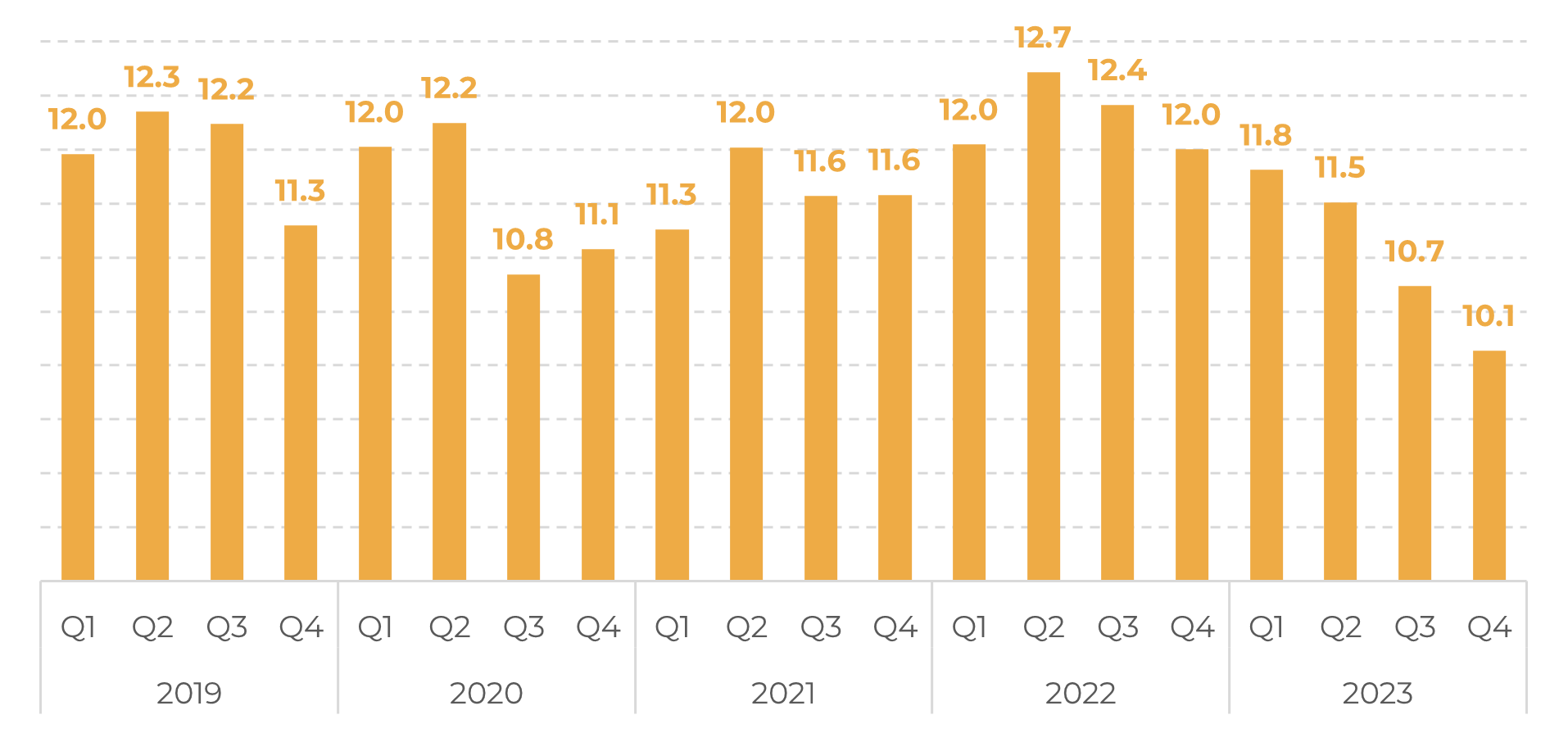

Overall, the bloc has seen a steady decrease in imports since 2022 (Figure 3) – a direct reflection of higher storage costs, as seen in previous reports. The more substantial drop between Q2/23 and Q3/23 was also linked to new legislation surrounding deforestation in countries of origin.

Consequently, destination countries have depended more on these local supplies, which has led to a withdrawal of stocks, leaving this fact as one of the main points of support for prices, especially with the new trade flow structure – lower imports, greater concentration.

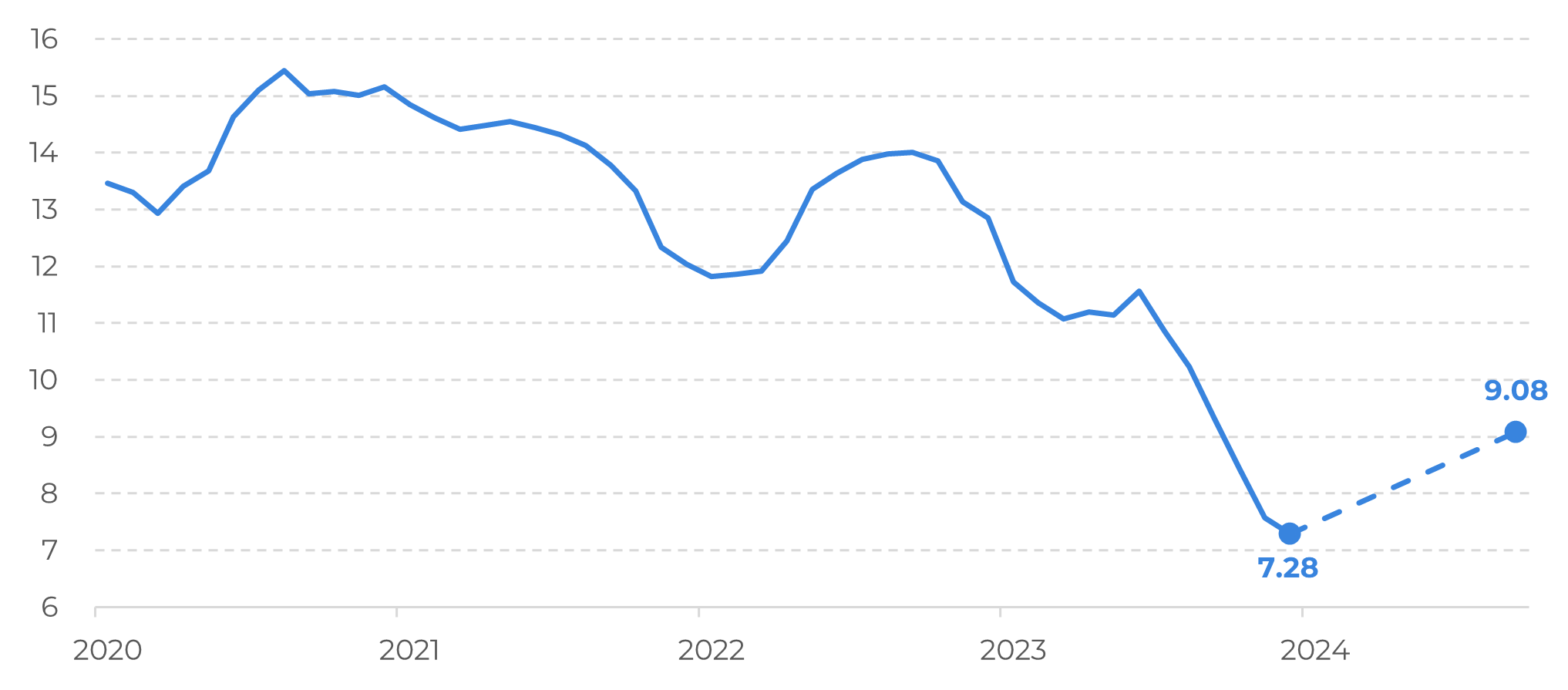

Currently, using USDA figures as a marker for what the market currently expects, ending stocks for the 23/24 cycle are being estimated at 9.08 million bags in the European Union. This would require a 25% increase in stocks – which is, in fact, higher than the average expected for the period (+6%, considering data from the last 10 years). Still, it's important to note that stocks in the EU increased by 38% between December 2013 and September 2014, and there are similarities: origin stocks were 7% higher in the 13/14 cycle compared to 13/12, and helped to sustain trade flow during a global deficit point (as origins were heavily affected by El Niño). Therefore, the recovery to the 24/25 cycle may be a mirror of its historical counterpart.