Oct 31

/

Natália Gandolphi

Crop Forecast: Coffee Brazil

24/25 Brazil Crop Update

In this report, we will go over the last updates on the 24/25 Brazilian crop. In the interest of focusing on the major regions, we will highlight the adjustments to South of Minas Gerais, Zona da Mata, and Espírito Santo.

As a result, with the revision of Brazil's numbers, the Supply and Demand (S&D) outlook is expected to show a surplus. The midpoint of the global balance shifted from -1.03 million bags to +3.38 million bags in 24/25, with the potential to reach 6.38 million bags in the upper range of estimates, considering a revision of the total production from 180.5 million bags to 184.9 million bags.

SMG shows more uniformity in rainfall within the analyzed cities, with an average dispersion of 4% among the three points. However, despite the improvement in precipitation (with the cumulative figure above the average, indicating progress compared to the last 3 years), other factors have impacted the growth of production volume in the region.

With levels similar to those in 2020, especially in the second half of the year, 2023 records higher average temperatures overall in the South of Minas region. This has affected the foliage coverage, which is below the adequate level, and consequently, has impacted productivity. Therefore, our estimate for the region has been changed from 19.35M bags to 17.93M bags (within the 17.22M bags range).

Unlike SMG, Zona da Mata showed greater dispersion of rainfall among the analyzed points.

The region also recorded higher daily temperatures, although not at historically high levels in all areas, as observed in SMG. Good foliage coverage also contributed to protection against more significant damage. Therefore, we readjusted ZDM's figures, closer to the high end of estimates, moving from 8.4M bags to 9.93M bags.

The region also recorded higher daily temperatures, although not at historically high levels in all areas, as observed in SMG. Good foliage coverage also contributed to protection against more significant damage. Therefore, we readjusted ZDM's figures, closer to the high end of estimates, moving from 8.4M bags to 9.93M bags.

Specific regions contribute to the dispersion of rainfall in Espírito Santo (Appendix III) but the overall outlook is optimistic. Despite the accumulated volume below average in some areas, especially after the volumes recorded in October, the non-uniformity of rainfall does not currently pose a threat to this year's production.

The temperature scenario in Espírito Santo is above average but does not pose immediate risks. Falling short of records in the 20-year historical data, regions are experiencing higher temperatures – a result of El Niño, as in other areas – but there are no immediate threats to productivity at the moment. Consequently, the figure was revised up, to 22.91M bags (including arabica and robusta).

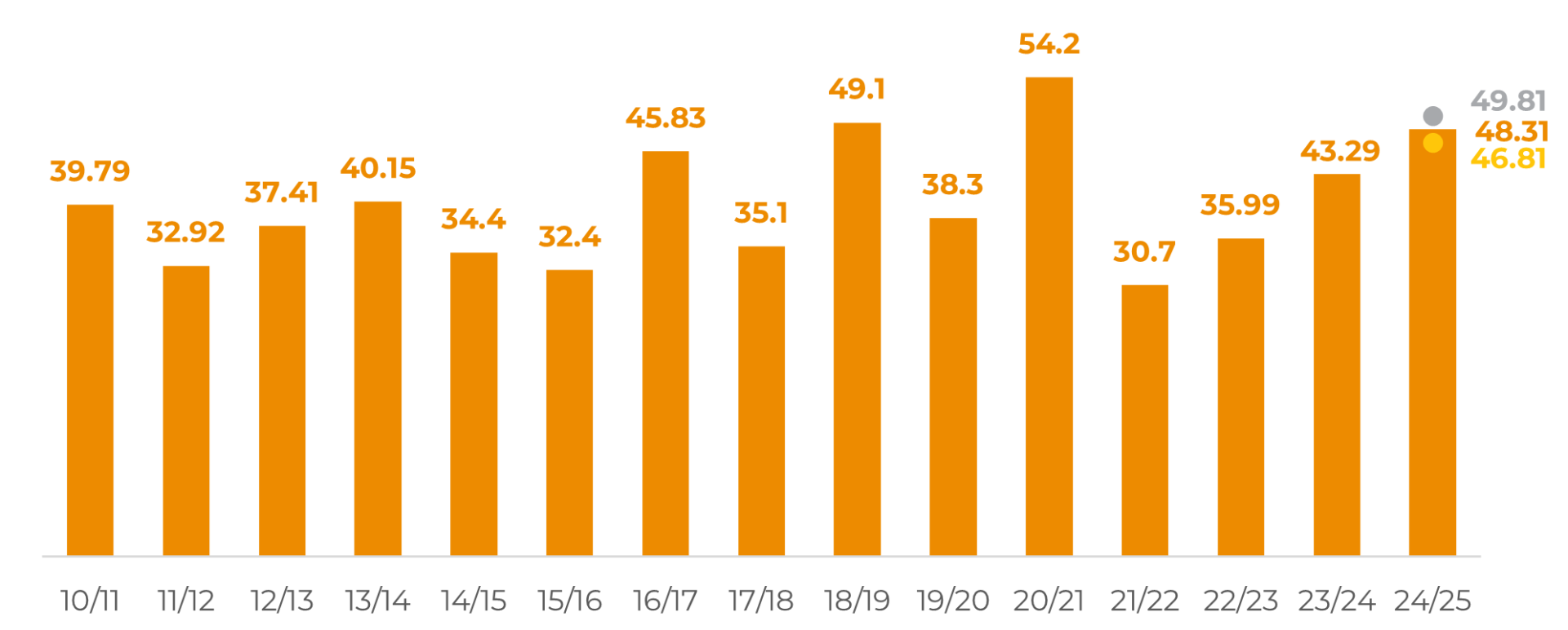

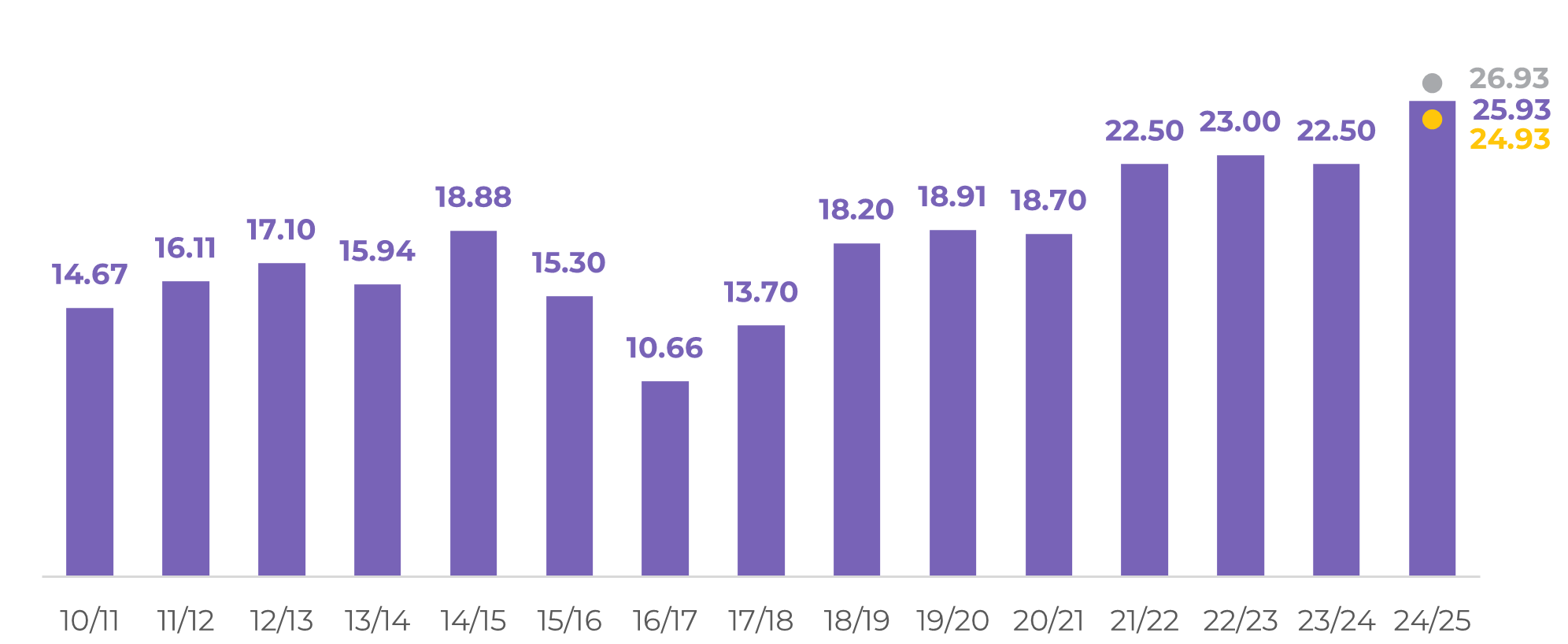

Alongside other minor adjustments, our arabica figure for 24/25 moved from 47.63M bags to 48.31M bags, and conilon from 23.28M bags to 25.93M bags.

The region also recorded higher daily temperatures, although not at historically high levels in all areas, as observed in SMG. Good foliage coverage also contributed to protection against more significant damage. Therefore, we readjusted ZDM's figures, closer to the high end of estimates, moving from 8.4M bags to 9.93M bags.

The region also recorded higher daily temperatures, although not at historically high levels in all areas, as observed in SMG. Good foliage coverage also contributed to protection against more significant damage. Therefore, we readjusted ZDM's figures, closer to the high end of estimates, moving from 8.4M bags to 9.93M bags.

Specific regions contribute to the dispersion of rainfall in Espírito Santo but the overall outlook is optimistic. Despite the accumulated volume below average in some areas, especially after the volumes recorded in October, the non-uniformity of rainfall does not currently pose a threat to this year's production.

The temperature scenario in Espírito Santo is above average but does not pose immediate risks. Falling short of records in the 20-year historical data, regions are experiencing higher temperatures – a result of El Niño, as in other areas – but there are no immediate threats to productivity at the moment. Consequently, the figure was revised up, to 22.91M bags (including arabica and robusta).

Alongside other minor adjustments, our arabica figure for 24/25 moved from 47.63M bags to 48.31M bags, and conilon from 23.28M bags to 25.93M bags.

As a result, with the revision of Brazil's numbers, the Supply and Demand (S&D) outlook is expected to show a surplus. The midpoint of the global balance shifted from -1.03 million bags to +3.38 million bags in 24/25, with the potential to reach 6.38 million bags in the upper range of estimates, considering a revision of the total production from 180.5 million bags to 184.9 million bags.

Arabica Production, Midpoint and Range – Brazil (M bags)

Source: hEDGEpoint

Robusta Production, Midpoint and Range – Brazil (M bags)

Source: hEDGEpoint

In Summary

The 24/25 Brazilian crop update focuses on South of Minas Gerais, Zona da Mata, and Espírito Santo. SMG experiences uniform rainfall but contends with production challenges, leading to a revised estimate of 17.93M bags due to higher temperatures impacting foliage coverage. ZDM faces rainfall dispersion but maintains good foliage coverage, resulting in an adjustment to 9.93M bags. Despite rainfall disparities in Espírito Santo, the overall outlook is optimistic, with no immediate risks from temperature scenarios. Overall adjustments anticipate a surplus, with the global balance potentially reaching 3.38M bags, driven by a revised total production estimate of 184.9M bags.

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.