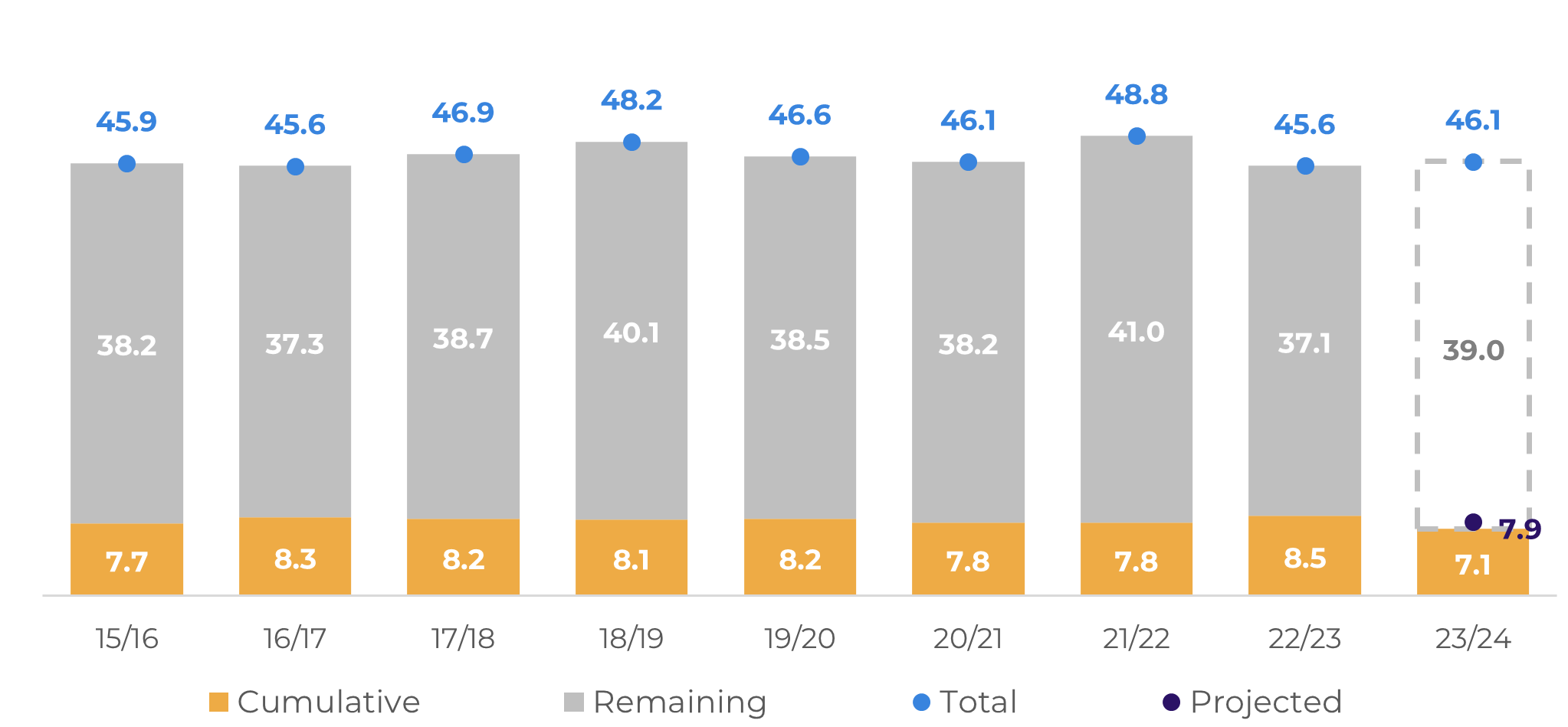

Cumulatively in 23/24, the European Union imported 7.1M bags – slightly lower than the 7.9M bags expected for the period, considering a 1% increase in imports to support a 1.5% increase in demand – however, it’s still early to affirm that this will last throughout the whole cycle.

In fact, in order to go back to normal stocks levels in the bloc, imports would need to ramp up in this cycle. Still, we highlight the argument from earlier in the report: even though stocks fell more than expected, likely due to the new deforestation regulation, that coffee may just have been reallocated.

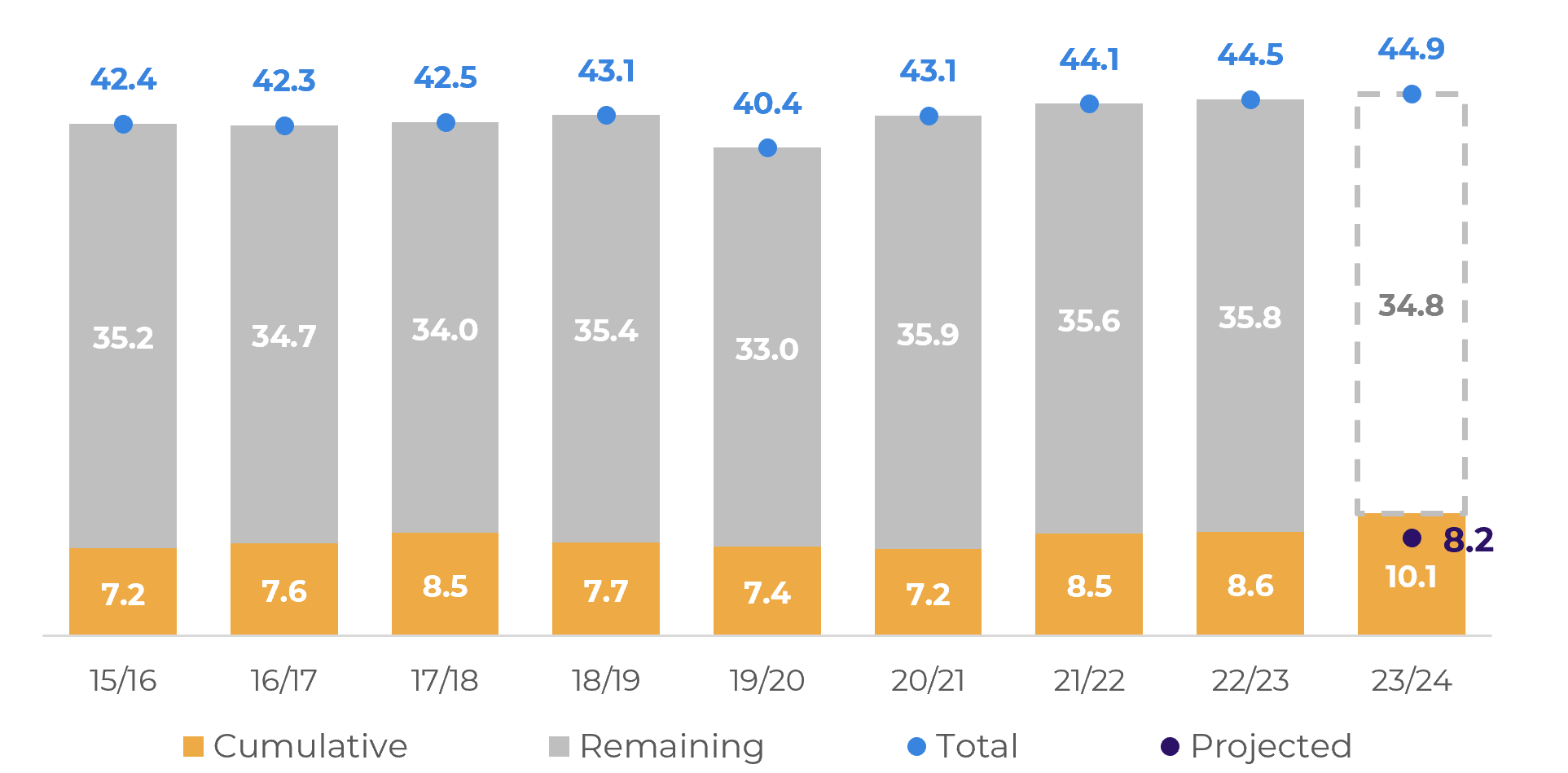

For the cumulative figure in 23/24, apparent consumption results may also be still reflecting this trend: the bloc has reportedly consumed 10.1M bags, vs. 8.6M bags at the same period last year – which was a record. In this sense, demand figures are bullish, but should be considered carefully, since part of the movement is exogenous to the market demand itself.