Jan 15

/

Alef Dias

Macroeconomics Weekly Report - 2024 01 15

Back to main blog page

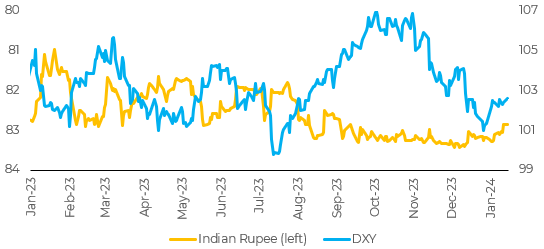

Recent data supports the Indian Rupee

- In 2023, the Indian Rupee recorded an unfavorable performance, mainly due to a historically low interest rate differential against the US.

- Despite this, the Indian economy has shown a remarkable expansion trajectory, fueling optimistic long-term prospects.

- In addition, recent data also suggests a more positive outlook for the Indian currency in the short term. Indian inflation accelerated to 5.7% p.a. from 5.6% in November, which should lead the RBI to start its interest rate cut cycle later than the Fed.

- The reduction in trade deficits should also strengthen the Rupee in the short term. India's trade deficit narrowed for the second month in December, after reaching a record high in October.

Introduction

The Indian Rupee had a negative performance in 2023, largely due to a historically low interest rate differential against the US. However, the Indian economy has shown a robust growth trend, which gives rise to long-term optimism, and recent data also points to greater support for the Indian currency in the short term.

Image 1: Indian Rupee and DXY

Source: Refinitiv

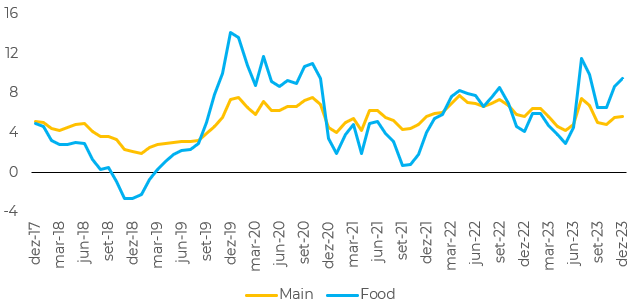

Accelerating inflation is far from worrying and should strengthen the interest rate differential in the short term

Indian inflation accelerated to 5.7% p.a. from 5.6% in November. The increase was due to higher food inflation, especially vegetables. A lower base compared to the previous year and a shortage of onions and tomatoes due to unseasonal rains increased vegetable inflation. These gains are likely to be reversed in January amid increased supply.

There was a general drop in the components of core inflation, which fell further from 4.5% in November to 4.3%. This helped prevent a further increase in the headline reading. Another measure of core inflation, which includes transportation fuels and is monitored by the RBI (India's central bank), also slowed down - falling to 3.9% from 4.1% in November.

A sustained decline in core inflation over the last year suggests that the central bank's tight monetary policy is helping to contain demand-induced pressures. Lower commodity prices and falling logistics and business input costs are also reducing the core reading. On a quarterly basis, core inflation decreased to 5.4% in 4Q23, from 6.4% in 3Q23.

A separate data release showed that industrial production growth slowed to 2.4% year-on-year in November, from a downwardly revised 11.6% in October (11.7% previously). This result was below the consensus estimate of 3.5%. The sharp slowdown was due to seasonal distortions and the base effects of the timing of festive holidays. In 2023, the holidays took place in November, reducing the number of working days. In 2022, these holidays were in October.

This is unlikely to be a major concern for the central bank, since GDP growth has been surprisingly positive. The government's advance estimate of GDP growth for the year ending in March is 7.3%. This beats both the RBI's estimate of 7% and the consensus estimate of 6.6%. As the RBI's current focus is more aligned with reducing inflation to the medium-term target of 4%, policymakers will probably maintain the status quo in February, keeping a tight monetary policy stance.

Image 2: India CPI (%, YoY)

Source: Bloomberg

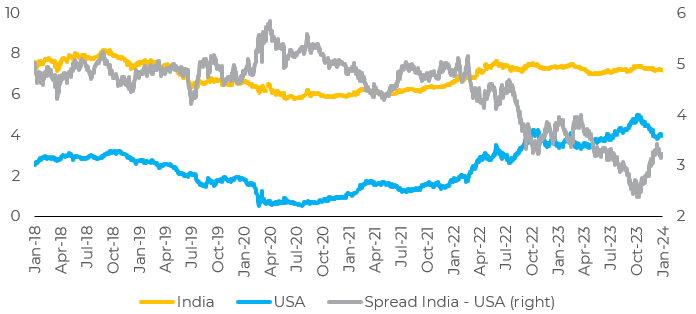

Image 3: 10-year yields

Source: Bloomberg, Refinitiv

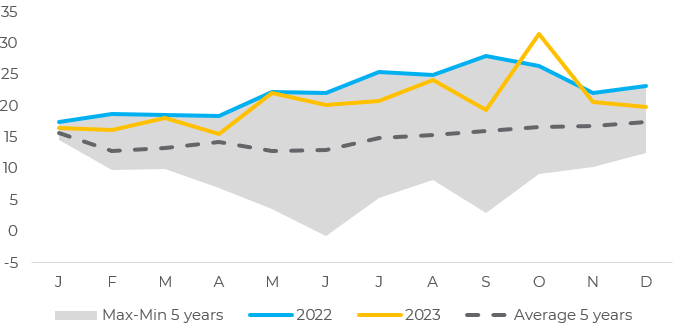

Trade balance should also support the Rupee

India's trade deficit narrowed for the second month in December, after reaching a record high in October. The deficit fell to US$ 19.8 billion, from US$ 20.6 billion in November and US$ 31.5 billion the previous month.

The government's focus on manufacturing is likely to continue to encourage more domestic production. This should mean fewer imports, all things being equal. But faster economic growth will lead to more foreign purchases in general. Meanwhile, a global slowdown is likely to weigh on exports.

A trade deficit that remains close to the current modest level, together with positive investment flows, should bring stability to the rupee this quarter.

Image 4: Trade Deficit - India (USD billion)

Source: Refinitiv

In Summary

The Indian Rupee had a negative performance in 2023, largely due to a historically low interest rate differential against the US. However, the Indian economy has shown a robust growth trend, which gives rise to long-term optimism.

In addition, recent data also suggests a more positive scenario for the Indian currency in the short term. The recent acceleration in inflation should cause the RBI to start its interest rate cut cycle later than the Fed, raising the interest rate differential. The reduction in trade deficits should also strengthen the Rupee in the short term.

Weekly Report — Macro

Written by Alef Dias

alef.dias@hedgepointglobal.com

alef.dias@hedgepointglobal.com

Reviewed by Pedro Schicchi

pedro.schicchi@hedgepointglobal.com

pedro.schicchi@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.