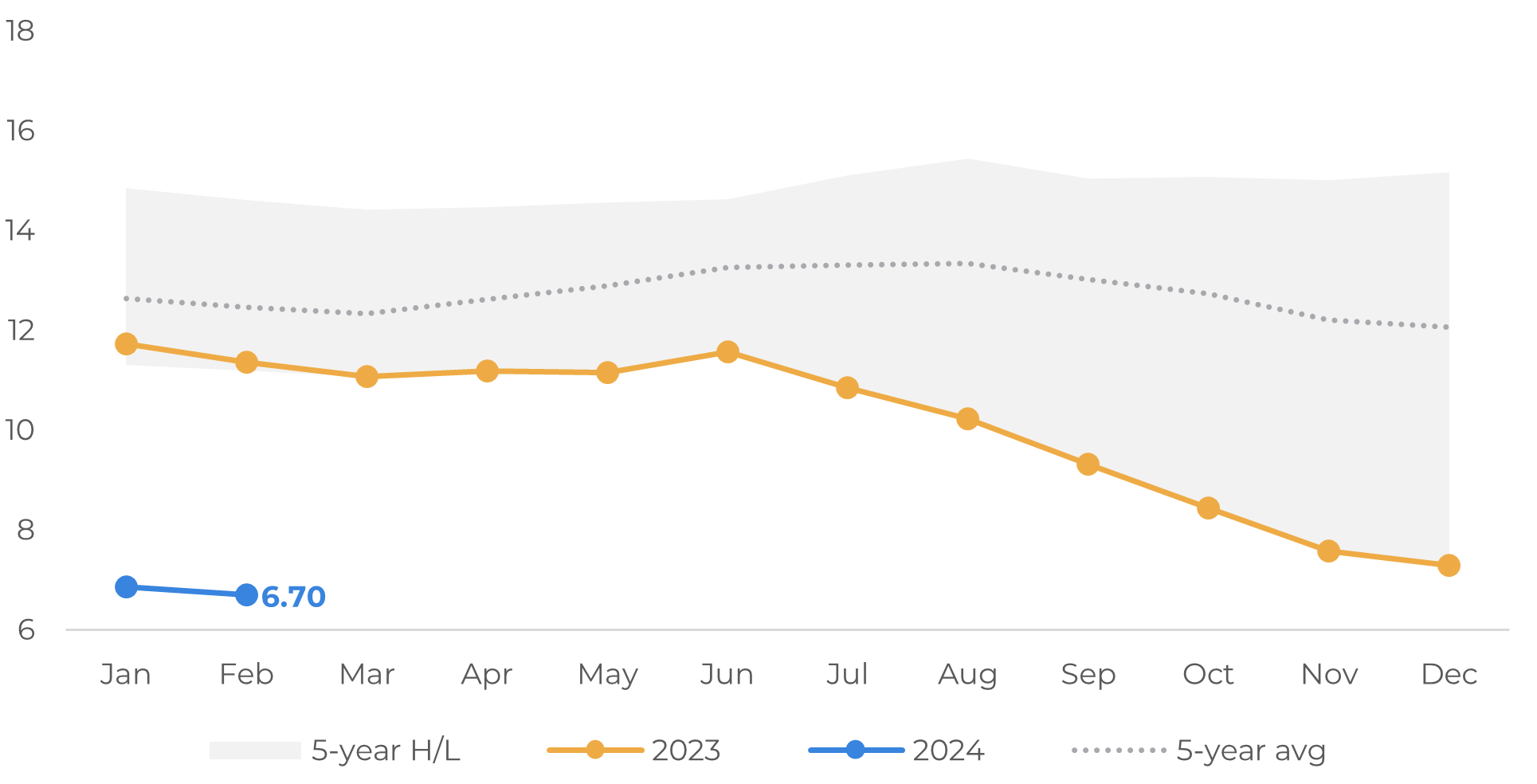

Following up on last week’s report about expectations regarding demand through the European Union lens, this week we will add to the analysis using the latest European Coffee Federation stocks release, with figures from January and February 2024.

Stocks fell to a staggering 6.70M bags low, which represents a decrease of 4.65M bags when compared to the same period last year (even though the monthly decrease was not far from the seasonal pattern, -2% vs. -1.3%).

The results were very bullish – even though the market was already working with lower stock levels for the region, the newly reached levels present a whole different scale of challenges for supply in the European Union.

The decrease was especially driven by robusta; washed arabica stocks remained roughly unchanged (-10K MoM), representing the higher share across coffee types (2.6M bags, or 40% of the total). Natural arabicas had a small increase (+8K bags, to 2.1M bags), and robusta stocks fell by 170K bags, reaching a low of 1.9M bags – now making up only 28% of the total stocks, 10 p.p. less than what would be expected.