26/27 Brazilian Coffee Crop Estimate

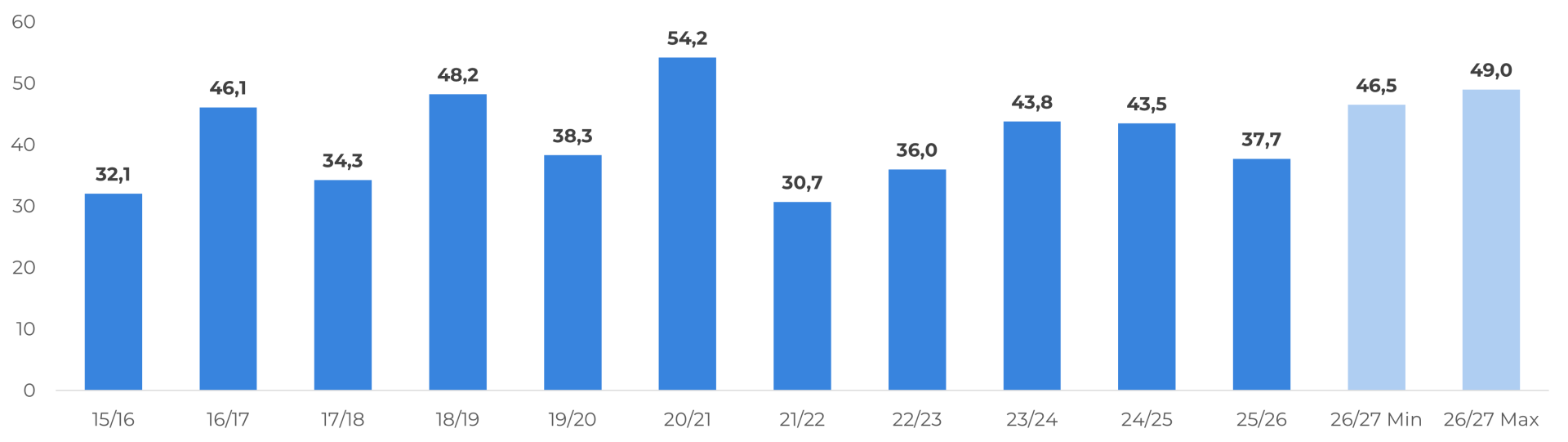

Rains in October and November allowed the Arabica flowers to set

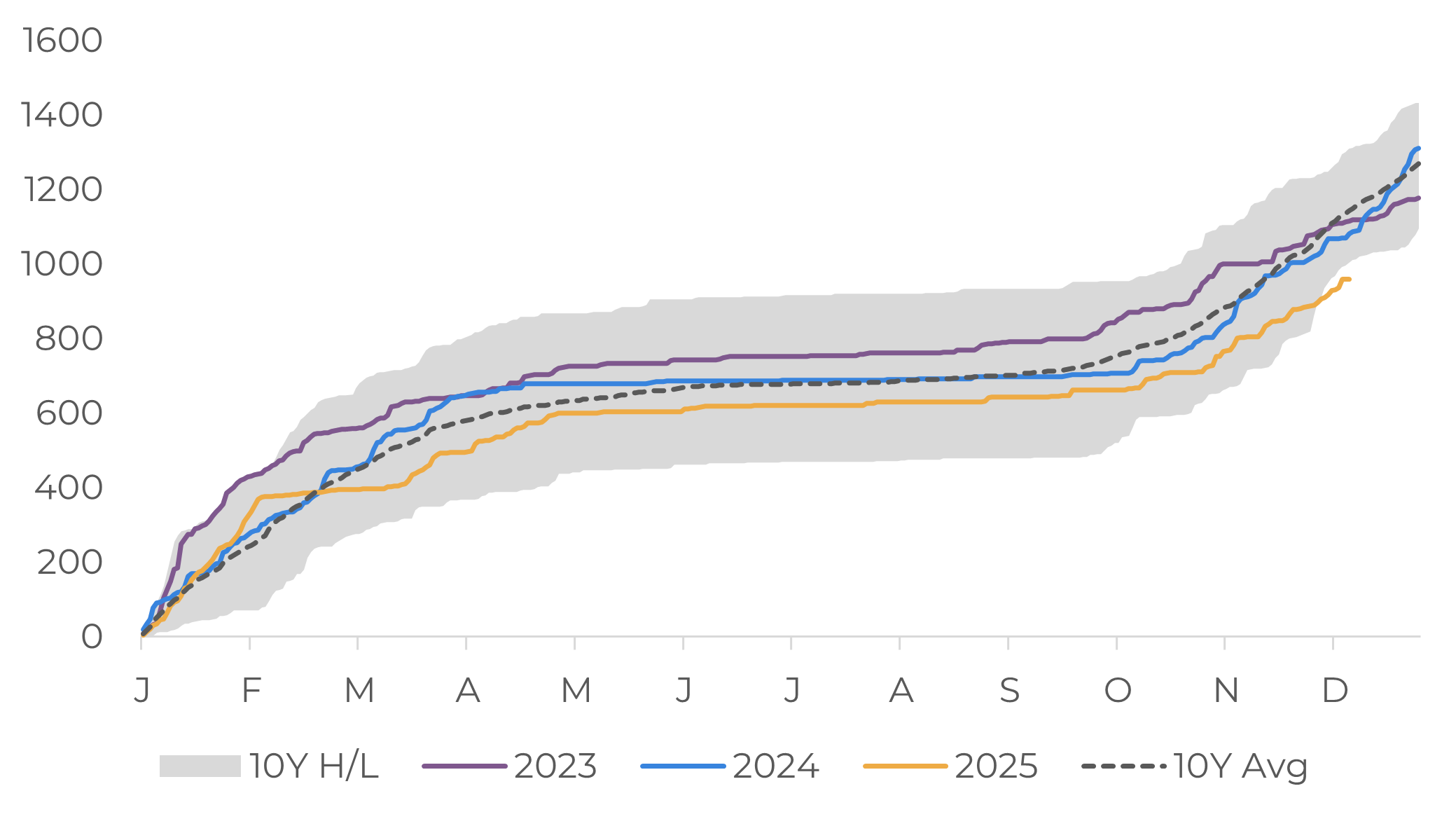

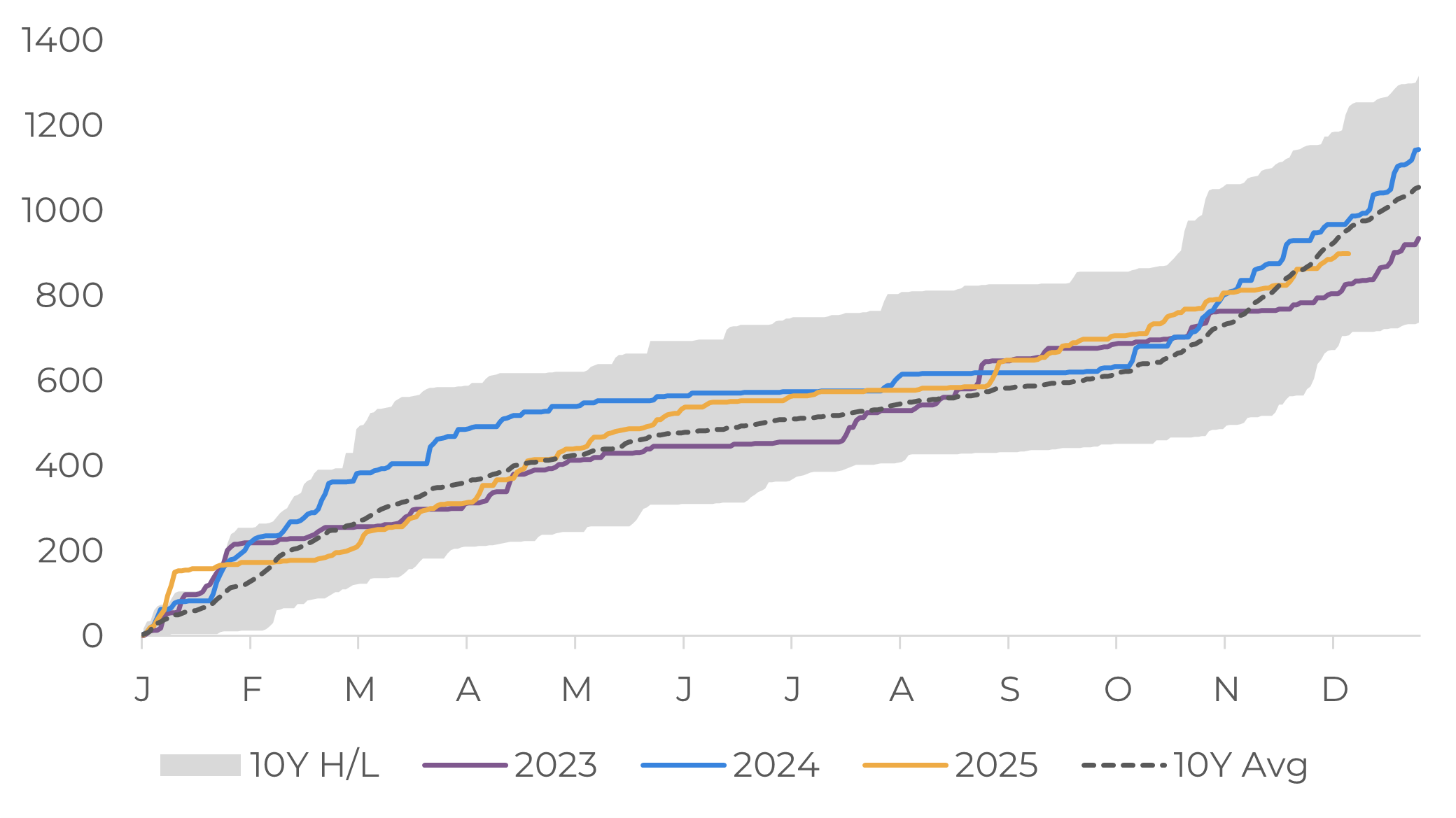

Minas Gerais: Weighted Cumulative Precipitation in Coffee Areas (mm)

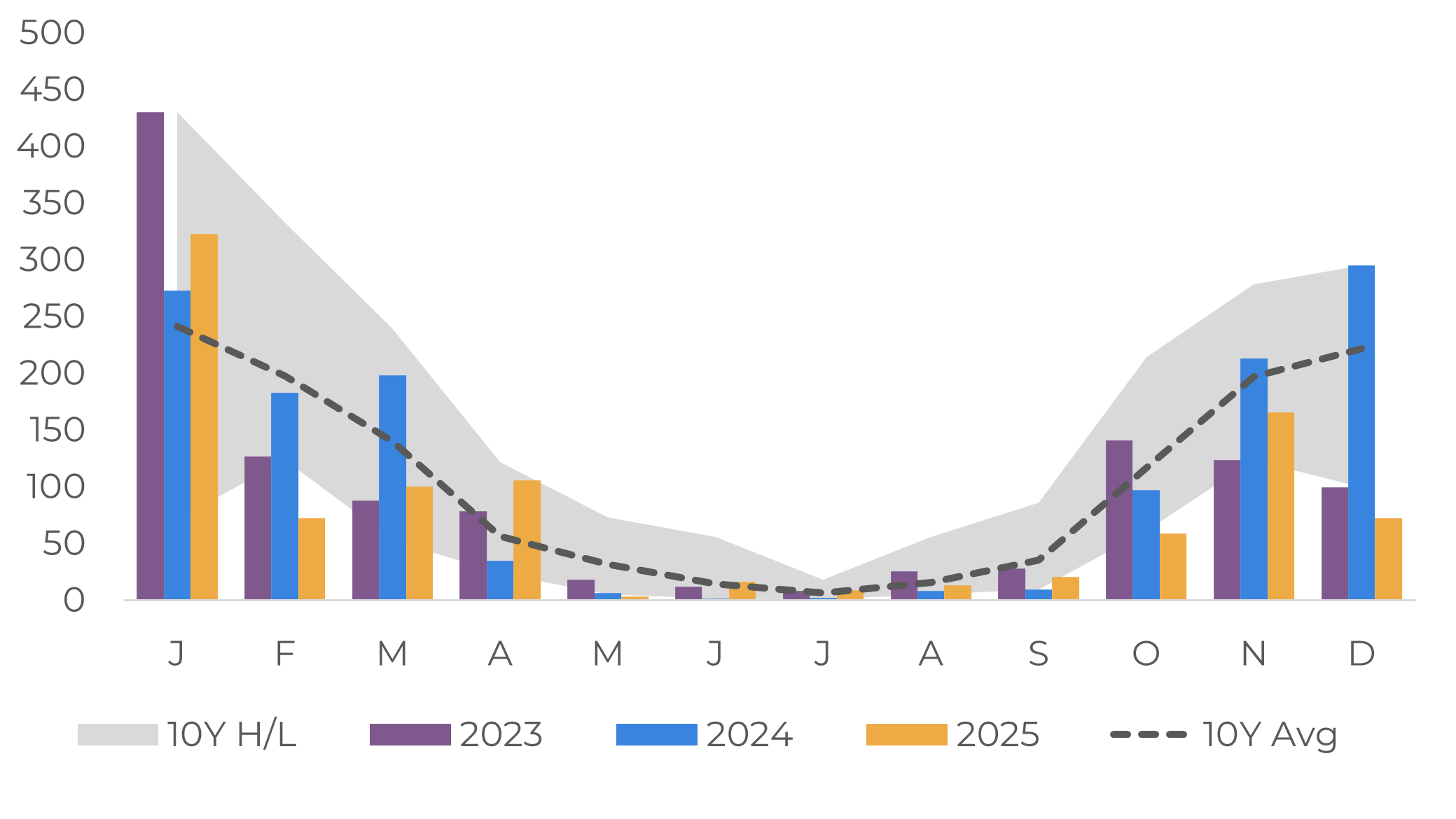

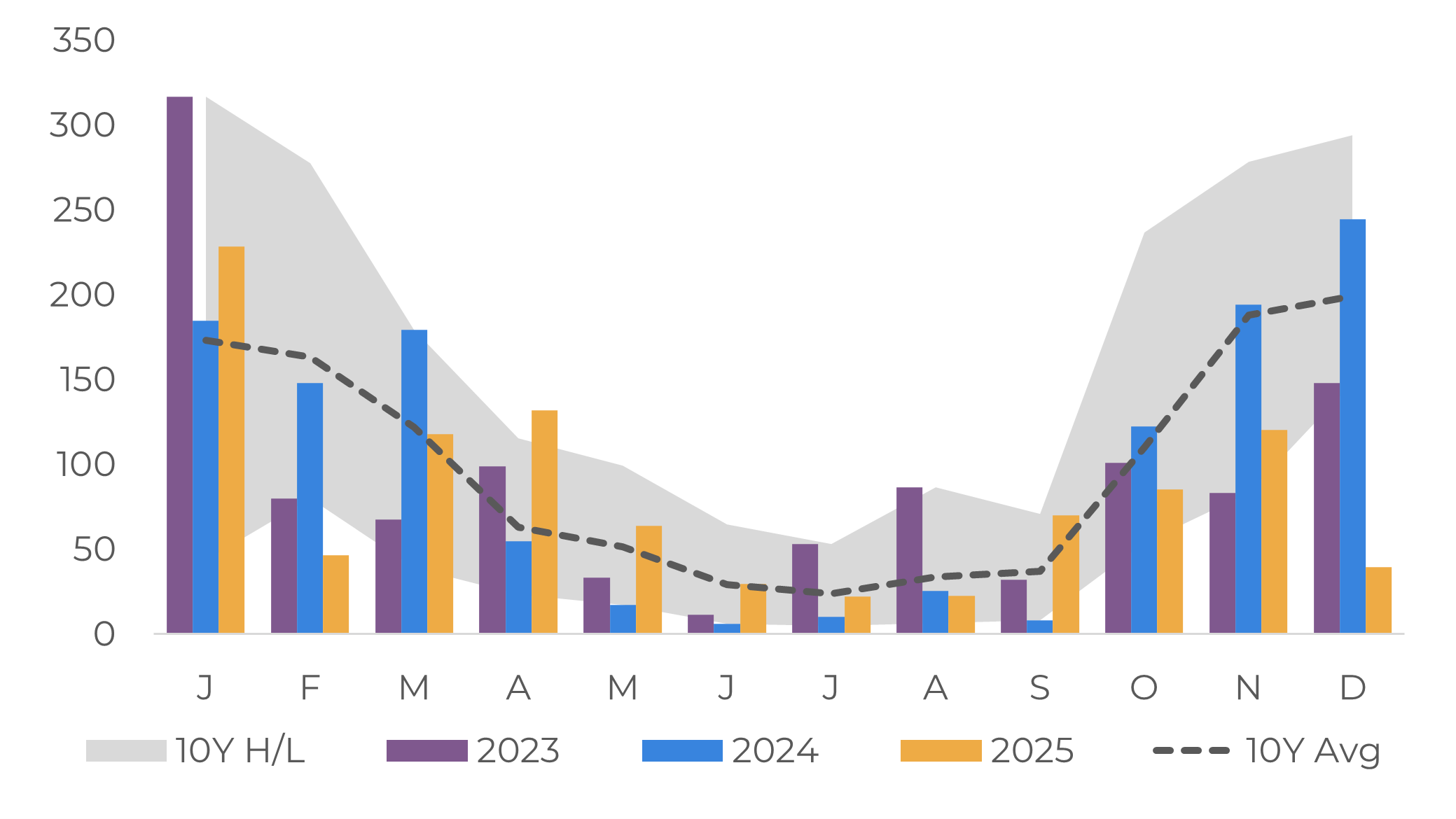

Minas Gerais: Weighted Monthly Precipitation in Coffee Areas (mm)

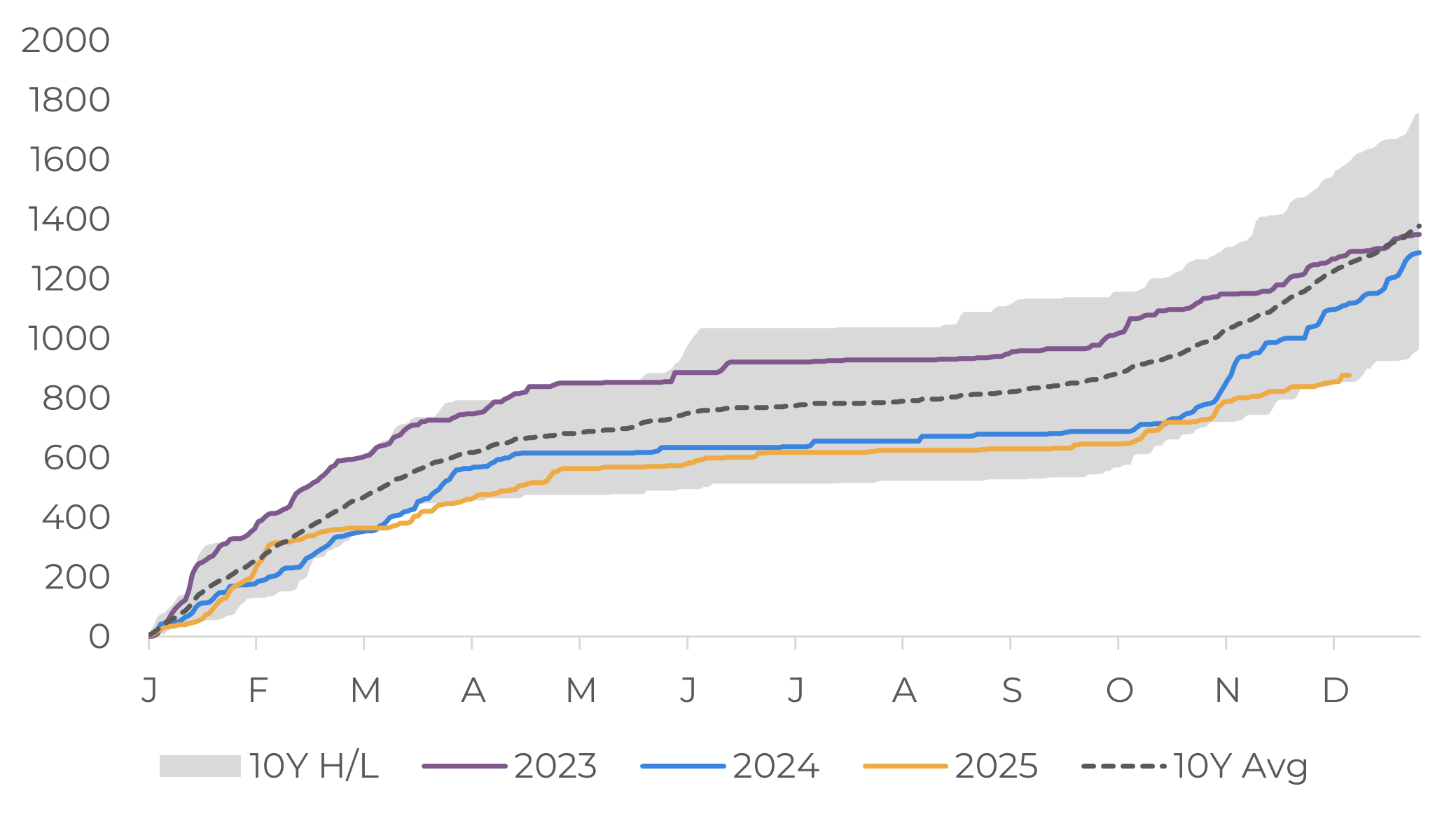

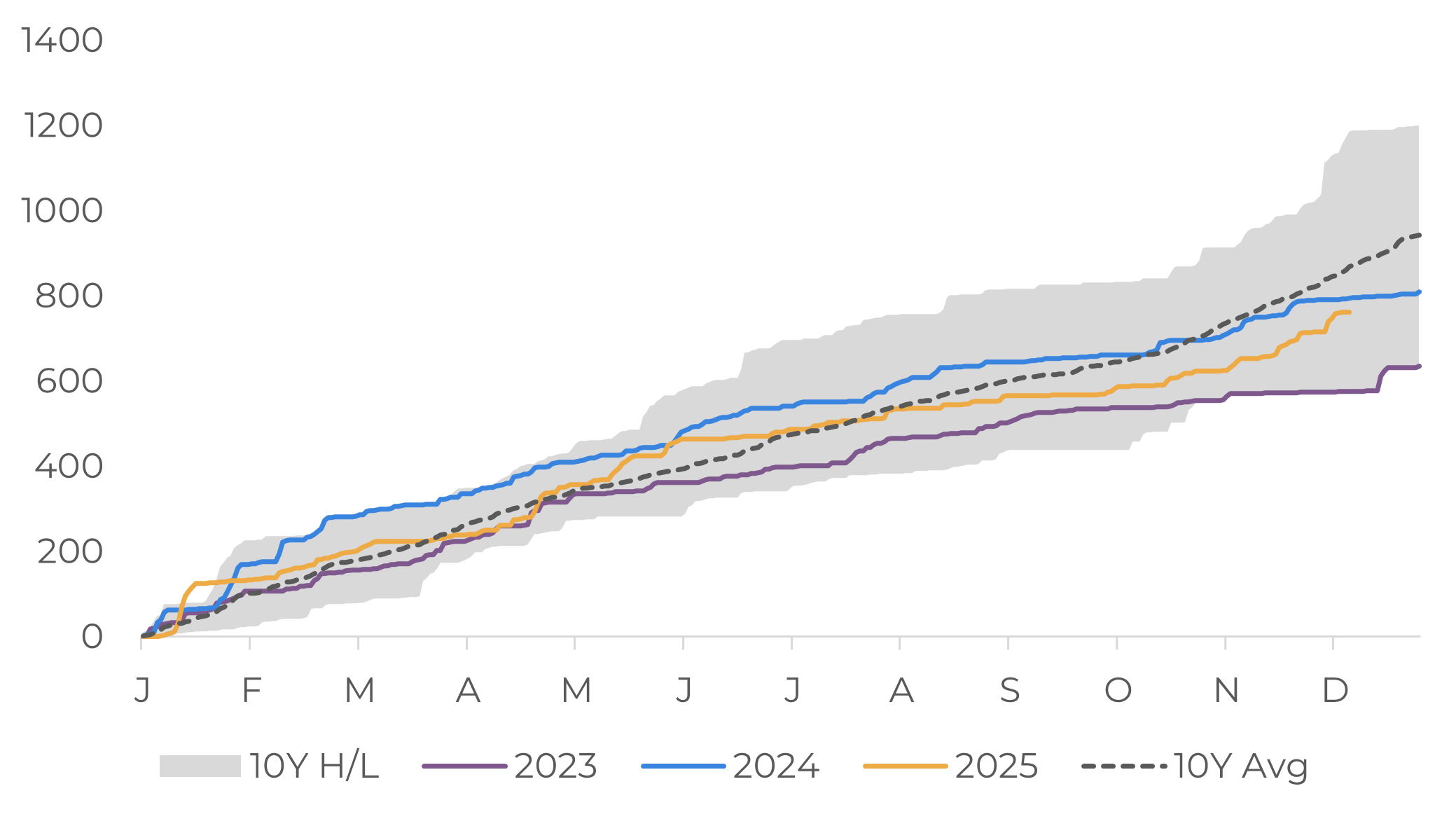

São Paulo: Weighted Cumulative Precipitation in Coffee Areas (mm)

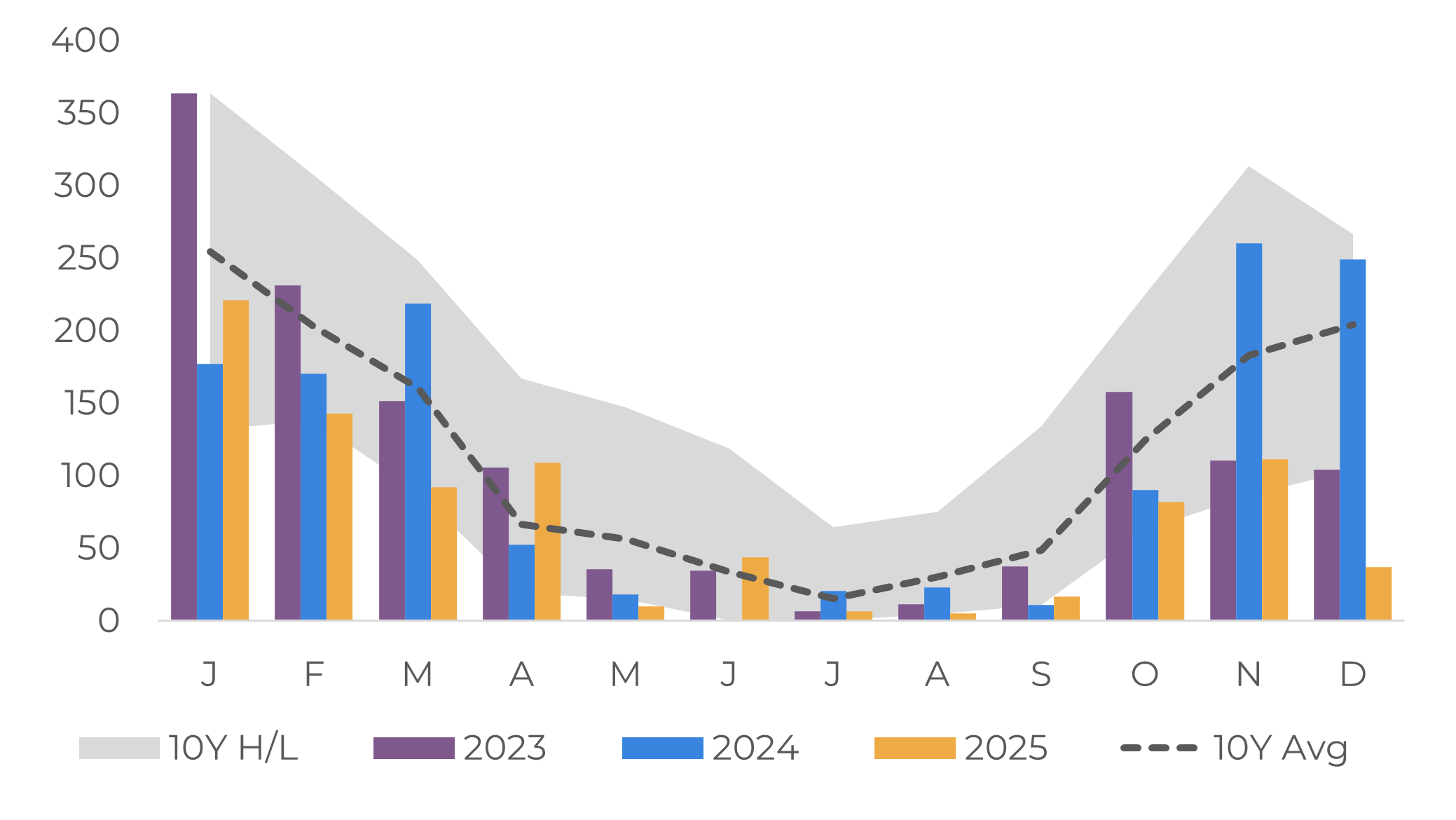

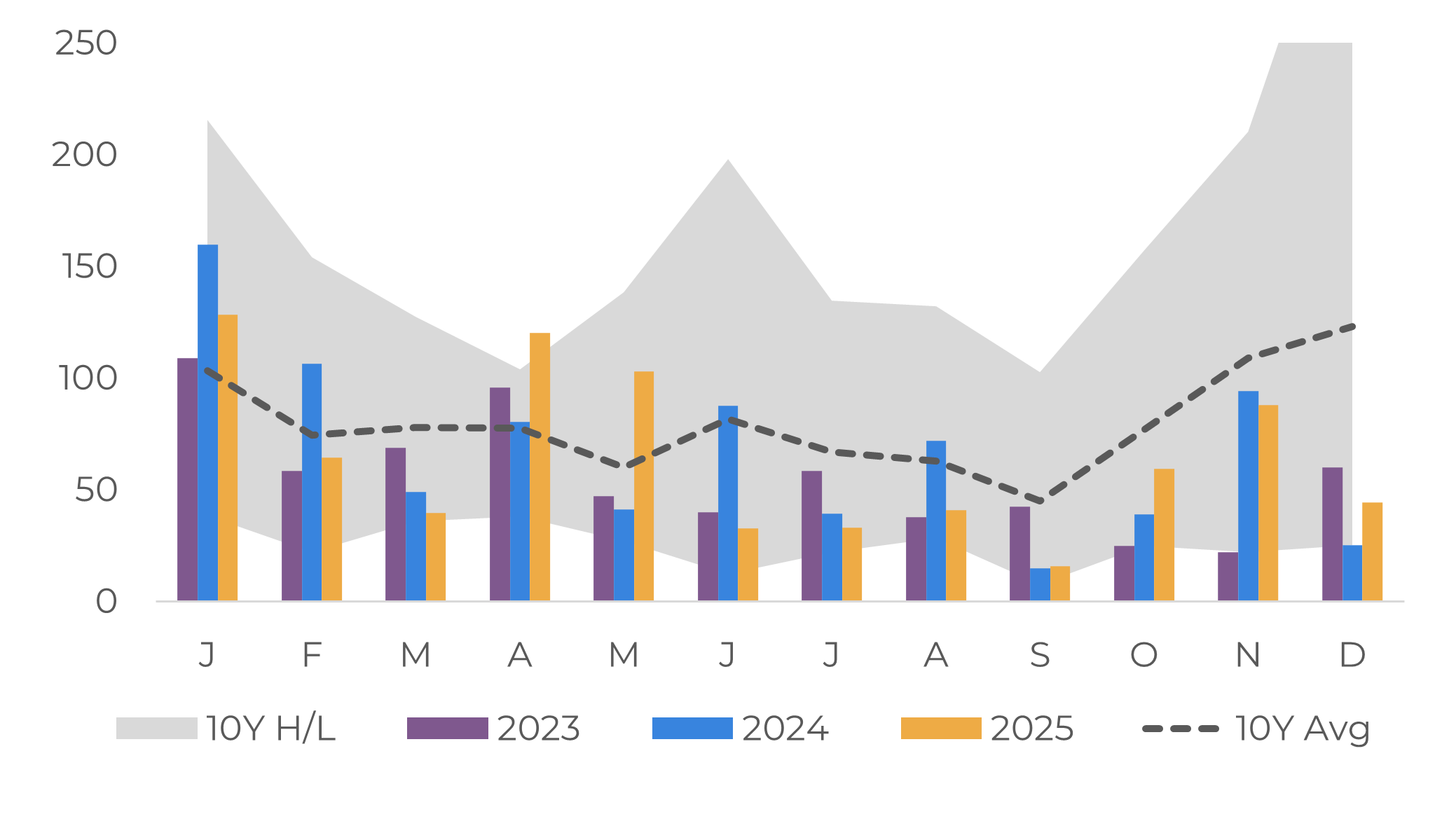

São Paulo: Weighted Monthly Precipitation in Coffee Areas (mm)

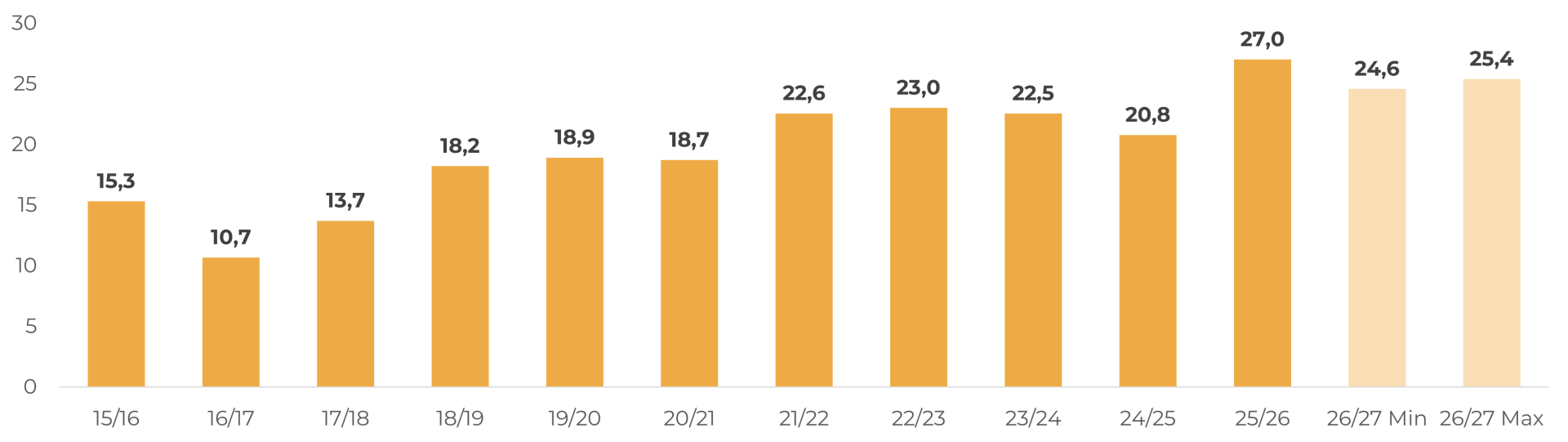

Conilon production will be good, but below 25/26

Espírito Santo: Weighted Cumulative Precipitation in Coffee Areas (mm)

Espírito Santo: Weighted Monthly Precipitation in Coffee Areas (mm)

Bahia: Weighted Cumulative Precipitation in Coffee Areas (mm)

Bahia: Weighted Monthly Precipitation in Coffee Areas (mm)

Brazil’s 26/27 season could contribute to global stock recovery

Hedgepoint: Brazil’s Arabica Production (M bags)

Hedgepoint: Brazil’s Conilon Production (M bags)

Coffee Report

Disclaimer

To access this report, you need to be a subscriber.