Dec 11

/

Alef Dias

Grains, Oilseeds and Livestock Weekly Report -2023 12 11

Back to main blog page

Chicago wheat hit 4-month highs at the beginning of last week, and this rise was greatly influenced by large purchases of US Soft Red Wheat (SRW) by China. With these significant movements, new questions arise. Will this demand continue throughout the year? Can it continue to impact prices?

The combination of a smaller, low-quality crop in the Asian giant and smaller crops in its more "common" suppliers (Australia and Canada) should keep Chinese demand for US wheat strong. However, the drought in the Panama Canal poses an important risk to this scenario.

In addition, other fundamentals may encourage speculators to continue reducing their short positions, such as the delay in planting in France and the estimate of tighter global stocks published in the latest WASDE.

Wheat: Chinese demand should continue to support prices

Introduction

The last two weeks have brought some interesting new fundamentals to wheat markets, most of them with a bullish bias. Among these new fundamentals, Chinese demand certainly stands out the most.

Chicago wheat hit 4-month highs at the beginning of last week, and this rise was greatly influenced by large purchases of US Soft Red Wheat (SRW) by China. The USDA confirmed bookings of more than 1M mt to China at the beginning of last week, the largest volume of sales in a week to the Asian country since July 2014 and close to the largest weekly quantity ever recorded.

With these significant movements, new questions arise. Will this demand continue throughout the year? Can it continue to impact prices? This report aims to provide some guidance on these questions.

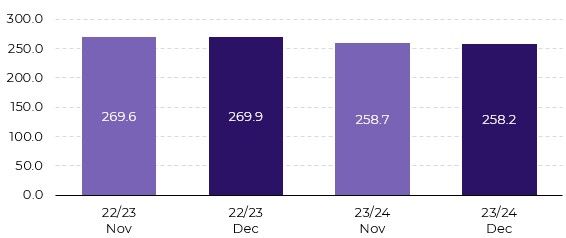

Fig. 1: Wheat Seasonal Imports - China (M mt)

Source:Refinitiv

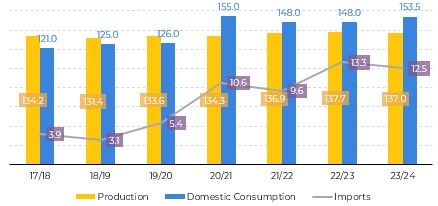

Fig. 2: Wheat S&D balance - China (M mt)

Source: USDA

Chinese demand will likely remain strong

China is on course to import almost record volumes of wheat this year, following a poor harvest and a rise in domestic prices.

The country's wheat crop fell to 137M mt in 2023/24, slightly down on last year and the first drop in five years. The abundance of rainfall in the country's main wheat-growing regions before harvest substantially reduced the quality of the crop, Leading to an unusually large percentage of the crop to be used for animal feed.

This year, domestic wheat prices in China began to rise at the end of July and surpassed those of corn and rice by mid-August. As a result, the country's wheat imports soared in 2023, with totals for the first nine months of the year increasing by 64% compared to the same period last year. However, looking at the accumulated figures, there is still room for a strong import pace to continue.

Demand should be directed to the US

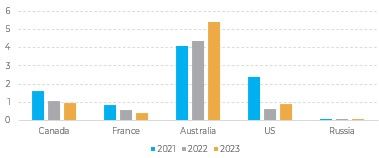

The increase in Chinese demand this year comes at a time when the global supply of wheat has been restricted by extreme weather conditions. Australia, which is China's main source of wheat imports, has been facing its own production cuts resulting from drought exacerbated by the El Niño.

The crop in Canada, another of China's main wheat trading partners, has also suffered this year from drought and extreme temperatures. Historically, France and the US are other countries with a significant share of the Chinese market, but the former had a smaller harvest vs. 22/23 and the already pessimistic projections for the 24/25 harvest in France due to the delay in planting are likely to harm the competitiveness of French wheat in the coming months.

As a result, the US should continue to be the main alternative for Chinese imports throughout the 23/24 harvest, given its good crop - especially SRW, which has been the main type bought by the Chinese

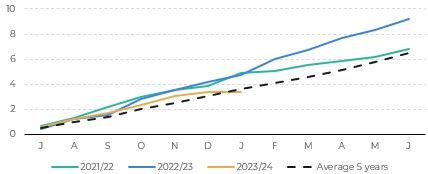

Fig. 3: Wheat Cumulative imports - China (M mt)

Source: Refinitiv

Fig. 4: Main Import Origins - Wheat China (M mt)

Source: Refintitiv

However, it's important to note that the drought in the Panama Canal - one of the main export route for American grain to Asian markets - could have an impact on the competitiveness of US wheat.

The Panama Canal Authority has restricted boat transits this fall, as a severe drought has limited the water reserves needed to operate its lock system. Currently, only 22 transits a day are allowed, compared to around 35 under normal conditions.

The restrictions will probably continue to prevent grain transport until 2024, when the region's wet season could begin to recharge the reservoirs and normalize transport in April or May. In February, transits will decrease even more, to 18 per day.

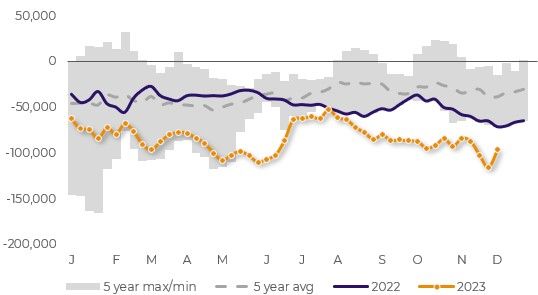

Fig. 5: Speculator positions - SRW wheat (lots)

Source: CFTC

Fig. 6: Global Ending Stocks – Wheat (M mt)

Source: USDA

Conclusions

If the market continues to react to Chinese demand for US wheat as it did last week, price support should remain strong throughout the 23/24 crop year. The combination of a smaller, low-quality crop in the Asian giant and smaller crops in its more "common" suppliers (Australia and Canada) should keep demand for US wheat strong. However, the drought in the Panama Canal poses an important risk to this scenario.

In addition, other fundamentals could push speculators to continue reducing their short positions, as happened in the latest CFTC report. It is already virtually certain that the delay in planting in France will lead to a reduction in the area planted and last Friday's WASDE report brought a further cut in global stocks.

Weekly Report — Grains and Oilseeds

Written by Alef Dias

alef.dias@hedgepointglobal.com

alef.dias@hedgepointglobal.com

Reviewed by Pedro Schicchi

pedro.schicchi@hedgepointglobal.com

pedro.schicchi@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.