Jun 28

/

Laleska Moda

Coffee Weekly Report - 2024 06 28

Back to main blog page

- The weather continues to be monitored in Vietnam, as it will have a major impact on the 24/25 production.

- Rainfall has improved since May, benefiting coffee trees and the development of the nesting season, bringing hope to part of the market.

- However, dry and hot weather in the first four months of 2024 could still penalize 24/25 yields, with could bring production to the lower end.

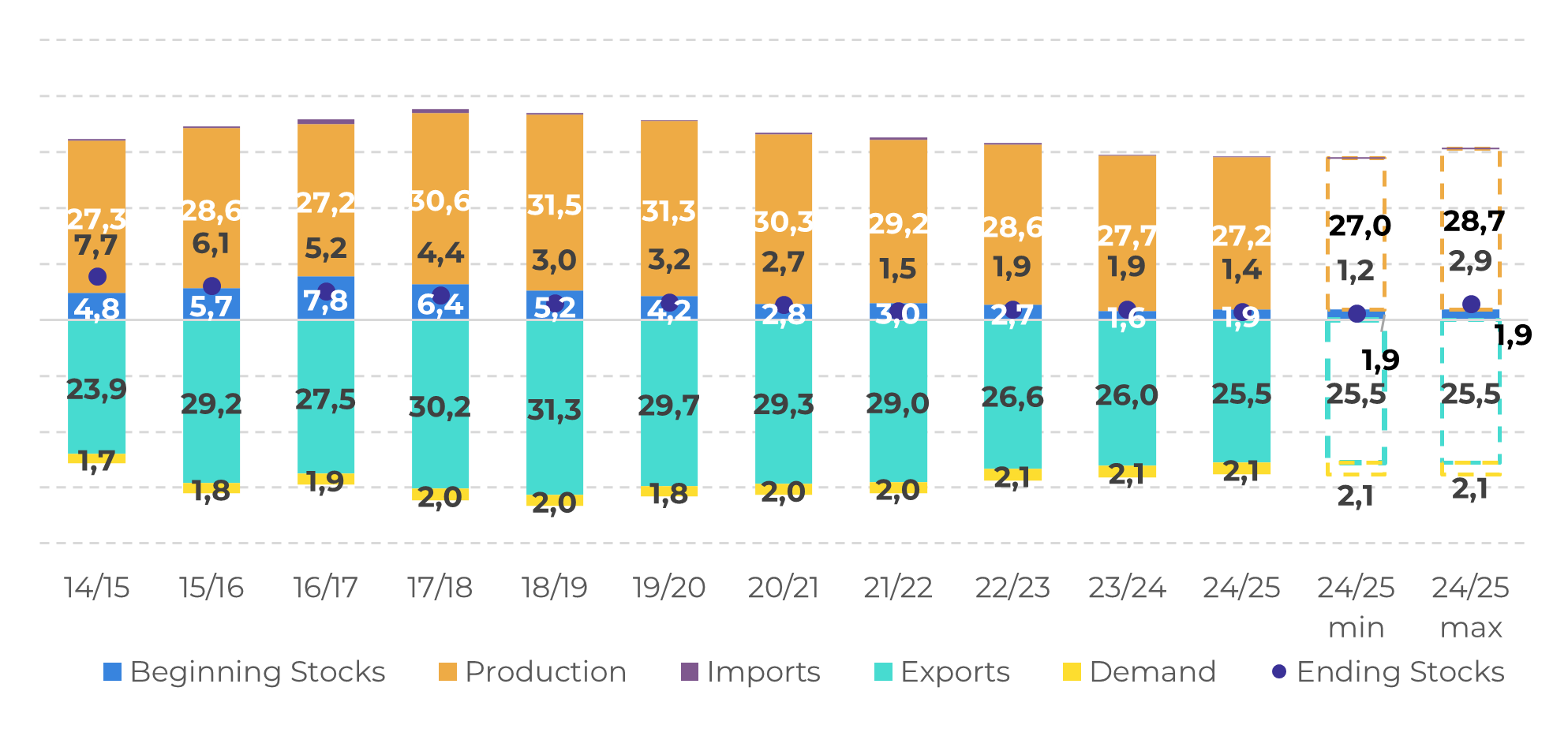

- We currently expect production in Vietnam in 24/25 to be 27.2 M bags in our base scenario. However, our models (given the correlation between rainfall, temperatures and yields, indicates we could have a more positive (28.7 M bags) or negative (27 M bags), so we still need to monitor crop development in following months.

- Its good to note that, in any of this scenarios, stock levels on Vietnam will remain tight, leading to another cycle of thigh global robusta supply.

Weather improves in Vietnam, but will it be enough to change the numbers?

Weather has been a major concern in Vietnam in recent months. Following the 23/24 crop failure and global robusta supply tightening, the market is anxiously awaiting the definition of the Asian country's 24/25 season. In this scenario, the dry and hot weather between January and April has pushed LN prices to historic highs this year.

Since May, however, rainfall levels have improved, benefiting coffee trees and contributing to this year's crop development. This also led to a price correction in May and the last days of June, as part of the market became more hopeful about the Vietnamese 24/25 season.

On the other hand, we cannot ignore the fact that cumulative rainfall up to June is still below the historical average, while temperatures in Vietnam remain high. In this sense, we may still have room for a correction in the 24/25 numbers, so it crucial to monitor closely crop development.

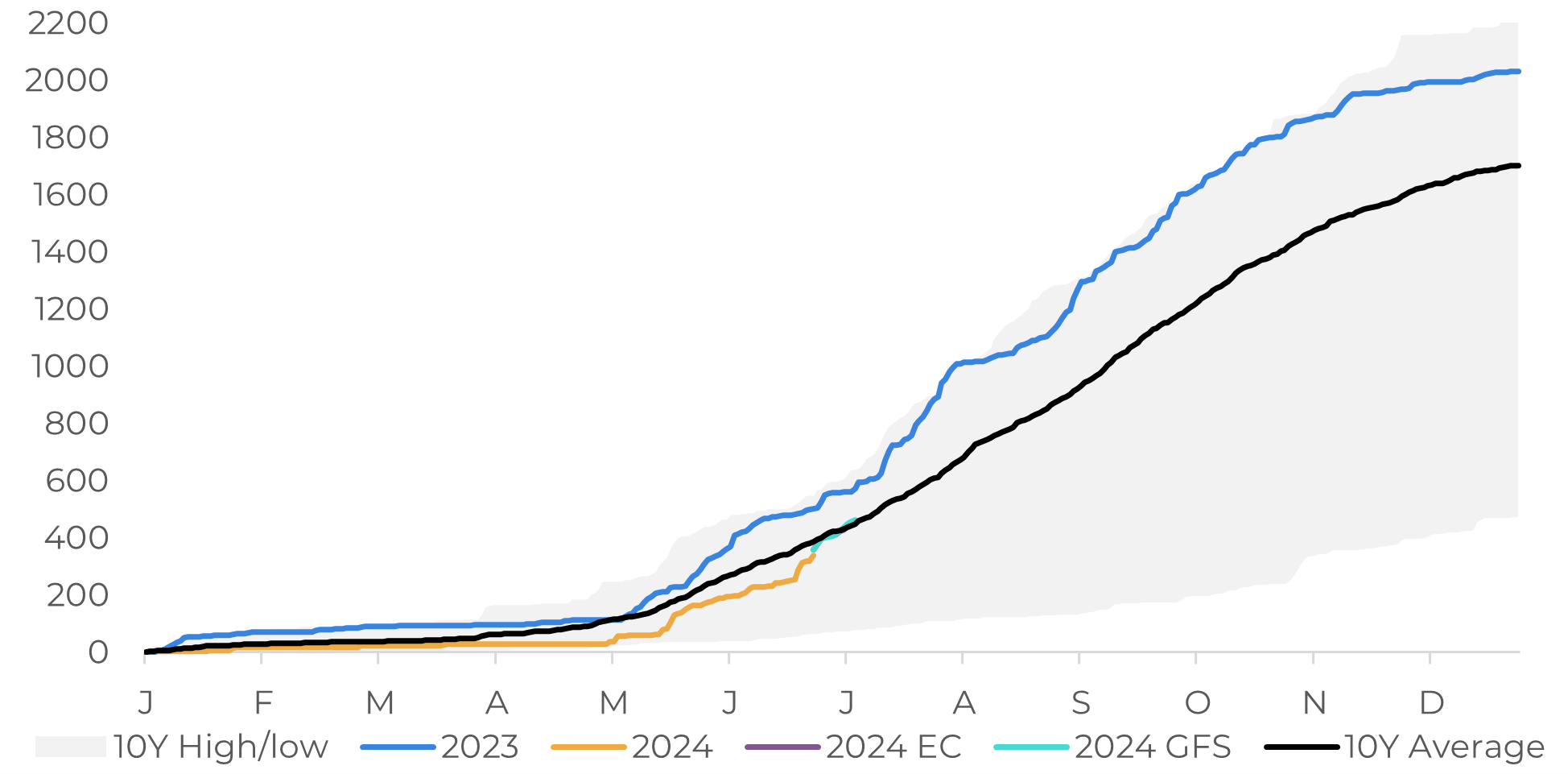

Central Highlands – Cumulative Precipitation (mm)

Source: Refinitiv

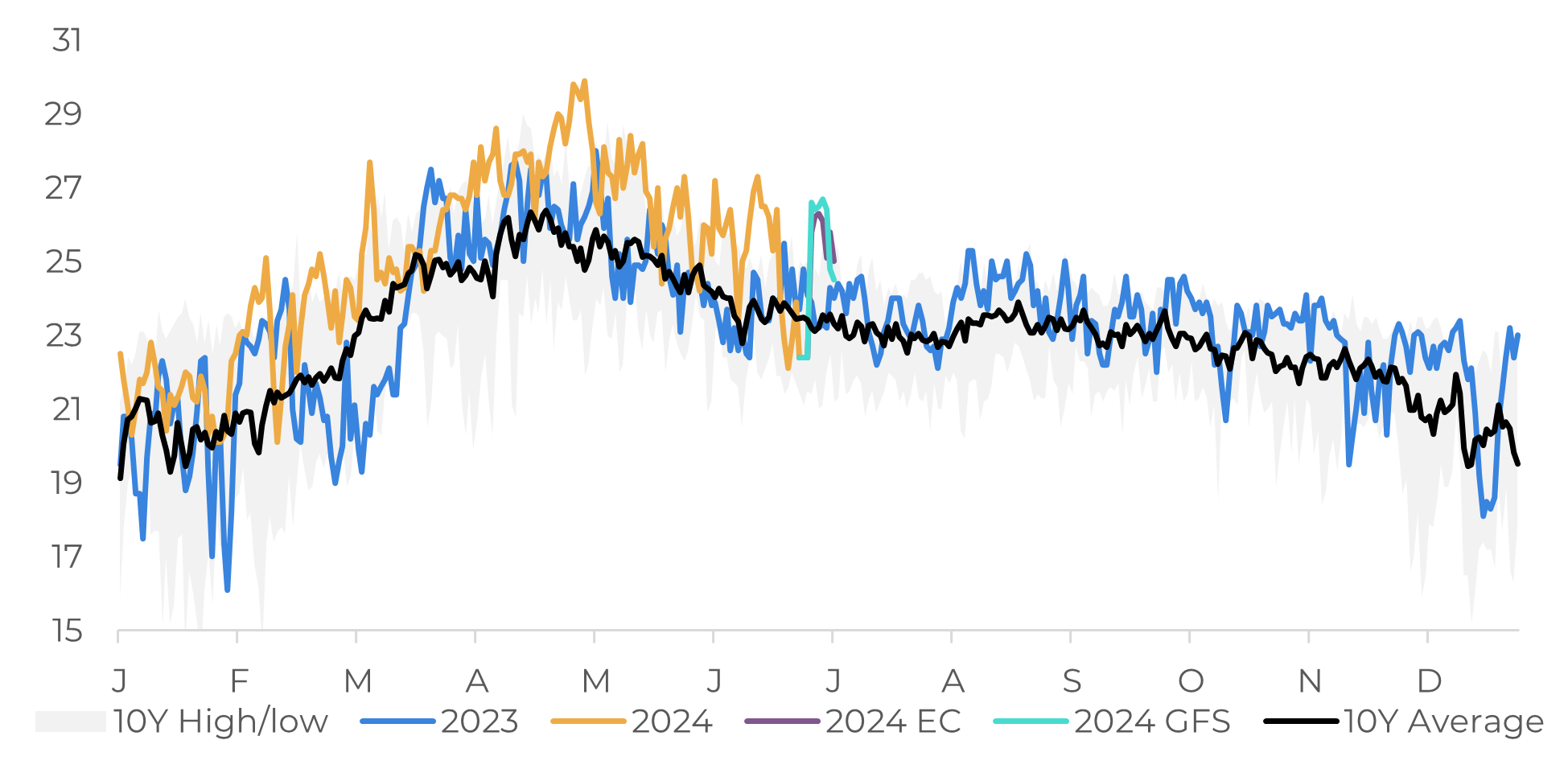

Central Highlands – Average Temperature (°C)

Source: Refinitiv

Our current expectation for the Vietnamese 24/25 season production is 27,2 M bags of coffee, but there are two other possible scenarios depending on future weather.

Considering the cumulative rainfall until May and average temperatures, our models suggest that, in a more optimistic scenario, production in Vietnam could rise to 28.7 M bags in 24/25. On the other hand, considering the minimum variation, production in this next season could end at 27 M bags.

Considering the cumulative rainfall until May and average temperatures, our models suggest that, in a more optimistic scenario, production in Vietnam could rise to 28.7 M bags in 24/25. On the other hand, considering the minimum variation, production in this next season could end at 27 M bags.

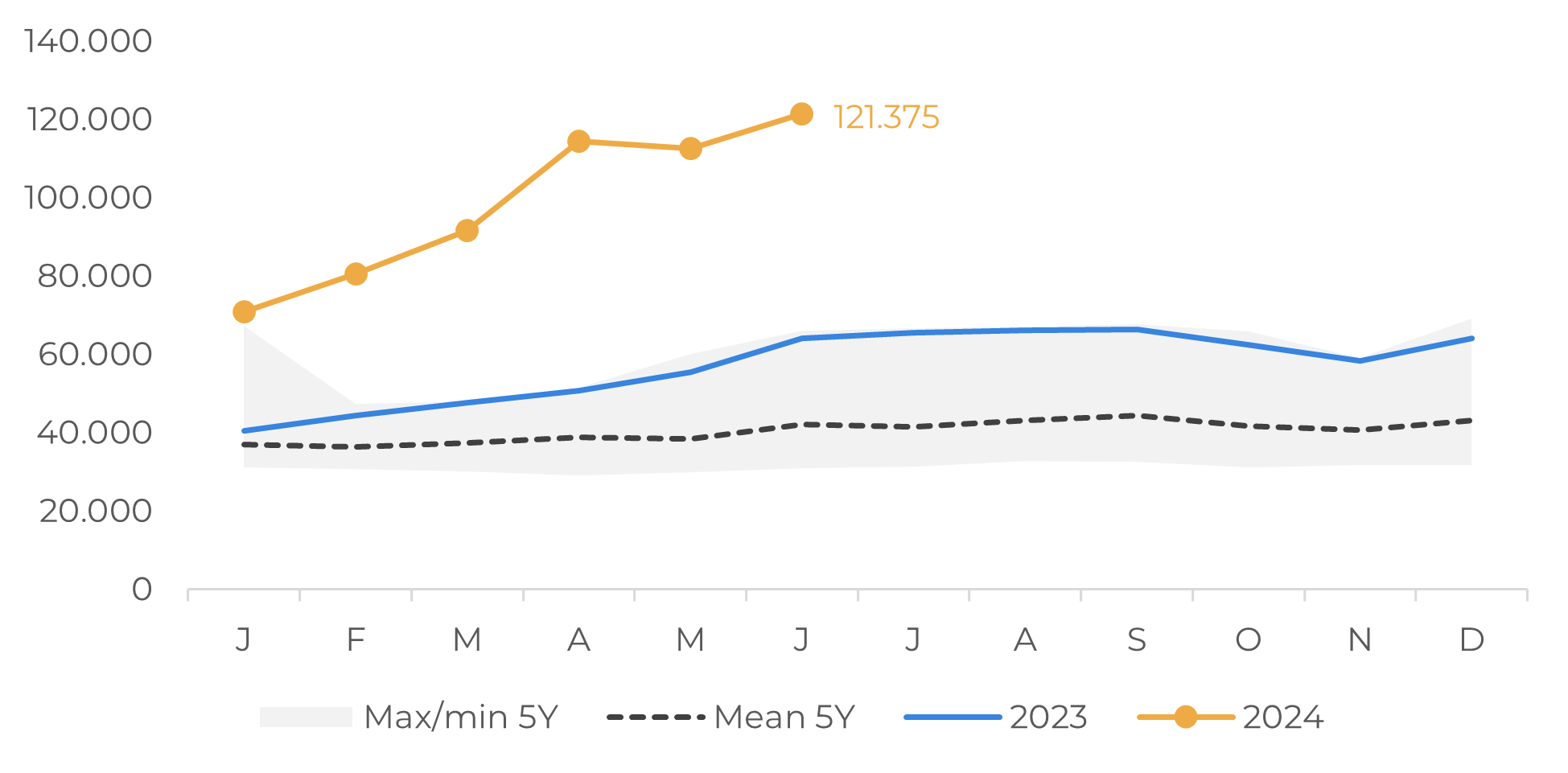

It is worth noting that in the three scenarios (baseline, maximum and, minimum) the country's inventories would remain tight, which could provide some support for prices in the long term. Lower stocks in 23/24 have already been reflected in lower exports from Vietnam in 2024 and have boosted local prices since the beginning of the year. Despite the fall in LN prices in recent days, domestic prices in Vietnam remain at near record levels of around VND 120,000/kg due to low stock levels and producers' reluctance to sell.

So, while domestic prices may see further corrections in the coming months – depending on expectations for the 24/25 season in Vietnam –, levels are likely to remain above those of previous years as supplies of Vietnamese beans will remain tight until the end of the cycle (September/24). This could also give some support in the global market, albeit prices probably will remain below April levels, given the advance of Brazilian harvest in the coming weeks.

Supply and Demand – Vietnam (M bags)

Source: Hedgepoint

Local price - Robusta - Vietnam (VND/kg)

Source: Refinitiv

In Summary

Following the 23/24 crop failure, the market continues to closely monitor the impact of weather on the 24/25 Vietnam crop. While rainfall levels have improved since May, they remain below historical averages. The impact of dry and hot weather from January to April 2024 on the 24/25 crop should also not be ignored.

We currently estimate the 24/25 season close to 23/24 levels, but production could be either slightly lower or higher depending on the weather in the coming weeks, as coffee trees in Vietnam are still in the development stage. However, stocks in the Asian country are currently tight and could remain so in the coming season, contributing to another season of limited robusta supply.

Weekly Report — Coffee

Written by Laleska Moda

laleska.moda@hedgepointglobal.com

Reviewed by Livea Coda

livea.coda@hedgepointglobal.com

livea.coda@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Global Markets LLC and its affiliates (“HPGM”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint Commodities LLC (“HPC”), a wholly owned entity of HPGM, is an Introducing Broker and a registered member of the National Futures Association. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and outside advisors before entering in any transaction that are introduced by the firm. HPGM and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. In case of questions not resolved by the first instance of customer contact (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ombudsman@hedgepointglobal.com) or 0800-878- 8408/ouvidoria@hedgepointglobal.com (only for customers in Brazil)

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.