Jan 9

/

Ignacio Espinola

Weather market and funds activity

Back to main blog page

• Lack of rains bring concern for the Argentinean crops

• Brazilian soybean crop should be record; harvest about to begin

• USDA January report unlikely to bring major changes to soybean figures

Weather situation in Argentina starting to raise concerns in the market.

Even though during November we experienced rains with 30% above normal values, during December the situation changed with only 80% rains versus historical values.

Over the last weeks, Argentina has suffered from dry weather and low rains raising concerns about potential reduction in the yields. If this is confirmed, we could be in front of the sixth consecutive season of low yields for Argentina, with 2023 being the worst example.

For the near future, weather forecasts suggest that the situation could remain unchanged of get even worst due to lack of rains for at least two more weeks. If this happens, we could end this current month with only 35% of rains versus normal levels which could affect the crop prospects. In theory, we should experience a strong February in terms of rains which could rescue the soybeans and corn crops from a bad January, assuming the crop can resist this current weather.

For now, what we can mention is that the planted soybean crop is in good condition, with 53% of the crop rated good/excellent and only 4% in poor condition which is double versus the previous year at 2% but is below the two-digit numbers that we saw three years ago.

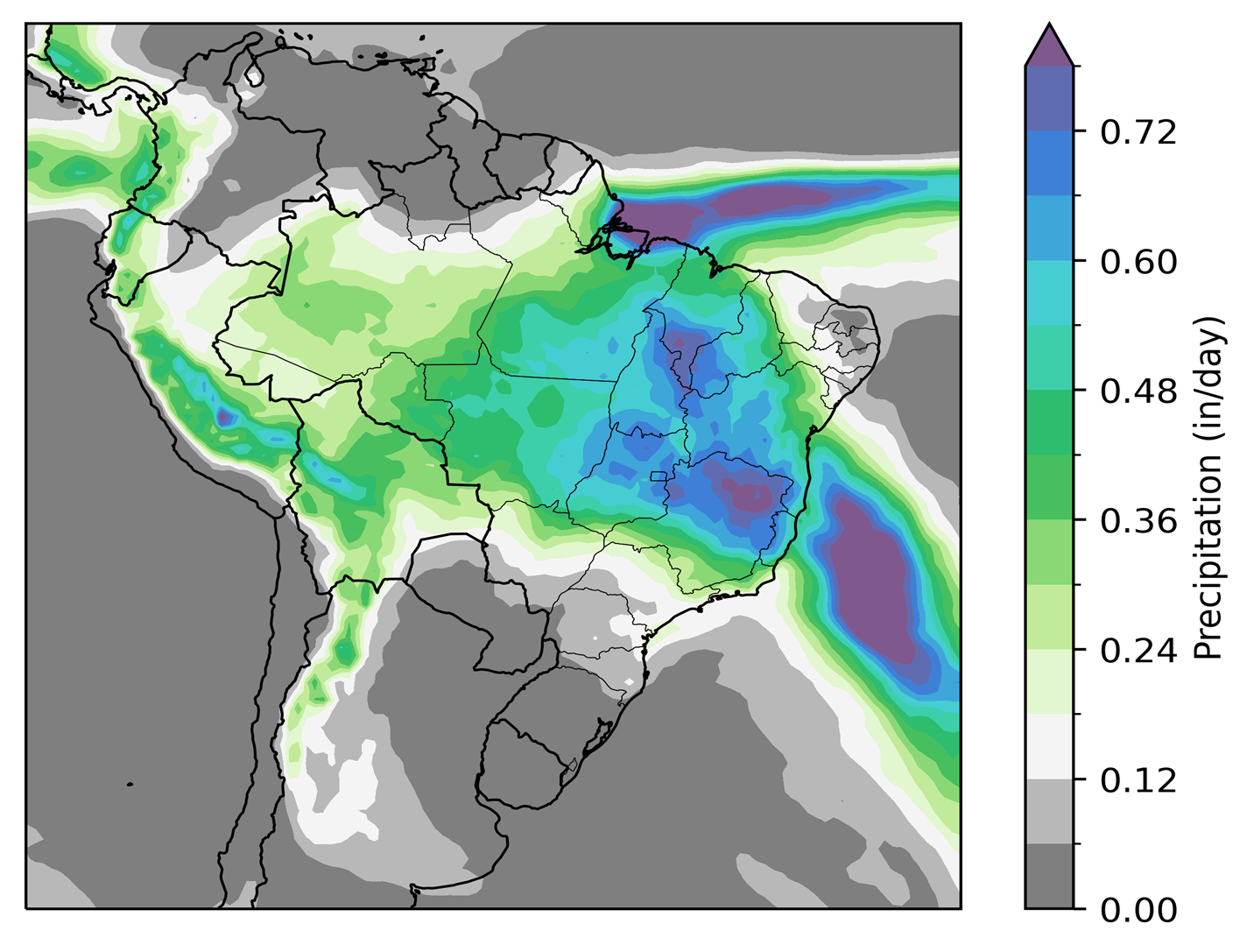

Precipitation – Days 1-14 (in/day)

Source: NOAA, Hedgepoint

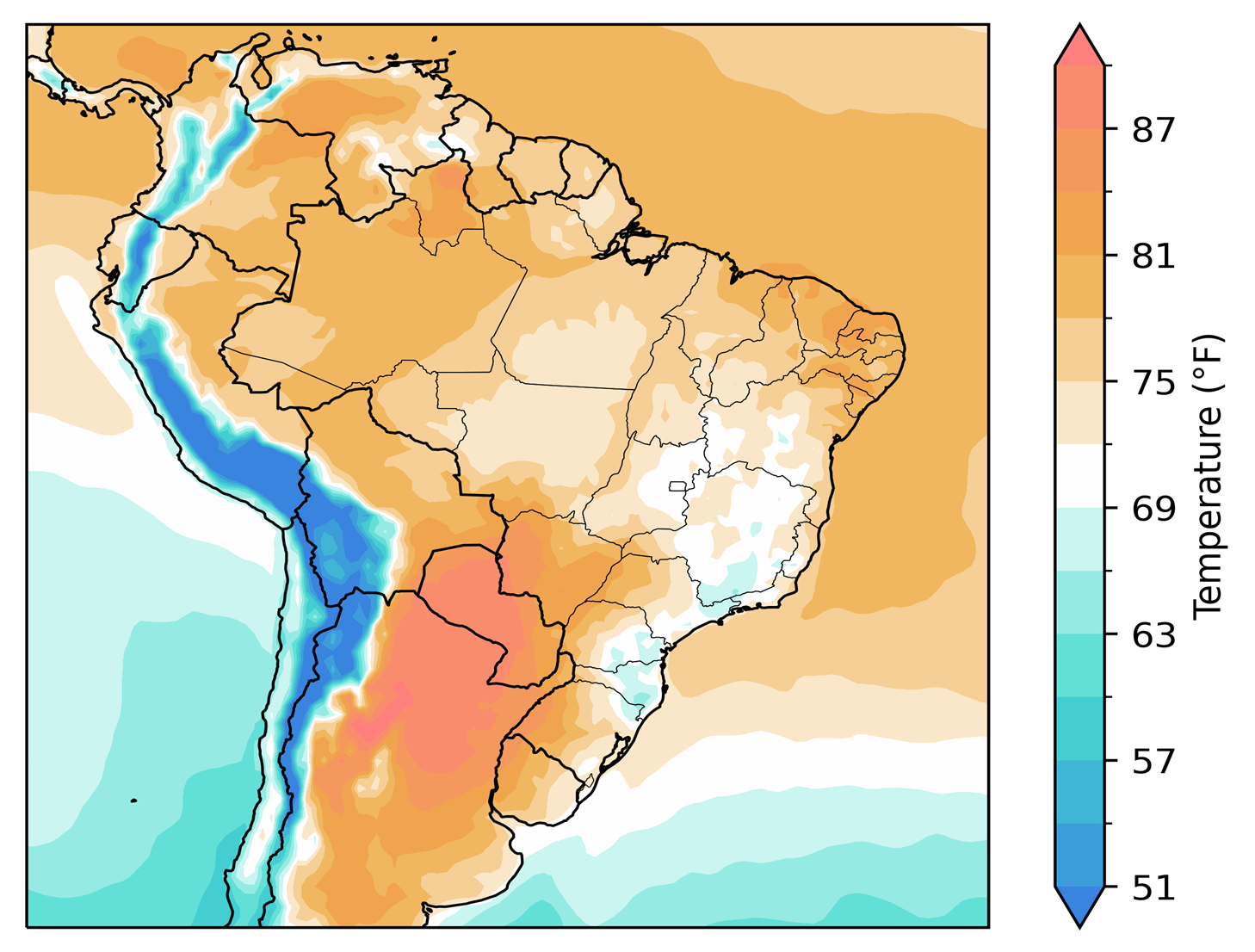

Temperature – Days 1-14 (°F)

Source: NOAA, Hedgepoint

Record crop to be confirmed in Brazil, but weather in Rio Grande do Sul worries

Harvest works on Brazil's new soybean crop is about to begin in the country. Some crops sown earlier in Paraná should be the first to be harvested, with works beginning in the first half of January. We would like to point out that the first yield results for Paraná's crops may be slightly below the plants' productive potential due to the lack of rainfall in the early sowing period in the state. In any case, we expect the results to improve as the work progresses, bringing very high productivity to Paraná's harvest, which should continue to be the second largest soybean producing state in Brazil.

Regarding the other Brazilian states, at least until the end of January we shouldn't see harvest works starting widely, as the delays in planting should also bring initial delays to the harvest, especially in Mato Grosso. However, as soon as the works gains strength, it should move forward at an accelerated pace, especially in the fields where the crops were sown from October onwards. In the Midwest and Southeast, we should see the harvest gaining strength from the second half of February. In the North and Northeast, harvesting should begin in the last few days of February. We would point out that so far there have been no major problems in the crops of the country's main producing states, which leads us to estimate a full and record crop, with high yields expected mainly in the Midwest and Southeast regions.

Regarding to Rio Grande do Sul, there are concerns about the weather for the development of the state's crops, given that January began with little humidity and that this situation could continue until the end of the month. Remember that Rio Grande do Sul is one of the last states to plant in the country. As such, the weather still needs to be favorable for crops that are at an early or intermediate stage of development. For the time being, we think it's a little early to talk about a reduction in the productive potential of Rio Grande do Sul's crop, but if the rains take a long time to return and are not regular, especially in February, losses could occur.

In any case, the trend continues to be for a full and record crop in Brazil, which could exceed 170 million tons for the first time in history. But we need to watch out for the weather over the next 60 days in Rio Grande do Sul.

January's USDA report should bring few changes for soybeans

The United States Department of Agriculture's (USDA) monthly supply and demand report for January, which will be released on Friday (10), should not bring any relevant changes to the main soybean figures, despite expected cuts to US production and stocks.

Although there are currently some concerns about the weather in Argentina and southern Brazil, the market is not expecting any cuts in production figures for these countries for the time being. In any case, it is important to pay special attention to these figures.

On the US side, it is possible that we will see some adjustments to production and ending stocks figures, with the USDA making fine adjustments that may not have a major impact on the market. However, surprises cannot be discarded.

International analysts are projecting US stocks of 454 million bushels (12.36 million tons) for 2024/25, down from the USDA's forecast of 470 million bushels (12.79 million tons) in December.

For the US crop, the USDA is expected to adjust its estimate from 4.461 billion bushels (121.41 million tons) to 4.451 billion bushels (121.14 million tons), in line with market expectations.

In the global soybean supply and demand scenario, the market forecasts ending stocks of 132 million tons for 2024/25, slightly above the 131.9 million estimated in December.

The moment is still a South American weather market and the consolidation of production in Brazil and Argentina. If the weather does not improve, especially in Argentina, it's possible that we'll see more significant adjustments to the South American figures in the February report. However, we cannot discard any surprises in this January report.

Funds Activity

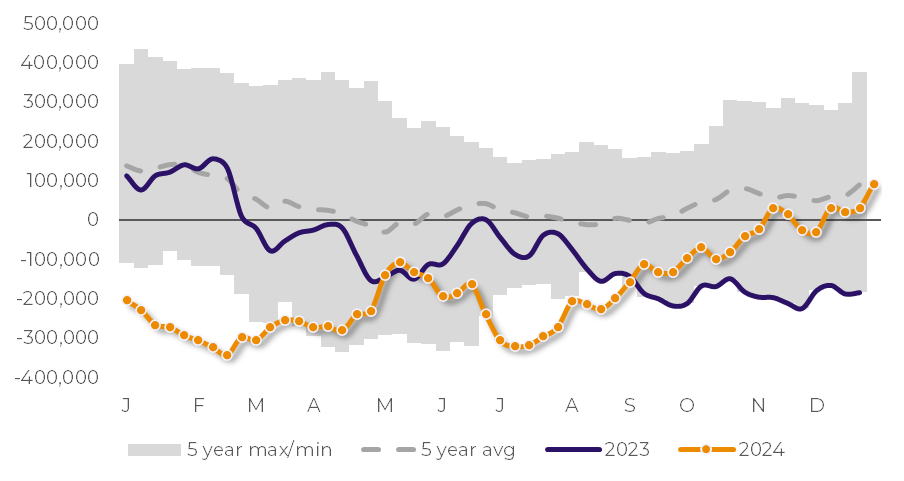

Over the past month of December funds have increased their long positions in corn reaching a level close to the 5-year average position. On the soybean complex side, they have been reducing their short in soybeans and soybean meal while they have increased their short positions in soybean oil.

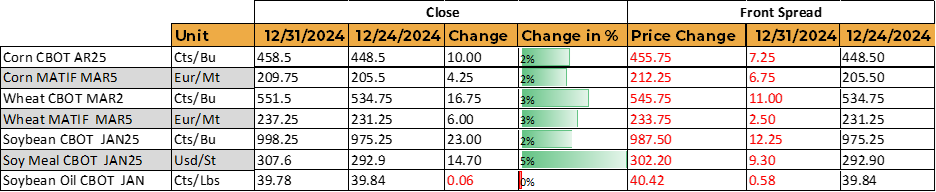

Price evolution in between the last two COT reports:

Source: Reuters

Non-Commercial (Spec) Soybean complex net position

Source: CFTC

Non-Commercial (Spec) Corn net position

Source: CFTC

Written by Ignacio Espinola and Luiz Roque

ignacio.espinola@hedgepointglobal.com

ignacio.espinola@hedgepointglobal.com

Luiz.Roque@hedgepointglobal.com

Reviewed by Ignacio Espinola and Luiz Roque

ignacio.espinola@hedgepointglobal.com

ignacio.espinola@hedgepointglobal.com

Luiz.Roque@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.

Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information.

The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions.

Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.

Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).

Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.

“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint.

Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.