Mar 11

/

Alef Dias

Macroeconomics Weekly Report - 2024 03 12

Back to main blog page

China shows signs of recovery

- Significant challenges have been present for the Chinese economy. However, recent developments have improved the outlook for the Chinese economy.

- China's CPI rose 0.7% year-on-year, breaking a four-month streak of declines. The reading was above market expectations of a 0.3% increase.

- Chinese Premier Li Qiang's first budget indicated a strong commitment to growth. The 5% target for 2024 sets a high bar, given a more challenging base than last year - and achieving it will require more stimulus.

- Export growth accelerated to 7.1% YoY in January-February, compared to 2.3% in December, coming in above the consensus estimate (1.9%). Imports, meanwhile, grew 3.5% YoY in the two-month period, following a 0.2% increase in December, beating the consensus forecast (2.0%).

- However, many of the challenges to Chinese economic growth remain, requiring a certain amount of caution

Introduction

Significant challenges have arisen for the Chinese economy. The real estate sector is weak, with less and less stimulus, youth unemployment has risen, the currency has depreciated sharply in the last year and the deflationary scenario has added further risks to Chinese economic activity.

However, recent developments have improved the outlook for the Chinese economy. Based on this new data, we will update our view of China and its possible impacts on commodities.

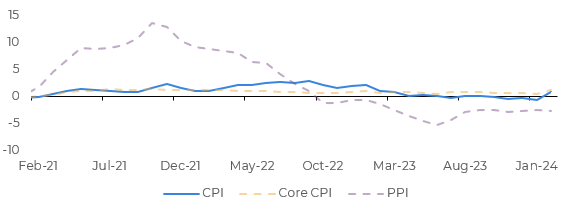

Country returns to inflation, but deflationary risk persists

China's CPI rose 0.7% YoY, breaking a four-month streak of declines. The reading was above market expectations of a 0.3% increase. On a monthly basis, the CPI rose 1.0%.

Slower deflation in food prices was the main factor behind the rise in the CPI. The fall in food prices slowed to -0.9% year-on-year, from -5.9% in January. Demand related to the Lunar New Year holiday probably gave these prices a boost.

Higher travel prices - probably driven by holiday demand - were another important reason. These prices rose 23.1% YoY, accelerating from the 1.8% increase recorded in January. Adverse weather, with freezing rain in central China in mid-February, also fueled upward pressure on food and travel prices.

Despite the positive result for economic activity, the factors that led to the end of deflation are temporary. The producer price index, which tends to be much less affected by the Lunar New Year holidays, fell by 2.7% YoY, more than the 2.5% drop in January. This was larger than the consensus estimate of a 2.5% drop.

Image 1: Consumer and Producer Price Indexes - China (%)

Source: National Bureau of Statistics of China

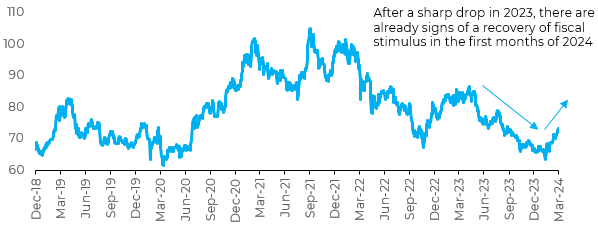

Growth target shows commitment to economic activity, but fiscal policy is challenging

Chinese Premier Li Qiang's first budget indicated a strong commitment to growth. The 5% target for 2024 sets a high bar, given a more challenging base than last year - and achieving it will require more stimulus.

However, the stronger than expected budget deficit is consistent with the ambitious target. The target is considerably higher than the consensus projection that the Chinese economy will expand by 4.5%. It is also higher than the potential growth for the year, estimated at 4.9%.

The government has set the broad fiscal budget deficit at 8.96 trillion yuan, or 6.6% of GDP. This includes a deficit of 4.06 trillion yuan (3.0% of GDP) in the general budget, 1 trillion yuan in special bond issues by the central government and 3.9 trillion yuan in special bonds by the local government. This figure is higher than last year's original budget deficit, which was set at 5.9%.

In 2023, local governments delayed spending, impacting growth. The risk is that this will happen again this year. Restrictions on the expansion of local government debt could prevent projects from being carried out, as the corresponding local resources are usually needed for large projects.

In 2023, local governments delayed spending, impacting growth. The risk is that this will happen again this year. Restrictions on the expansion of local government debt could prevent projects from being carried out, as the corresponding local resources are usually needed for large projects.

The strength of private sector confidence will also determine the effectiveness of fiscal policy. Unless there is a change in sentiment, private investment will be slow - and the government alone cannot generate a lasting recovery.

Image 2: GS Fiscal Stimulus Index - China

Source: Bloomberg

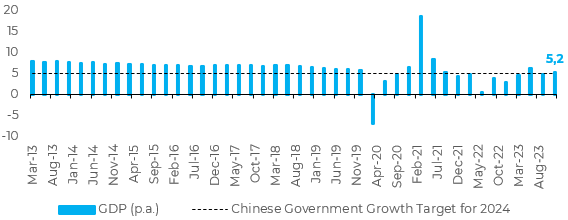

Image 3: GDP – China (%, YoY)

Source: Refinitiv

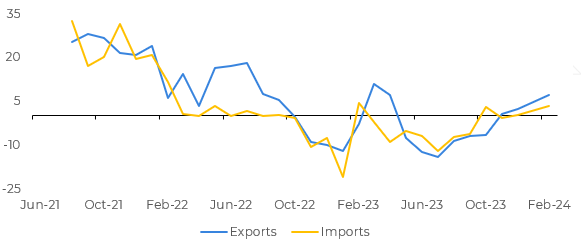

External sector has solid results, showing recovery ahead of 2023

Export growth accelerated to 7.1% year-on-year in January-February, compared to 2.3% in December, coming in above the consensus estimate (1.9%). The increase in export growth partly reflected the effects of the statistical base. In the same period last year, shipments fell by 8.4%, before recovering with growth of 10.9% in March.

Even so, the MoM downturn in exports - due to the Lunar New Year interruptions - was less than the typical seasonal drop. However, the first indicators of foreign demand point to a weak picture for the beginning of 2024.

Even so, the MoM downturn in exports - due to the Lunar New Year interruptions - was less than the typical seasonal drop. However, the first indicators of foreign demand point to a weak picture for the beginning of 2024.

Manufacturing PMIs from the US (ISM), the euro zone and Japan signaled deeper contractions in February, after brief recoveries in January. An indicator of new export orders in China's official manufacturing PMI also showed a deeper contraction in February.

Imports grew by 3.5% year-on-year in the two-month period, following a 0.2% increase in December, beating the consensus forecast (2.0%). Imports fell by 5.5% in 2023, although the last quarter was firmer, with an increase of 0.8%.

Import growth also benefited from more favorable base effects. More data is needed in the coming months to assess whether the recent stimulus is feeding the economy and increasing demand in a sustainable way.

Looking at grain demand, the data remains positive. Accumulated corn imports for the 23/24 harvest are at their highest levels in recent years, while data from Refinitiv shows that China's wheat imports in February reached their highest monthly level in five years.

However, demand for soybeans has not shown the same strength. China's soybean imports in January-February fell 8.8% YoY to 13.04M mt, according to preliminary data released by the country's General Administration of Customs (GACC). This is the lowest level seen for the period in five years.

Image 4: Exports and Imports - China (%, YoY)

Source: China Customs

In Summary

Recent data has brought more optimism about the Chinese economy. The country has left deflationary territory - at least for now. The government has set ambitious fiscal targets for 2024 and the first foreign trade results for the year were positive.

However, many of the challenges to China's economic growth remain, requiring a certain amount of caution - executing the fiscal deficit and restoring the confidence of the private sector are key to a sustainable change in the outlook for the Chinese economy.

However, many of the challenges to China's economic growth remain, requiring a certain amount of caution - executing the fiscal deficit and restoring the confidence of the private sector are key to a sustainable change in the outlook for the Chinese economy.

Looking at the grain and oilseed markets, demand for corn and especially wheat continues to heat up while soybean imports have been falling amid higher stocks and slower crushing, following weak demand for meal.

Weekly Report — Macro

Written by Alef Dias

alef.dias@hedgepointglobal.com

alef.dias@hedgepointglobal.com

Reviewed by Victor Arduin

victor.arduin@hedgepointglobal.com

victor.arduin@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by hEDGEpoint Global Markets LLC and its affiliates ("HPGM") exclusively for informational and instructional purposes, without the purpose of creating obligations or commitments with third parties, and is not intended to promote an offer, or solicitation of an offer, to sell or buy any securities or investment products. HPGM and its associates expressly disclaim any use of the information contained herein that may result in direct or indirect damage of any kind. If you have any questions that are not resolved in the first instance of contact with the client (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ouvidoria@hedgepointglobal.com) or 0800-878-8408 (for clients in Brazil only).

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.