Sep 8

/

Alef Dias

Grains, Oilseeds and Livestock Weekly Report - 2023 09 08

Back to main blog page

"In Argentina, recent rains in the central and eastern agricultural regions improved hydric conditions slightly. However, the overall crop situation remains challenging. The western Pampas areas still suffer from moisture deficiency, jeopardizing yields as the prime growing period approaches.

Australia continues to suffer with persistent drought conditions since July. Limited rainfall in August exacerbated the situation, except for some areas in Western Australia. Weather forecasts predict below-average rainfall for the next 15 days. Consequently, ABARES revised wheat production estimates down by 800k mt tons to 25.4M mt, 3.6M mt less than the USDA's current estimate.

The world's stock/use ratio is already at its lowest level since 2014/2015, and the situation in the Southern Hemisphere will likely add to this tightness. However, speculative funds keep increasing their short positions, making it uncertain when and if these fundamentals will be priced."

Wheat: Updates on Southern Hemisphere crops

As harvest of spring crops in the Northern Hemisphere advances, our focus turns even more to Southern Hemisphere, as crops in Argentina and Australia enter their critical development months.

Even with the severe decline in Australia’s output due to the El Niño and the “not-so-great” recovery of Argentina’s crop, these countries still rank among the top exporters and combined they will be responsible for around 15% of global exports according to USDA’s current estimates.

Consequently, impacts on their crops remain relevant to the world’s wheat supply and demand balance, so this report aims to discuss the recent developments in Argentina’s and Australia’s crop

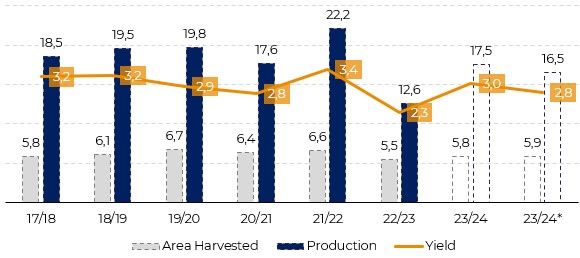

Fig. 1: Argentina Wheat Production, Area and Yield (M mt, M ha, mt/ha)

Source: USDA, Bolsa de Cereales (*)

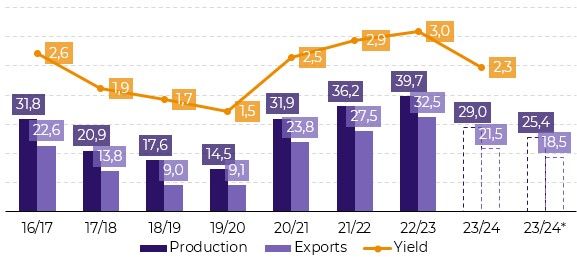

Fig. 2: Australia Wheat Production, Exports and Yields (M mt, mt/ha)

Source: USDA, ABARES(*):

Argentina

In Argentina, it can be said that the crop situation has slightly improved in the past few weeks, but it doesn’t mean that there’s no room for cuts in the current USDA’s estimate.

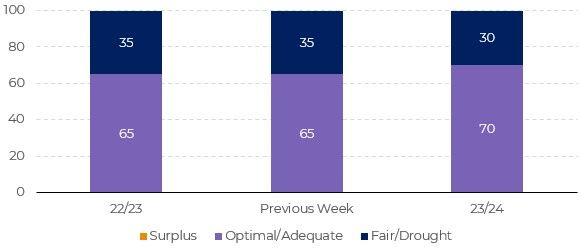

The recent rains recorded over the center and east of the agricultural area produced an increase in hydric conditions. Adequate/Optimal conditions went up by 5.3 p.p., leaving behind the same levels of 22/23.

Nonetheless, the overall situation of the crop remains challenging. Good and excellent crop conditions remain at the same level seen last year (18%) and most crop areas of the western half of the Pampas are still suffering from overall lack of moisture, warranting attention.

Crops in these regions are in great need of more water supply, which must be provided immediately to avoid significant yield reduction, as they enter the prime growing season early September.

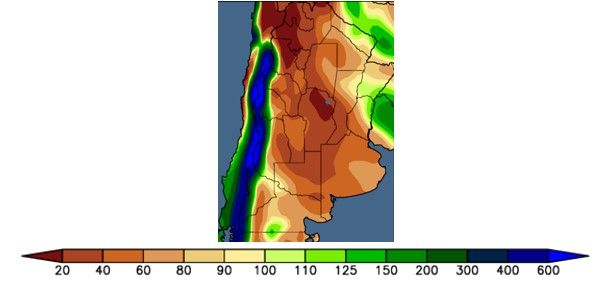

As it is shown in Figure 4, it doesn’t seem to be the case for the next 15-days, as most of the country is expected to witness below-average precipitation levels.

Given this scenario, the current yield estimated by the USDA seems too optimistic and it will likely be adjusted in the coming months. The Buenos Aires Exchange current estimate released this week sits at 16.5M mt, but should this dry scenario for September be confirmed, even this number may be at risk.

Fig. 1: Argentina Wheat Production, Area and Yield (M mt, M ha, mt/ha)

Source: Bolsa de Cereales

Fig. 2: Australia Wheat Production, Exports and Yields (M mt, mt/ha)

Source: World AgWeather

Australia

As it was mentioned in the report of August 18th, when it come to the largest exporters of wheat, Australia is probably the most affected by the El Niño, and crop conditions at that time weren’t great at all – and the situation hasn’t changed much since then.

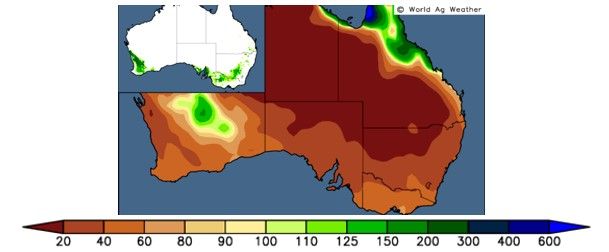

Drought-like conditions have endured across Australia since the start of July. While there were minor rain showers in early to mid-August, arid circumstances have resurfaced in the last fortnight (with the exception to some regions in Western Australia). Weather forecasts are anticipating below-average rainfall for the next 15 days in top producing regions.

Consequently, the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) downgraded its estimates for wheat production by 800k tons to 25.4M mt. The number is 3.6M mt lower than the currently estimated by the USDA.

Fig 5: 15-day forecast precipitation – Australia (% of normal)

Source: World AgWeather (Wheat production shown inset)

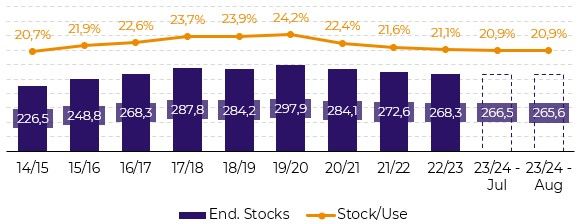

Fig. 6: World Ending Stocks and Stock/Use – Wheat (M mt)

Source: USDA

Conclusion

In general, wheat crops in both Argentina and Australia are suffering with challenging weather in the past few months, which has been hindering the yield potential in both countries. Looking at the difference between local exchanges and agencies estimates vs the USDA, there’s room for an additional 4M mt cut to world supplies.

The world stock/use ratio is already at the lowest level since 14/15, so that’s another bullish risk on the radar, but it’s hard to tell when and if market participants will consider those risks at all, as speculative funds keep increasing their net short positions.

Nonetheless, should any of the bullish risks (lower production in the Southern Hemisphere, India importing relevant amounts, disruptions in the Black Sea grains flow, etc.) trigger a correction in wheat prices, short covering moves can happen, leading to a greater volatility in wheat markets.

Weekly Report — Grains and Oilseeds

Written by Alef Dias

alef.dias@hedgepointglobal.com

alef.dias@hedgepointglobal.com

Reviewed by Victor Arduin

victor.arduin@hedgepointglobal.com

victor.arduin@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.

To continue using the Hedgepoint HUB, please review and accept the updated terms.