Feb 20

/

Victor Arduin

Macroeconomics Weekly Report - 2024 02 20

Back to main blog page

US Inflation Surprise Increases Risk Aversion

- Last week was marked by a rise in US inflation data, which contributed to the strengthening of the US dollar, due to the scenario of greater risk aversion.

- US Treasury bond yields continue to rise, reaching levels not seen since mid-December, when expectations of an interest rate cut in the first quarter of 2024 were gaining momentum.

- These movements can be seen on a broader scale, such as in the commodities market, which reflects a more bearish sentiment due to the stronger dollar and the risks of lower demand in the future.

Introduction

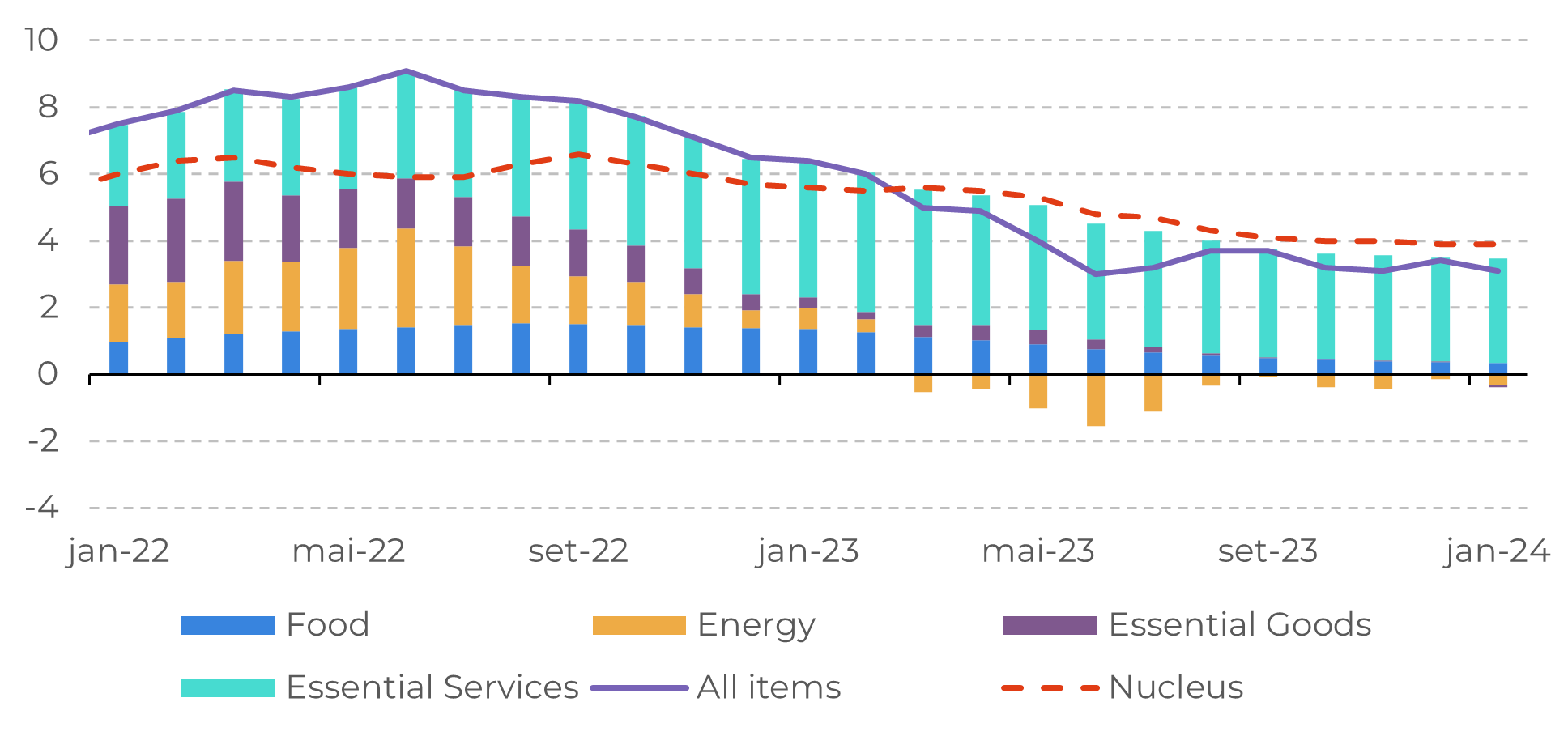

Last week, the US Treasury bond market was in turmoil due to inflation data, which exceeded expectations, increasing risk aversion. The upward surprise, especially in the services sector, reinforces the idea that there is still some way to go to reach the 2% inflation target.

Looking at the macroeconomic scenario, with a resilient labor market and strong economic activity, there is a growing feeling that interest rates will remain high for longer, something that has an impact not only on the US sovereign bond market, but also on the commodities market.

Image 1: USA - Inflation (%)

Source: Bureau of Labor Statistics

Image 2: USA - Yield on US Treasury Notes (%)

Source: Refinitiv

Where are US Treasuries going?

The level of interest rates in the United States has a broad impact on the world economy, as the US dollar is the world's main reserve currency. For this reason, the market is eagerly awaiting interest rate cuts from the Fed. However, positive employment data and the country's recent inflation figures, which registered 3.1% in January, indicate that the economy can live with the current restrictive monetary policy for longer. Therefore, we shouldn't see an easing of borrowing costs before June.

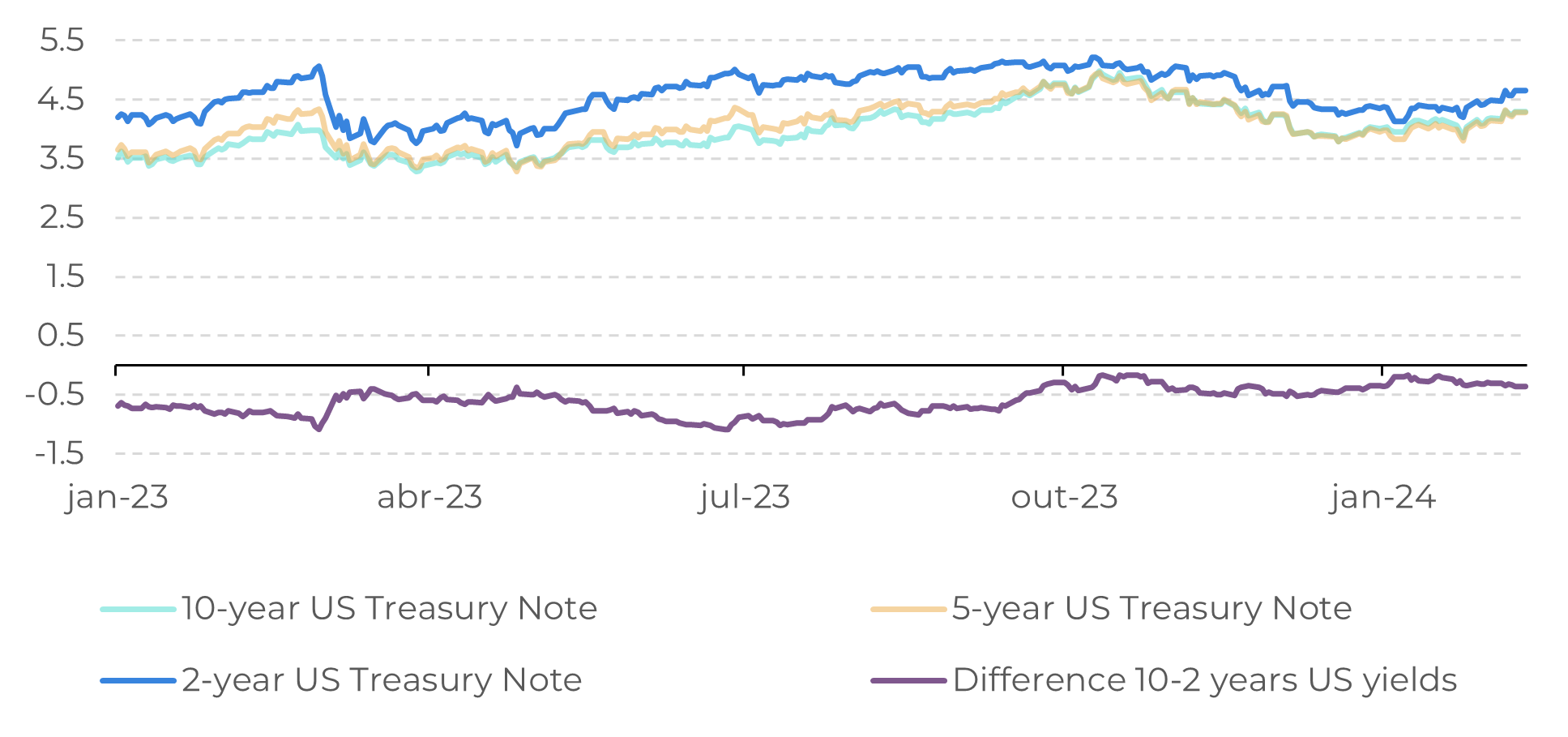

As the market's perception that interest rates will remain high for longer increases, US treasury yields have reacted, gaining strength in recent weeks. For example, the 2-year benchmark (2A T-Note) closed last Friday, February 16, at 4.65%, up 0.16 (+3.74%). This level hasn't been seen since mid-December, when many market bets took an interest rate cut in March 2024 for granted.

Image 3: DXY Index

Source: Refinitiv

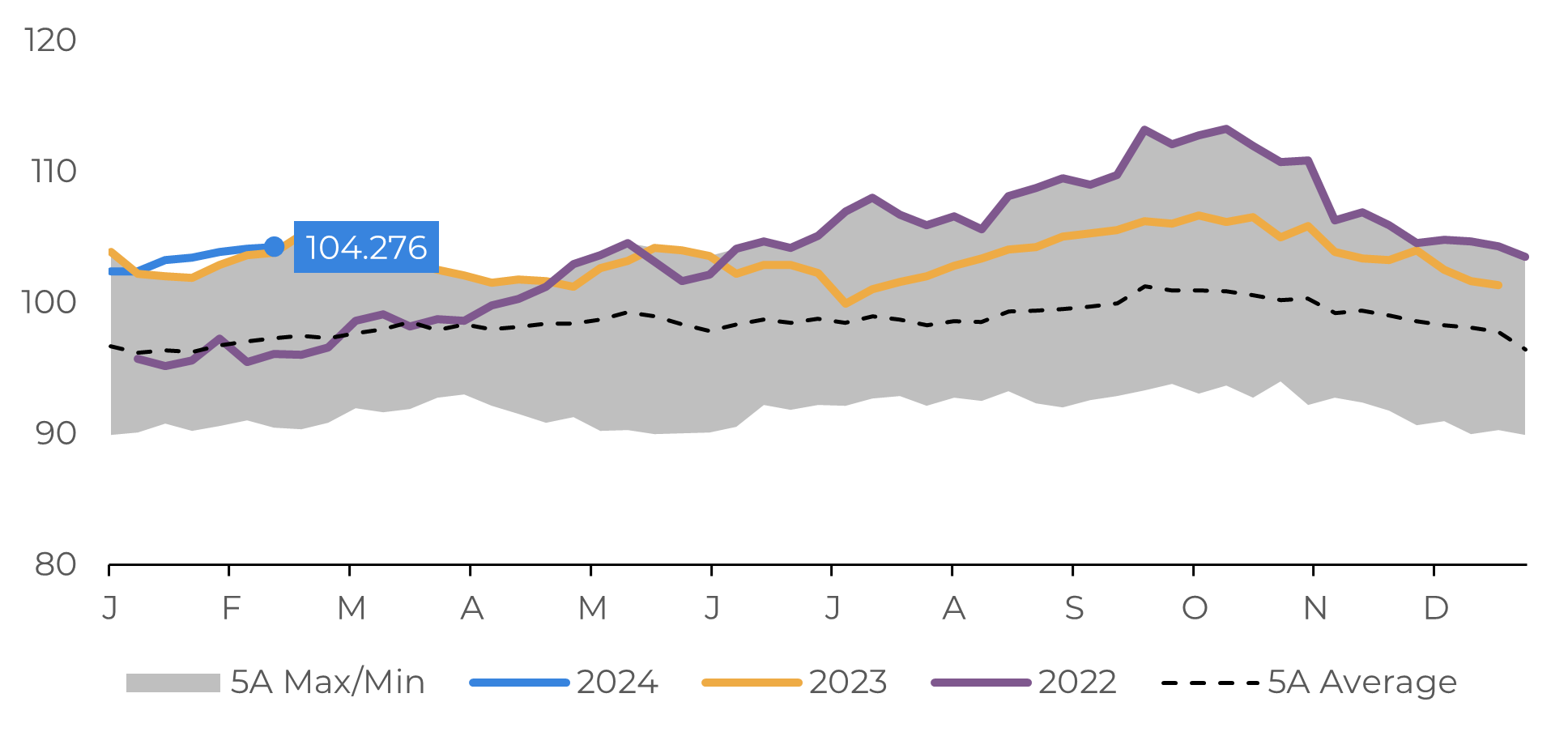

If, on the one hand, high interest rates in the world's largest economy are worrying because they make it difficult to access credit and reduce consumption, they are also worrying emerging countries and making them apprehensive, especially commodity exporters. As these products are generally traded in dollars, the strengthening of the American currency makes them more expensive, resulting in downward pressure on this market

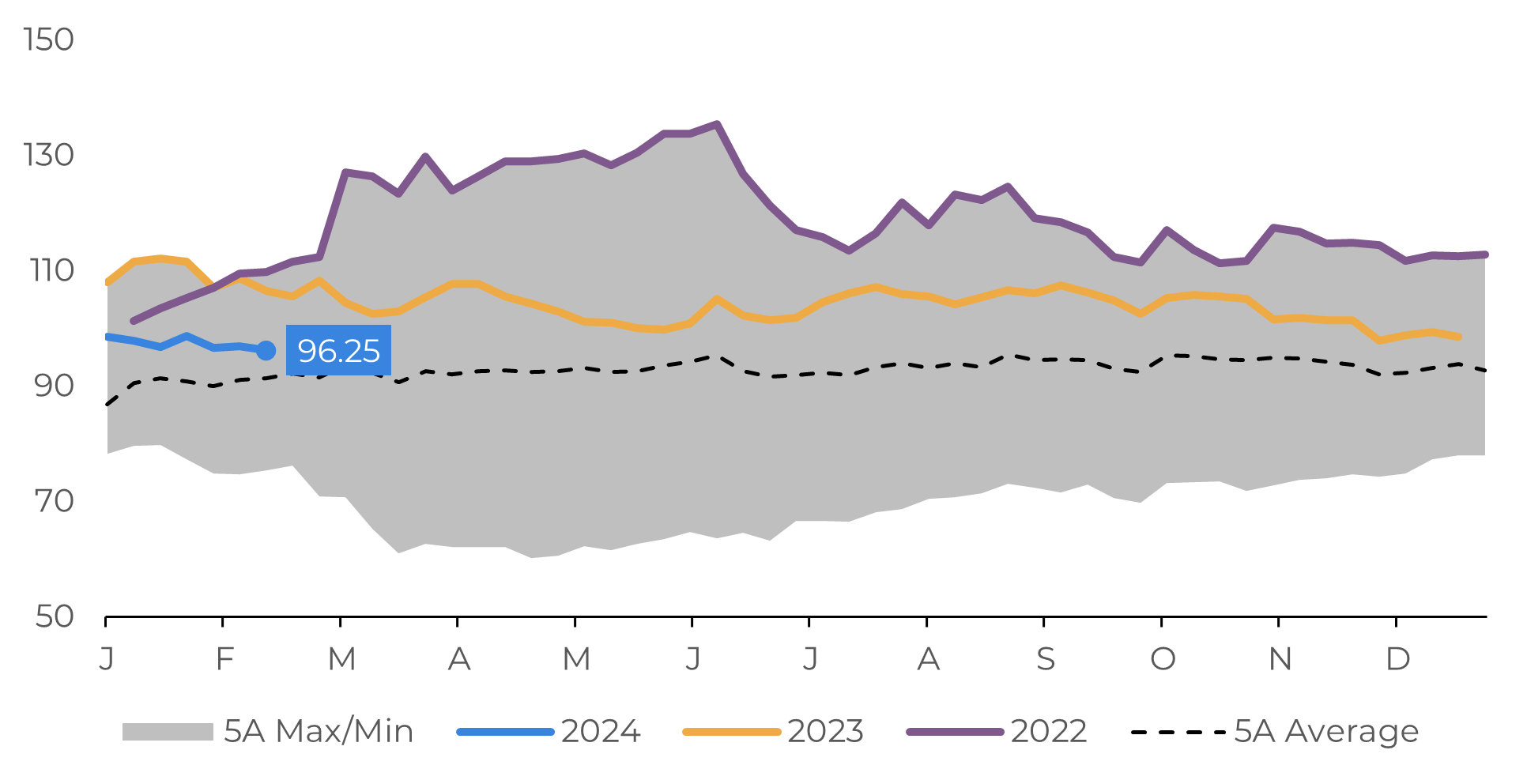

The influence of market movements can be seen in the DXY, an index that tracks the performance of the dollar, which is up 2.96% (+2.92%) so far in 2024, and the BBG Commodities, an index that monitors the appreciation or devaluation of commodities, which is down 2.39% (-2.43%) this year. Thus, much of the ground gained by commodities since the end of last year is being lost, reflecting higher interest rates for a longer period than initially forecast.

The influence of market movements can be seen in the DXY, an index that tracks the performance of the dollar, which is up 2.96% (+2.92%) so far in 2024, and the BBG Commodities, an index that monitors the appreciation or devaluation of commodities, which is down 2.39% (-2.43%) this year. Thus, much of the ground gained by commodities since the end of last year is being lost, reflecting higher interest rates for a longer period than initially forecast.

Image 4: BBG Commodities Index

Source: Refinitiv

In Summary

The interest rate cut in the United States will take place sooner or later this year, but robust data from the American economy is delaying this initial move.

As the Fed fails to reduce the country's borrowing costs, the premiums on US treasury bonds are rising, as are the fundamentals of the stronger dollar against other currencies.

Meanwhile, commodities continue to face an adverse scenario, marked by the strength of the US dollar, reduced demand and the risk of recession, although the latter is much reduced, it still persists amid a very restrictive monetary scenario.

Weekly Report — Macro

Written by Victor Arduin

victor.arduin@hedgepointglobal.com

victor.arduin@hedgepointglobal.com

Reviewed by Alef Dias

alef.dias@hedgepointglobal.com

alef.dias@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.