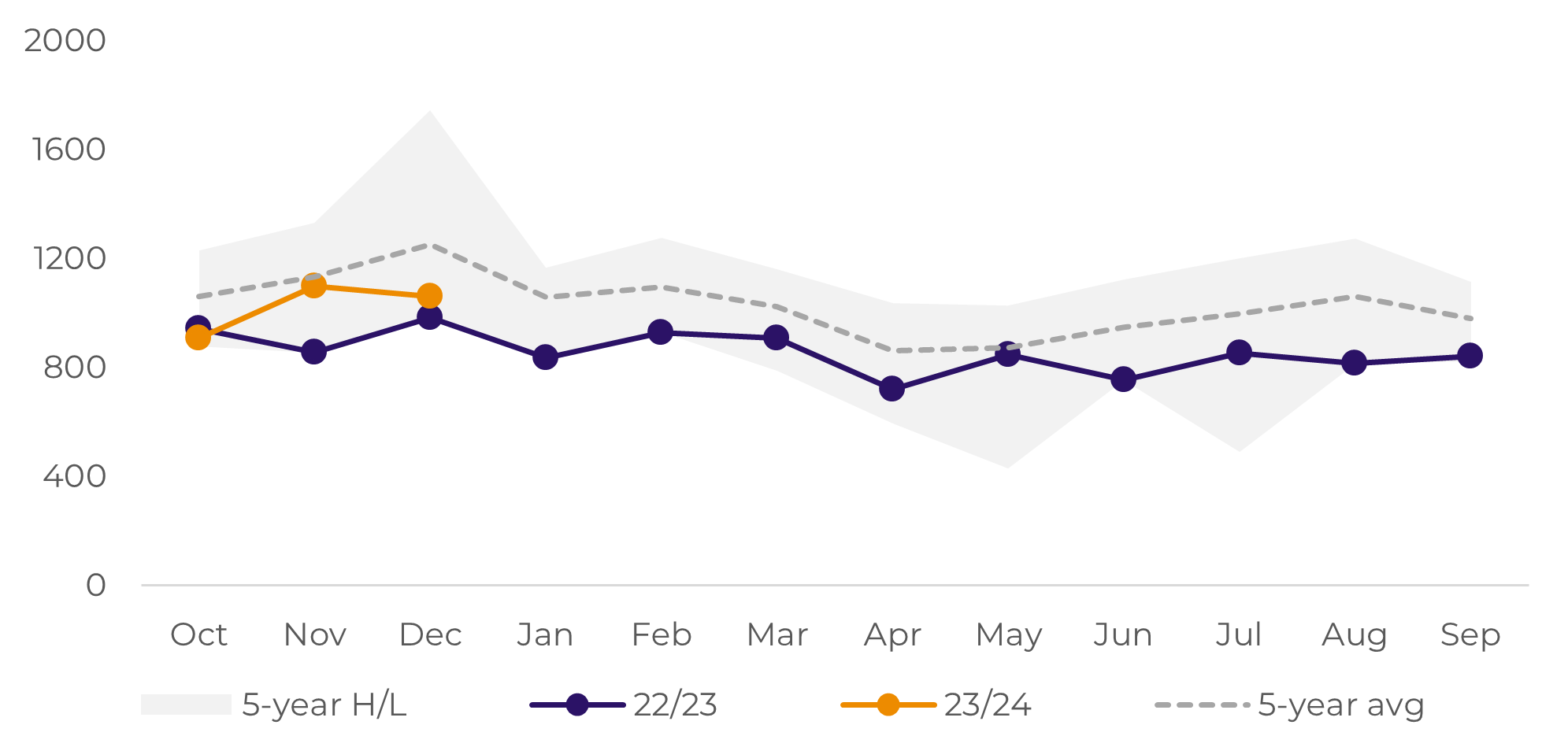

Furthermore, the drier weather expected in the coming days may aid in harvesting the main crop, but attention is needed for the mitaca.

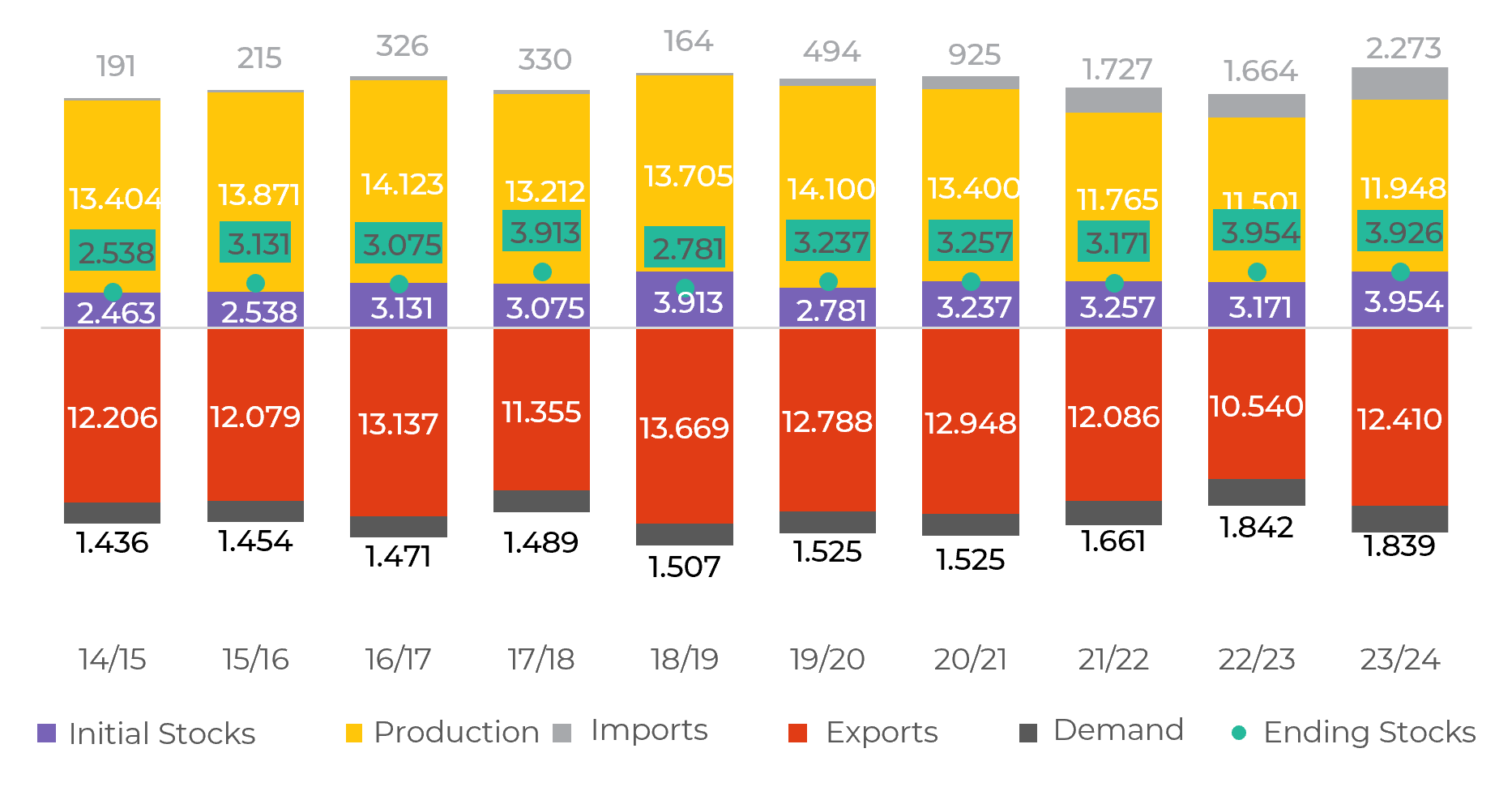

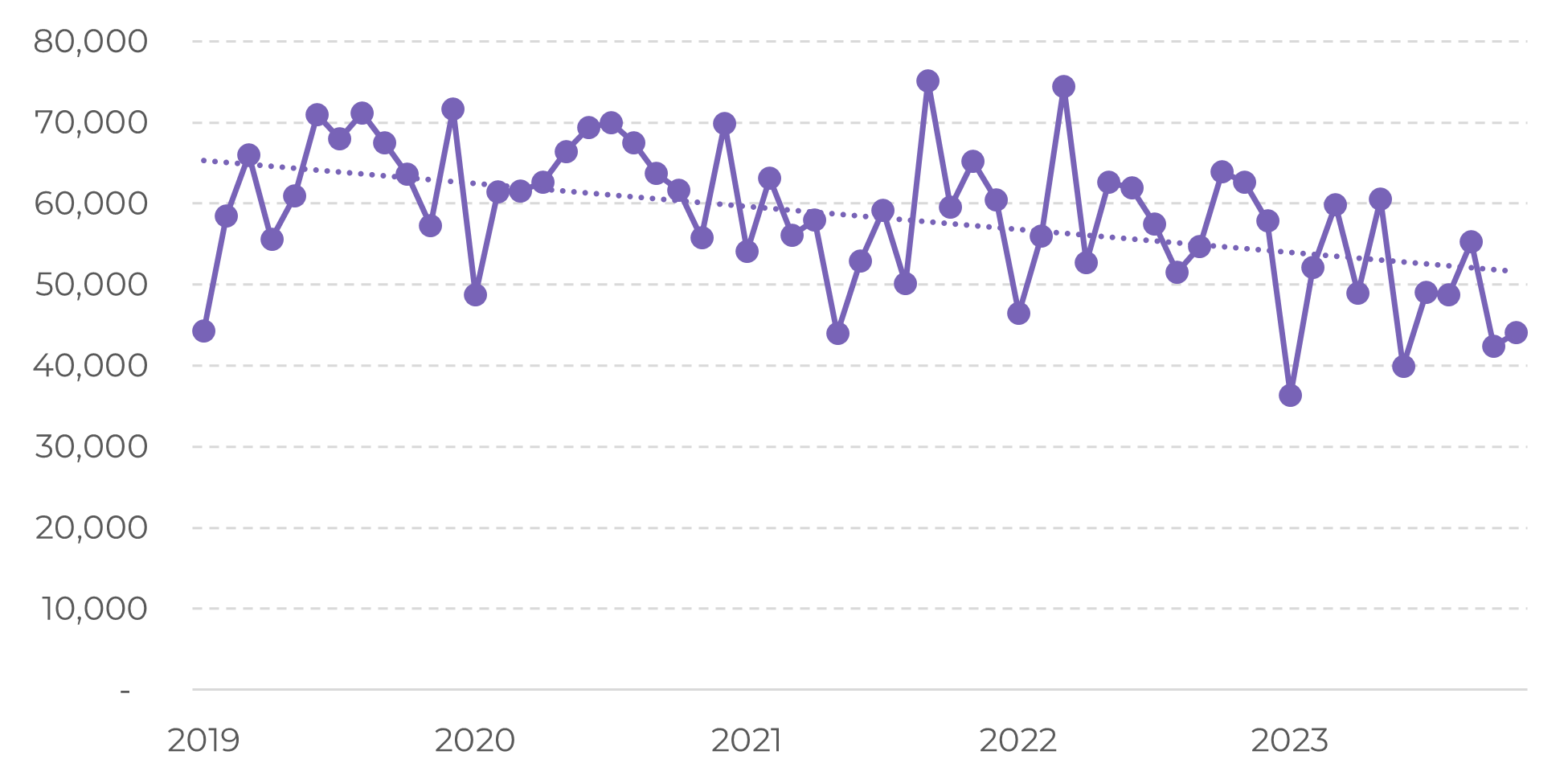

Additionally, the country reduced export volumes beyond what was necessary to accommodate the production reduction in 22/23, with producers on the sidelines, reluctant to sell at local price levels throughout the entire cycle. Consequently, the country begins the 23/24 cycle with higher beginning stocks.