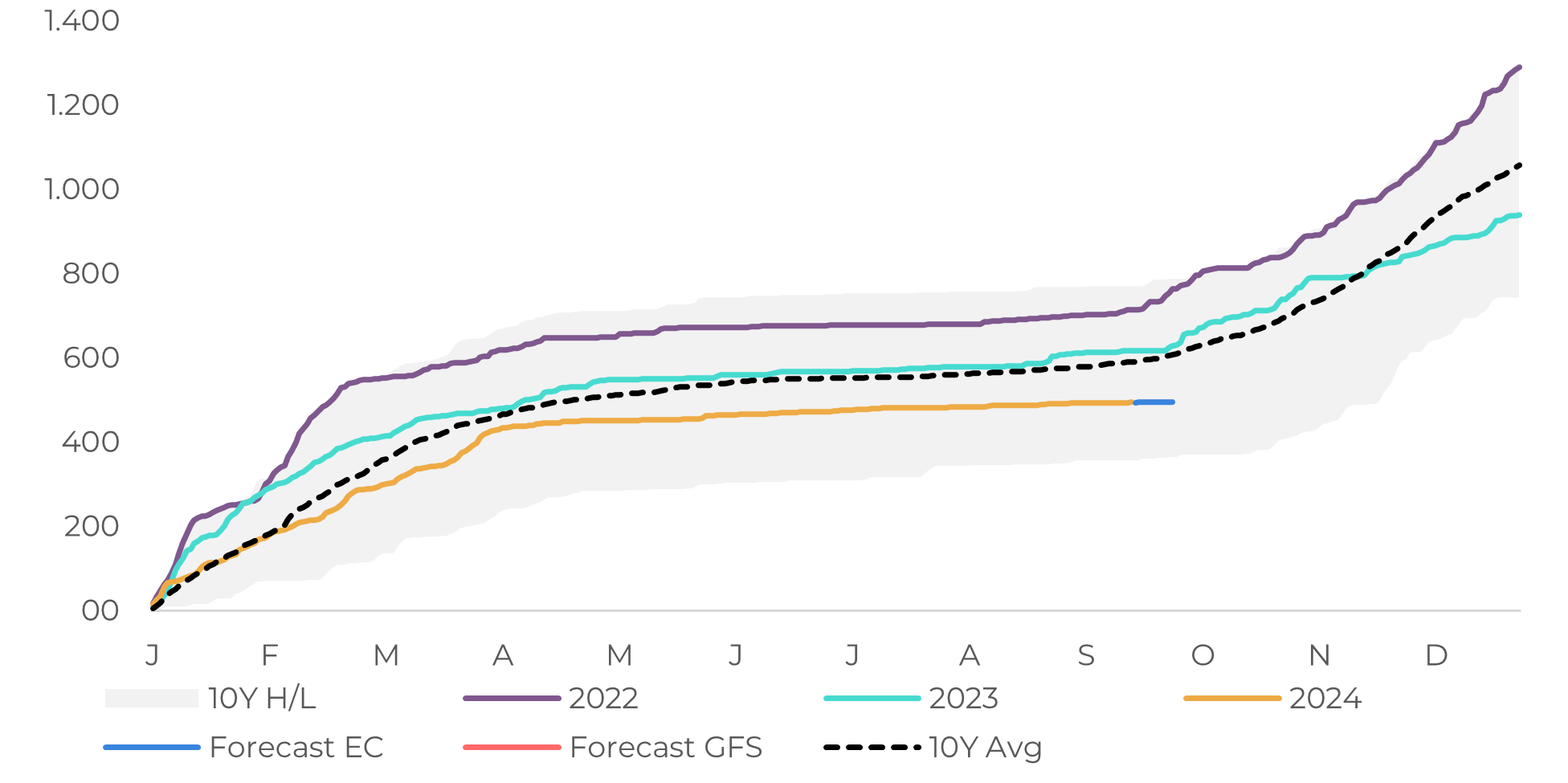

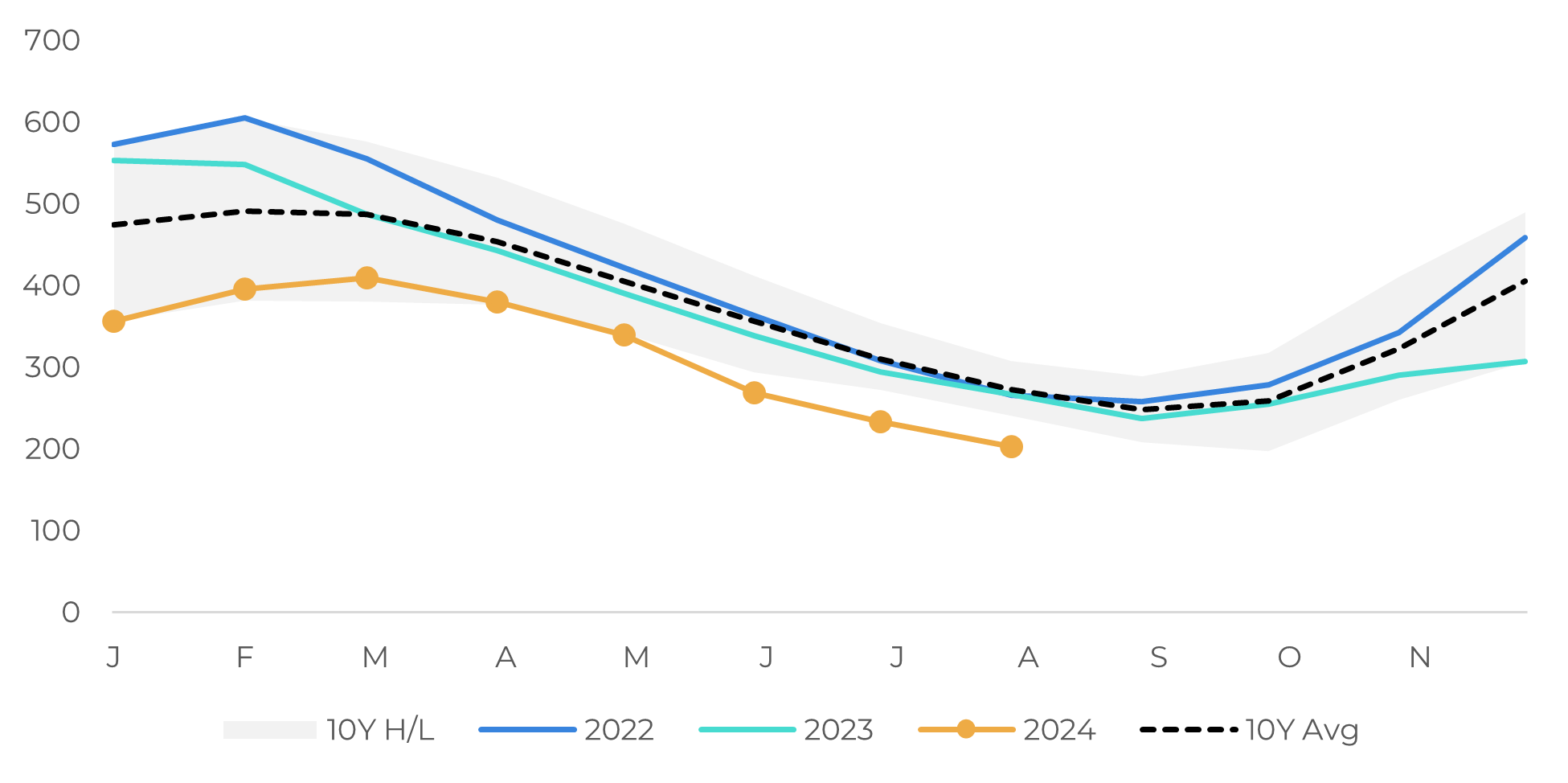

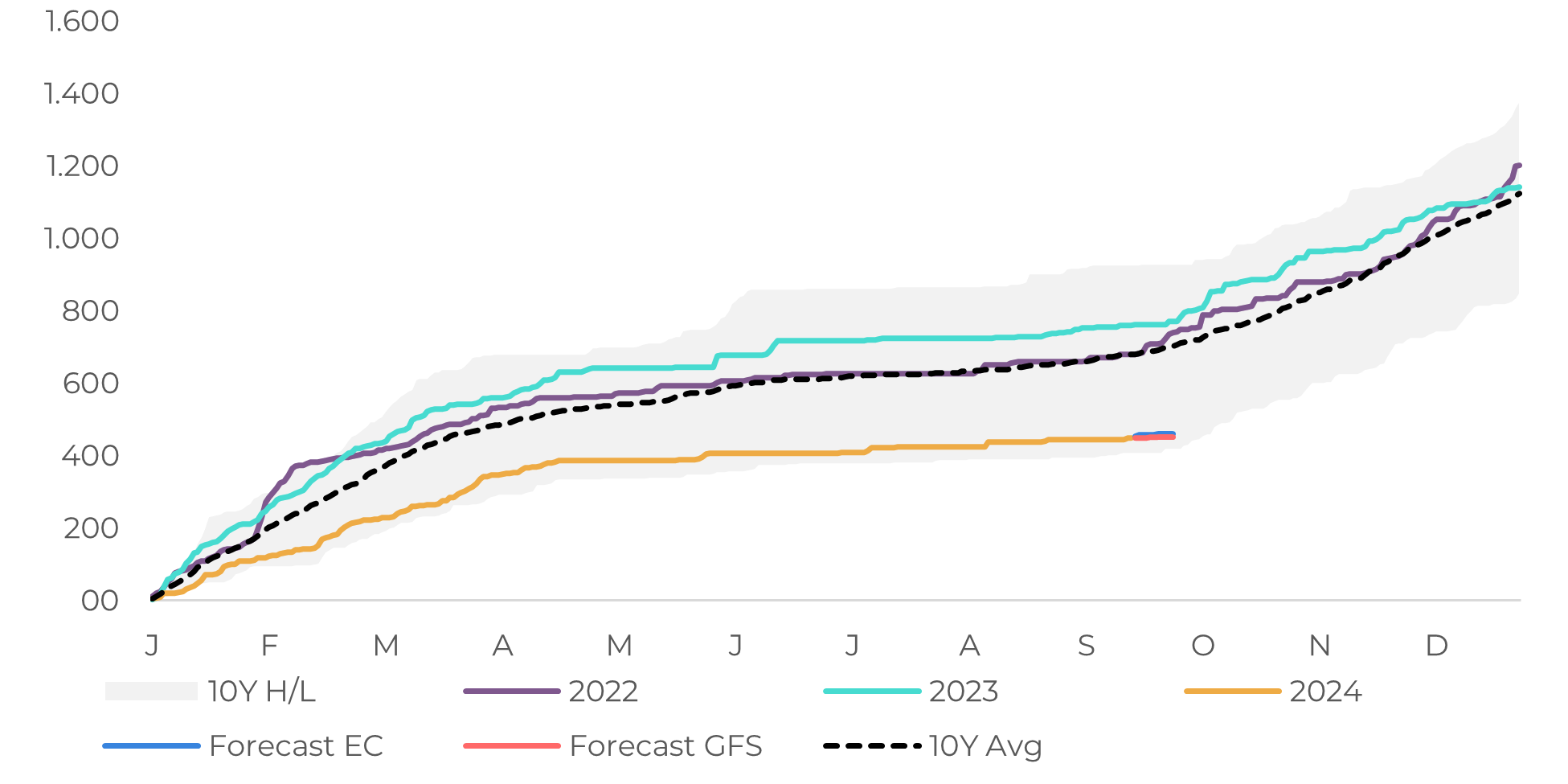

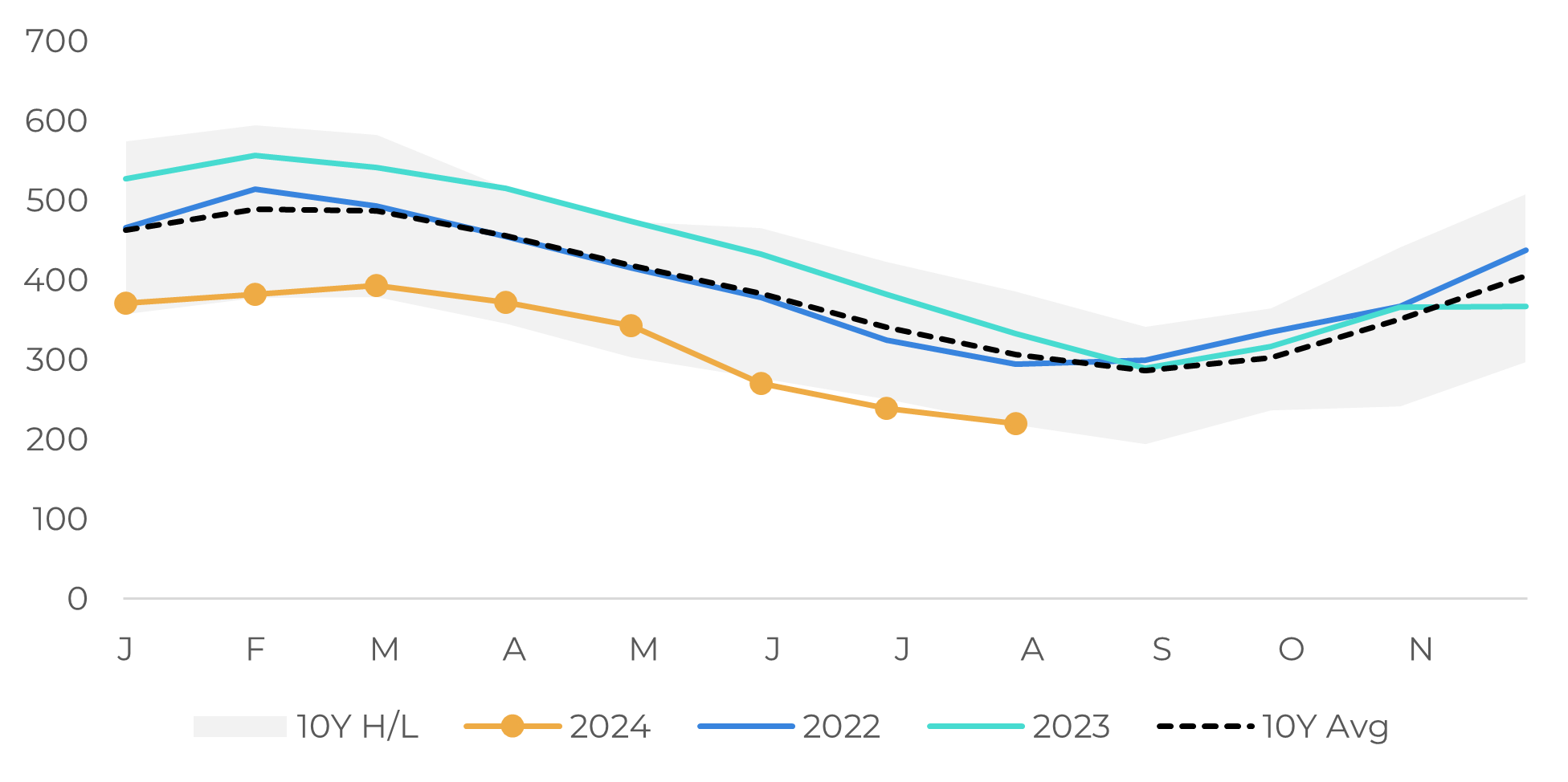

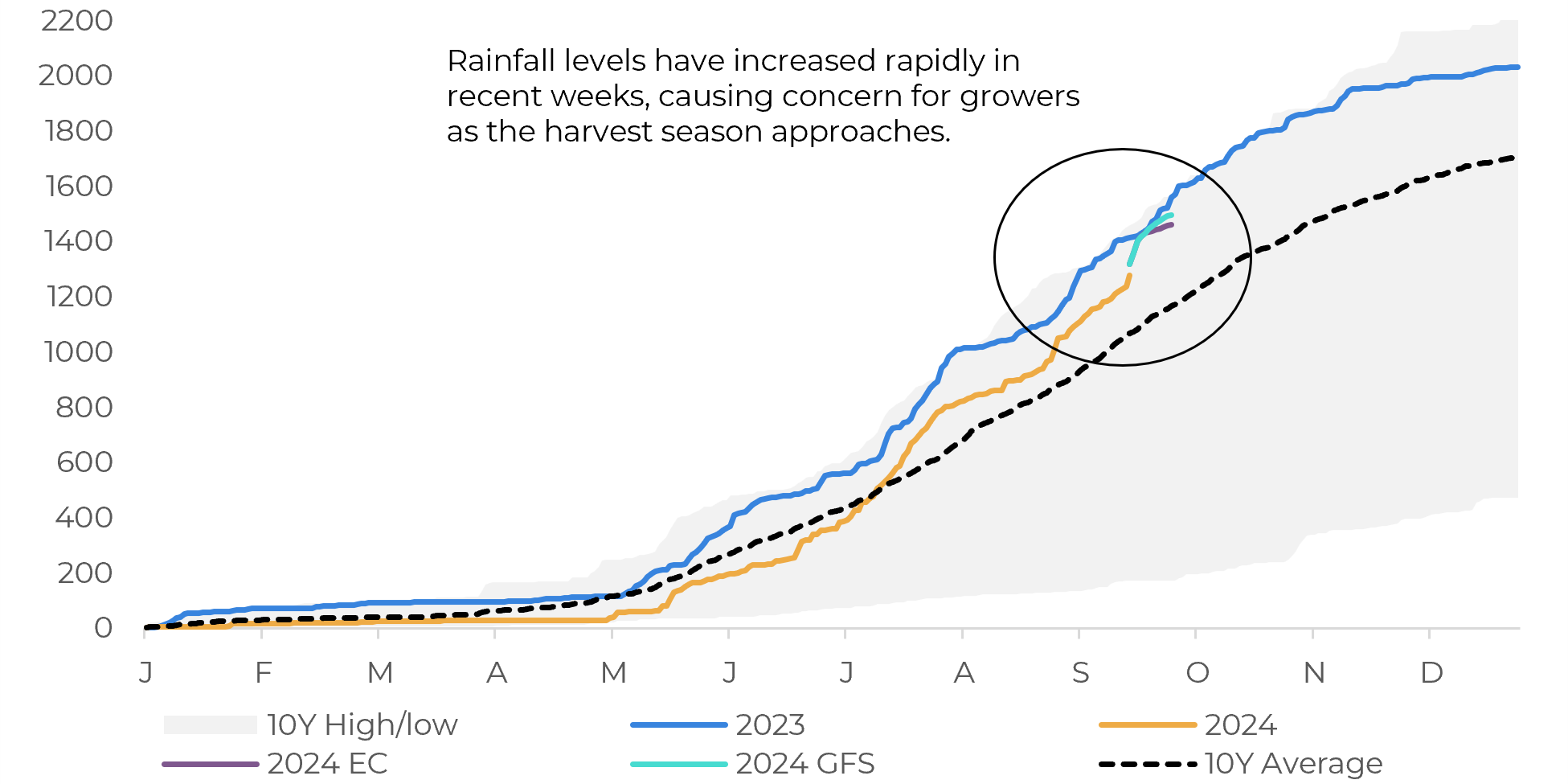

In the last few days, coffee futures have decreased, reaching multiple years records early this week after rains were reported in part of the coffee regions in Brazil. However, fundamentals still shows support to prices, as the volume of rainfall was still low, but might induce flowering. This may increase the risk of negative impacts on 25/26 season, as the forecast for the next weeks still shows scarce rainfall and high temperatures in the coming weeks.

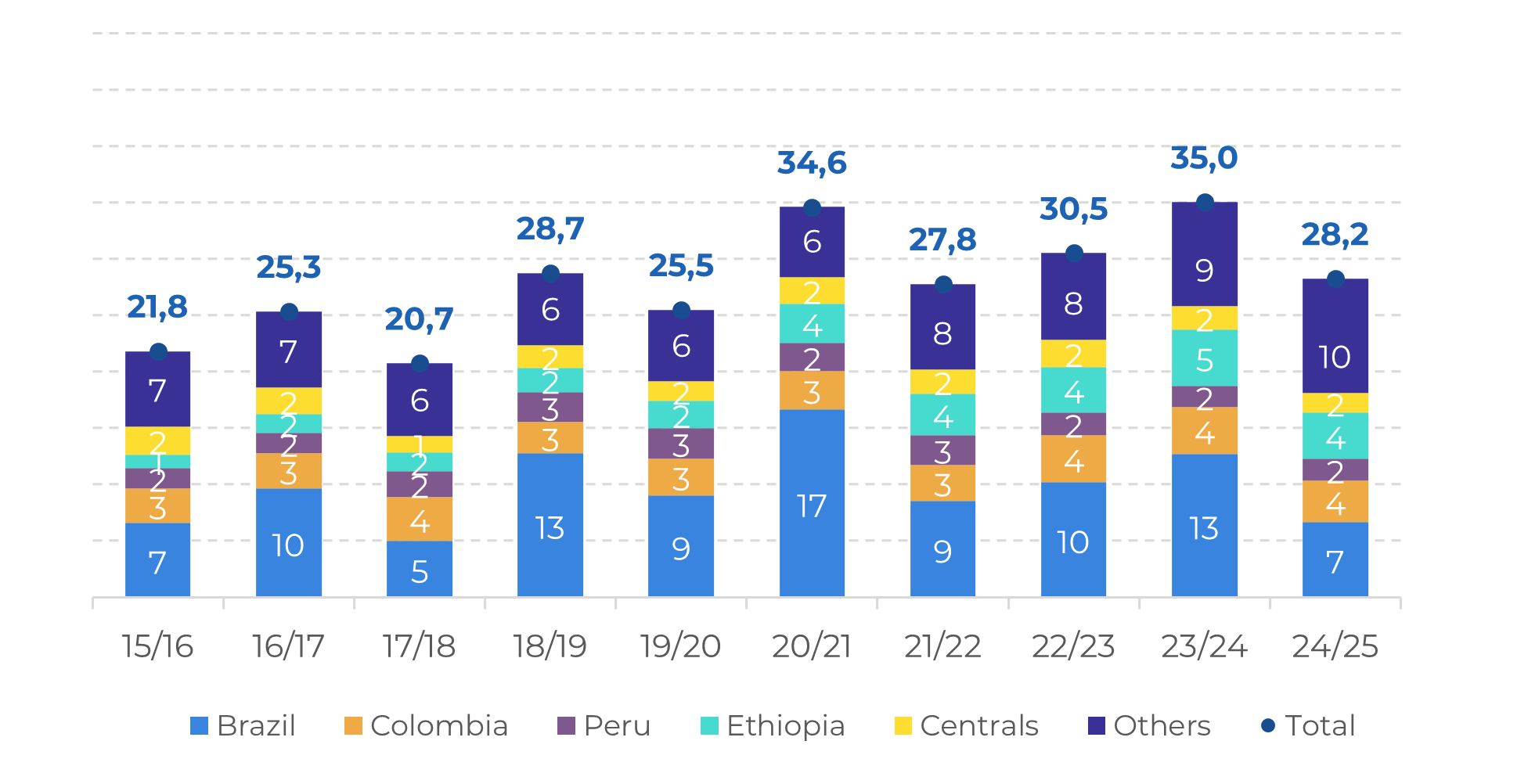

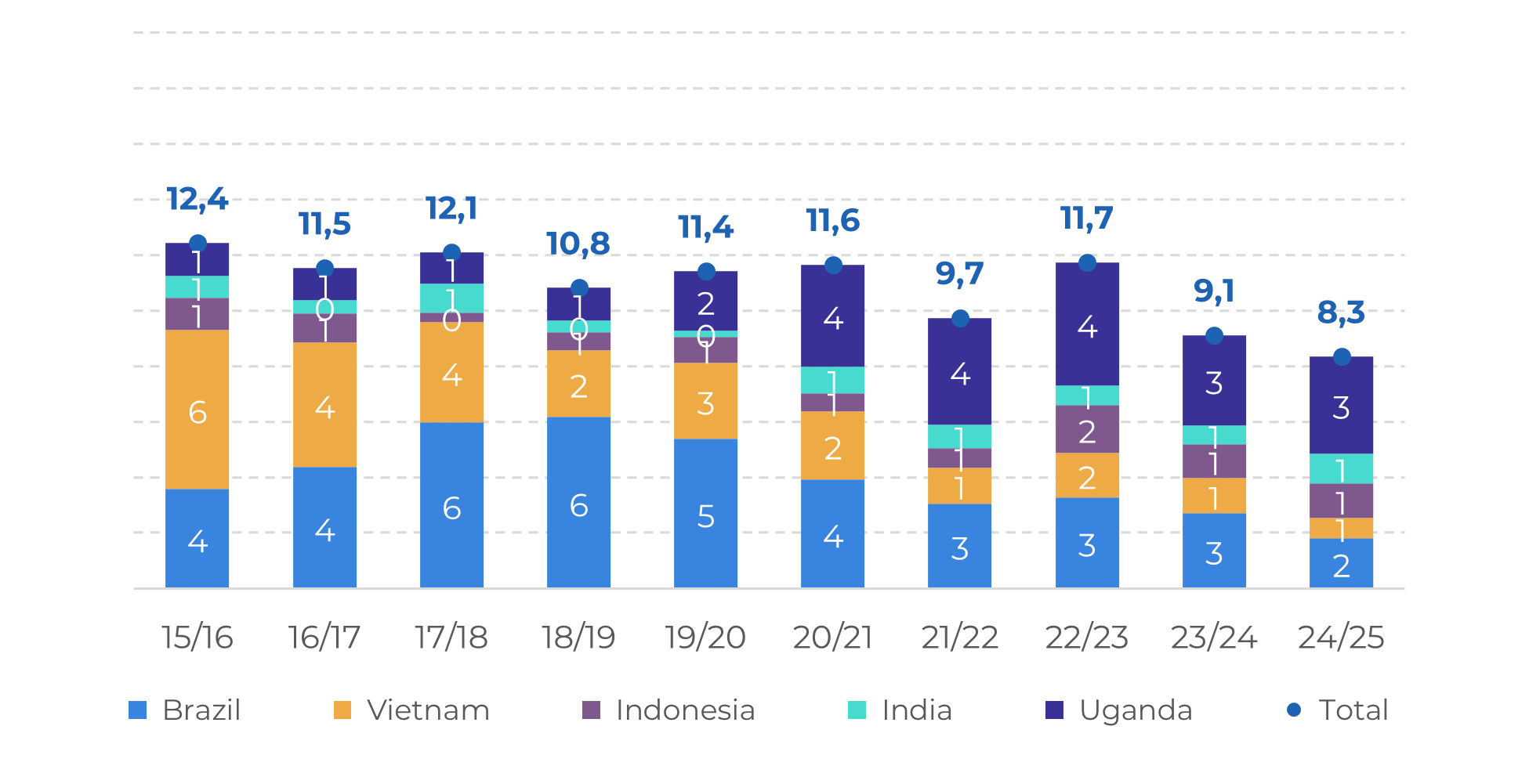

Moreover, soil moisture in most of the regions is also below averages and, in some case, even below historic lows. This also contributes to the increasing risk in the coffee market, especially since weather adversity already impacted 24/25 output. This Thursday, 19, Conab reduced 4 M bags its estimates for the 24/25 crop, to 54.8 M bags, with a reduction in both arabica, to 39.5 M bags, and conilon, to 15.2 M bags due to poor weather conditions during the development of the coffee trees. Our estimates are of 63 M bags in 24/25 (43 M of arabica and 20 M of conilon) 3 M bags below 23/24 numbers.