Scenarios for vegetable oils markets in 2025/26

Production and consumption of vegetable oils likely to grow in the new season

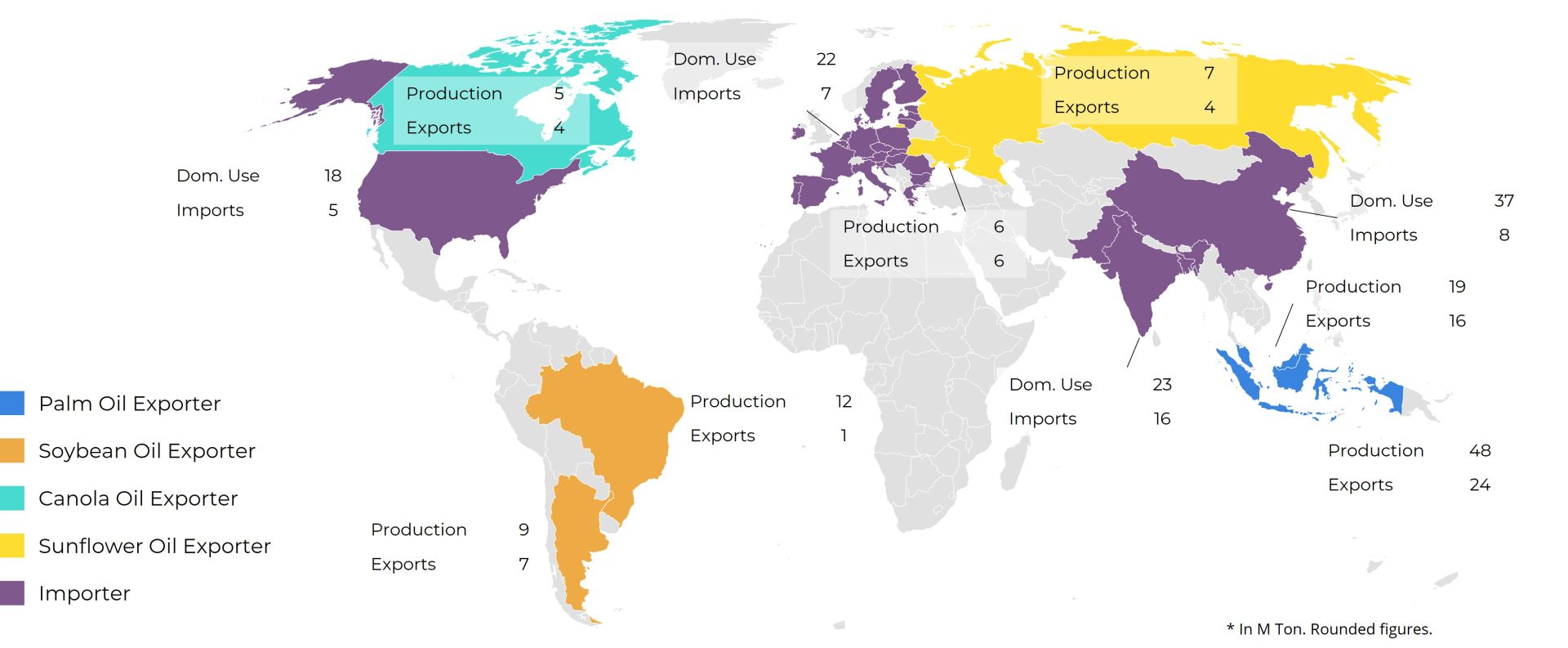

The 2025/26 season should see an expansion in the production and consumption of vegetable oils worldwide. The trend towards larger crops in major producing countries should lead to an environment in which supply expands, making it possible to increase use and imports from major consumer countries. Greater demand for the manufacture of biofuels should be an important driver for consumption in the new season, with increases in mandatory blends expected in some countries. Below are the scenarios for the four main vegetable oils produced and consumed worldwide.

World Map - Vegetable Oils (M ton)

Source: USDA, Hedgepoint

Soybean Oil

Soybean Oil

In the case of soybean oil, the 2025/26 season should bring an environment of greater supply on the global market, due to higher expected production in major producing and exporting countries such as Argentina, Brazil and the United States. On the demand side, there is a trend towards greater consumption in China and India, as well as an increase in domestic use in the large producers mentioned above. In the case of China, there is also an increase in supply due to a probable increase in soybean crushing, which will require greater imports of soybeans (112 M tons).

Soybean Oil - World Supply and Demand - Main Countries (M Ton)

Source: USDA, Hedgepoint

Palm Oil

Palm Oil

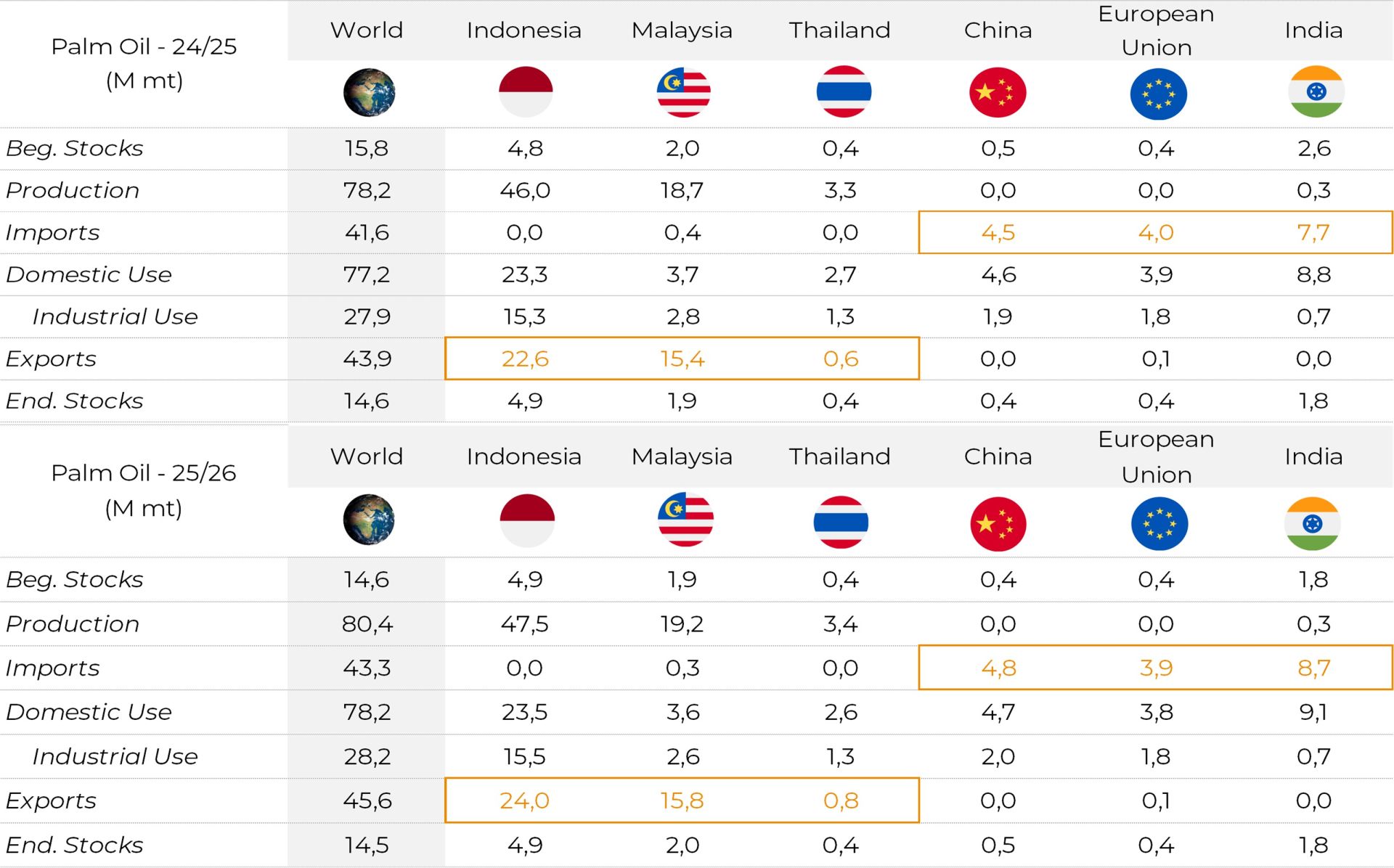

Regarding palm oil, the trend is also for an increase in supply in the 2025/26 season, supported by the likely increase in production in the two main producing and exporting countries, Indonesia and Malaysia. In this sense, if the higher productions are confirmed, we should see a further increase in palm oil exports from these countries.

Palm Oil - World Supply and Demand - Main Countries (M Ton)

Source: USDA, Hedgepoint

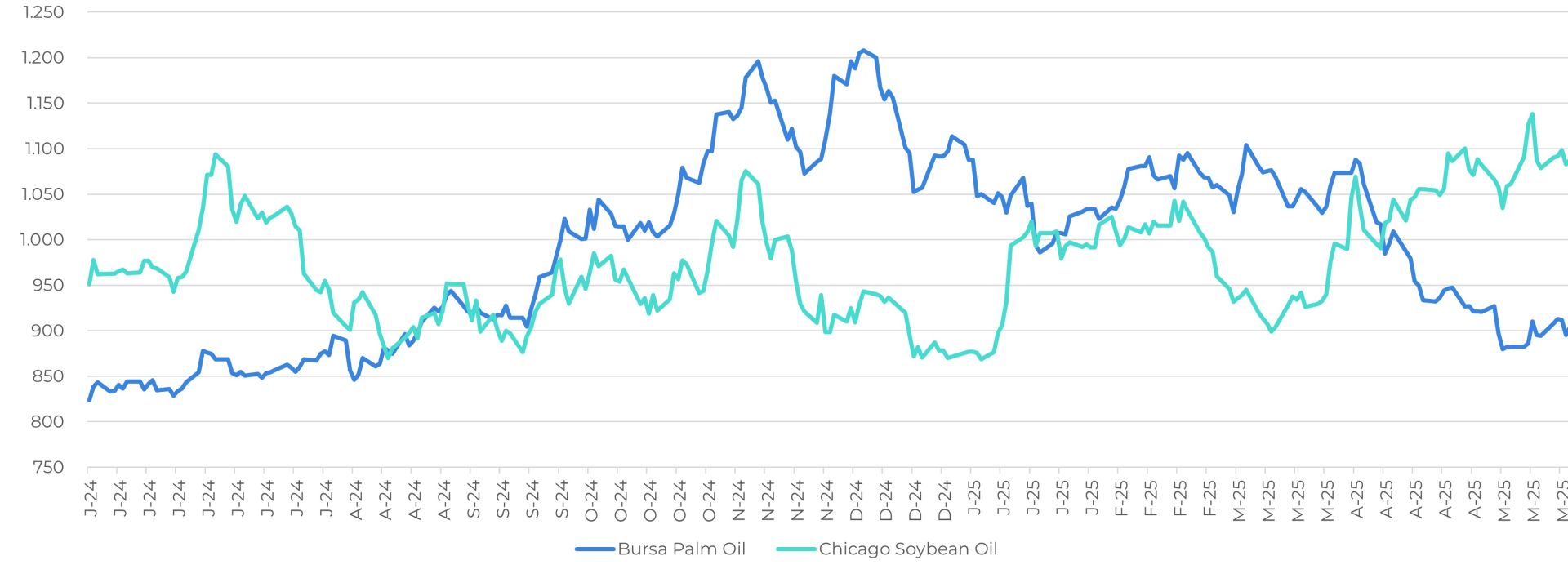

Regarding the price relationship between soybean oil and palm oil, the momentum points to a more favorable scenario for increased consumption of palm oil in the coming months, which after several months is registering prices at lower levels than the soybean-derived pair.

Prices - Soybean Oil vs Palm Oil (USD/ton)

Source: Refinitiv, Hedgepoint

Canola Oil

Canola Oil

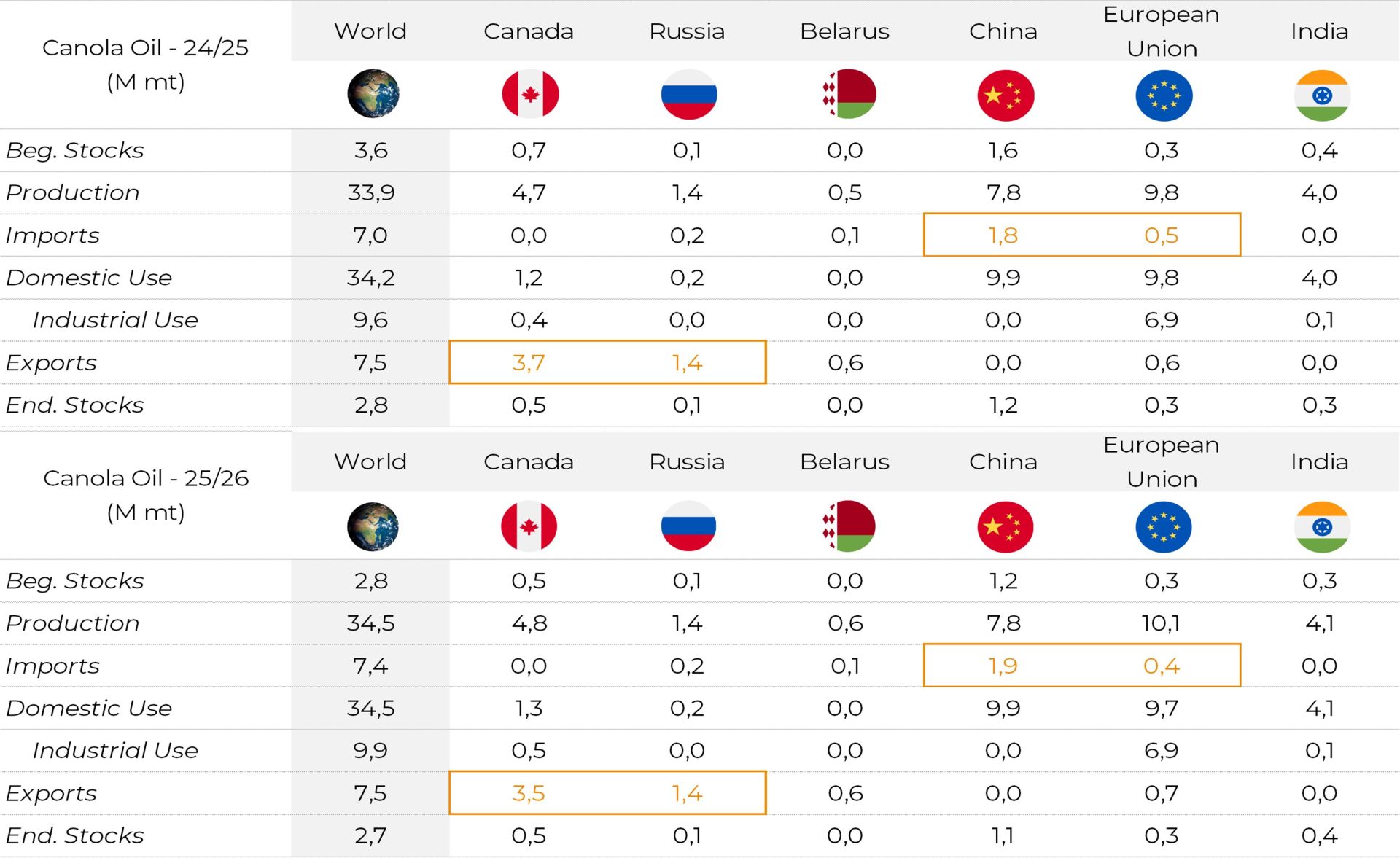

In the scenario for canola oil, initial projections for the 2025/26 season point to a very similar picture to that seen in the 2024/25 season, with few changes in the main figures.

Canola Oil - World Supply and Demand - Main Countries (M Ton)

Source: USDA, Hedgepoint

Sunflower Oil

Sunflower Oil

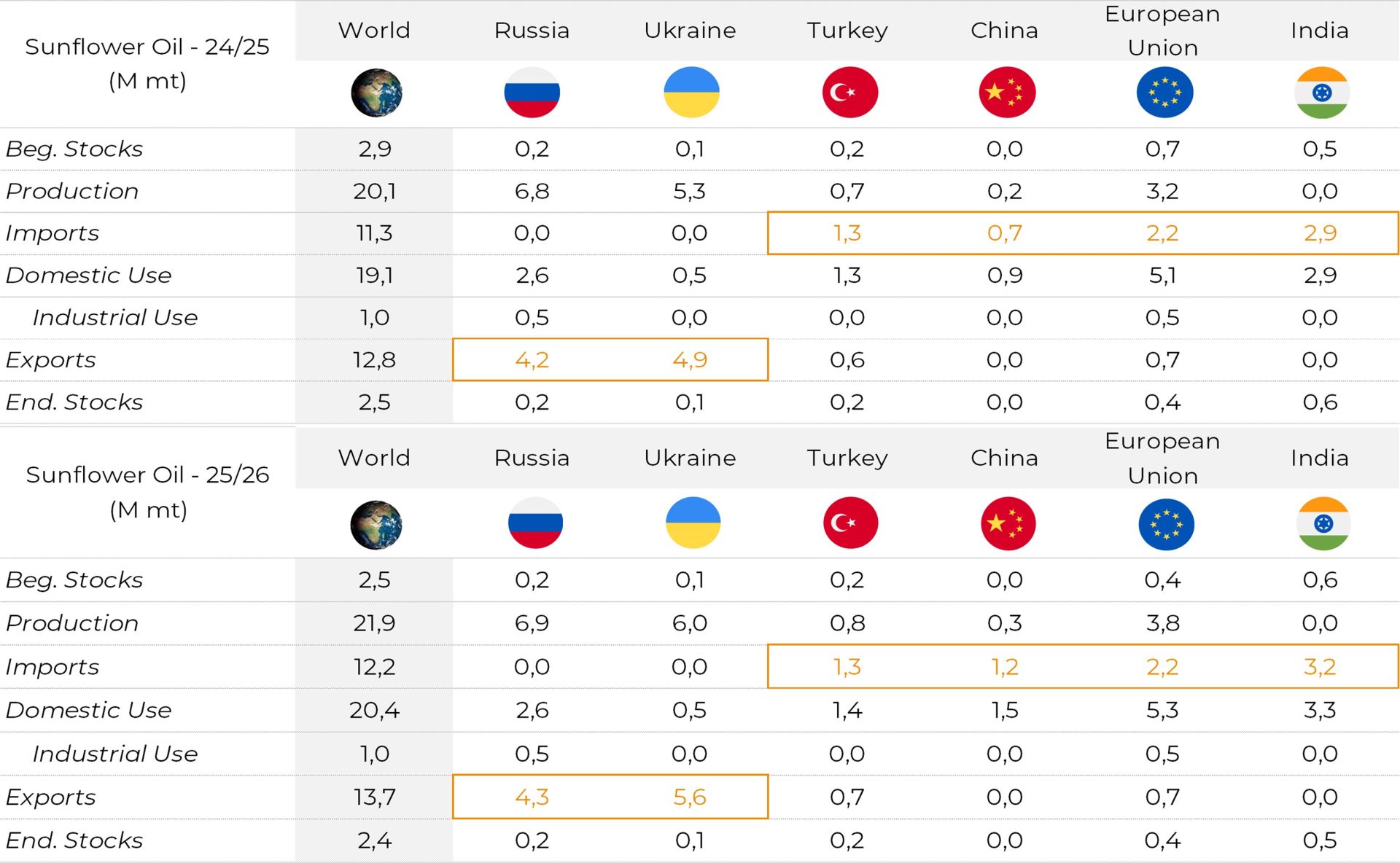

The world scenario for sunflower oil differs somewhat from other vegetable oils in that it is more influenced by the conflict between Russia and Ukraine, a fact that deserves special mention. This is because these two countries are the world's main producers of this oil, as well as naturally being the biggest exporters. Thus, the conflict affects not only production, but mainly exports from these countries, since the main route for exports is the Black Sea (a region considered key in the conflict).

Sunflower Oil - World Supply and Demand - Main Countries (M Ton)

Source: USDA, Hedgepoint

Market Intelligence - Grains & Oilseeds

Luiz.Roque@hedgepointglobal.com

Thais.Italiani@hedgepointglobal.com

Disclaimer

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.