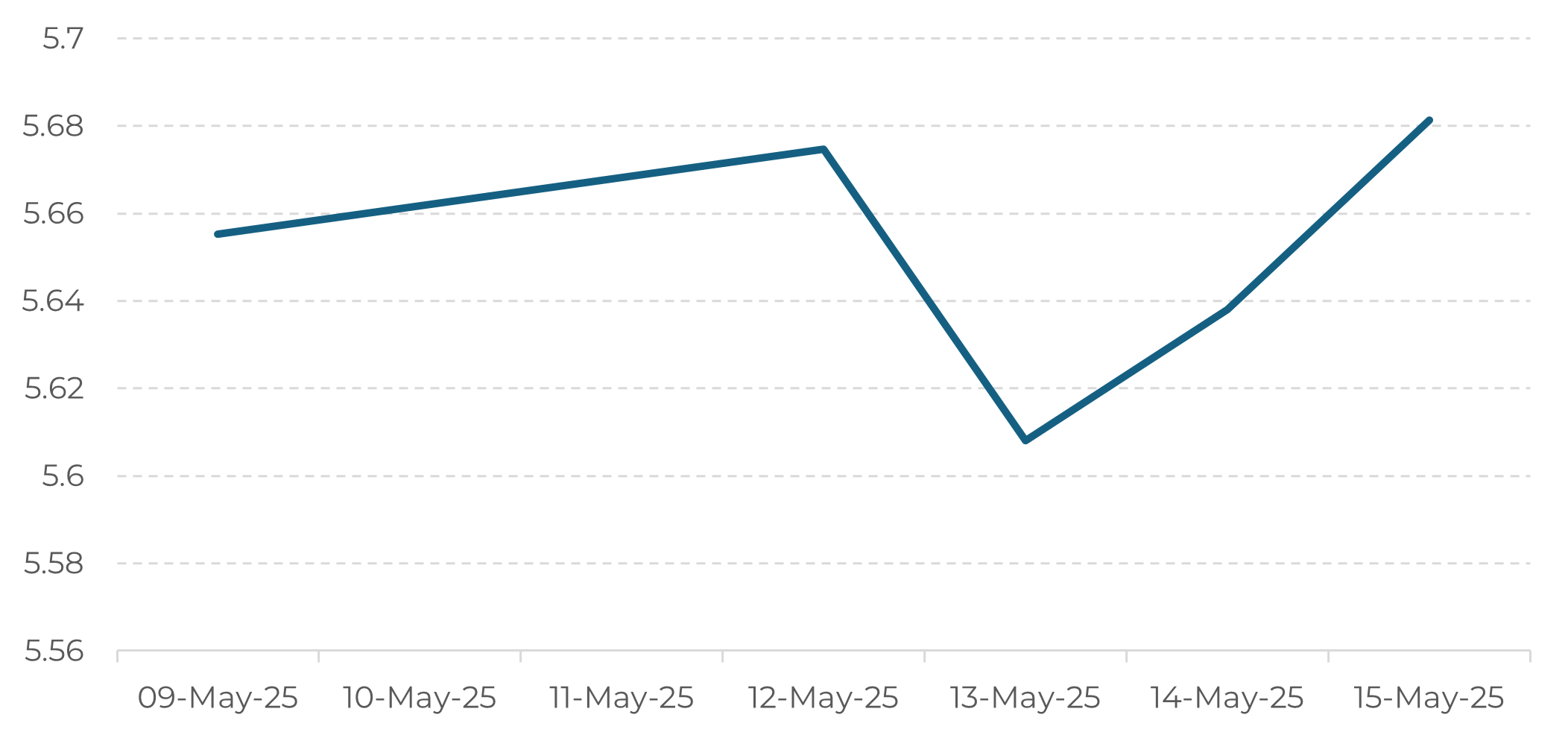

Source: Reuters, Hedgepoint

• Weekly variation: +0.47%

• Low: R$ 5.6085 (May 13th)

• High: R$ 5.6821 (May 15th)

The main catalyst for the change in the exchange rate last week was growing pessimism about Brazil's fiscal sustainability. Signs of non-compliance with the targets established in the new fiscal framework - especially after the release of a lower-than-expected primary result for the first quarter - have raised concerns about the government's ability to contain the growth of the public debt. In addition, rumors of an increase in discretionary spending, coupled with political pressure for an increase in public investment in a pre-election year, have increased fears of deviation from the commitment to fiscal consolidation.

This more fragile fiscal environment reinforced uncertainty in the market, impacting the confidence of local and foreign investors. As a result, there was a risk aversion movement with capital outflows from domestic assets, which put pressure on the futures interest rate curve and boosted the dollar against the BRL.

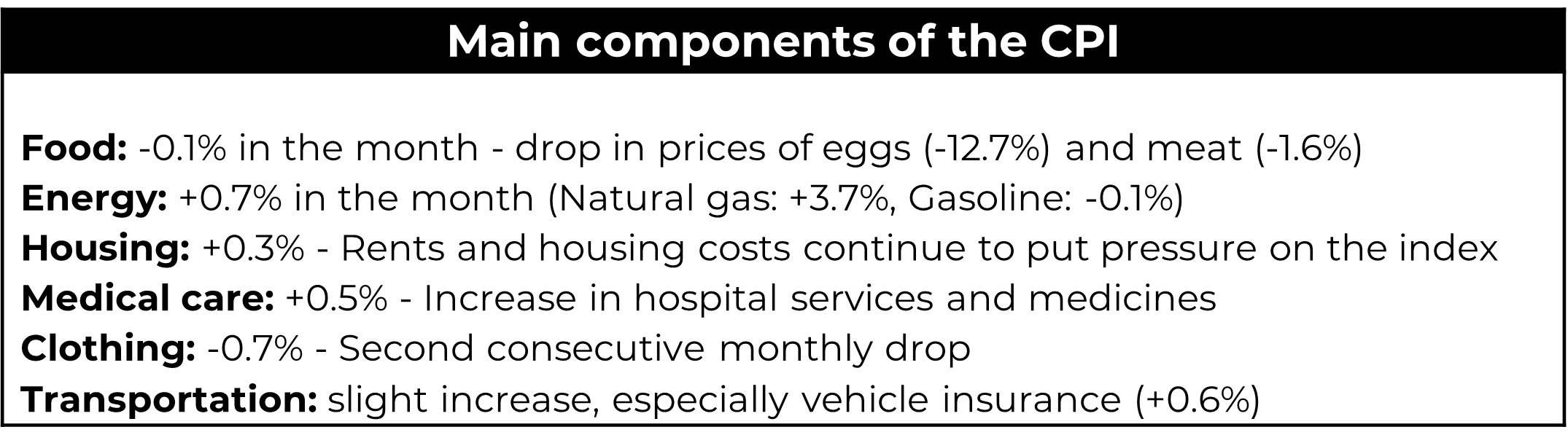

This past week saw the release of relevant indices in the United States, adding more uncertainty and expectations about the world's largest economy. The CPI (Consumer Price Index) for April rose by +0.3%, below the market consensus (+0.4%), showing annual inflation of 2.3% for 2025. On the other hand, the PPI (Producer Price Index) fell -0.1%, reinforcing the expectation that the Fed may start the interest rate cut cycle in 2025, which we have already discussed in past reports. The market is showing a consensus for possible interest rate cuts from September 2025. The global dollar (DXY) retreated momentarily, favoring emerging currencies - an effect that was limited in the case of the real due to the local risk of the Brazilian economy.

Source: Bureau of Labor Statistics (BLS), Hedgepoint

The softer reading of inflation was well received by the markets, but, as discussed here in previous reports, it is believed that the real effects of the tariffs have not yet been reflected in final consumer prices, either because of remaining stocks acquired previously or because they simply haven't been passed on yet. As a result, inflationary pressure could be seen in the coming months.

The Fed's stance on prices remains cautious, observing the behavior of the economy in the coming weeks.

Still on the global scene, after negotiations in Geneva, the US and China reached an agreement to reduce tariffs for 90 days. The US reduced tariffs on Chinese products from 145% to 30%, while China changed its tariffs on American products from 125% to 10%. This agreement was welcomed by the market - still with many uncertainties - as an attempt to ease trade tensions and establish a mechanism for ongoing dialog between the countries.

In recent weeks, Brazil has distanced itself from the performance seen in other emerging markets, with the real depreciating against the dollar, despite a more constructive international environment. The improvement in global risk appetite, driven by trade negotiations between the United States and China - with significant progress announced on May 12, 2025 - was not enough to support Brazilian assets.

Internally, the growing loss of confidence in the conduct of economic policy, coupled with fiscal instability and rising political tensions, has contributed to the weakening of the real. This adverse domestic scenario prevents Brazil from benefiting from the favorable winds from abroad, putting the country in the opposite direction of the appreciation trend seen in other emerging economies.