Feb 14

/

Victor Arduin

Macroeconomics Weekly Report - 2024 02 14

Back to main blog page

China contributes to the slowdown in global inflation

- Inflation has been one of the main challenges in the world economy over the last three years, but in the last year China has helped to alleviate this pressure.

- With the devaluation of its currency and the fall in domestic prices resulting from the lack of consumer and investor confidence in the country, the world's second largest economy has spread its deflation globally.

- However, the persistent deflation in its economy is beginning to pose risks for its economic growth, which could mean fewer commodity imports in the coming years.

Introduction

After a long period of lockdown, a measure imposed to combat Covid-19, China began the process of reopening its economy in 2023. A year of recovery was expected in the world's second largest economy, where the return of economic activity would bring more consumption and growth, but this is not exactly what happened.

The Chinese economy is facing significant challenges. The real estate sector is weak, with less and less stimulus, youth unemployment has risen and the currency has depreciated sharply as a result of high interest rates in the world's major economies. However, one of the most significant challenges has been deflation.

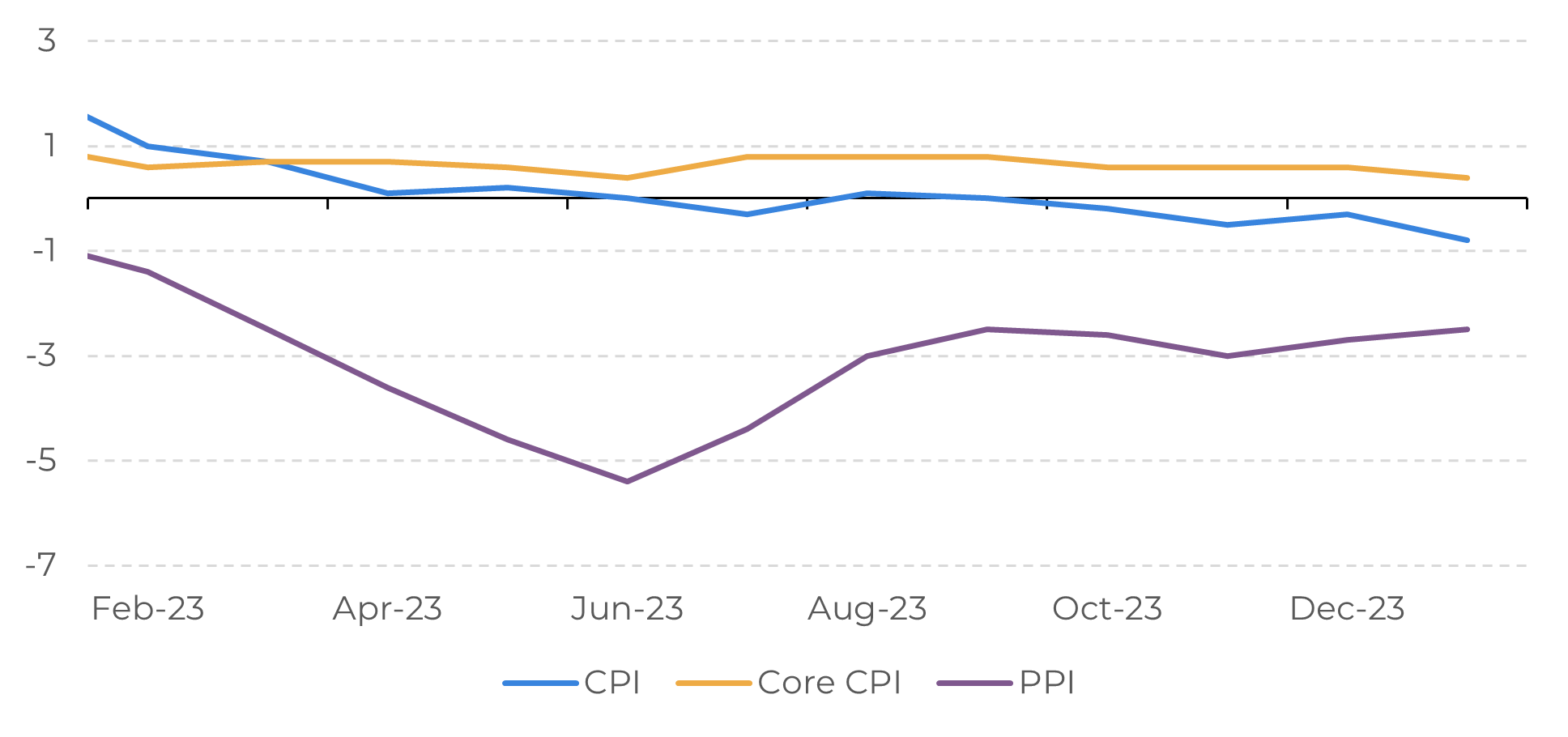

Image 1: China - Consumer and Producer Inflation (%)

Source: National Bureau of Statistics of China

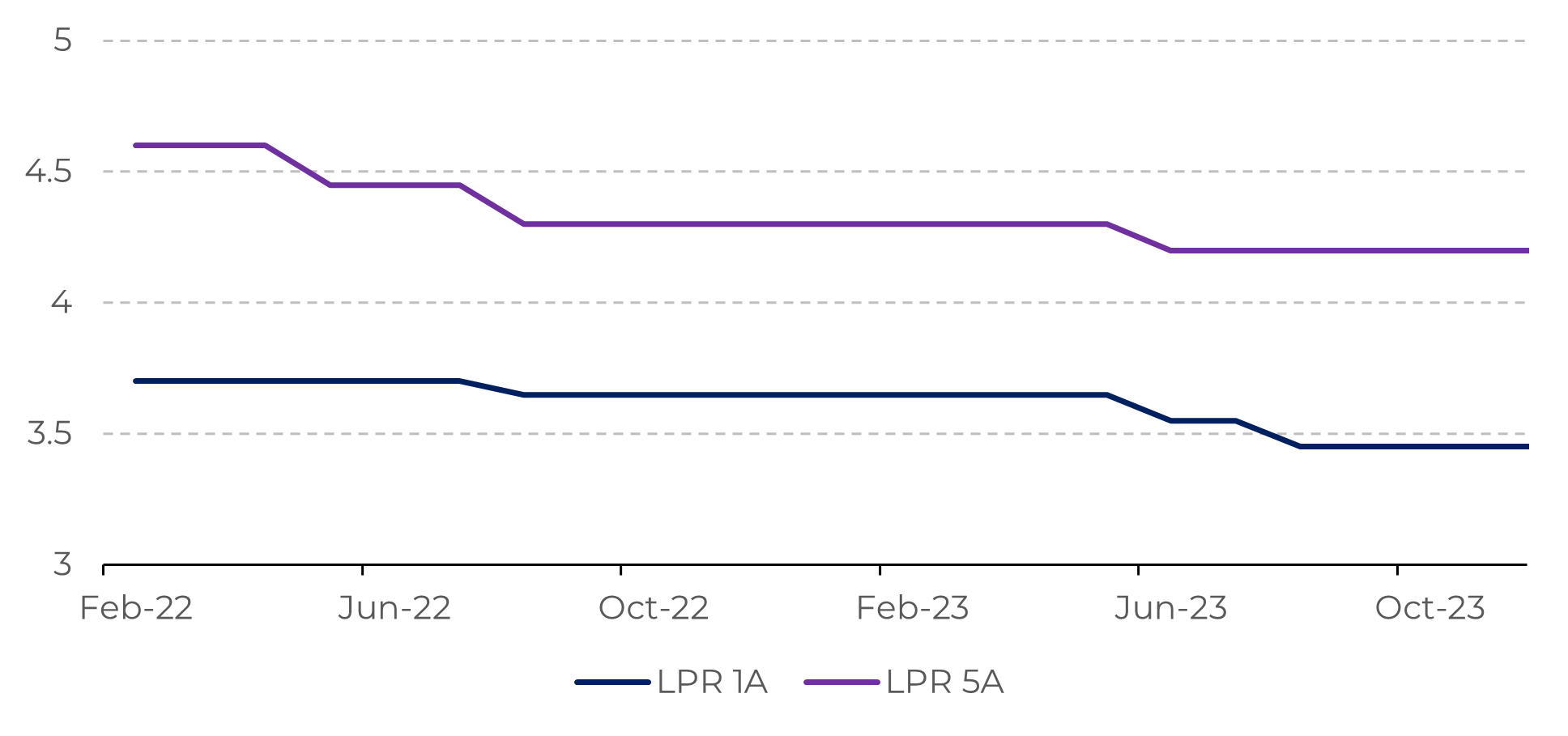

Image 2: China - Basic Interest Rates (%)

Source: PBoC

Chinese export prices falling

In recent years, China has attracted attention due to a less robust economic performance than that seen in recent decades. Despite registering lower growth, with a GDP expansion of 5.2% in 2023, the country still maintains its importance as a significant driver of the global markets. However, it is undeniable that there are significant challenges, such as inflation, which closed at -0.8% in January.

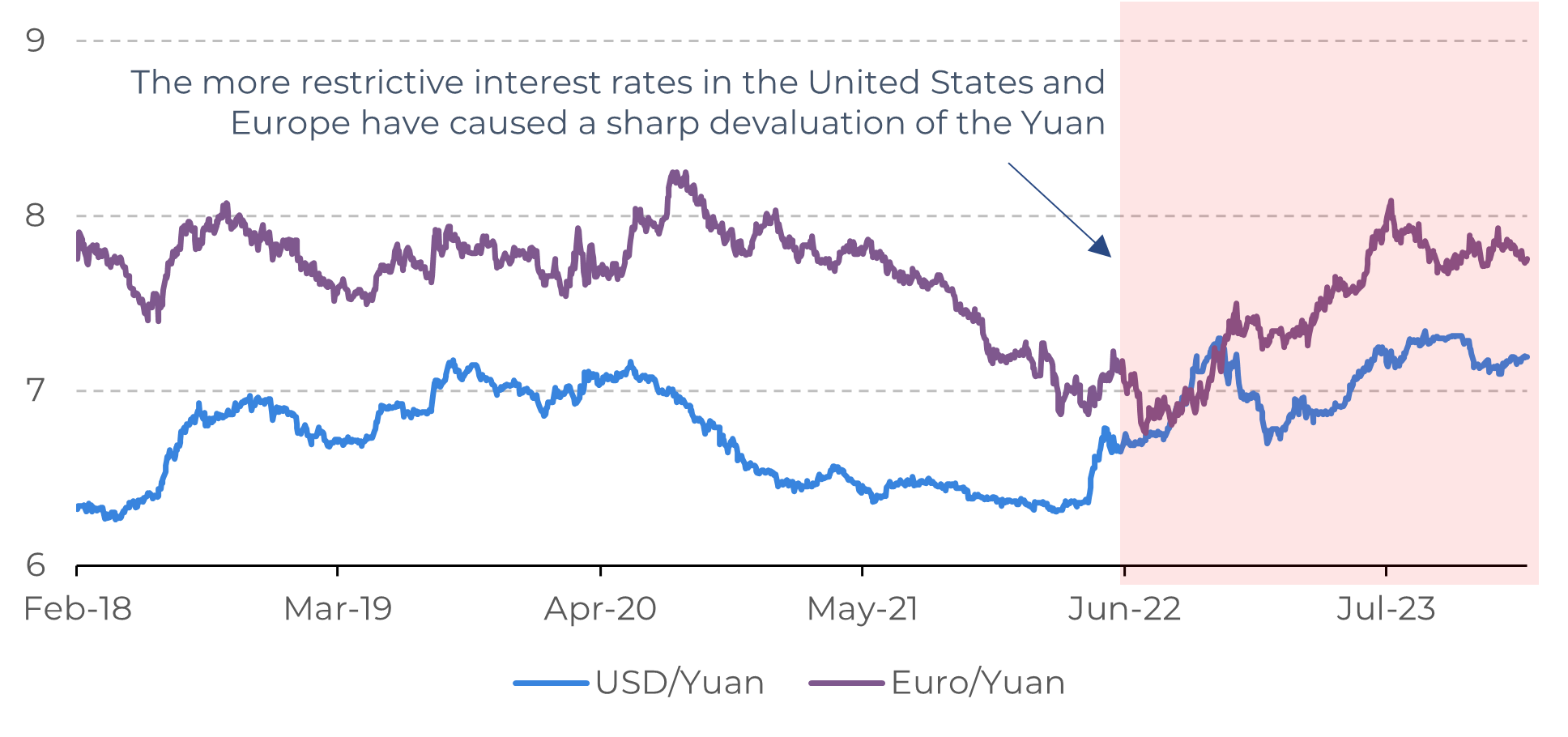

Consumer prices are falling at the fastest rate in 15 years, reflecting investors' lack of confidence in the Asian country's economy. With persistent deflation, the stock market has been devaluing, falling by more than -10% in 2023, as has its currency, which in recent months has depreciated against the euro and the dollar. If Chinese products were already cheaper due to internal deflation in the country, the currency devaluation makes them even more competitive. The combined effect of lower prices and a devalued exchange rate has contributed to global disinflation.

Image 3: China - Yuan Exchange Rate

Source: Refinitiv

In general, lower prices are welcome, but not when they spread deflation in an economy, as has been the case in China. The persistent deflation in the country is affecting economic growth. An example of this is that the IMF predicts growth of 4.6% in 2024, which could fall to 3.5%, and 2% in 2025.

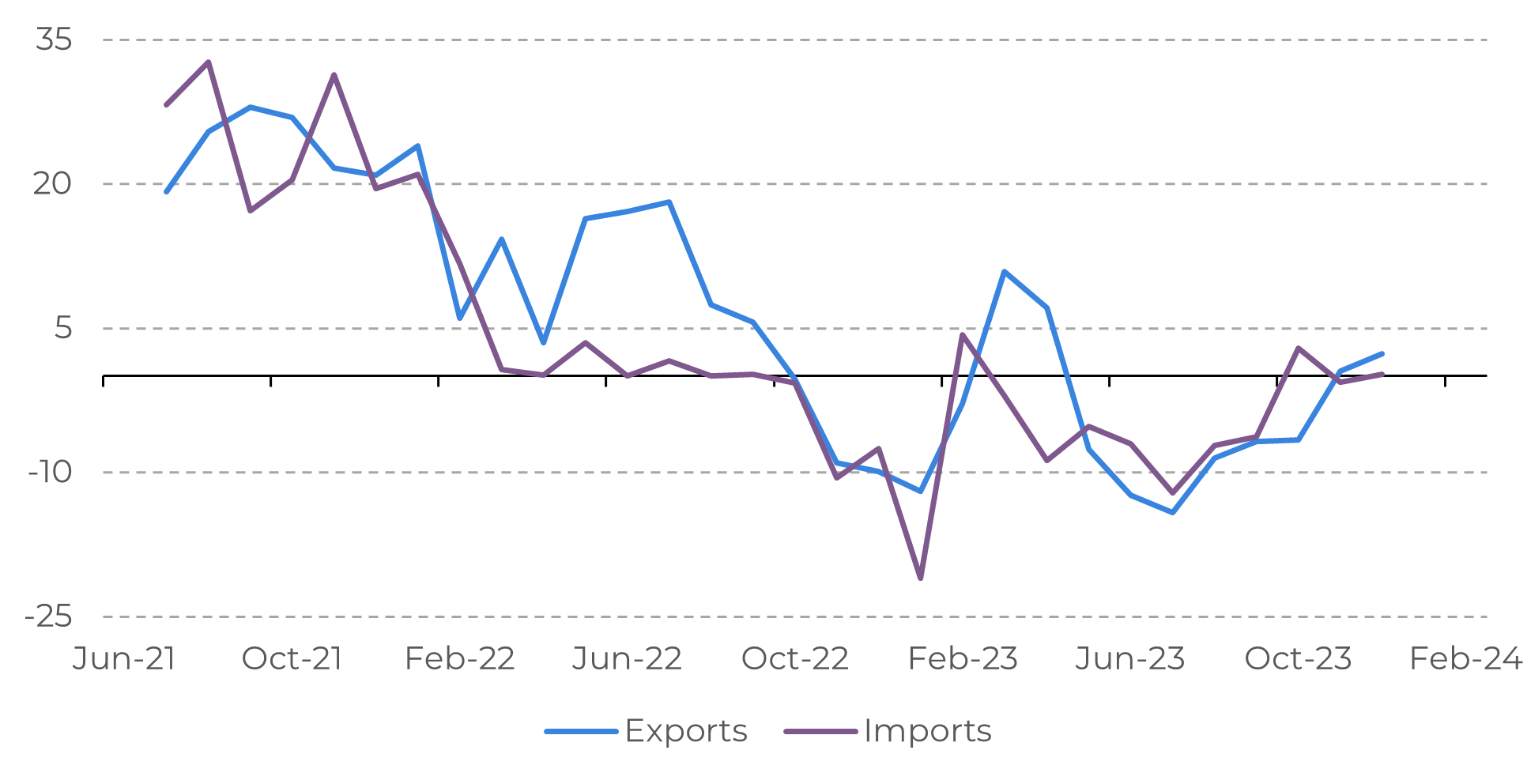

In this sense, the country is expected to adopt stronger stimuli, both in its monetary policy, by cutting interest rates, and in fiscal policy, with stimuli aimed at sectors of the economy, especially real estate. Without economic support from Beijing, 2024 could become a more difficult year for commodities. With lower economic growth and a devalued currency, the country may import fewer inputs, which could affect emerging economies.

Image 4: China - Exports and Imports Year on Year in USD (%)

Source: China Customs

In Summary

Despite more modest economic growth in 2023, China continues to play a crucial role as an important driver of the global markets. Some sectors, such as electric car manufacturing, continue to thrive, as does the service sector, demonstrating the resilience and diversification of the Chinese economy.

Consumer prices in China are falling rapidly, reflecting a lack of confidence in the Asian country's economy. As long as deflation persists, there will be a significant risk to consumption and investment.

China is expected to implement more robust stimulus in 2024, both in its monetary policy, through interest rate cuts, and in fiscal policy, with a focus on specific sectors such as real estate.

Weekly Report — Macro

Written by Victor Arduin

victor.arduin@hedgepointglobal.com

victor.arduin@hedgepointglobal.com

Reviewed by Alef Dias

alef.dias@hedgepointglobal.com

alef.dias@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.

To continue using the Hedgepoint HUB, please review and accept the updated terms.