Sugar | Crop Update: Brazilian Center-South - 2026 04 10

More cane ahead, but El Niño still gives the bulls some hope

- Brazilian Center-South supply remains strong, with 2025/26 sugar production expected above 40 Mt and 2026/27 cane projected near 635 Mt under normal weather conditions.

- Global trade flows are oversupplied due to Brazil’s high output and recoveries in India, Thailand, and Mexico, keeping sugar prices structurally bearish.

- Recent price strength to ~16.1 c/lb faded as geopolitical risk premium eased and the energy complex retreated, underscoring limited macro support.

- Ethanol has regained parity versus sugar during 2025 last three months, encouraging mix reductions; market equilibrium would require a sugar mix near 44.5%, though physical constraints cap adjustments and maintain it closer to 48%.

- The effective sugar price floor is estimated around 13.5 c/lb (BRL 2.2/liter ex-mill hydrous), with the strongest upside risks concentrated in 2027 via the possible El Niño–related weather impacts in the Northern Hemisphere 2026/27 crop developments.

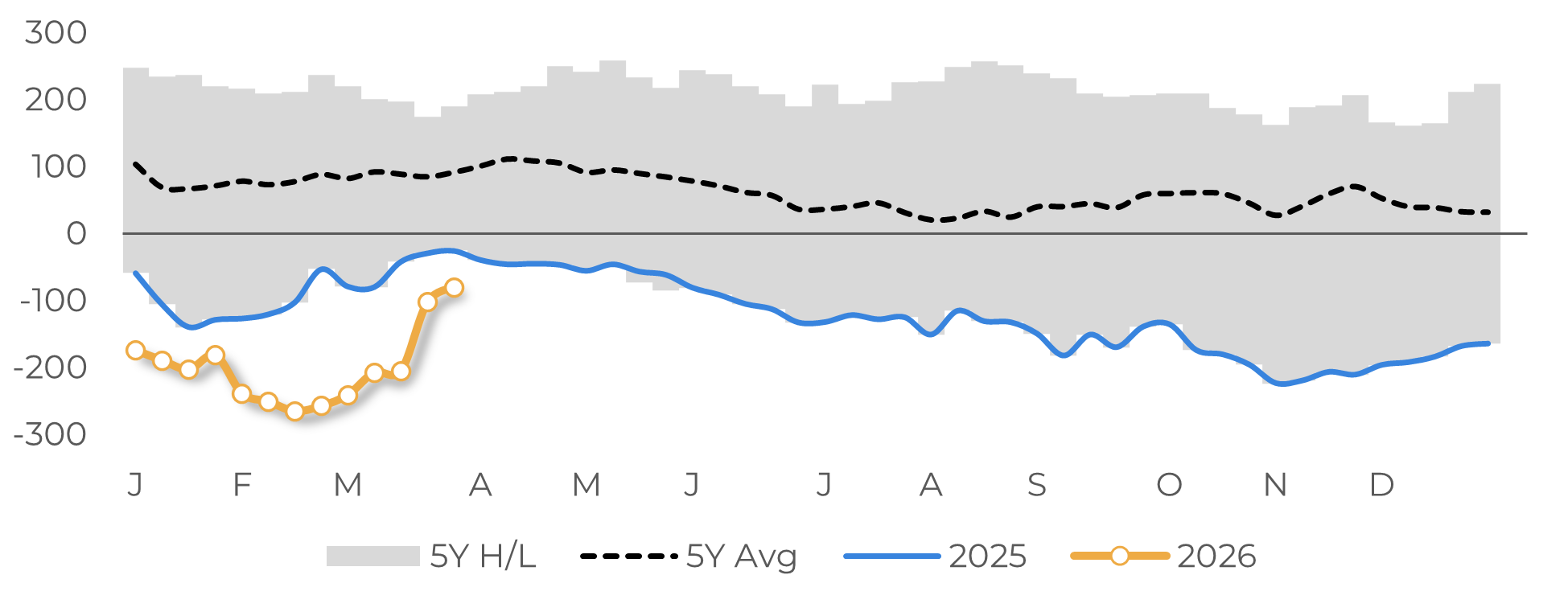

Technical factors played a significant role in the recent price rise, as speculators reduced their short positions, pushing them closer to minimum levels observed in the recent past. However, they have no reason to, in the short term, keep up the buying momentum as market fundamentals remain strictly bearish. Nonetheless, some degree of volatility may still emerge from specs should tensions between the United States and Iran re-escalate.

Figure 1 – Speculative Net Positioning (‘000 lots)

Source: CFTC, Hedgepoint

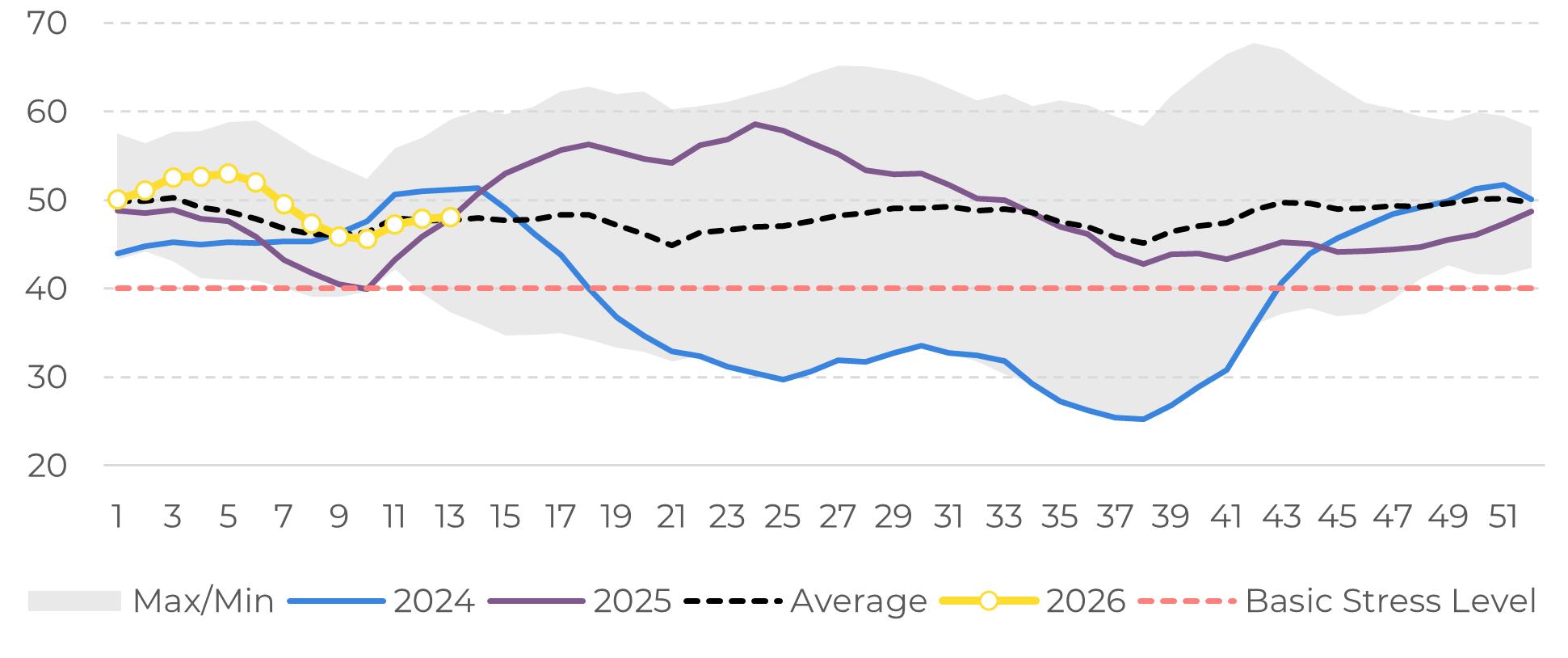

Despite some recovery in Northern Hemisphere production, Brazil - particularly the Center-South region - remains the primary driver of the bearish trend in the sugar market. The 2025/26 season is set to deliver another robust result, with sugarcane crushing exceeding 600 million tons and sugar production surpassing 40 million tons in Center-South, supported by a high sugar mix. Exports may, therefore, exceed 31 million tons, reinforcing Brazil’s role in global supply. Looking ahead to 2026/27, weather conditions have improved, with favorable rainfall recorded between October 2025 and February 2026. These conditions have resulted in a stronger Vegetation Health Index (VHI), which remains close to or above historical averages, allowing for the expectation of a solid yield performance, currently estimated at 78.5 t/ha. As a result, assuming normal weather patterns persist, sugarcane production in the Center-South is projected to reach approximately 635 million tons in the 2026/27 season. Sugar mix remains the hot topic, though.

Figure 2 – Weekly Vegetation Health Index – Center-South

Source: NOAA

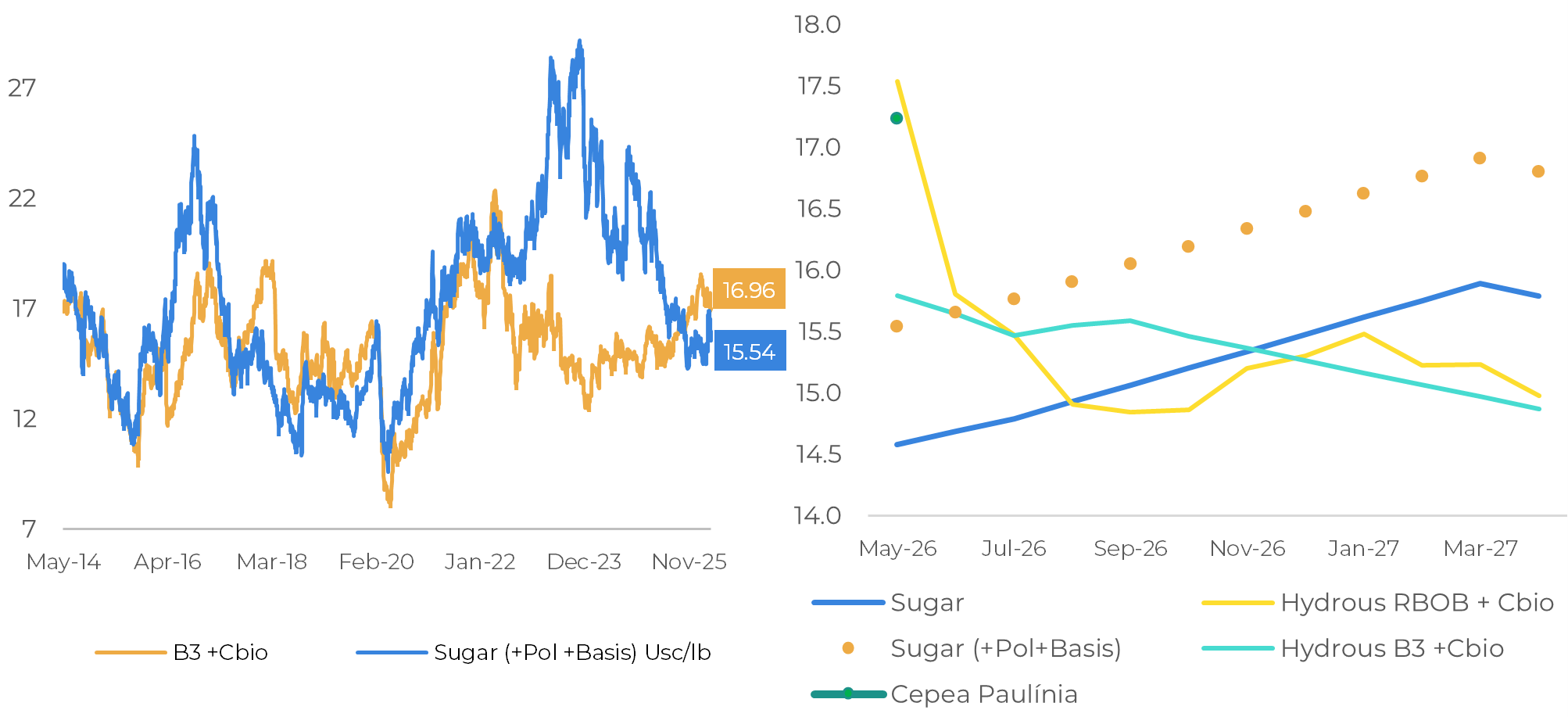

Figure 4 – Historical sugar and ethanol parity (left) and current future parity (right)

Source: Bloomberg, Hedgepoint

- Previously sold or contracted sugar volumes should prevent a complete shift of the mix toward ethanol, as many mills are resistant to repositioning themselves.

- Changes in fuel demand and adjustment mechanism are not immediate and may also limit the decline in the mix.

Therefore, we remain conservative with a 48% sugar mix for 2026/27, guaranteeing a 40.5 Mt sugar production and another robust contribution to the trade flows – also pushing prices towards the estimated floor.

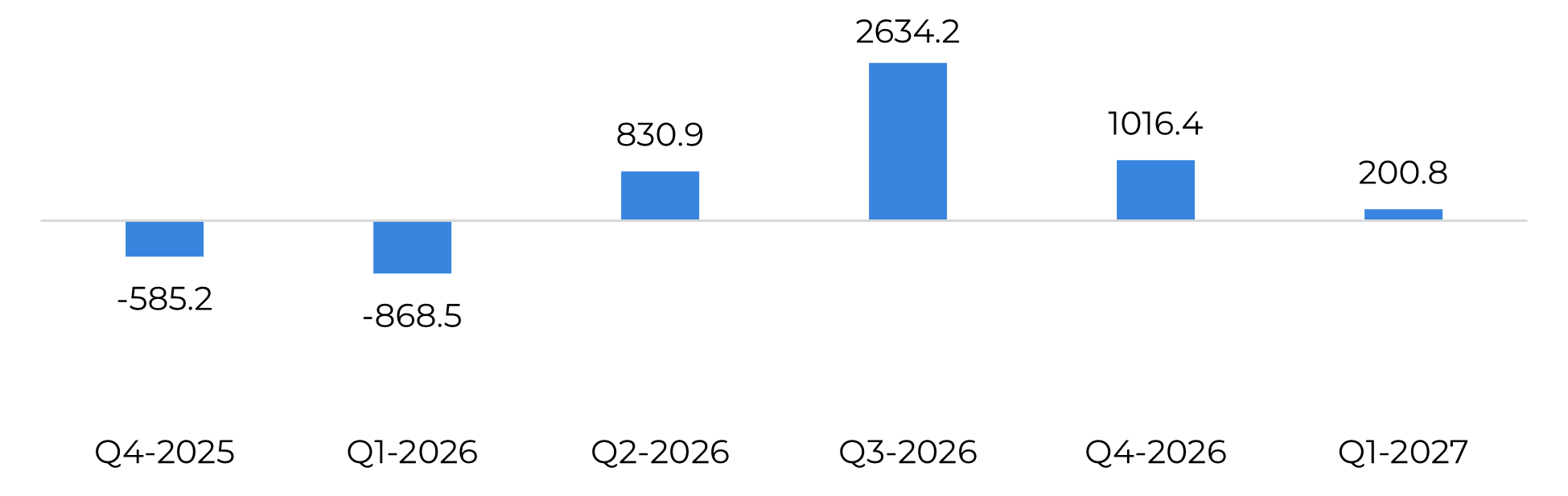

Figure 5 – Total sugar trade flows (‘000t tq) – 48% sugar mix generates a 3.2+ surplus

Source: Greenpool, Hedgepoint

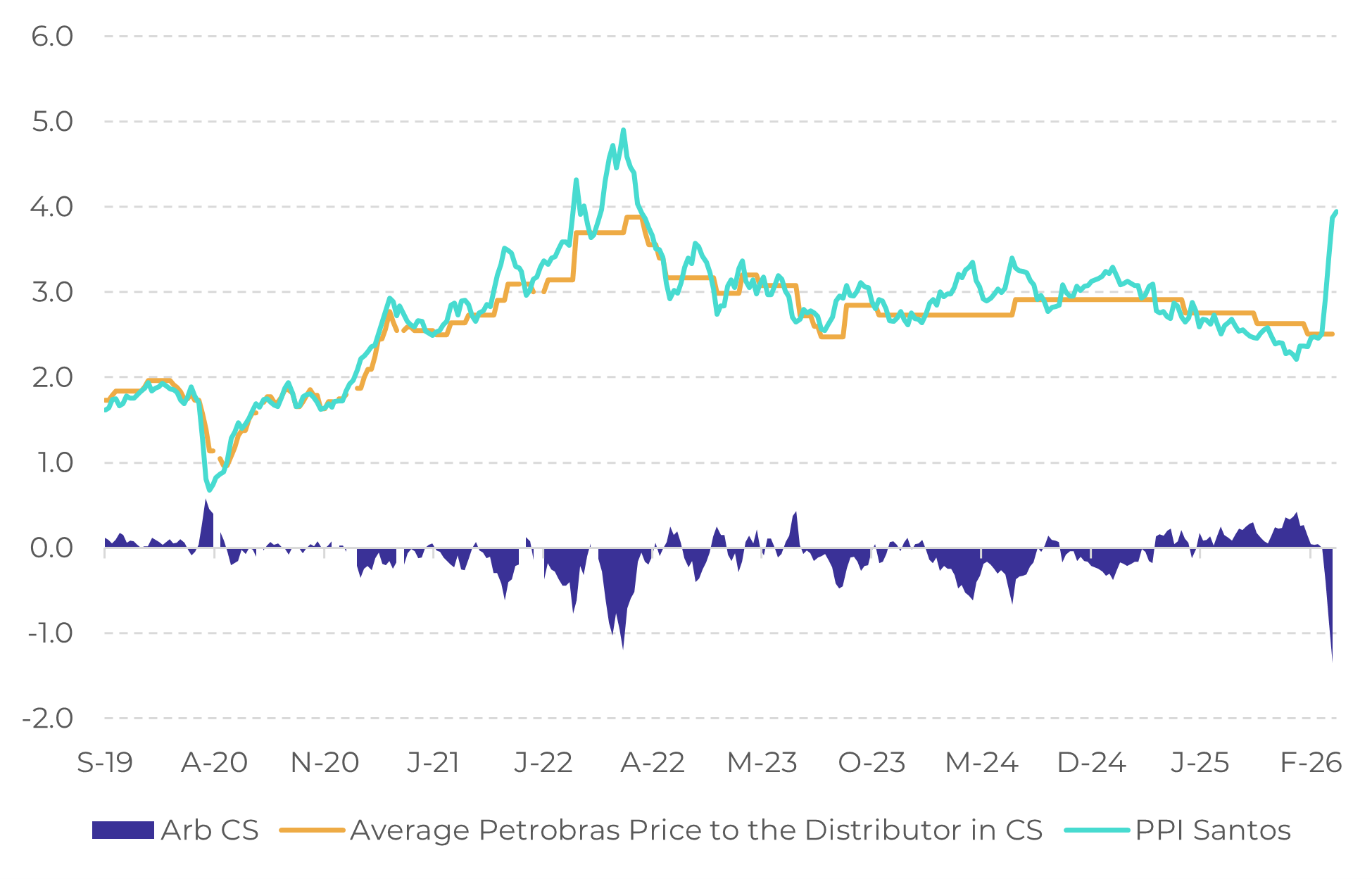

Image 6: Petrobras' average import arbitrage in the Central-South region (BRL/liter)

Source: ANP, Bloomberg, Hedgepoint

For bullish participants, there are some upside risks worth monitoring, although the most relevant one is set to affect the 2027 contracts more. The first, although less likely, involves a renewed escalation of tensions between the United States and Iran that could lead to a pass-through of higher gasoline import costs by Petrobras. Given that Brazil is currently in an election year, we believe to be unlikely that the government would allow a meaningful increase in domestic fuel prices. Should this occur, however, a full pass through of the estimated gasoline import arbitrage of around BRL 1.7 per liter would imply a shift in the estimated price floor from approximately 13.5 cents per pound to around 16.7 cents per pound, a level very close to current hydrous parity based on CEPEA prices. Even so, this scenario would not alter market fundamentals and remains highly dependent on political decisions rather than structural supply-demand dynamics.

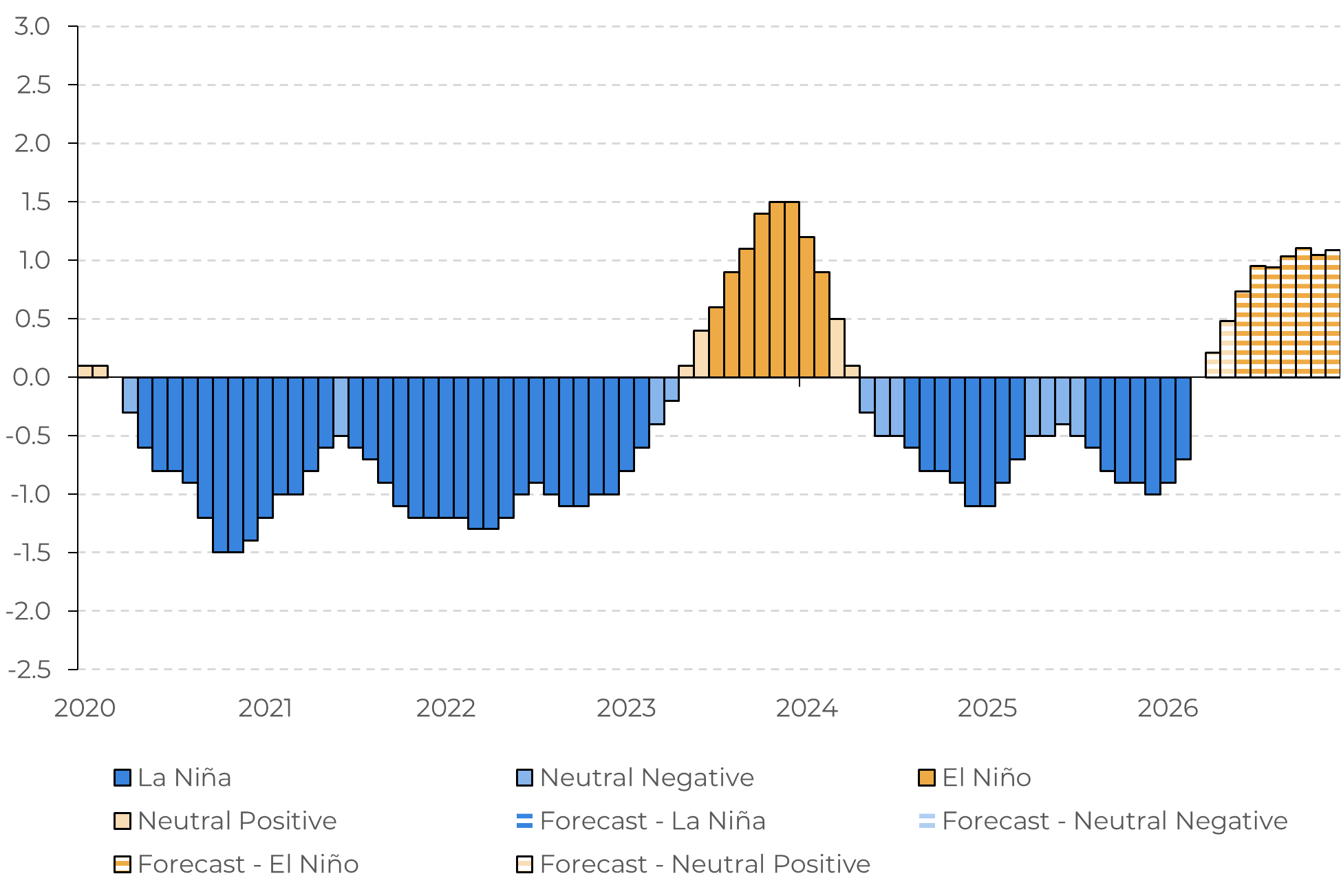

The second potential bullish driver, and more important one, is related to weather. Probabilities and expected intensity of El Niño have already been revised up for the May–June–July period. This increases the likelihood of a wetter winter in Southern Brazil, which could disrupt or slow the pace of the 2026/27 harvest in some states. Nevertheless, the more significant impact of an El Niño event would be felt in the Northern Hemisphere during the 2026/27 crop cycle development. Typically, El Niño conditions are associated with drier and warmer weather across Southeast Asia, southern North America and Central America, posing risks to production in key sugar exporting countries such as India, Thailand, Mexico and Guatemala. Therefore, this scenario could result in reduced sugar availability from the region in the following season and, as a consequence, contribute to firmer prices during 2027.

Image 7: Forecasted Sea Surface Temperature Anomalies (in ºC) in the Nino 3.4 Region

Source: International Research Institute for Climate and Society (IRI)

Crop Update - Sugar

livea.coda@hedgepointglobal.com

gustavo.costa@hedgepointglobal.com