Oct 10

/

Victor Arduin

Energy Weekly Report - 2023 10 06

Back to main blog page

"The energy market is heading towards a week-on-week loss, prompted by an increase in gasoline stocks, sparking concerns about lower demand in the last quarter of 2023."

The energy complex faces losses this week, but fundamentals remain strong

- Oil stocks are at their lowest level since December 2022, suggesting that it is too early to be pessimistic about the energy complex.

- The diesel market is more likely to experience scarcity than lower demand in the coming months, based on historically low stocks in Europe and the United States.

- Although high interest rates are a force that could harm the world's energy demand, their effects are not likely to be felt in the last quarter of the year.

Introduction

The energy market is heading towards a week-on-week loss, prompted by an increase in gasoline stocks, sparking concerns about lower demand in the last quarter of 2023.

Even the announcements by Saudi Arabia and Russia, confirming that the current voluntary supply cuts of 1.3 million barrels per day (bpd), werent not sufficient to drive prices higher. Nevertheless, energy stocks remain very low indicating the prices may go up again soon.

Despite signaling that prices of gasoline may drop in the coming weeks, easing inflation in the country, it also be a sign of economic weakness with U.S. government data showing the four-week average of gasoline demand at the lowest seasonal level in 26 years.

Even the announcements by Saudi Arabia and Russia, confirming that the current voluntary supply cuts of 1.3 million barrels per day (bpd), werent not sufficient to drive prices higher. Nevertheless, energy stocks remain very low indicating the prices may go up again soon.

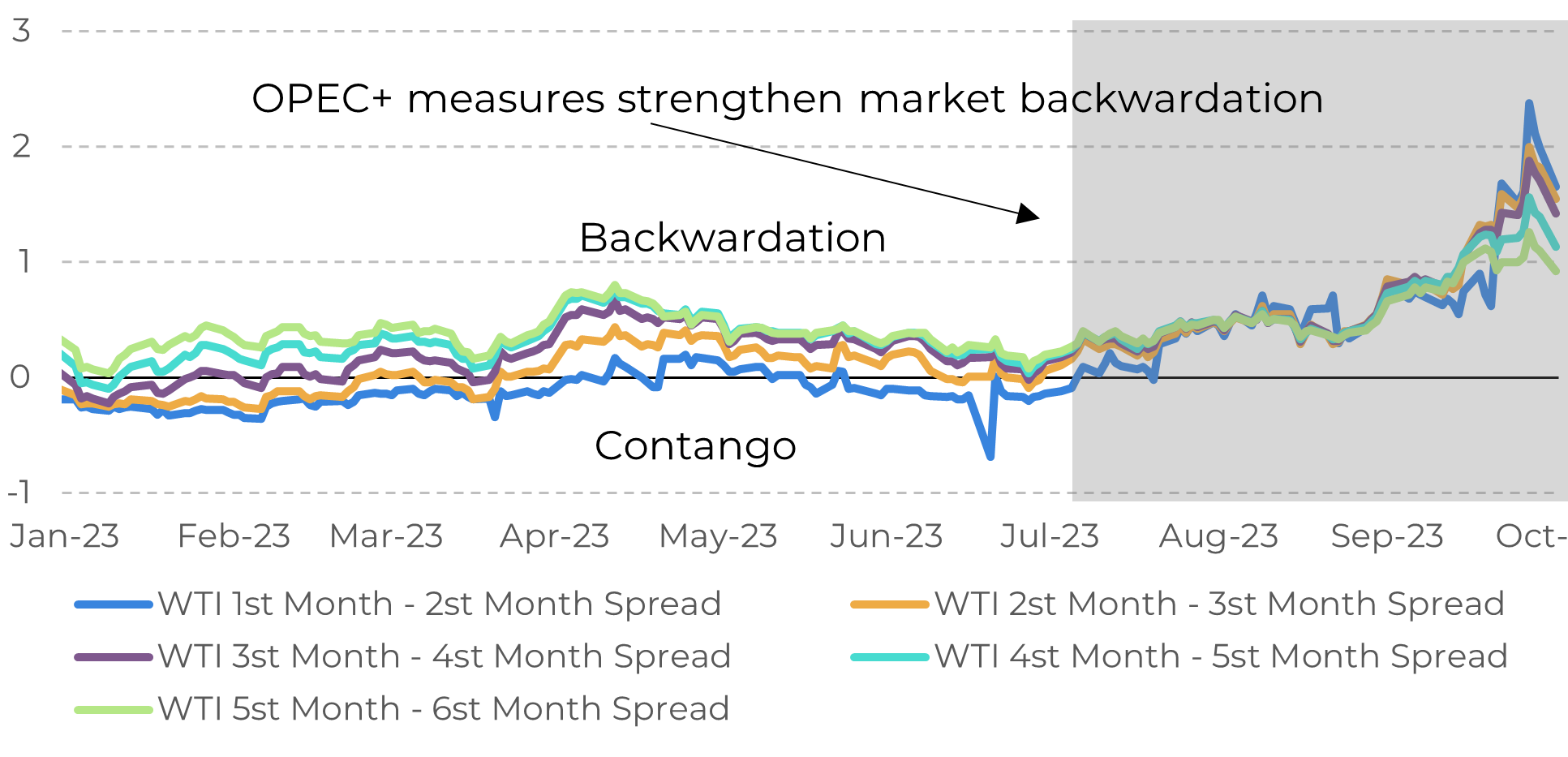

Image 1: Higher Premium for Nearer WTI Contracts (USD Spread)

Source: Refinitiv

Image 2: U.S. Weekly Gasoline Demand (M bpd)

Source: EIA

More scarcity than lower demand is more likely in the diesel market

In

recent days, the energy commodities markets have displayed a bearish reaction,

primarily driven by a significant increase in gasoline stocks, surpassing

expectations due to weakened demand. However, it's crucial to note that oil

stocks are currently at their lowest levels since December 2022, indicating

that it might be premature to adopt a pessimistic outlook for the energy

complex.

Looking ahead, the diesel market is more likely to face scarcity rather than reduced demand in the upcoming months. This prediction is based on historically low stock levels in Europe and the United States for this time of the year. The latest report from the Energy Information Agency reveals a 1.3 million barrel decrease in US stocks, approximately 13% below the 5-year average.

Looking ahead, the diesel market is more likely to face scarcity rather than reduced demand in the upcoming months. This prediction is based on historically low stock levels in Europe and the United States for this time of the year. The latest report from the Energy Information Agency reveals a 1.3 million barrel decrease in US stocks, approximately 13% below the 5-year average.

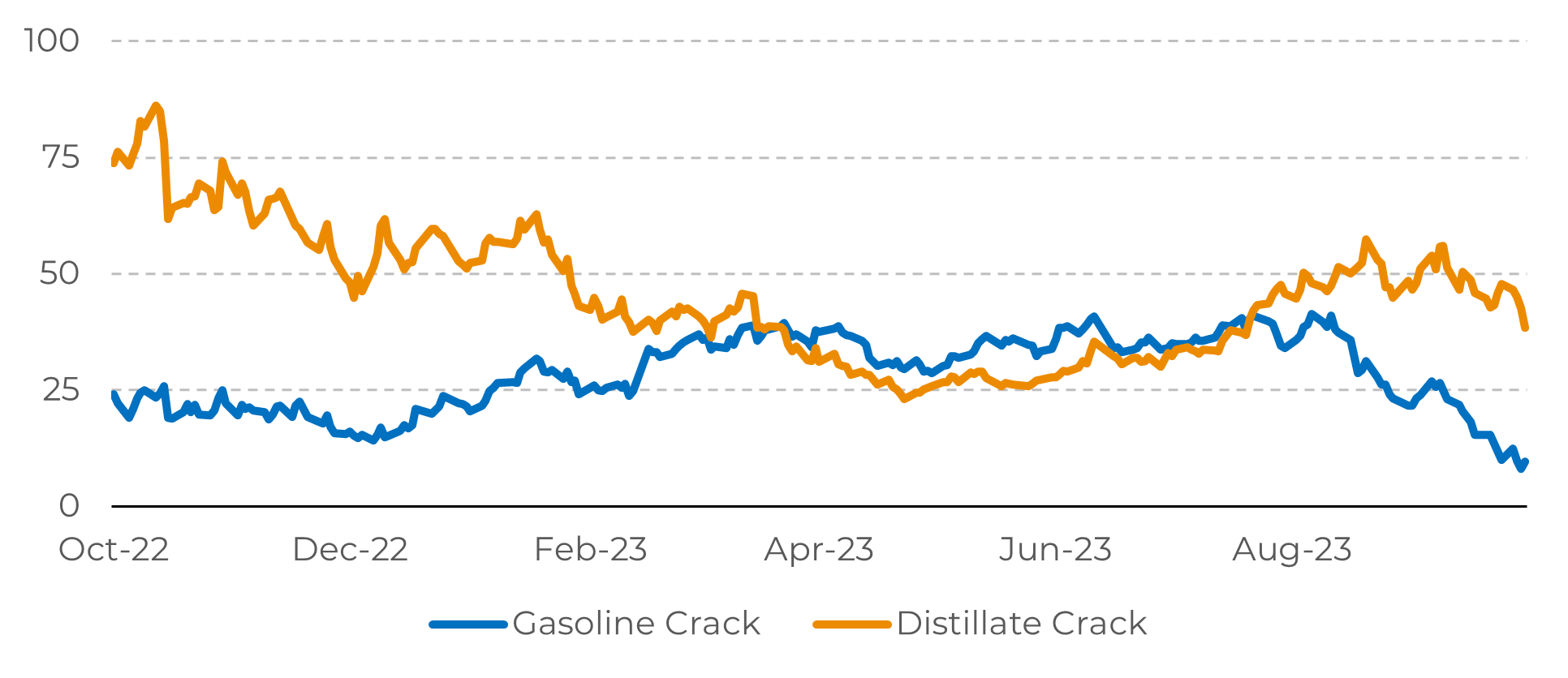

Image 3: Refinery Profit Margin (Barrel USD)

Source: Refinitiv

The rising U.S. production has enabled the country. to become a net exporter. Mexico stands out as one of the most significant consumers of U.S. natural gas, driven by its strategic advantage of readily accessible pipeline infrastructure. This has resulted in a rapid upswing in exports to the southern neighbor.

According to data from Wood Mackenzie, Mexico's electric power sector has experienced a steady annual growth rate of 3% in recent years. While Mexico successfully bolstered its domestic production in 2022, reducing its dependence on American LNG exports, but this year's demand surge has boosted imports from the U.S. to bridge the supply gap.

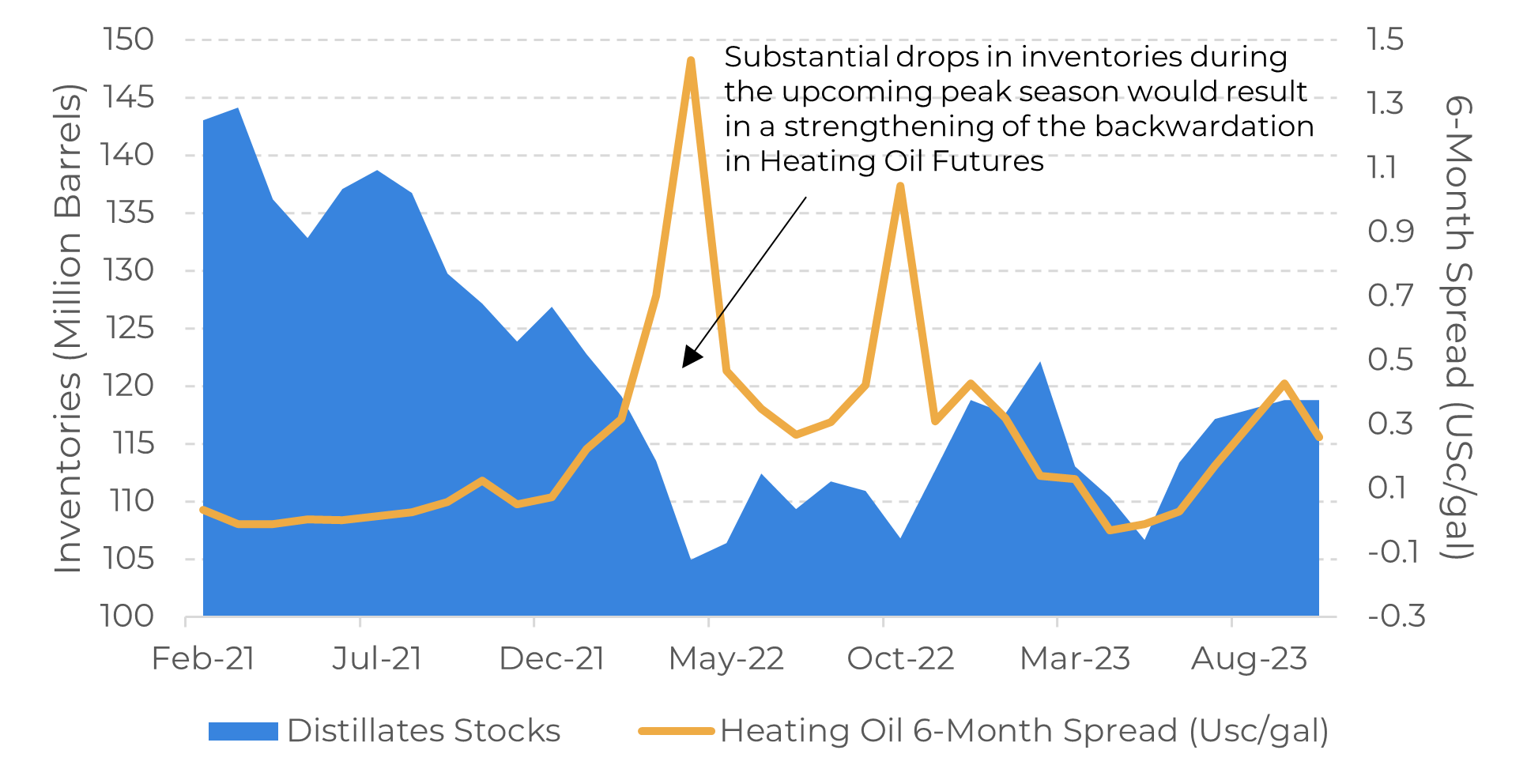

Image 4: Backwardation of Heating Oil vs. Middle Distillate Inventories in the U.S.

Source: Refinitiv

In Summary

The demand for diesel is entering its peak season, which could further strain already low inventories if production does not increase. This could lead to higher prices for diesel as well for other goods and services that rely on diesel as a fuel.

The tight global supply will benefit refineries that are still achieving favorable margins from refined products. Despite diesel being the primary margin driver for the last quarter, jet fuel is also performing well due to the increasing number of flights around the world.

Also, the market could find some relief with Russia's recent announcement that it has partially lifted the ban on diesel exports for shipments delivered to ports via pipeline, under the condition that companies must sell a minimum of 50% of their diesel production within the domestic market. This development is anticipated to bring about some normalization in the fuel market.

Nonetheless, it's crucial to take into account that interest rates are currently elevated, constituting a primary risk factor for energy demand. This is particularly significant given the strong correlation between energy demand and the economic cycles of countries, potentially resulting in decreased prices for energy products.

Weekly Report — Energy

Written by Victor Arduin

victor.arduin@hedgepointglobal.com

victor.arduin@hedgepointglobal.com

Reviewed by Natália Gandolphi

natalia.gandolphi@hedgepointglobal.com

natalia.gandolphi@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.

To continue using the Hedgepoint HUB, please review and accept the updated terms.