Sep 24

/

Ignacio Espinola

What is going to happen with Corn?

Back to main blog page

China's corn import pace has slowed down a lot this year. However, the Chinese Stock/Use ratio continues to be around the 68-70% level that the government targets in order to feel comfortable.

Brazil export corn program is underperforming versus previous year.

On the US side, exports are not looking as they where on this previous year.

Imports, exports and current situation

Much has been said about current soybean China purchases, where the Asian giant has been buying above normal volumes due to the fear of a new economic war with US and we could think than this same strategy will be repeated for other commodities but let`s have a look at the actual numbers.

Historically speaking, China started importing volumes above 20M Mt of corn in 2020 (imports 2019 – 7.5M mt vs imports 2020 – 29.5 M mt) and that was the year they started buying from the US. Two years later, they cleared the imports for Brazilian corn which came into the equation and took part of the shared that US was having alone for the first 2-3 years.

Corn - Talking about numbers

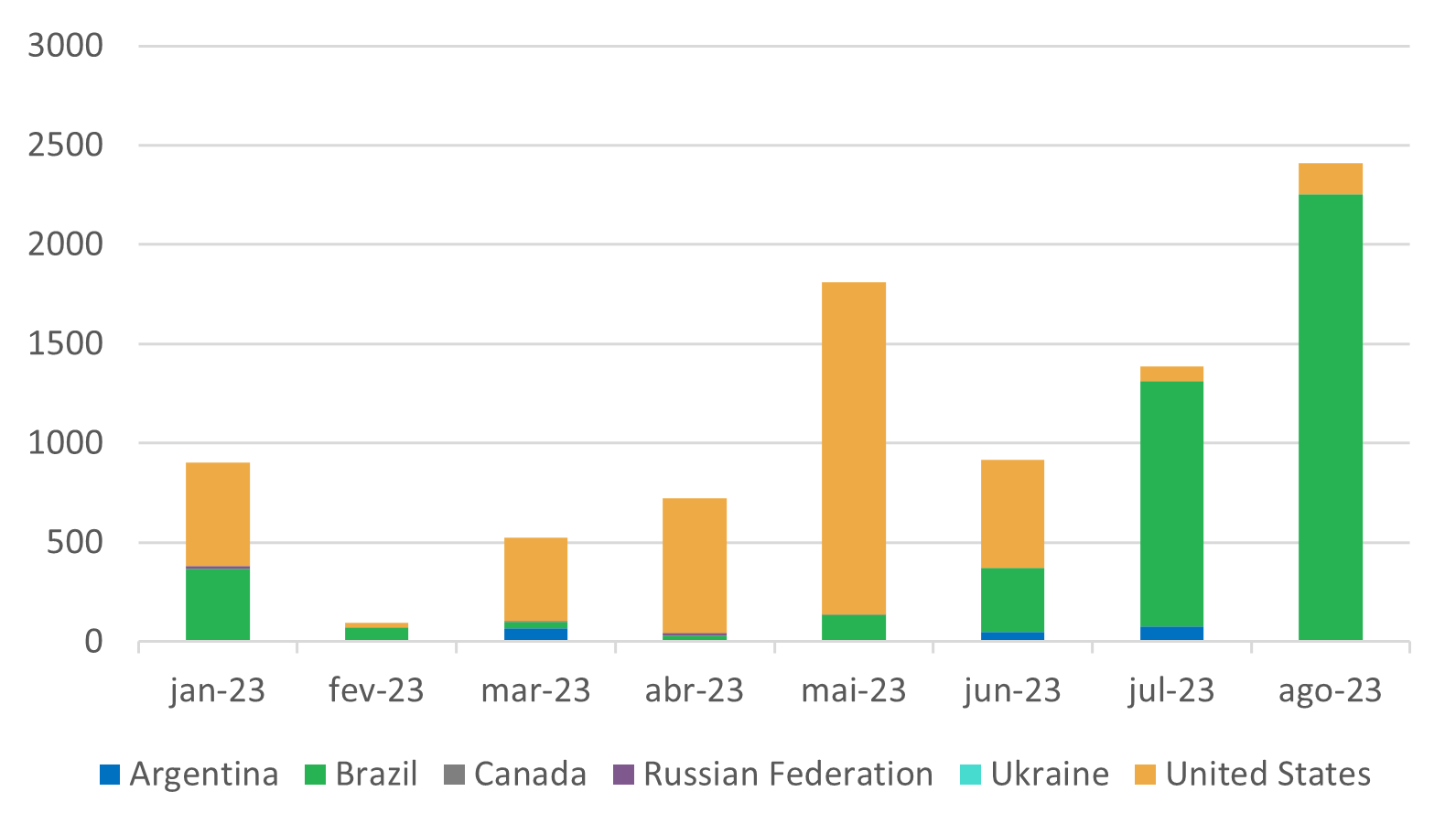

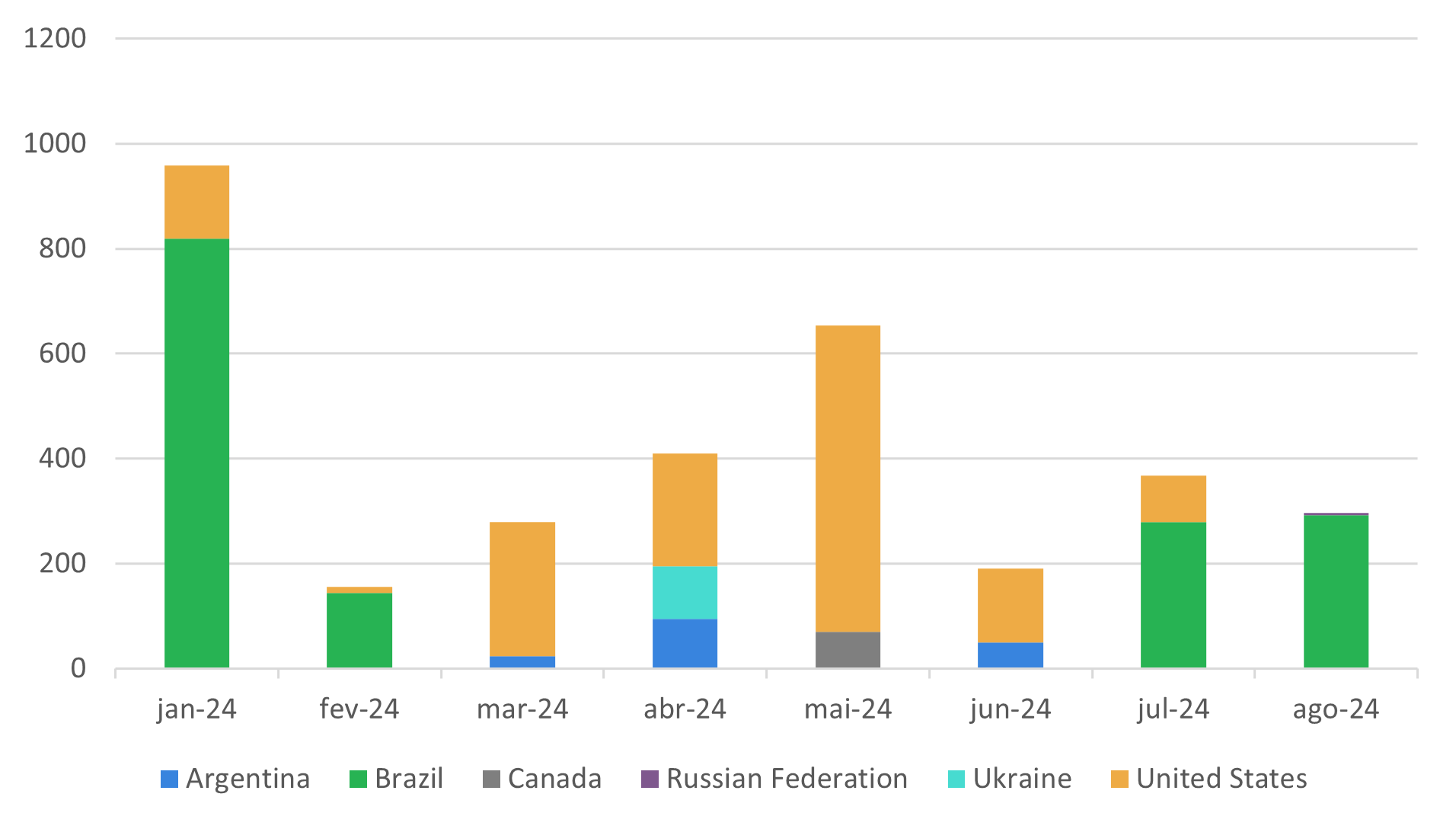

If we take a look at the numbers, China on this 2024 has reduced it`s purchase pace versus 2023. In 2023, according to China customs, they received 8.7M mt versus the 3.3M mt received this year which represents only 38% of the amount on 2023.

When we take a deeper look and we check the origins, the numbers have not changed much Y-o-Y with Brazil being the main origin with close to 48% and with U.S. being the second one with 44%. From the remaining 8%, 5% corresponds to Argentina and the last 3% is shared by Canada, Russia and Ukraine.

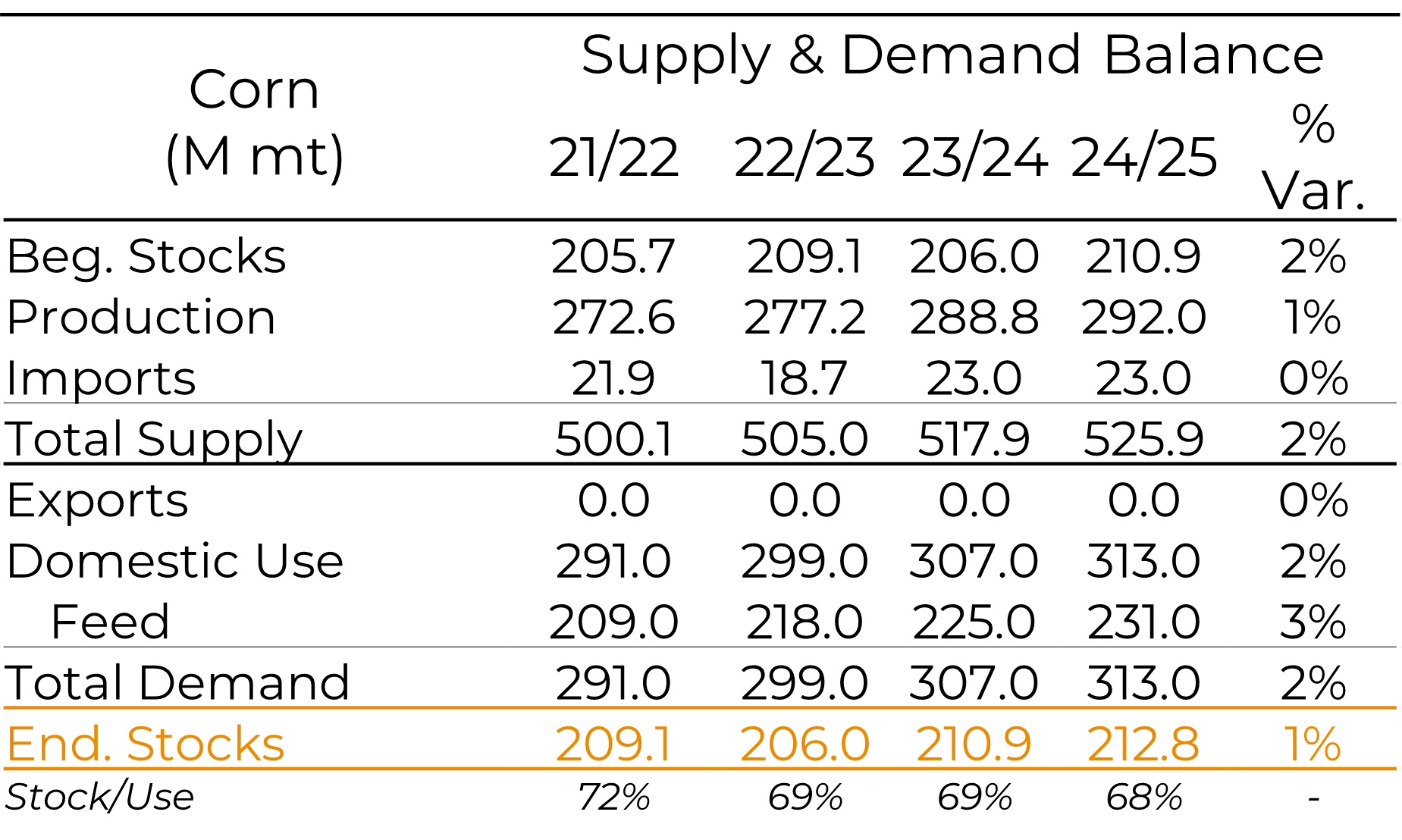

One of the reasons about this low import pace is the Chinese SnD, where this year Chinas production for 23/24 crop was expected at 288.8 Mmt, a 4% increase versus the 277.2 Mmt of the 22/23 crop. For 24/25 the USDA is expecting a 292 Mmt. This 2024/25 crop is supposed to be the fourth- consecutive record-large corn crop.

When we look at China’s imports, on 23/24 China imported 23M mt, 5M mt more versus the precious year and it’s expected to repeat the same 23 M mt for this current crop year. Finally, the third variable we must consider is the demand, which has been growing from 299 in 22/23, 307 in 23/24 and 313 in 24/25 crop.

China Imports Jan-Aug 2023

Source: USDA

China Imports Jan-Aug 2024

Source: USDA

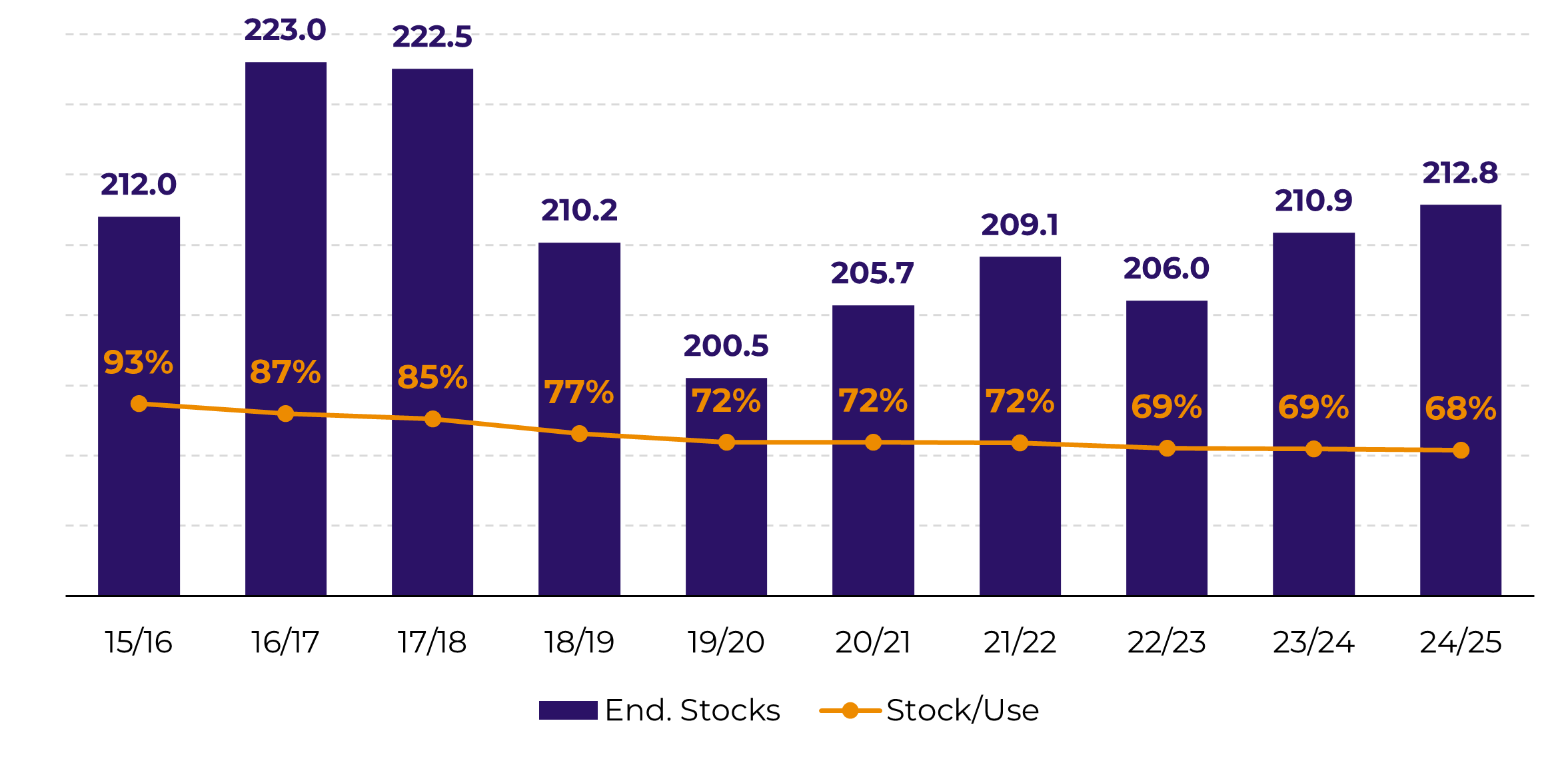

If we sum all those variables, we get to the conclusion that China has been trying to maintain an ending stock level that allows the country to have a 68-69% of stock use level. clearly this has been the government strategy at least for the last 5 years.

Another reason for this slow down on imports could be that the country is focusing more on the soybean side rather than the corn side. Finally, Brazil and US good crop expectations should flood the market with available corn pushing the prices down which may lead the Chinese government to wait for the cash flat prices to go down.

China Supply & Demand Balance

Source: USDA

China Stock/Use

Source: USDA

What is going to happen with prices

The key now is to understand how the prices are going to react to Brazil and US corn exports. On the Brazil side, this year the export program has been delayed due to an extended soybean export program thanks to outstanding purchases from China. If we compare numbers, this year Brazil has exported only 17M mt by the end of august which is 30% less versus the 25 M mt august 2023 exports. On the US side, the Jan-Aug 2023 period had 4.55M mt of corn exported to China while the Jan-Aug 2024 period has 2.77 M mt, 29% less Y-o-Y.

All factor indicates that China will not be able to import as much as the previous years. We only have 4 months to end the year, and if we compare numbers, we are also far beyond 2023. Corn imports to China in September 2023 where 4.25 M mt, but so far this year they are at 0.27 M mt. Same trend happens with Brazil corn and US corn exports so all indicates that this year China import numbers are going to be lower than 2023 but at the same time, Brazil export numbers and us export numbers should also be lower than the previous year.

In conclusion, we have analyzed China’s import pace and its effect on Brazil and US. We expect that China will be importing less than the previous year, and this will also generate a surplus in US and Brazil SnD. Considering the fact that this year Brazil and US crop are going to be big, it does seem that we will have a market flooded with corn which should push the prices down in order to incentivize buyers. Finally, funds are still short Corn, even though they have been slowly covering their position which could indicate that they are looking at some bullish fundamentals for now, otherwise they wouldn`t be covering their shorts. To conclude, we will have more physical corn available, and we are looking to a very good crop for this year which would possibly be a bearish factor for the cash prices.

CBOT Corn – Funds Net position ('000 lots)

Source: CFTC

Weekly Report — Grains and Oilseeds

Written by Ignacio Espinola

ignacio.espinola@hedgepointglobal.com

ignacio.espinola@hedgepointglobal.com

Reviewed by Thais Italiani

Thais.Italiani@hedgepointglobal.com

Thais.Italiani@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Global Markets LLC and its affiliates (“HPGM”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint Commodities LLC (“HPC”), a wholly owned entity of HPGM, is an Introducing Broker and a registered member of the National Futures Association. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and outside advisors before entering in any transaction that are introduced by the firm. HPGM and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. In case of questions not resolved by the first instance of customer contact (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ombudsman@hedgepointglobal.com) or 0800-878- 8408/ouvidoria@hedgepointglobal.com (only for customers in Brazil).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.