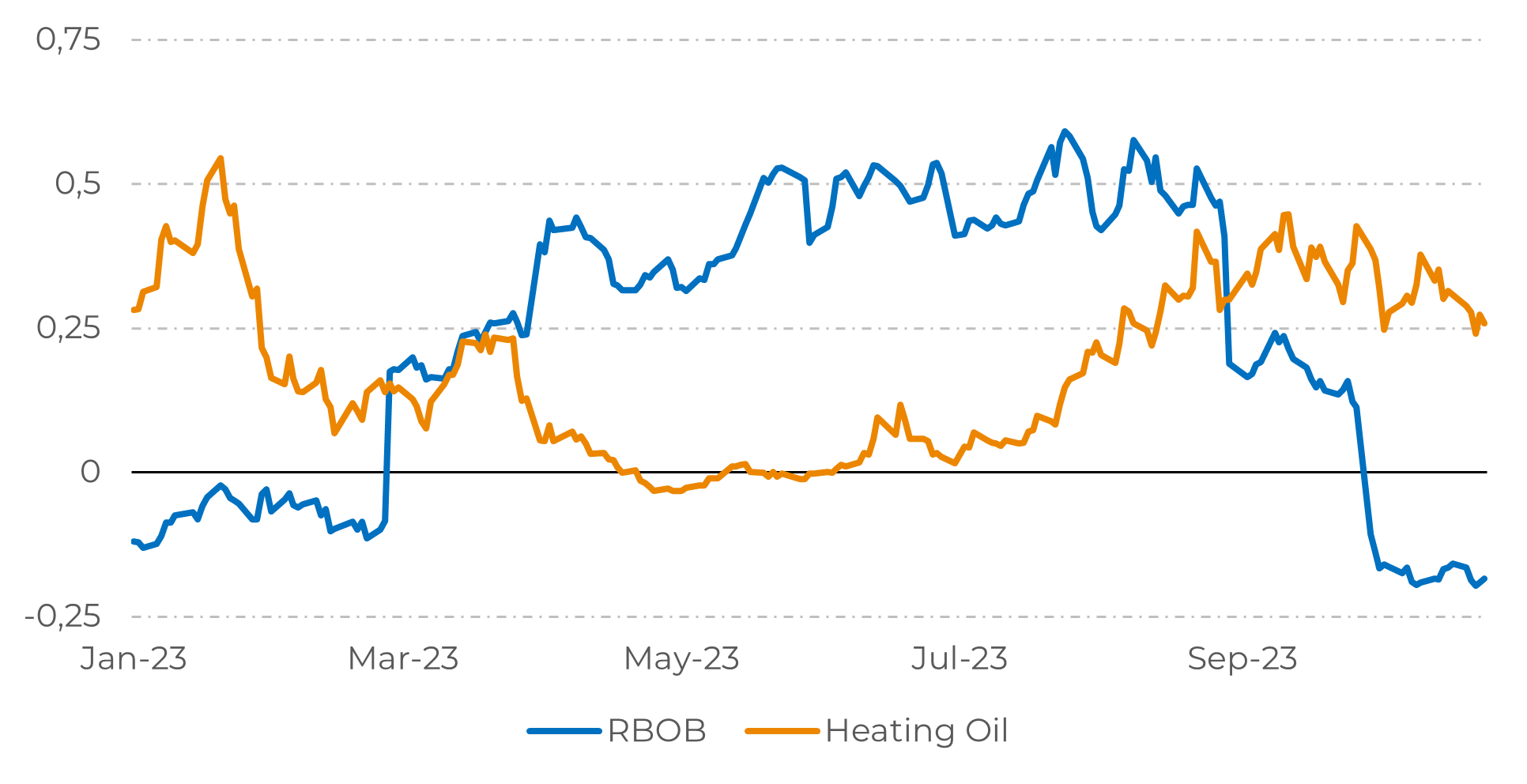

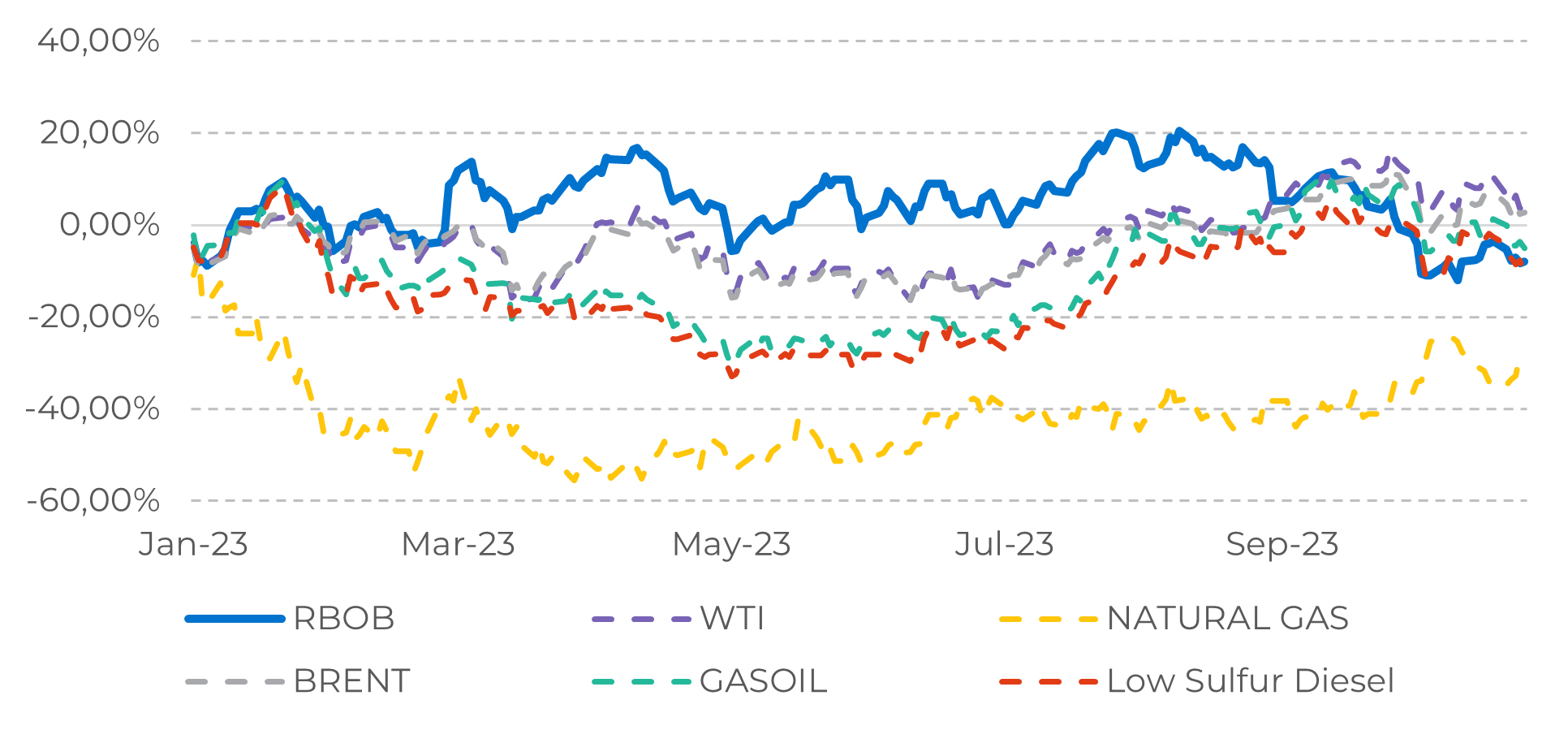

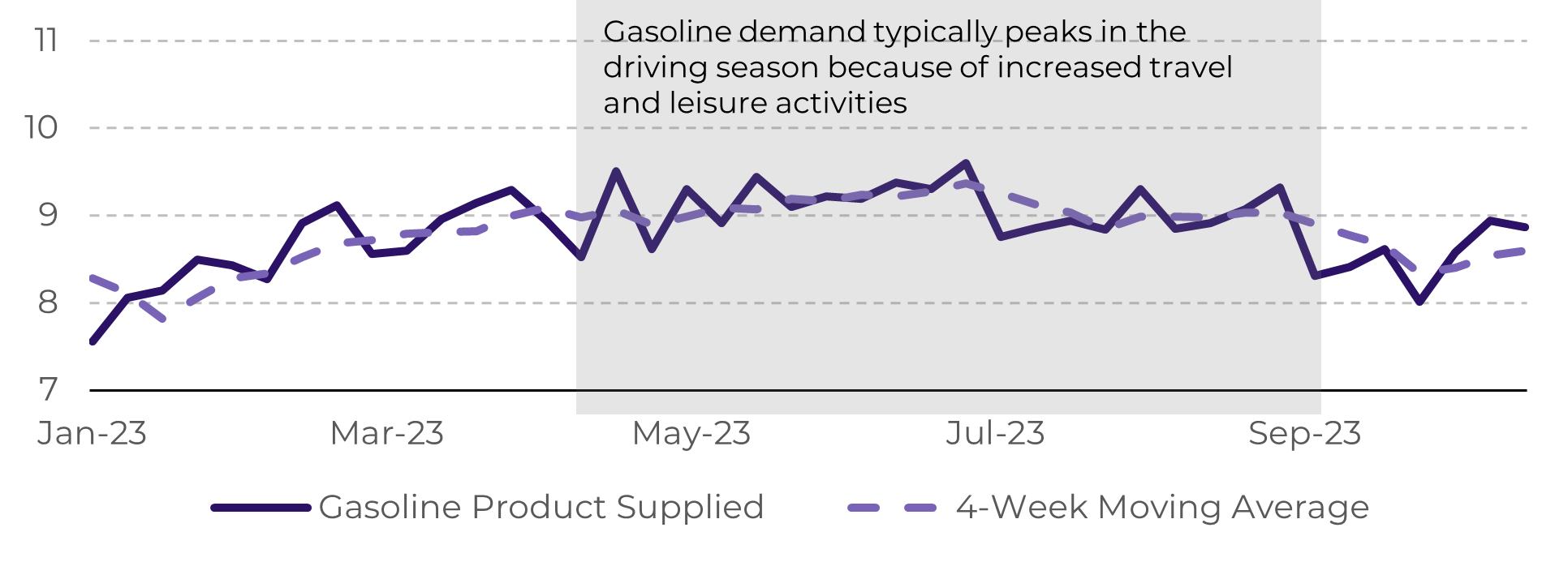

During the initial half of the year, gasoline stood out as the energy product that appreciated the most. High demand for travel and a robust household spending, promoted a bullish environment for this commodity. Nevertheless, as the driving season ended and with no significant risks of disruptions, such as hurricanes, RBOB has experienced a swift decline in value in recent weeks.

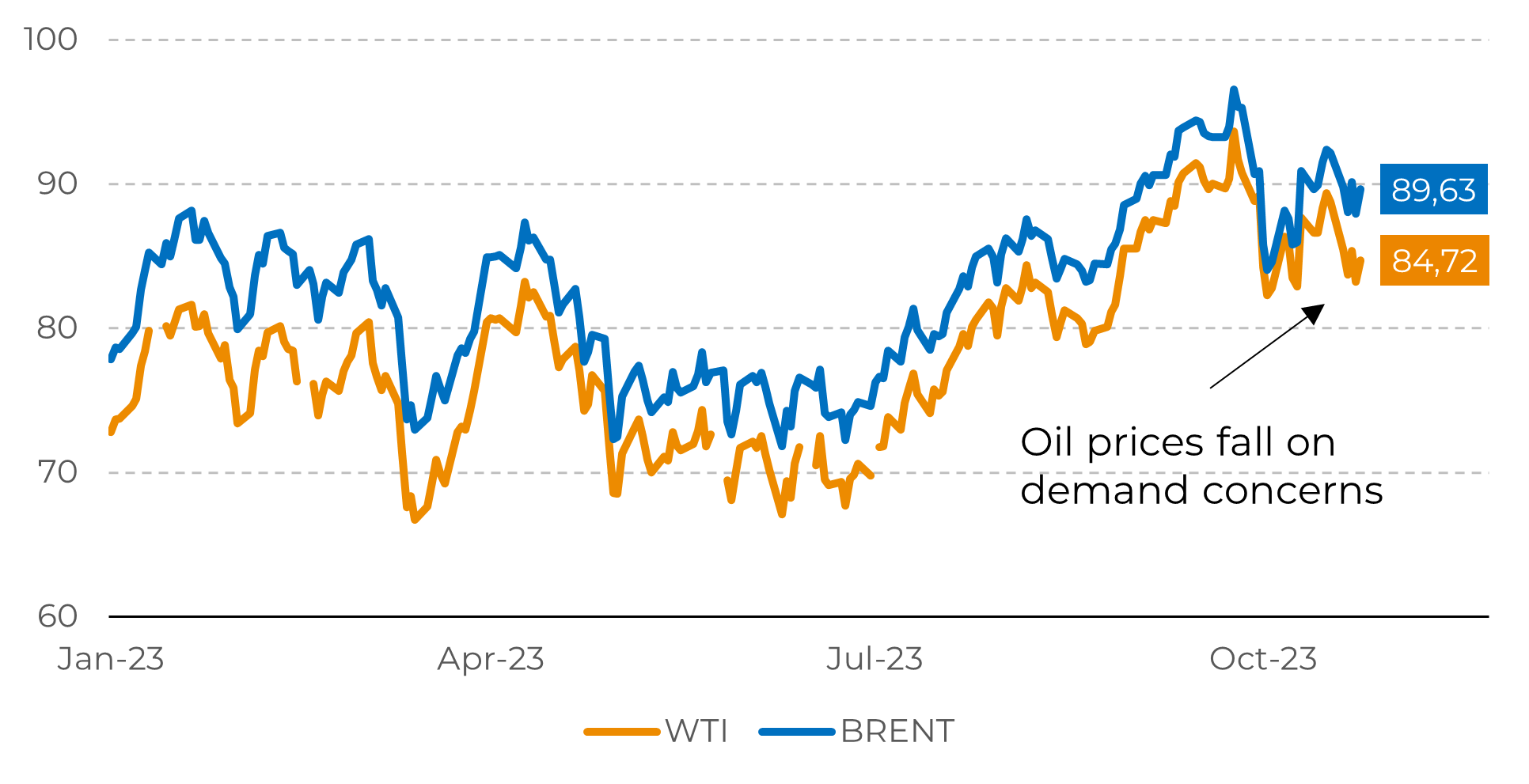

While further weakness in gasoline prices seems likely, it's important to note that market volatility can't be entirely ruled out. One significant factor that could potentially disrupt this downward trend is the Israel-Hamas conflict. Iran, the third-largest oil producer in OPEC, may face sanctions from Western nations or respond by blocking the Strait of Hormuz. Such actions could lead to an increase in oil prices, which are a primary cost in gasoline production. Geopolitical events worldwide continue to exert a strong influence on the oil market, potentially causing some fluctuations in the coming months.

The price structure of gasoline contracts has been in contango since early October, and this is likely to continue widening into the coming months, as there is no sign of strong demand in the northern hemisphere that would disrupt typical stock building behaviors, while refiners are expected to increase distillate production to meet diesel and heating oil demand, which is expected to increase during the winter.

Furthermore, If it depends on OPEC+, middle distillates are expected to experience a bullish winter for 23/24. Cuts in production by Saudi Arabia and reduced exports from Russia are expected to limit the supply of heavy oil, which is used in the production of heating oil and diesel fuel. Consequently, refineries will need to rely more on light oil, which yields less diesel.