Coffee Crop Update Brazilian 26/27 Season

26/27 Brazilian Coffee Crop Update

In this report, you can find the updated figures for the Brazilian 26/27 season. Given the favorable weather in past months and the increase in area and trees husbandry in recent seasons, Brazil’s production figures were revised up. Arabica total volume is expected to reach 50.2 M bags and Conilon, up to 25.6 M bags, with a total production of 75.8 M bags of coffee.

Figures for demand and exports were also updated, while 25/26 season exports figures were revised down, given the current shipments trend. Explore the detailed analysis below.

Abundant rains will increase Arabica yields

Since mid-October, weather has been favorable for the development of the 26/27 season in Arabica coffee regions. Although rainfall remained slightly below average levels in 2025, the volume combined with mild temperatures enabled a good flowering and start of the bean development phase. Trees were also reported to be in great condition due to favorable weather and good husbandry, while production areas have slightly increased from past years . Many renovated and newly planted areas are in their first year of production, while younger trees – in their second or third year of production – are showing strong yields.

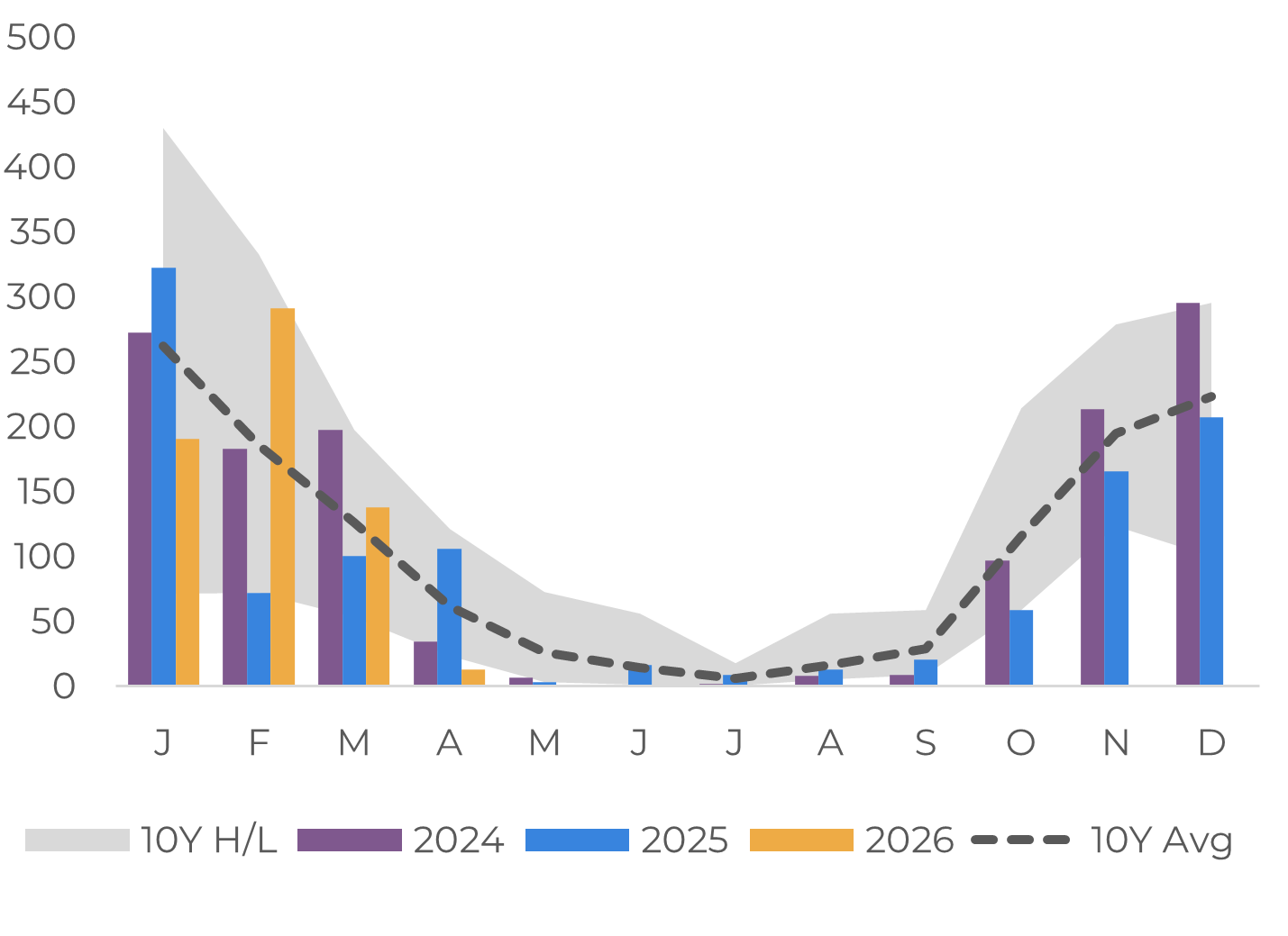

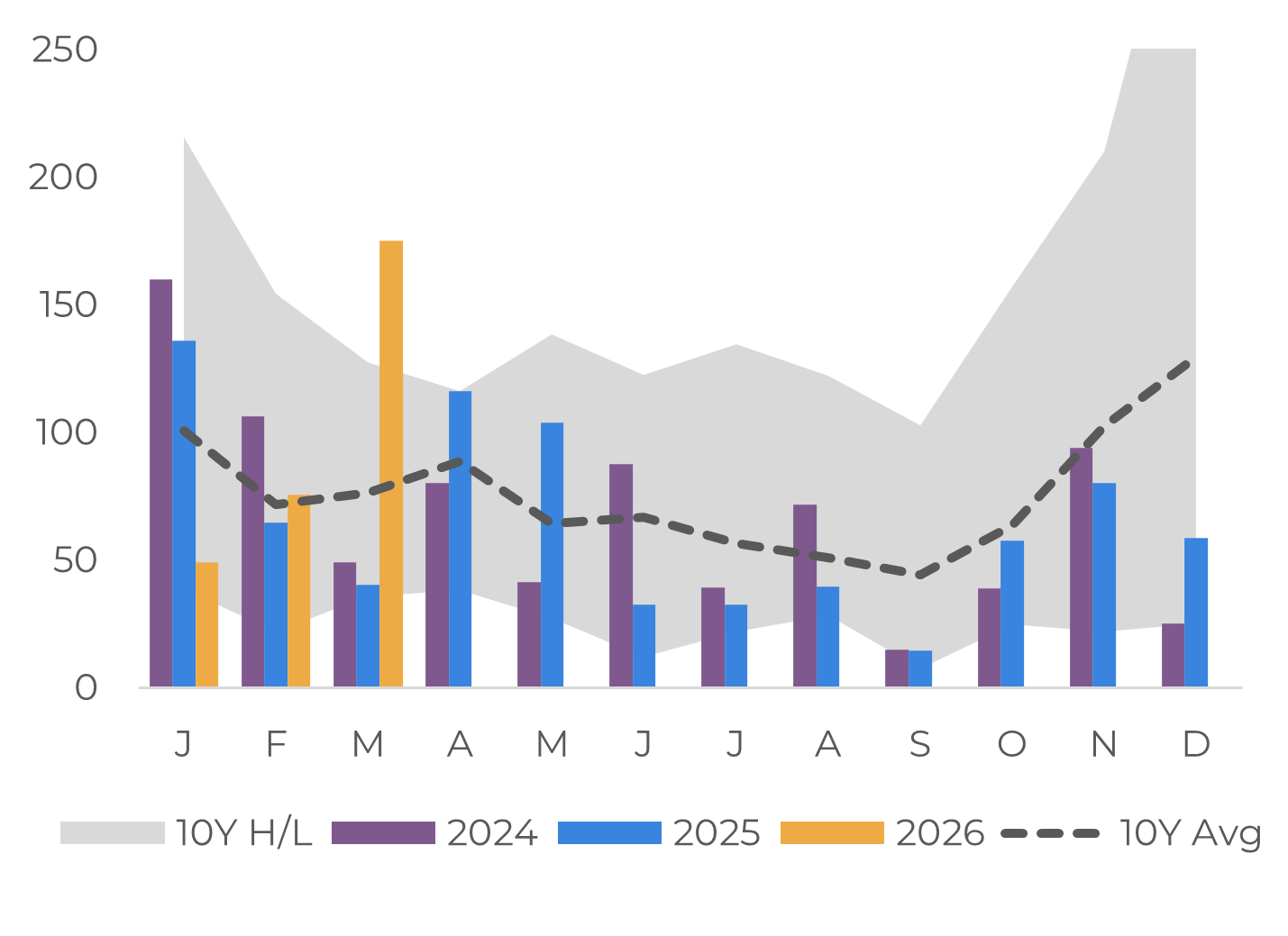

Cumulative Precipitation in Minas Gerais Coffee Regions (mm)

Source: Bloomberg, Somar, Hedgepoint

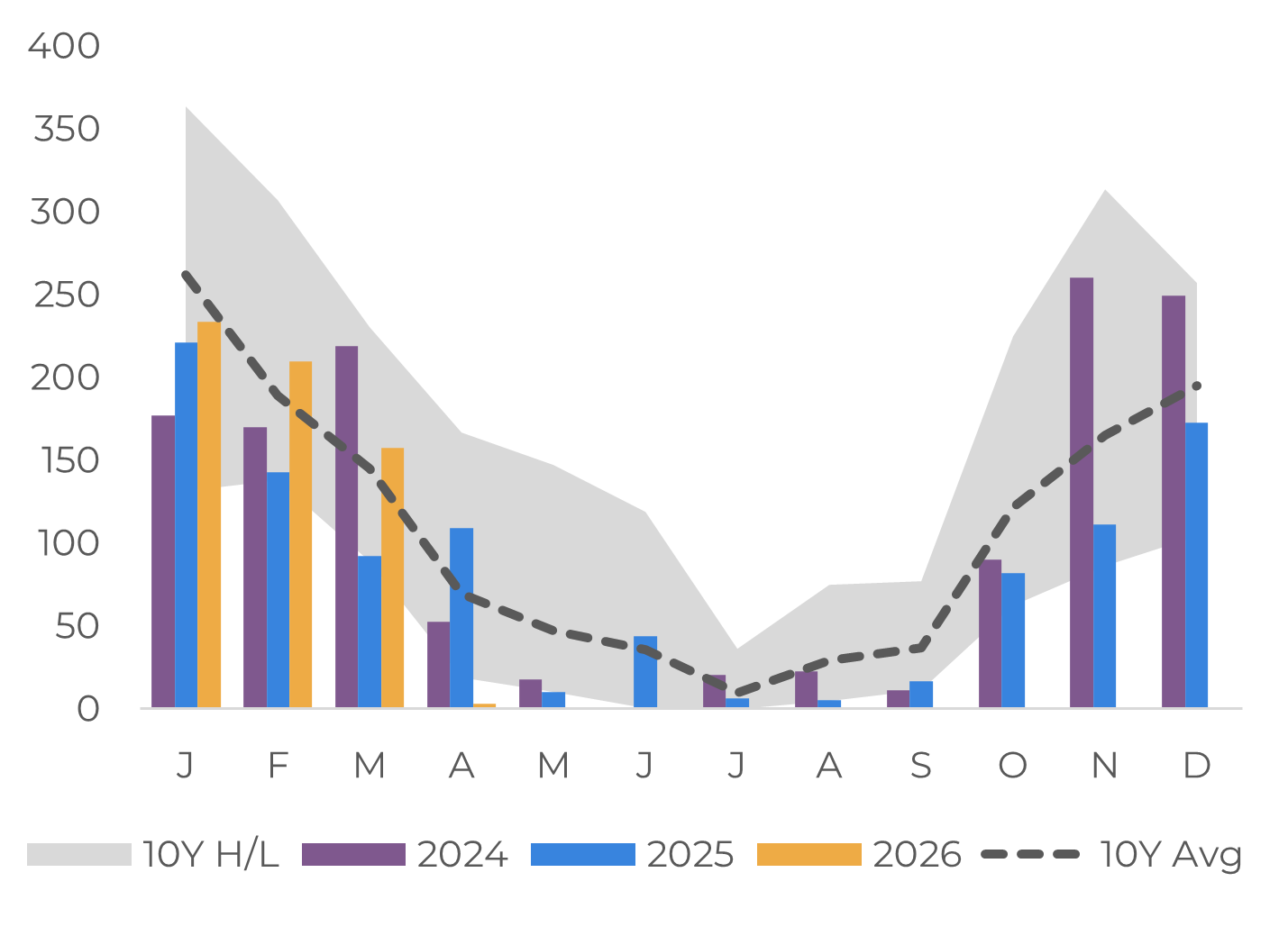

Cumulative Precipitation in São Paulo Coffee Regions (mm)

Source: Bloomberg, Somar, Hedgepoint

In 2026, during the bean-filling phase, rains continued, coming even above average in February and March, allowing the coffee beans to gain weight and screen size, which is expected to translate into higher processing yields. These excellent conditions, combined with an increase in area and higher yield, have led us to revise our figures up, with Arabica output at 50.2 M bags in 26/27, up 33.2% on 25/26. Further revisions are expected after the start of the harvest in May, once yields are thoroughly evaluated.

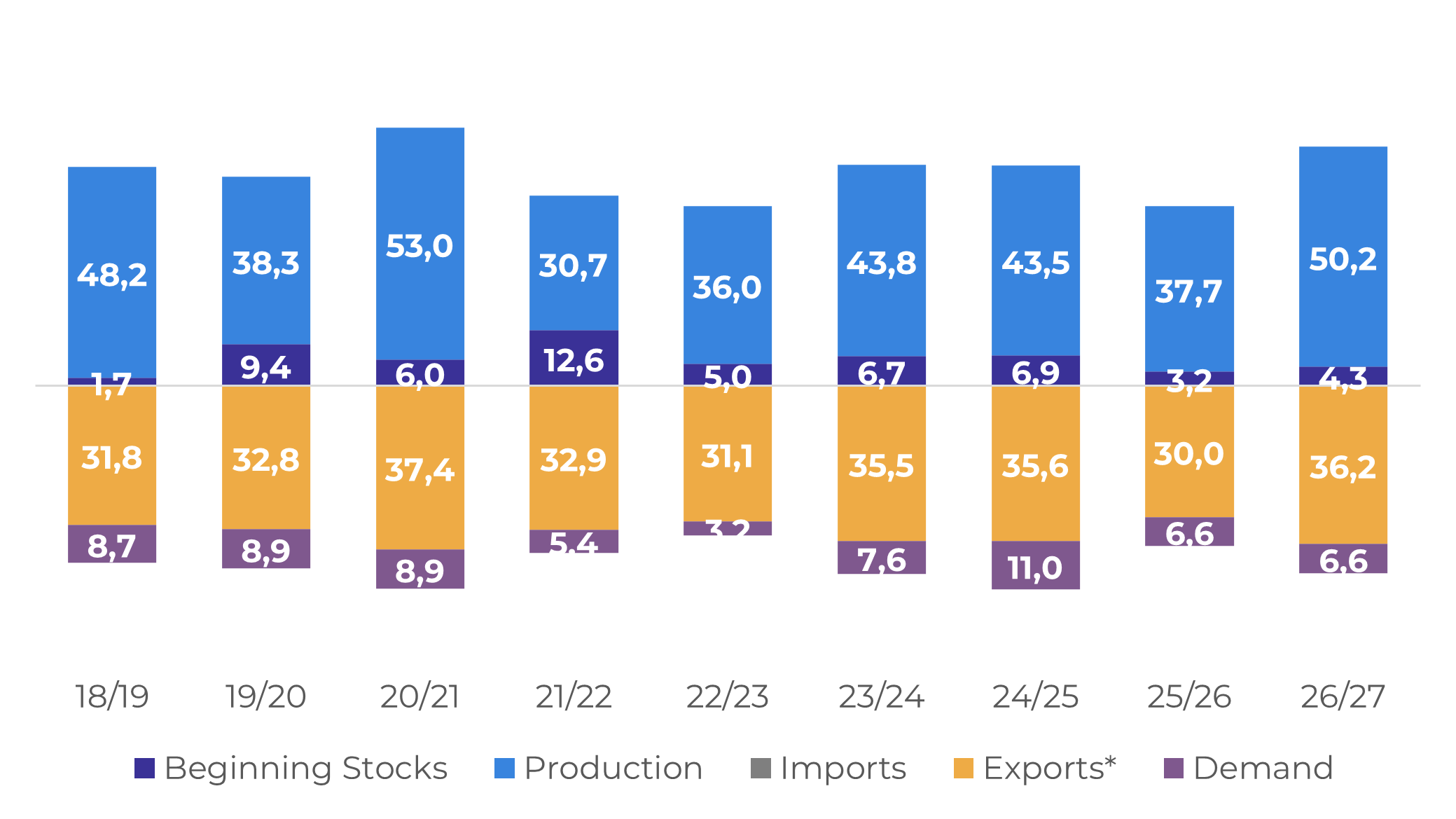

It is interesting to note that the 26/27 season will start with higher initial stocks than 25/26, as exports in the 25/26 cycle continue to underperform, leading us to revise these figures down. Exports in this season were affected not only by decreased farmers’ appetite for sales – choosing to hold larger stocks amid volatile prices and rising uncertainties – but also by the effect of the U.S. tariffs in part of 2025.

Regarding 26/27, the current inverted market and higher financial costs could lead destinations to withhold rebuilding stocks, which could affect coffee global exports figures. However, there is still the expectation of higher Brazilian shipments in the season, as supply will be higher.

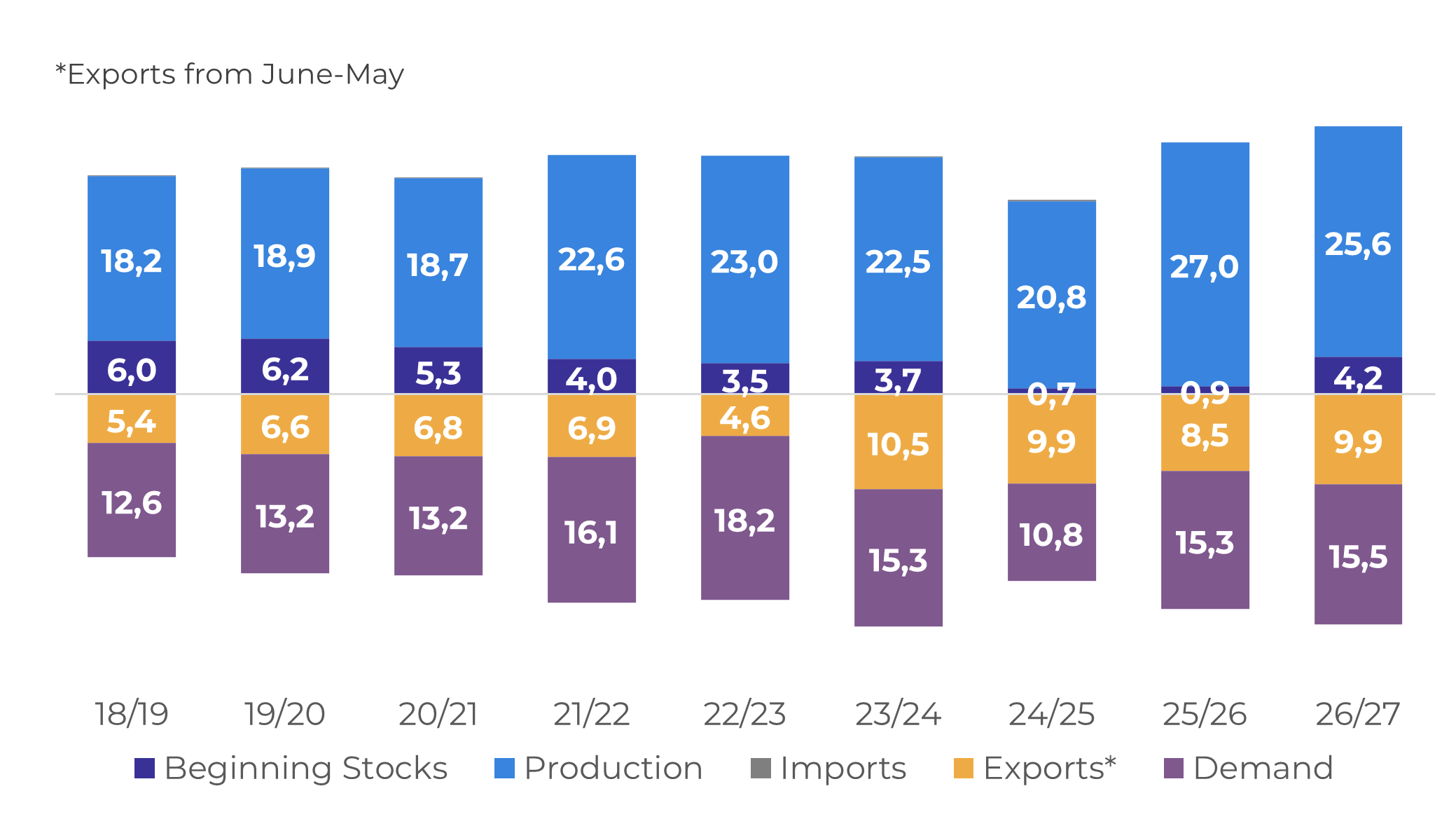

Hedgepoint: Brazil Arabica Supply and Demand (M bags)

Source: Hedgepoint

As for domestic demand, in 25/26 Brazilian roasters started using more Conilon than Arabica in the national blend, as Conilon became a cheaper option. For 26/27 we initially expect that roasters will continue to use more Conilon than Arabica for the domestic market, as the price difference between the two varieties remains relevant. Although a record crop on the Arabica side could reduce the variety prices in the coming months, a good crop of Conilon could keep prices more attractive for Brazilian Roasters, capping Arabica domestic demand.

New areas keep Conilon production high

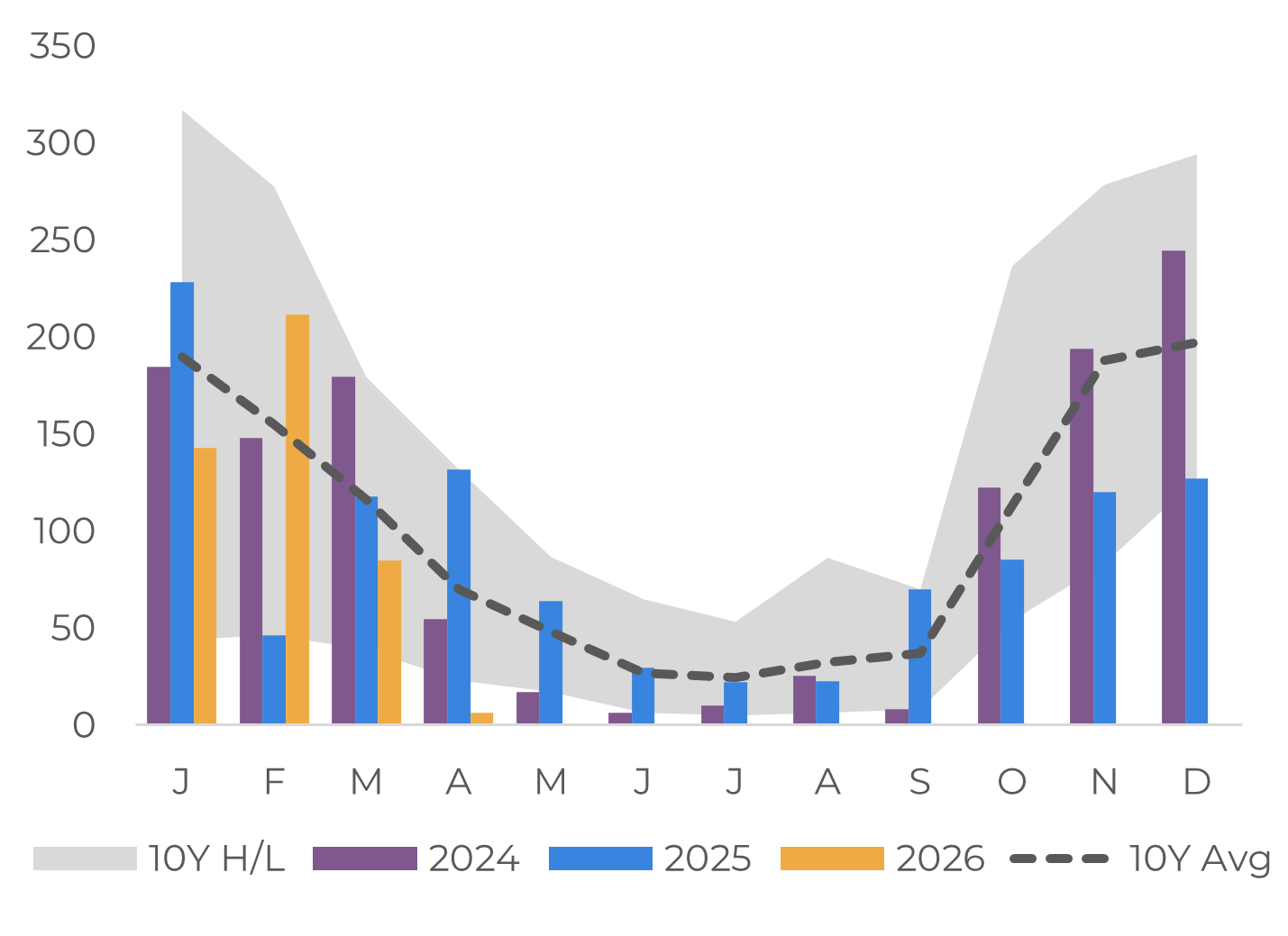

Conilon areas had a similar weather pattern to Arabica’s, with abundant rainfall and mild temperatures throughout the 26/27 season development. Albeit below average until February this year, rain was consistent in major regions, combined with good reservoir levels, allowed for a proper flowering and bean development.

Cumulative Precipitation in Espírito Santo Coffee Regions (mm)

Source: Bloomberg, Somar, Hedgepoint

Cumulative Precipitation in Bahia Coffee Regions (mm)

Source: Bloomberg, Somar, Hedgepoint

Brazilian farmers also continue to be highly capitalized and investing in tree husbandry and renovation areas. All these characteristics together allow Brazil to have one of the highest yields in the world. Consequently, the drop in production in 26/27 is expected to be only of 5.3%, with total Conilon volume at 25.6 M bags, the second largest figure for the country. The harvest has already started in some areas, but it is still at its early stage, with the pace likely increasing at the end of April and early May. Another crop review will be made after the bulk of the harvest to assess yields.

The season is also set to start with higher carryover stocks as – even more than the Arabica –, farmers have been selling less coffee compared to previous seasons. As Conilon prices reached extremely high levels in 2024 and 2025, most coffee producers are capitalized and in no rush for money. Although sales may increase in the next week, as harvest gains pace and open space for the new beans. However, there are reports of big warehouses operating with higher stock capacity than in previous years, highlighting the higher availability for the period.

Given this context and current shipment pace, export figures for the 25/26 season were also revised down. For 26/27, it is possible that exports will gain pace as supply will be plentiful and Robusta demand worldwide could remain higher, given continued lower prices than Arabica.

Normal heading 4

Soruce: Hedgepoint

Robusta prices could remain subdued in the next months as not only Brazil increased its supply in 25/26 and 26/27, but other key countries such as Vietnam and Uganda are also expected to have an increase in input, given the higher prices in past years. However, this scenario depends on weather developments next months, especially in a possible El Niño scenario, as, aside from Indonesia, other Robusta producers are only just entering the development period for the 26/27 season.

Finaly, Brazilian exports will also be dependent on domestic demand. In the past months, farmers prioritized selling coffee to domestic roasters over exporting due to more competitive prices from industry. For 26/27, domestic demand is still expected to rely more heavily on Conilon beans, but changes in lower quality Arabica beans availability and prices could lead to changes in the domestic mix.

Coffee Report

Reviewed by Livea Coda

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.