Dec 20

/

Victor Arduin

Fed decision reinforces cautious outlook for commodities in 2025

Back to main blog page

Fed decision reinforces cautious outlook for commodities in 2025

- Over the course of 2024, US inflation corrected enough for the Fed to begin easing its monetary policy, with the first cut of 50 basis points occurring in September, followed by two more cuts of 25 basis points in November and December.

- However, in its latest statement, the Fed noted the slower progress in the price reduction dynamic in the US and the perception of a more uncertain scenario for 2025 due to protectionist trade policies. Thus, the Fed adopted a more hawkish stance at its last meeting, signaling a high interest rate

- Considering the dollar's impact on the global economy, today's report will examine key concerns of US monetary authorities and provide an outlook for the upcoming months.

Introduction

Last month, the US Federal Reserve reduced interest rates by 50 basis points, reflecting growing concerns about the American labor market. Given the Fed's dual mandate, which aims to maintain price stability and support full employment, this move underscores the balancing act between controlling inflation and ensuring robust employment levels.

However, the latest payroll data came in 100,000 jobs above expectations. If, on the one hand, this is good news, as it reduces the chances of a hard landing (a scenario in which the recent restrictive monetary policy could lead the economy into recession), on the other hand, it affects market expectations, which are now predicting a slower pace of interest rate cuts in the current cycle.

Due to the influence of US interest rates on the dollar and, consequently, the impact of the US currency on the commodities market, this report will discuss how the weakening of the dollar will not be linear and may experience fluctuations in the coming months.

The country's heated job market still raises concerns

The US central bank, unlike other countries, has a dual mandate: to simultaneously pursue the inflation target and full employment. After a period with the highest interest rates in the last 20 years, one of the concerns of the monetary authorities is the impact on the labor market, which has so far proved to be quite resilient. Although in recent months some labor market indicators have shown signs of slowing down, the unemployment rate, at 4.2%, remains below the levels seen for most of the past decade.

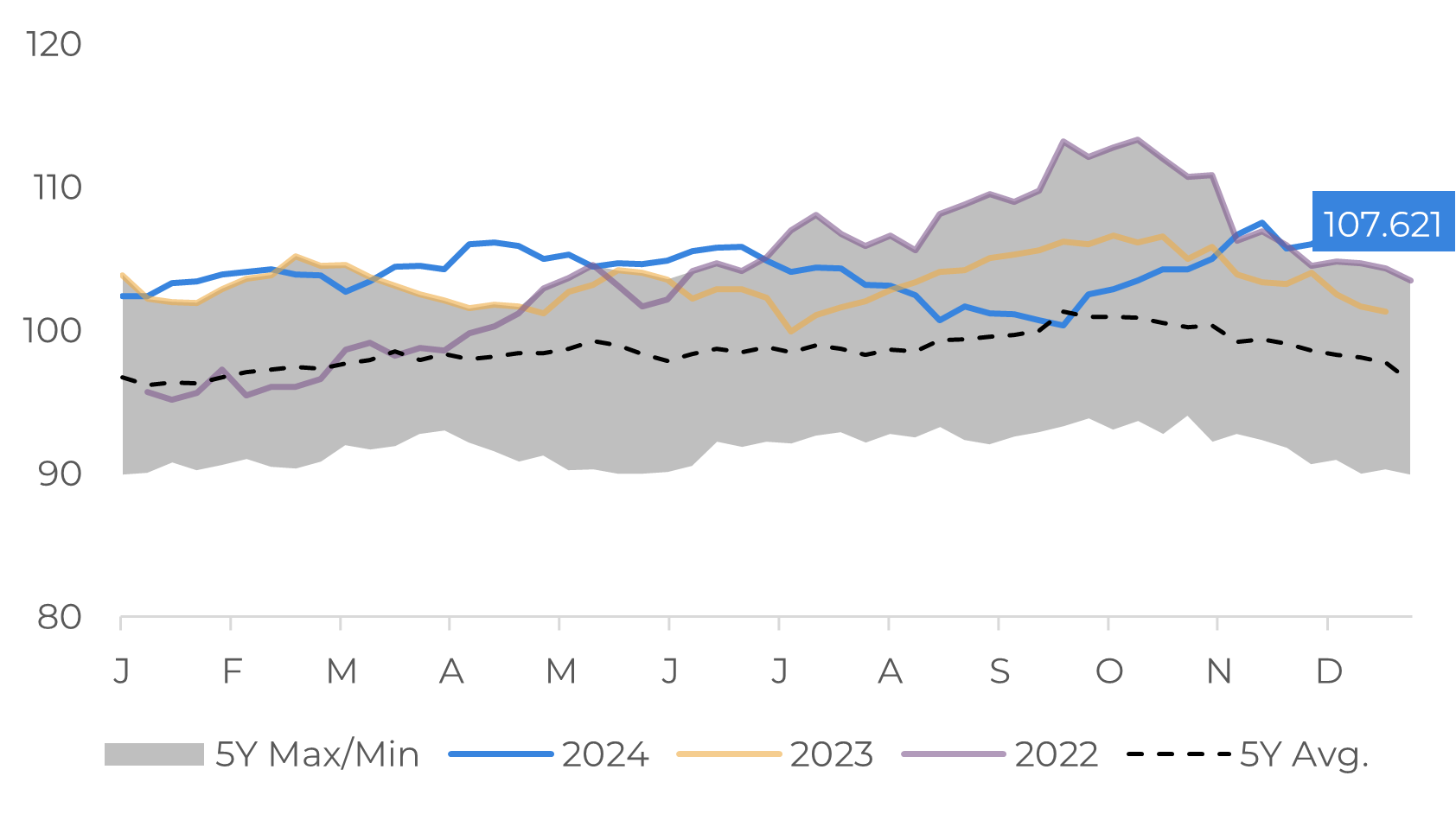

The new Trump administration starting in 2025, with expected policies to stimulate economic activity in the US and the application of tariffs against countries like China and Mexico, could result in a higher inflation environment next year. Because of this, the market has priced in the maintenance of high interest rates for longer into 2025, which has given support to the dollar with DXY surpassing the 108-point mark this week. Another important factor in the market is a possible worsening in the US fiscal deficit if tax cuts are confirmed in the country, which would require the US Treasury to pay higher yields to attract investors.

Image 1: Dollar Index (DXY)

Source: Refinitiv

Current scenario brings adversity for the commodities market in 2025

The dollar is the main reference for commodities around the world. When it rises in value, it tends to make products more expensive for countries whose currencies are devalued against it. This movement has a direct impact on global trade, especially in a scenario of higher tariffs in the US, which could hinder international trade and slow down the world economy.

Energy commodities, for example, are among the most sensitive to these factors due to their strong correlation with the macroeconomic scenario. Although specific fundamentals of the energy market point to caution - such as the reduction in Chinese imports in 2024 and the expectation of greater supply from non-OPEC countries - uncertainties about the trajectory of US interest rates adds to the bearish tone.

For emerging countries, the scenario is even more challenging. Many currencies around the world are facing a sharp devaluation, which could intensify inflation and put pressure on central banks to raise interest rates. In Brazil, for example, the basic interest rate was recently raised by 1 basis point to 12.25%. In addition, the Central Bank has signaled two more hikes of the same magnitude in the first quarter of 2025.

These global and regional dynamics illustrate the challenges that lie ahead for markets and economies in the coming year. The balance between restrictive monetary policies, exchange rate volatility and the global economic recovery will be crucial in determining the pace of growth and the stability of the commodities markets.

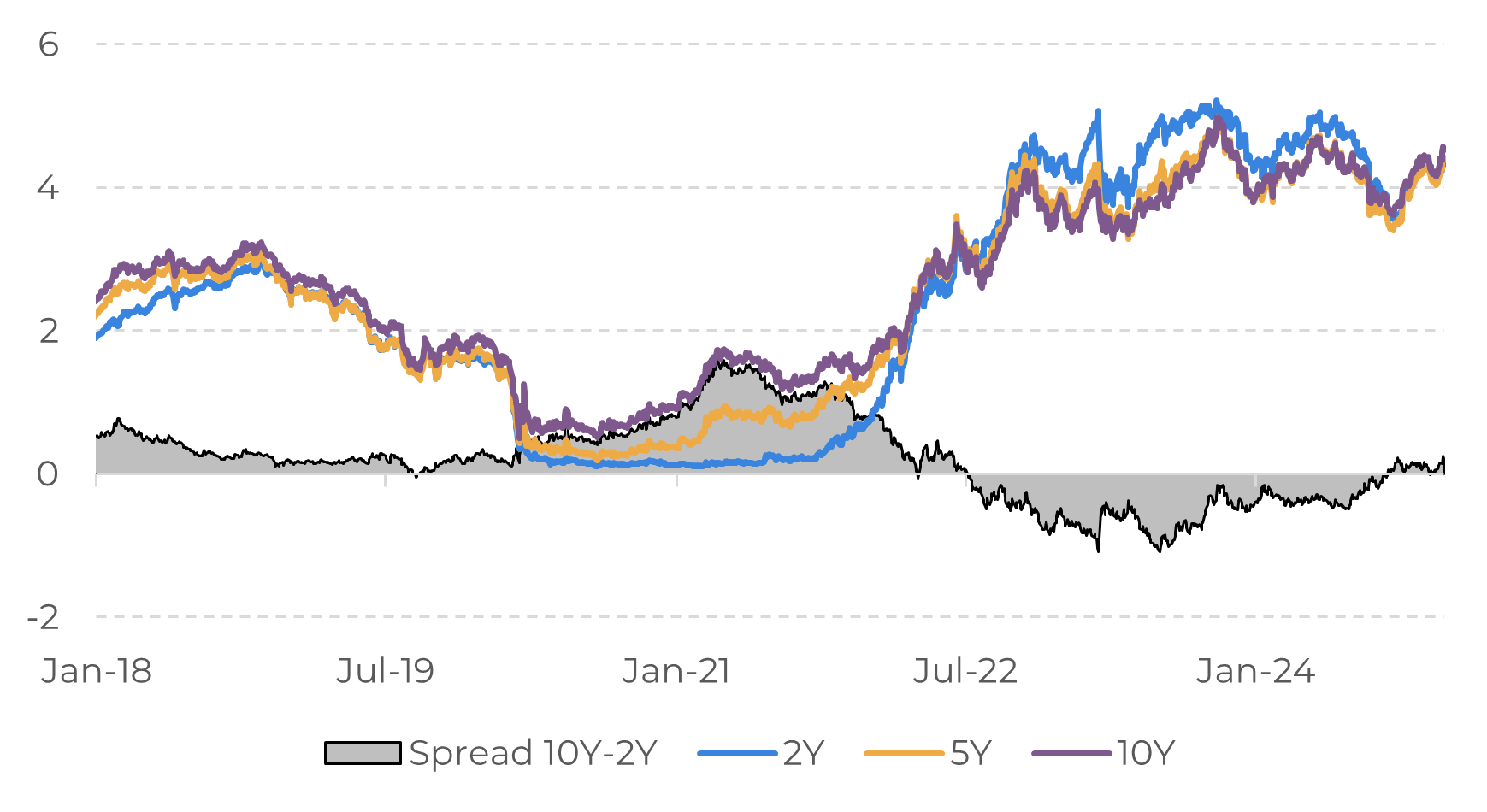

US – Treasury Yield (%)

Source: Refinitiv

Summary

Historically low unemployment data and above-target inflation (2.7% against 2%) suggest medium-term inflationary pressure, forcing the Fed to balance interest rate cuts with containing inflation. Expectations surrounding Donald Trump's administration could make a tariff war more realistic, putting pressure on prices.

In the short term, the US interest rate cut has a minimal impact on Brazil but could put pressure on the real due to the greater flow of funds to the US. Globally, the US has a more solid outlook compared to Europe, Latin America and Asia, making pressure on the USD against global currencies a long-term trend.

Written by Guilhermo Marques

victor.arduin@hedgepointglobal.com

victor.arduin@hedgepointglobal.com

Reviewed by Livea Coda

livea.coda@hedgepointglobal.com

livea.coda@hedgepointglobal.com

www.hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Global Markets LLC and its affiliates (“HPGM”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint Commodities LLC (“HPC”), a wholly owned entity of HPGM, is an Introducing Broker and a registered member of the National Futures Association. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and outside advisors before entering in any transaction that are introduced by the firm. HPGM and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. In case of questions not resolved by the first instance of customer contact (client.services@hedgepointglobal.com), please contact our internal ombudsman channel (ombudsman@hedgepointglobal.com) or 0800-878- 8408/ouvidoria@hedgepointglobal.com (only for customers in Brazil).

To access this report, you need to be a subscriber.

Contact us

hedgepointhub.support@hedgepointglobal.com

ouvidoria@hedgepointglobal.com

Funchal Street, 418, 18º floor - Vila Olímpia São Paulo, SP, Brasil

Check our general terms and important notices.

This page has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without the purpose of instituting obligations or commitments to third parties, nor is it intended to promote an offer, or solicitation of an offer of sale or purchase relating to any securities, commodities interests or investment products. Hedgepoint and its associates expressly disclaim any use of the information contained herein that directly or indirectly result in damages or damages of any kind. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests such as futures, options, and swaps involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgement and/or advisors before entering in any transaction.Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately.Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only).Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets.Security note: All contacts with customers and partners are conducted exclusively through our domain @hedgepointglobal.com. Do not accept any information, bills, statements or requests from different domains and pay special attention to any variations in letters or spelling, as they may indicate a fraudulent situation.“HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.

To continue using the Hedgepoint HUB, please review and accept the updated terms.