Crop Forecast: Brazilian Crop Update 25/26

Brazilian Crop Update 25/26

In this report, we will update the projection for the 25/26 Brazilian crop, discussing in more detail the changes in Hedgepoint's numbers, especially as we enter the harvest period. Our estimates point to a total production of 63.8 M bags in the next cycle, 0.6% higher than the 24/25 estimates, with an increase in the volume expected for Conilon, but a reduction in the numbers for Arabica.

While in our February estimate (link) we expected 42.6 M sc of Arabica, we reduced this volume to 39.6 M bags. The reduction reflected the low rainfall level during the new crop's development. Despite the good volumes between October and December 2024, the weather for the rest of last year, especially in the flowering period, was marked by below-average rainfall, in addition to high temperatures in some months, which ended up harming the development of the 25/26 season.

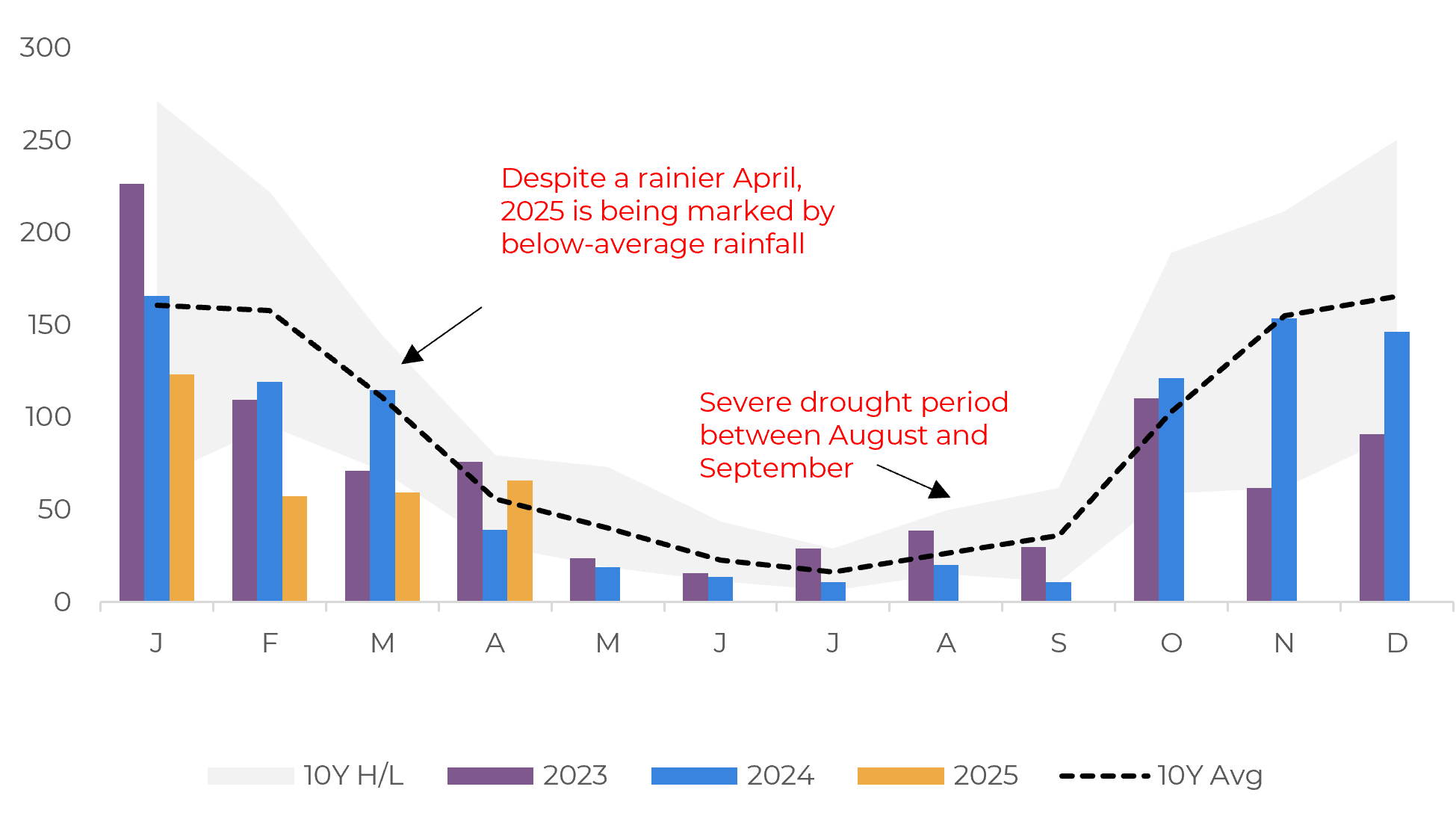

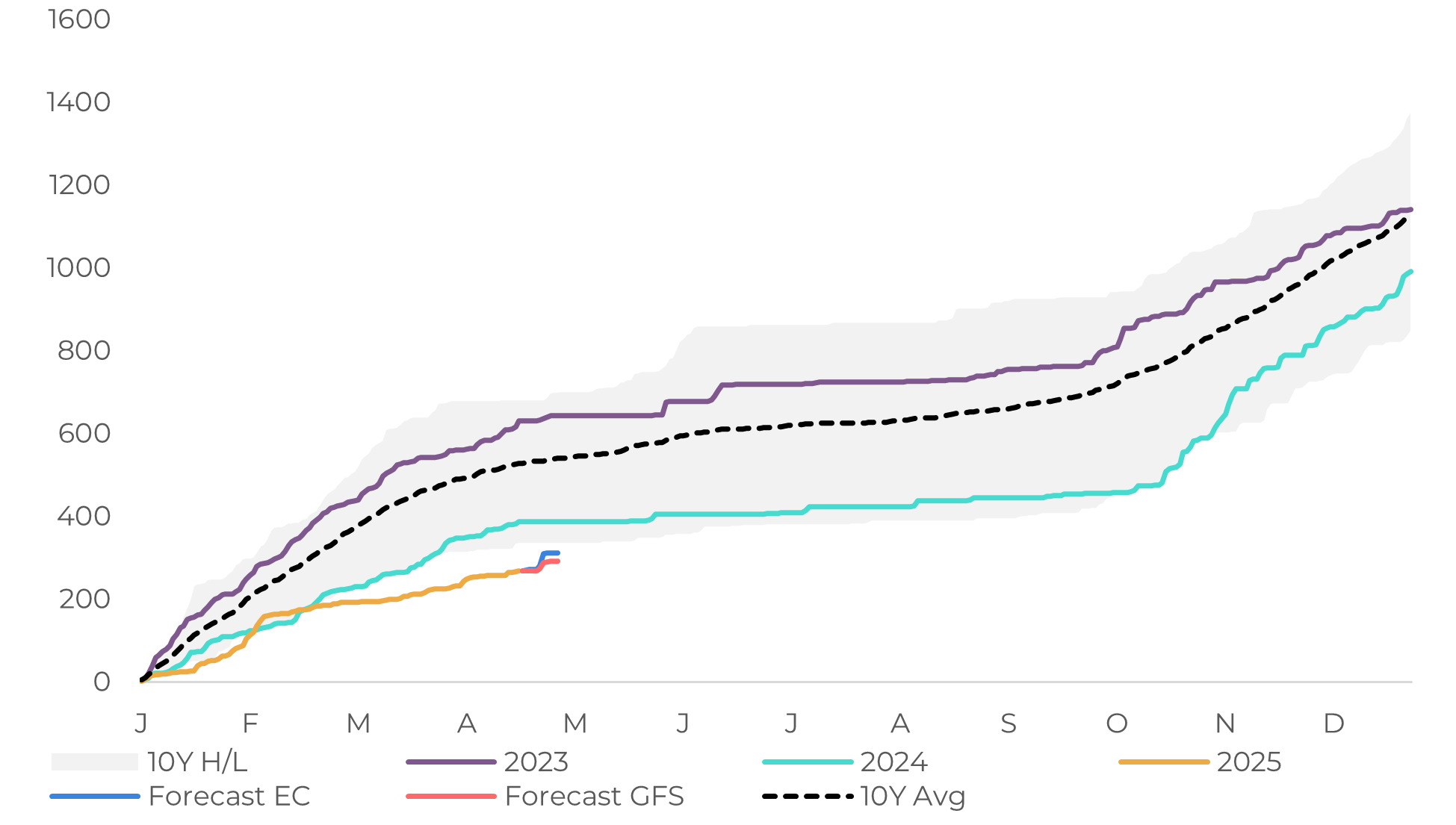

Brazil: Monthly Cumulative Precipitation in Coffee Areas (mm)

Source: Refinitiv, Hedgepoint

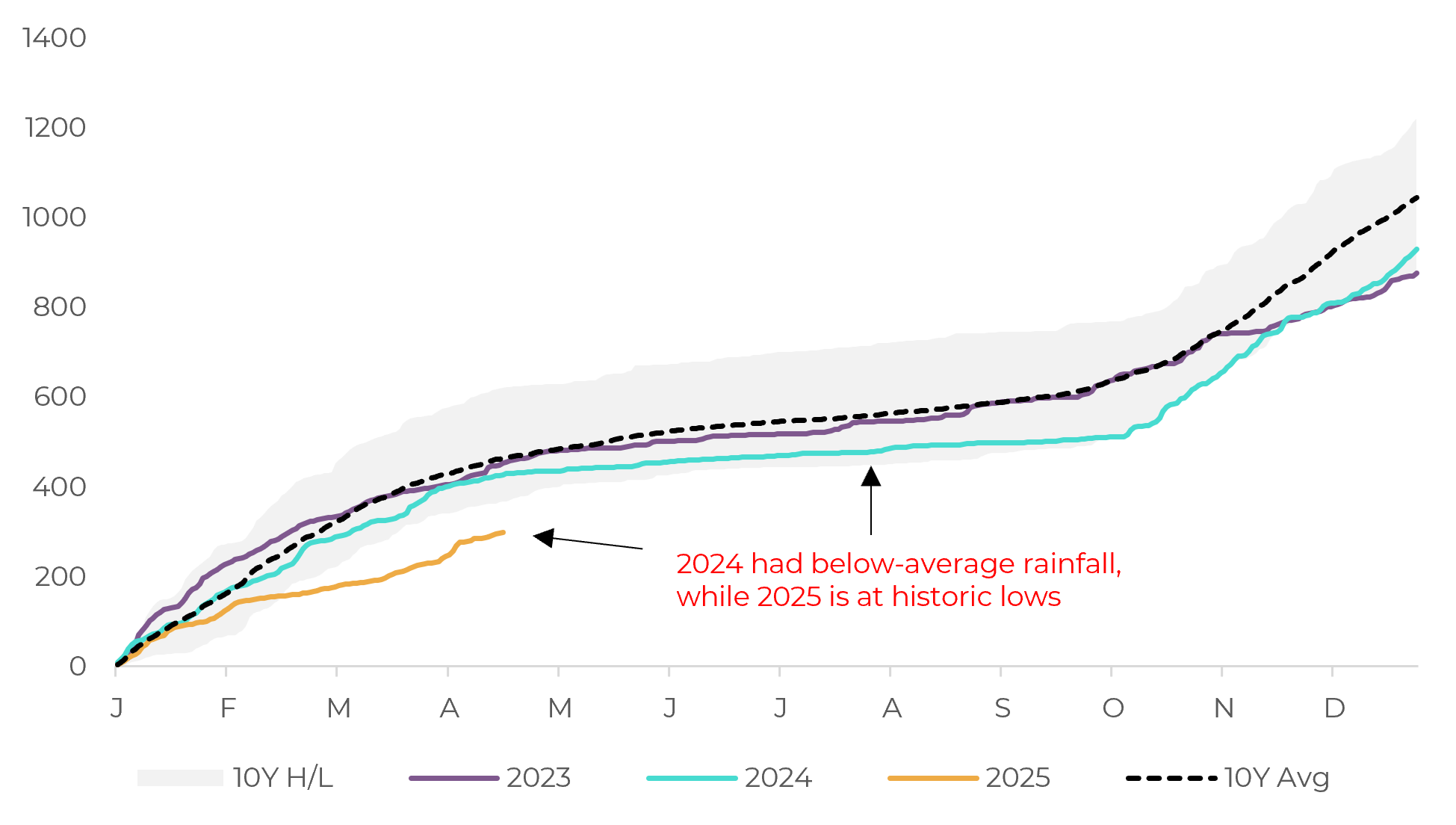

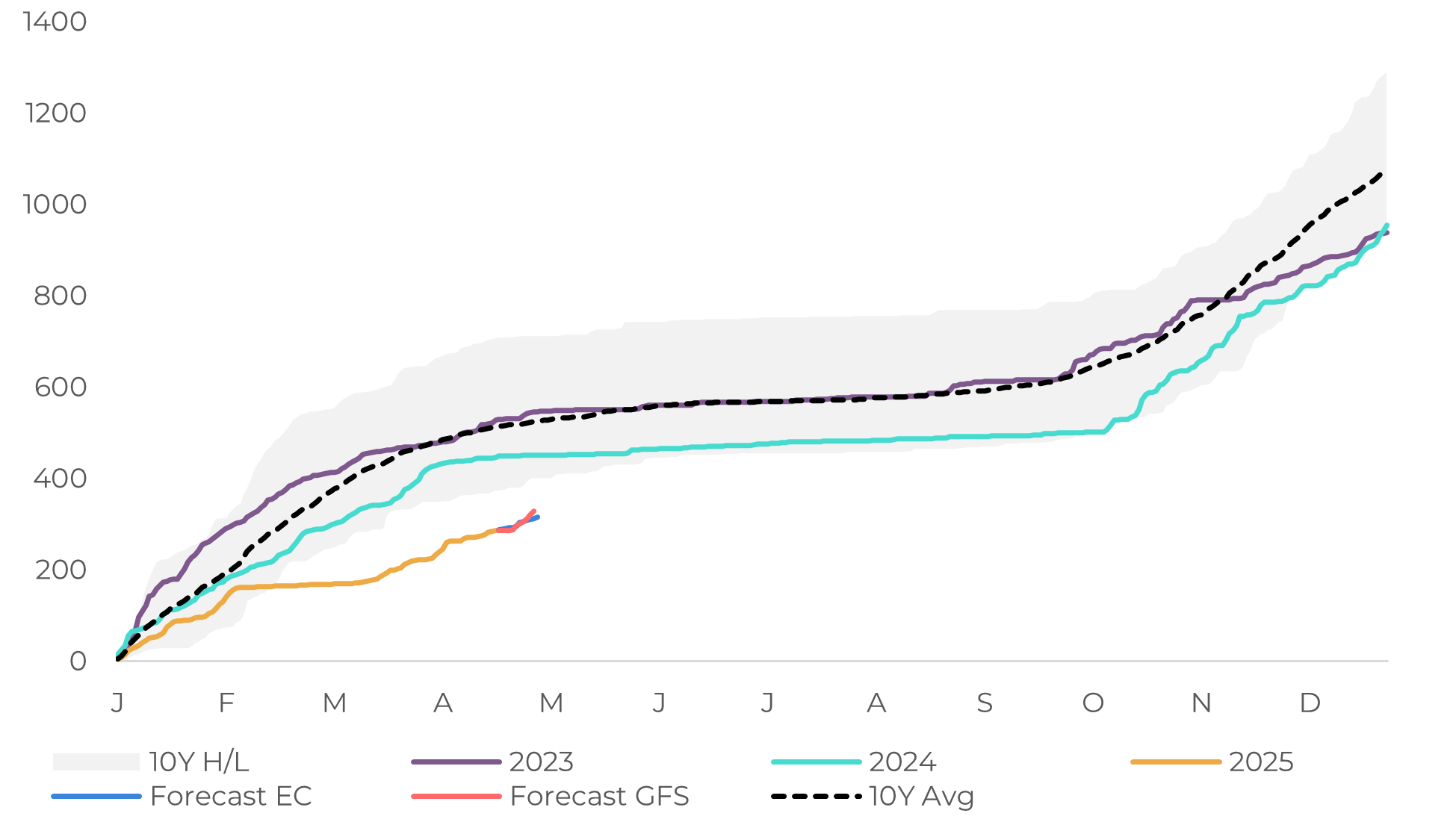

Brazil: Cumulative Precipitation in Coffee Areas (mm)

Source: Refinitiv, Hedgepoint

In 2025, rainfall also remained below average, with the year-to-date volume at minimum levels. On the other hand, it is believed that the effect of low humidity at the beginning of the year may not have such significant impacts on processing yield in most areas. Initially, there were also greater concerns about the effect of the weather in 26/27 season, however, the rains in April helped in the condition of the coffee trees, bringing better expectations for the next season.

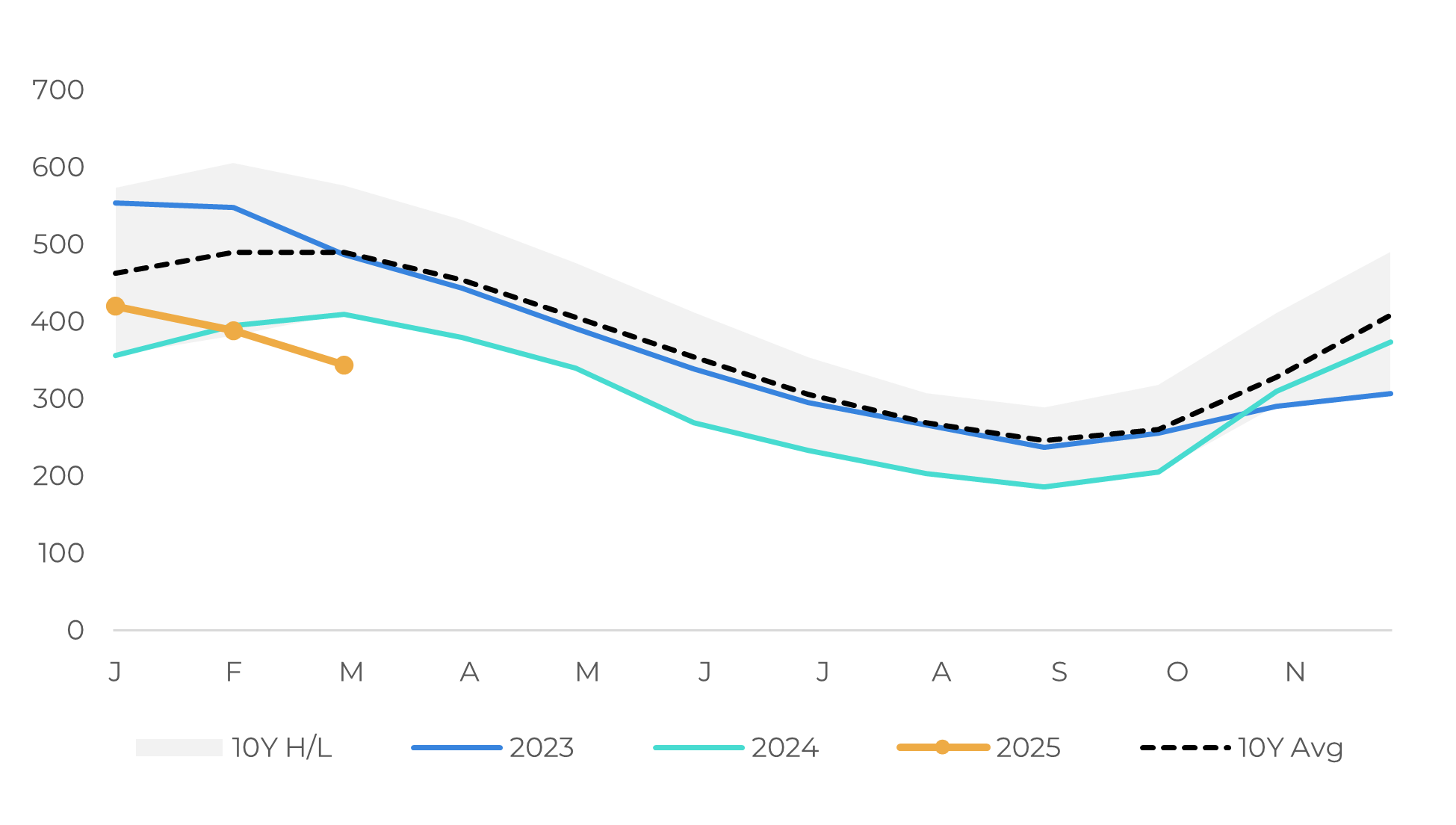

Regionally, Cerrado had rainfall in line with the historical average. However, Sul de Minas, Zona da Mata and the state of São Paulo witnessed rainfall below the 10-year average, both in 2024 and 2025. Soil moisture in these regions also remained low, despite volumes closer to average between November and December 2024.

The drought in 2025 does not seem to have had such a big impact on beans filling, and we expect an improvement in screen size compared to 24/25, due to the good rains at the end of 2024. The exception is the state of São Paulo, which witnessed higher temperatures in addition to the drought, with possible impacts on processing yield. Even so, adverse weather caused many producers to increase pruning, with a focus on 26/27 production, which reduced the production potential in the 25/26 harvest.

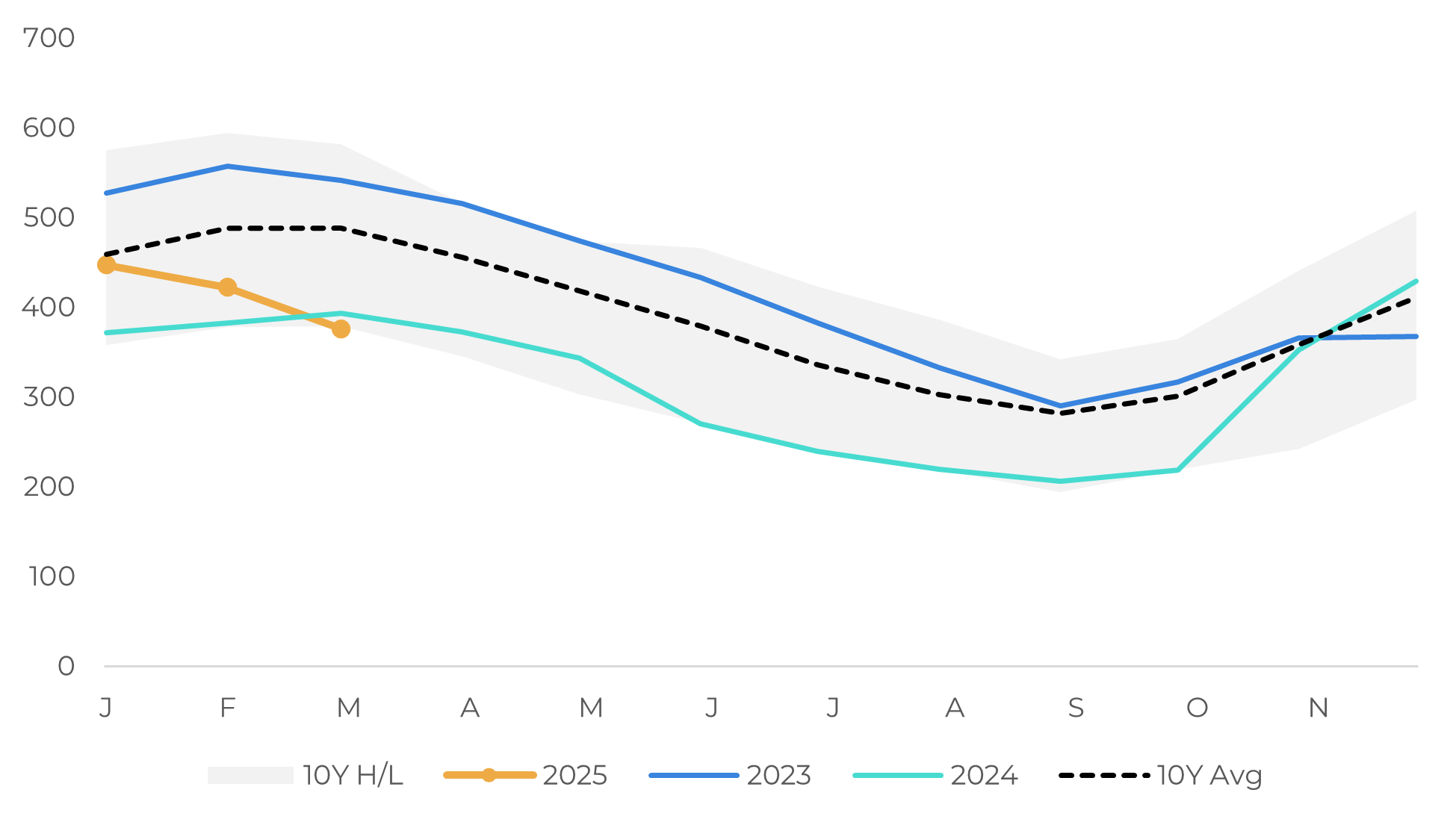

Brazil: Cumulative Precipitation – Minas Gerais (mm)

Source: Refinitiv, Hedgepoint

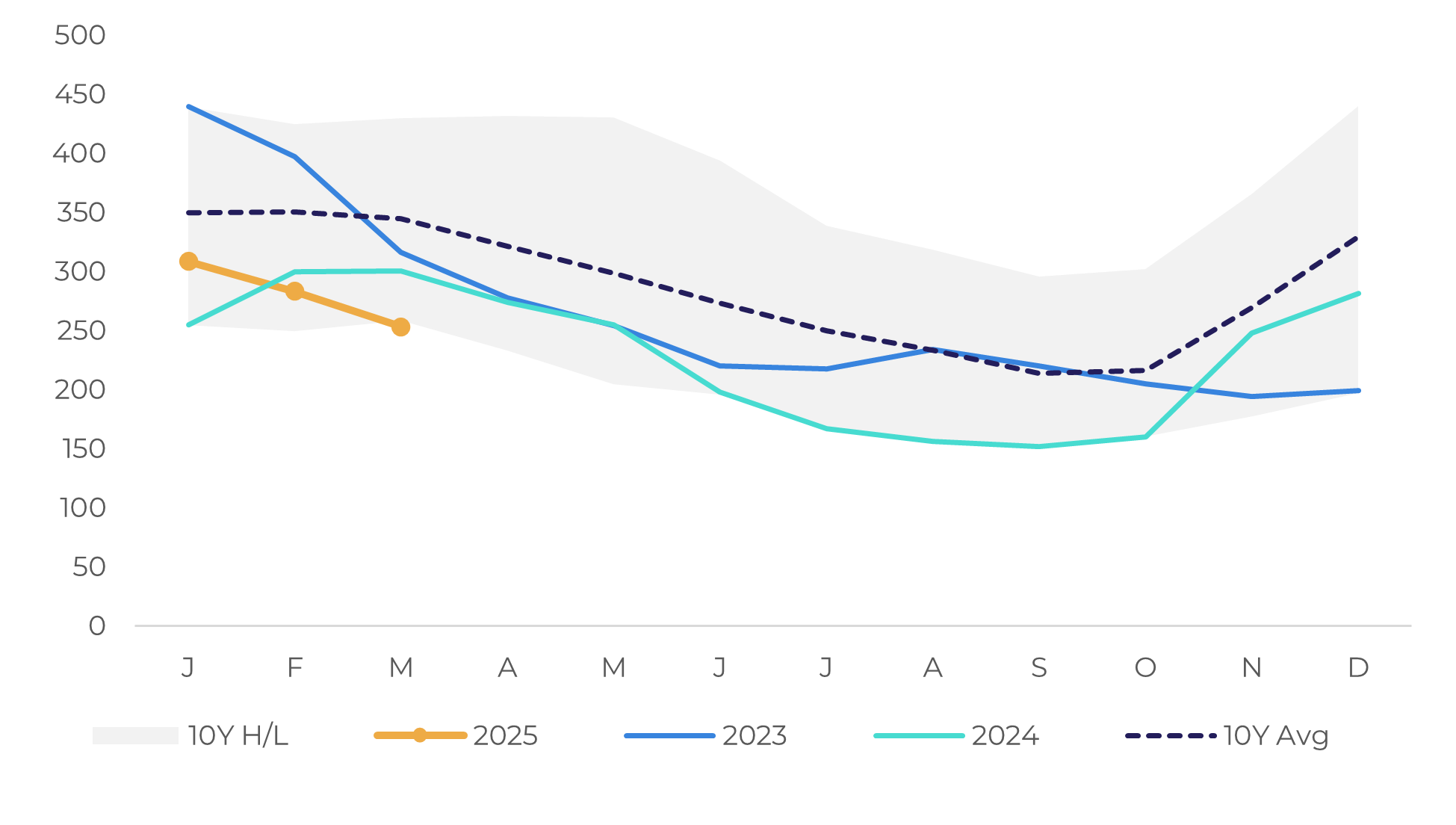

Brazil: Soil Moisture – Minas Gerais (mm/0-1.6 m)

Source: Refinitiv, Hedgepoint

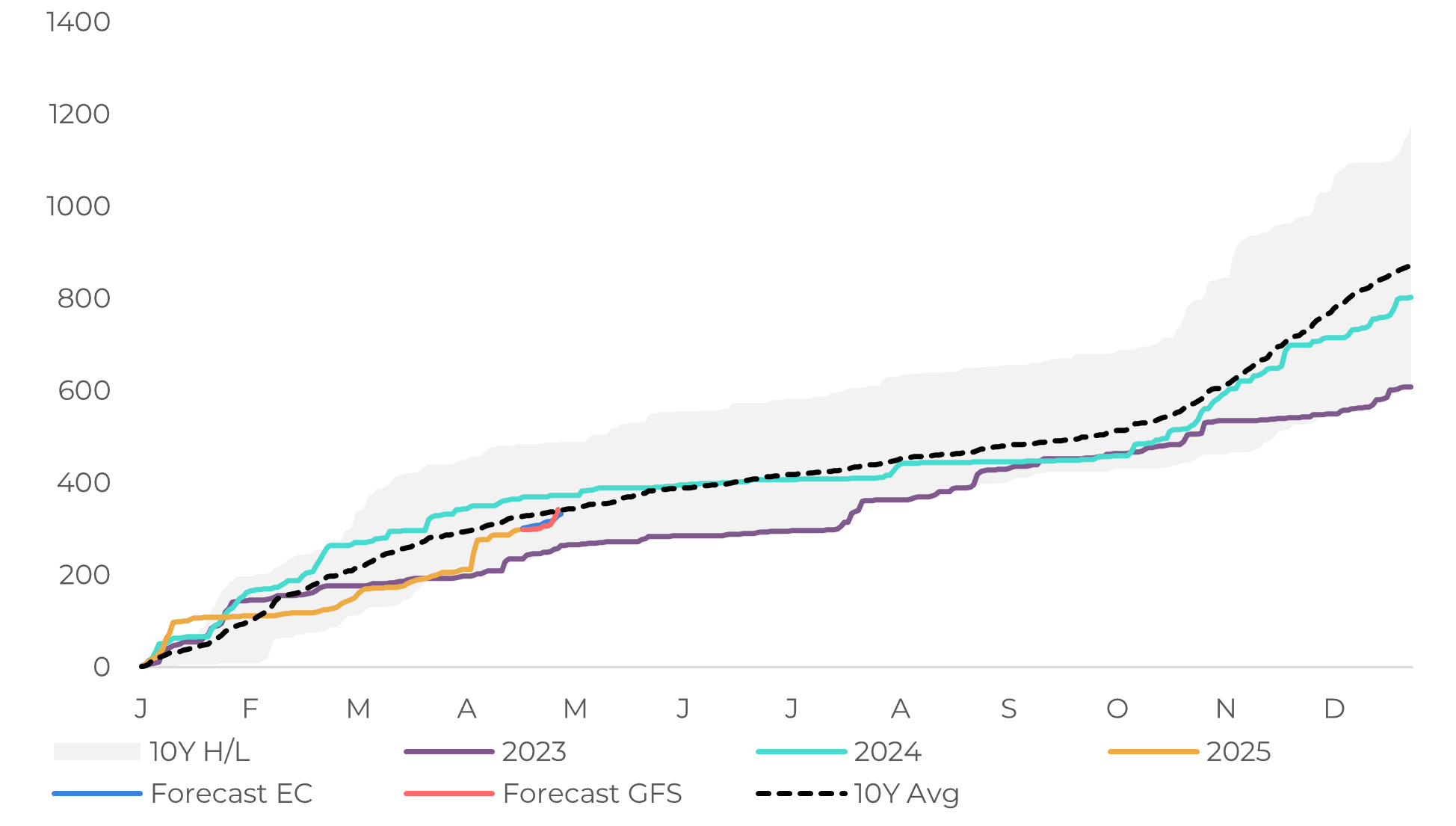

Brazil: Cumulative Precipitation – São Paulo (mm)

Source: Refinitiv, Hedgepoint

Brazil: Soil Moisture – São Paulo (mm/0-1.6 m)

Source: Refinitiv, Hedgepoint

In the regions of Conilon, the outlook is more positive. In Espírito Santo, the largest producing state of the variety, the weather in 2024 was wetter than in the regions of Arabica, with more uniform rainfall. In 2025, rainfall also remained more in line with the historical average. Thus, even with lower soil moisture, the productive potential is more optimistic, with a higher expected yield. The same pattern is also observed in other regions such as Bahia and Rondônia.

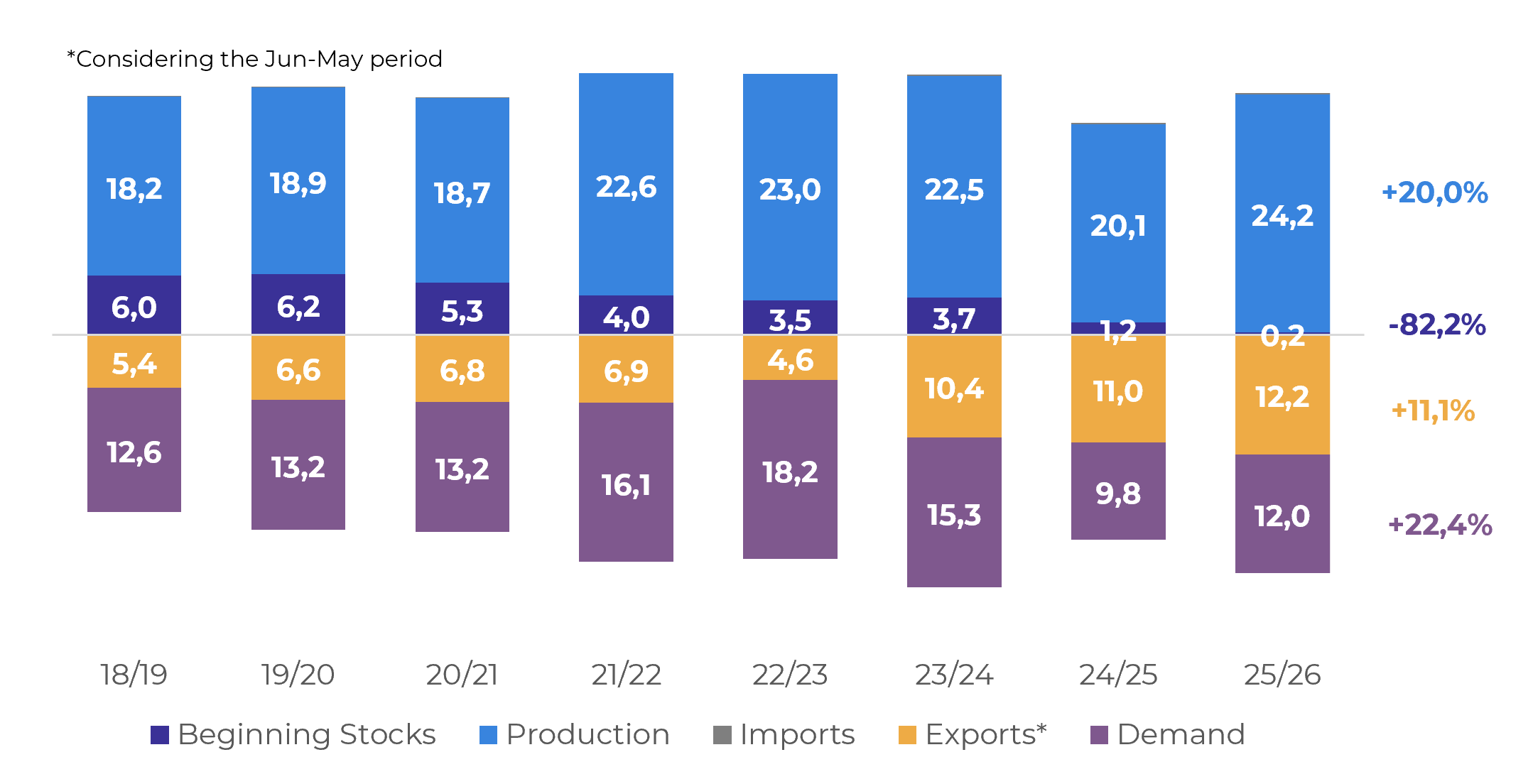

In addition, with higher coffee prices, producers continued to invest more in crops – including in the construction of artesian wells and irrigation systems – leading to a higher production expectation in the 25/26 harvest. Thus, while in February we estimated 22.5 M bags of Conilon in this next cycle, we increased this volume to 24.2 M bags, a rise of 20% compared to 24/25.

Brazil: Cumulative Precipitation – Espírito Santo (mm)

Source: Hedgepoint

Brazil: Soil Moisture – Espírito Santo (mm/0-1.6 m)

Source: Hedgepoint

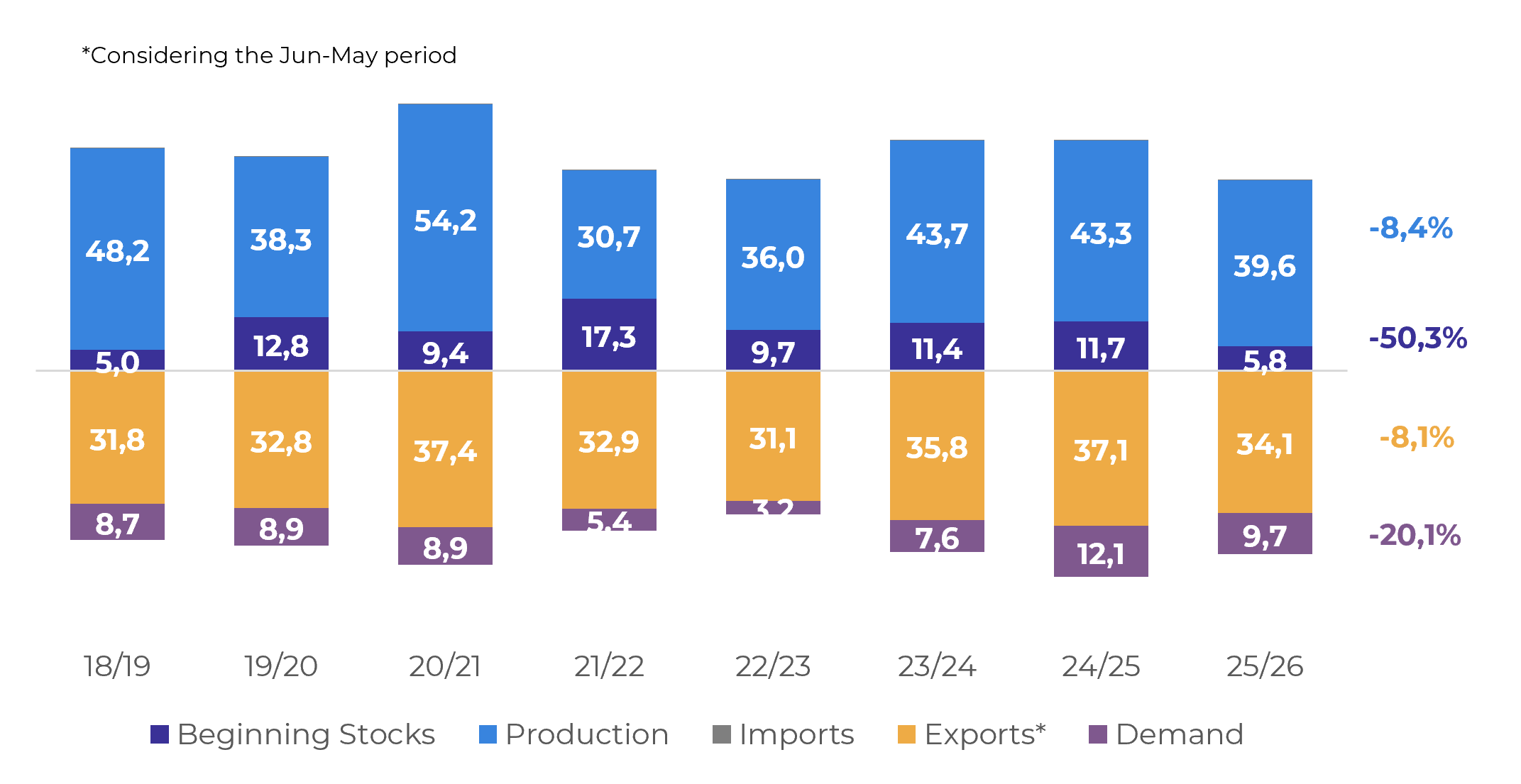

The change in production estimates also led us to revise our export figures for the 25/26 crop year. For Arabica, the expectation of lower production combined with lower carryover stocks and a possible drop in global demand may reduce shipments in the 25/26 cycle (June-May). Our estimates are for exports of 34.1 M of Arabica (green and processed), a decrease of 8.1% compared to the 24/25 estimate. For Conilon, we expect a total shipment of 12.2 M bags, an increase of 11.1% compared to the 24/25 estimate.

Finally, regarding demand, we reduced our expectation, with a slight decrease of 1% in 25/26. This picture is especially a reflection of the increase in consumer prices, with ABIC's retail price accumulating an increase of 102% in the first quarter of 2025, compared to the same period in 2024. In addition, the trade war between the US and China can still have negative impacts on the global economy, affecting coffee consumption.

However, we highlight that the decline is expected on the side of Arabica (20.1% vs 24/25), while Conilon may have an increase in demand (22.4% x 24/25), due to the lower prices of the variety compared to Arabica, which should lead to changes in the national mix.

Brazil: Arabica Supply and Demand (M bags)

Source: Hedgepoint

Brazil: Conilon/Robusta Supply and Demand (M bags)

Source: Hedgepoint

In Summary

Brazil's 25/26 season is expected to have a production close to the 24/25 cycle, with 63.8 M of bags. However, we reduced Arabica coffee production to 39.6 M bags (-8.4% vs 24/25), due to adverse weather in 2024 and pruning carried out in coffee plantations. Despite the drought in early 2025, in general, the processing yield tends to be better than in 24/25, due to the good rains between October and December. For Conilon, we have increased our expectation to 24.2 M bags (+20% x 24/25), due to good crop conditions and larger harvested area.

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.