2026 Q1 Update and Expectations for Q2

Macroeconomic Outlook

2026 Q2 Expectations: A ceasefire between the U.S. and Iran is likely to ease market tensions in the short term by reducing pressure on oil prices and improving risk appetite. This, in turn, could create more room for future interest rate cuts. Still, because the truce may prove temporary and the effects of the energy shock on inflation may persist, the situation would likely continue to call for caution from central banks.

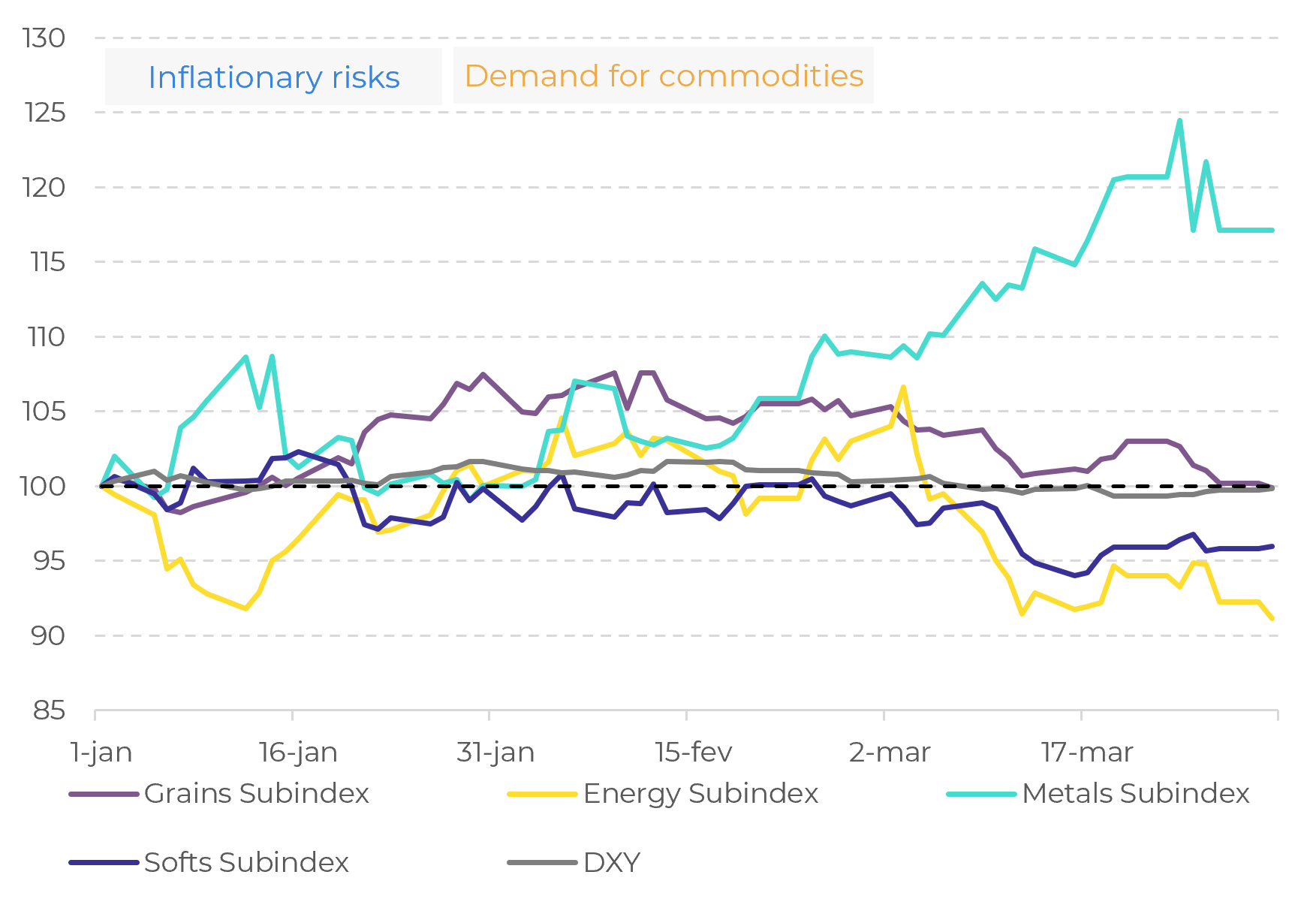

Bloomberg Commodity Subindexes and DXY (Jan26 = 100)

Source: LSEG, Hedgepoint

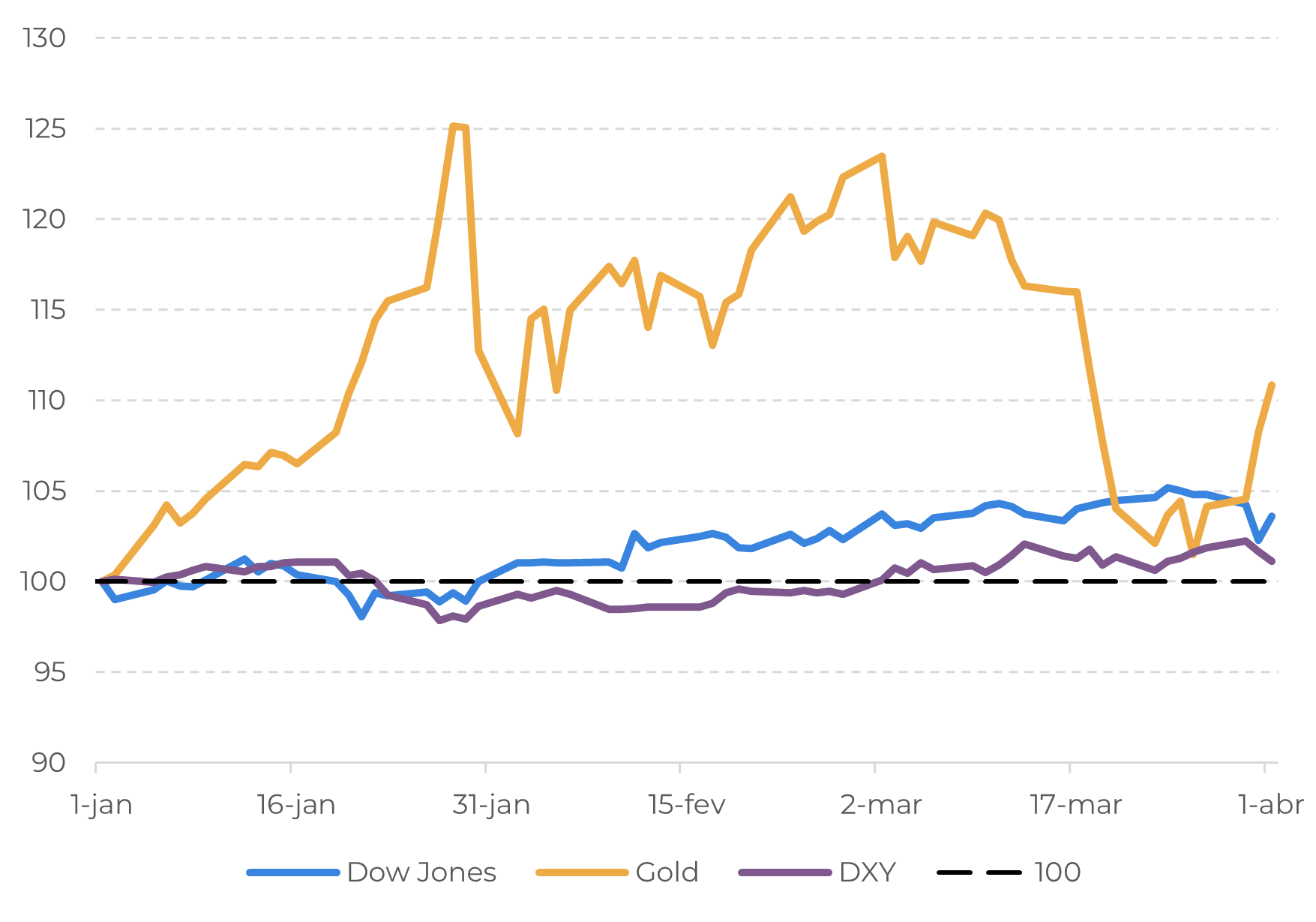

Macro Key Indicators (Jan 26 = 100)

Source: LSEG, Hedgepoint

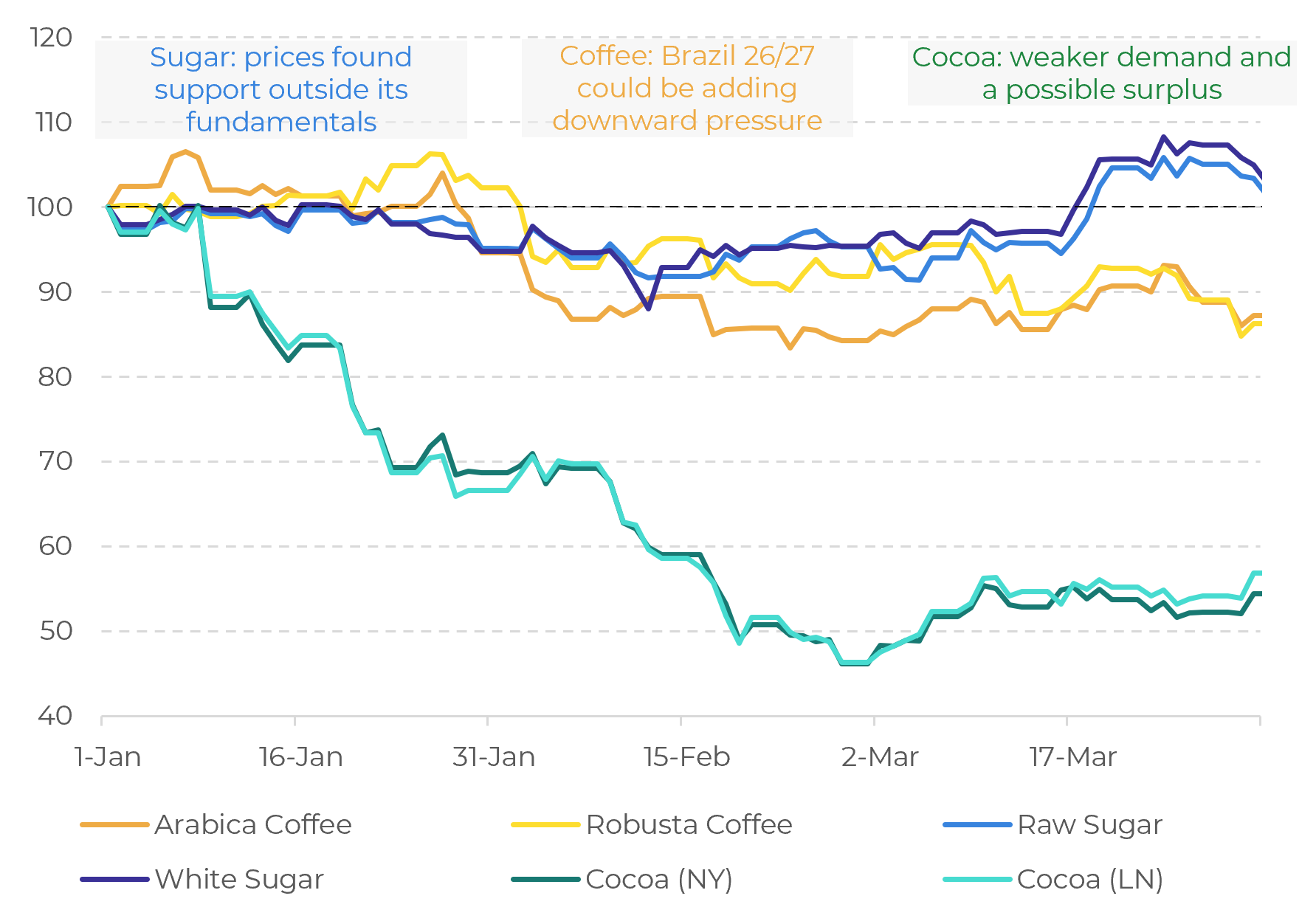

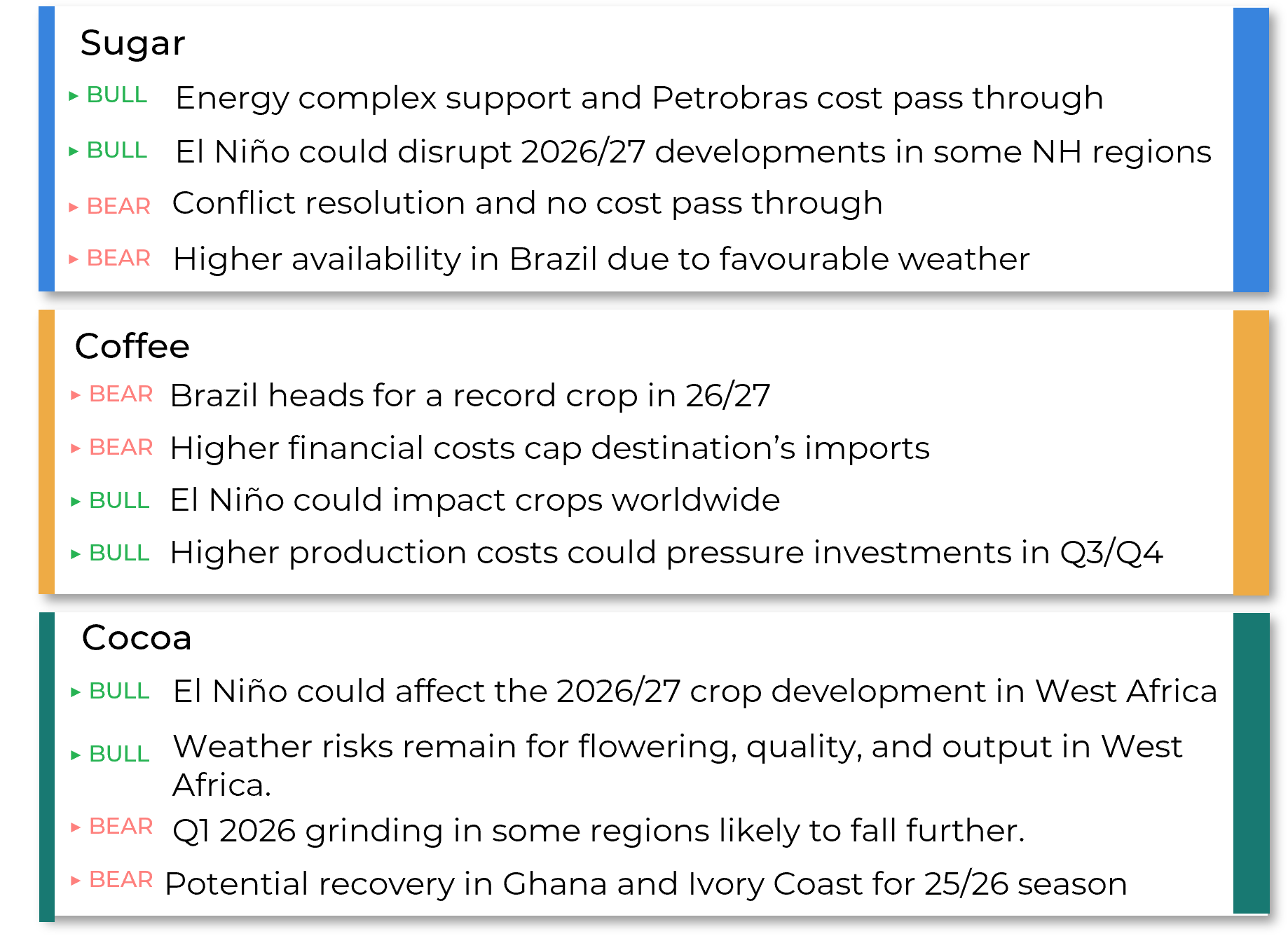

Softs Commodities Outlook

- Sugar: Fundamentals remain bearish due to oversupply; however, prices found support from the energy complex, given its direct link to ethanol and, consequently, Brazil’s sugar mix allocation.

- Coffee: With a record crop in Brazil in 26/27, broader fundamentals are bearish. But the current logistical challenges, rising production and financial costs, and inverted market are capping expected price corrections.

- Cocoa: Cocoa prices have been correcting amid expectations of surplus for the 25/26 crop year and weaker demand.

Softs Price Index (Jan 26 = 100)

Source: LSEG

Key Factors Going Forward

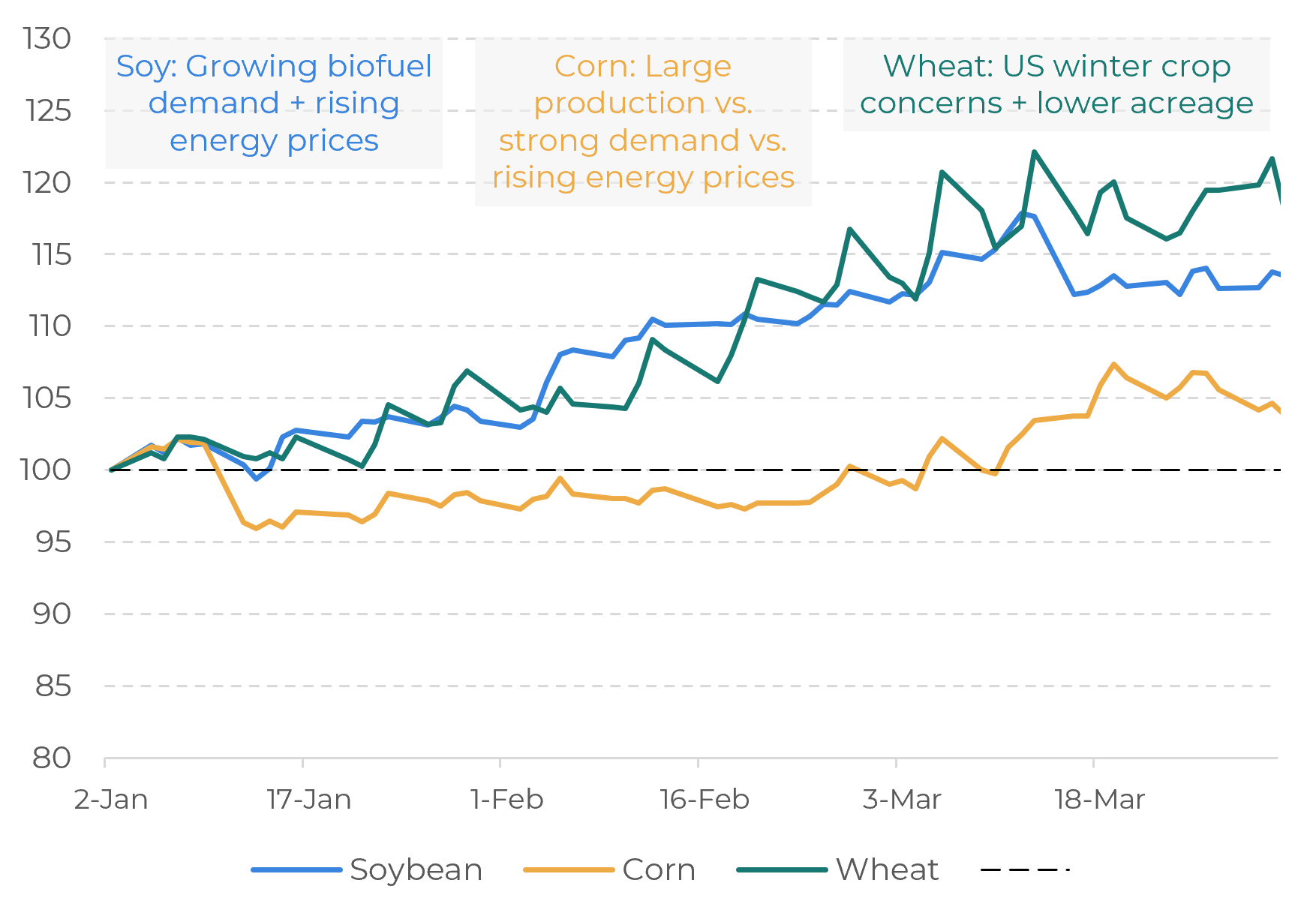

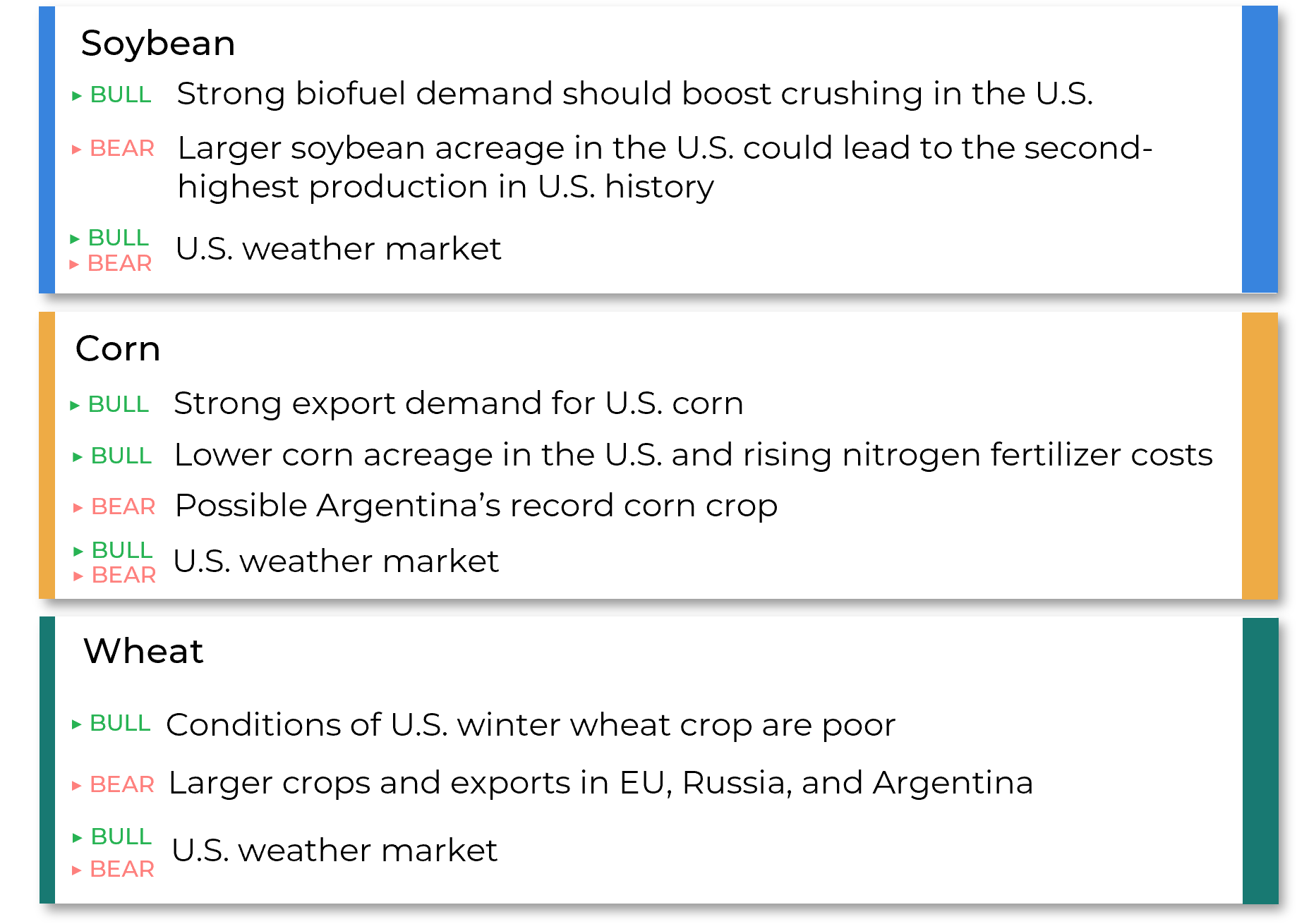

Grains & Oilseeds Outlook

- Soybean: Expectations of increased demand for U.S. soybeans, primarily due to the upcoming increase in biofuel blending, have provided a boost to prices. The outbreak of conflict in the Middle East has provided further support from the energy sector (soybean oil).

- Corn: The market traded sideways for much of the first quarter, as a large supply and a strong demand for exports to the U.S. balanced each other out. The conflict in the Middle East provided a boost starting in March through the energy sector (ethanol).

- Wheat: Concerns regarding the quality of the U.S. winter crop and the trend toward a reduction in planted area in 2026/27 provided support for higher prices in Chicago. The conflict in the Middle East added to the upward momentum.

Grains Price Index (Jan26 = 100)

Source: LSEG

Key Factors Going Forward

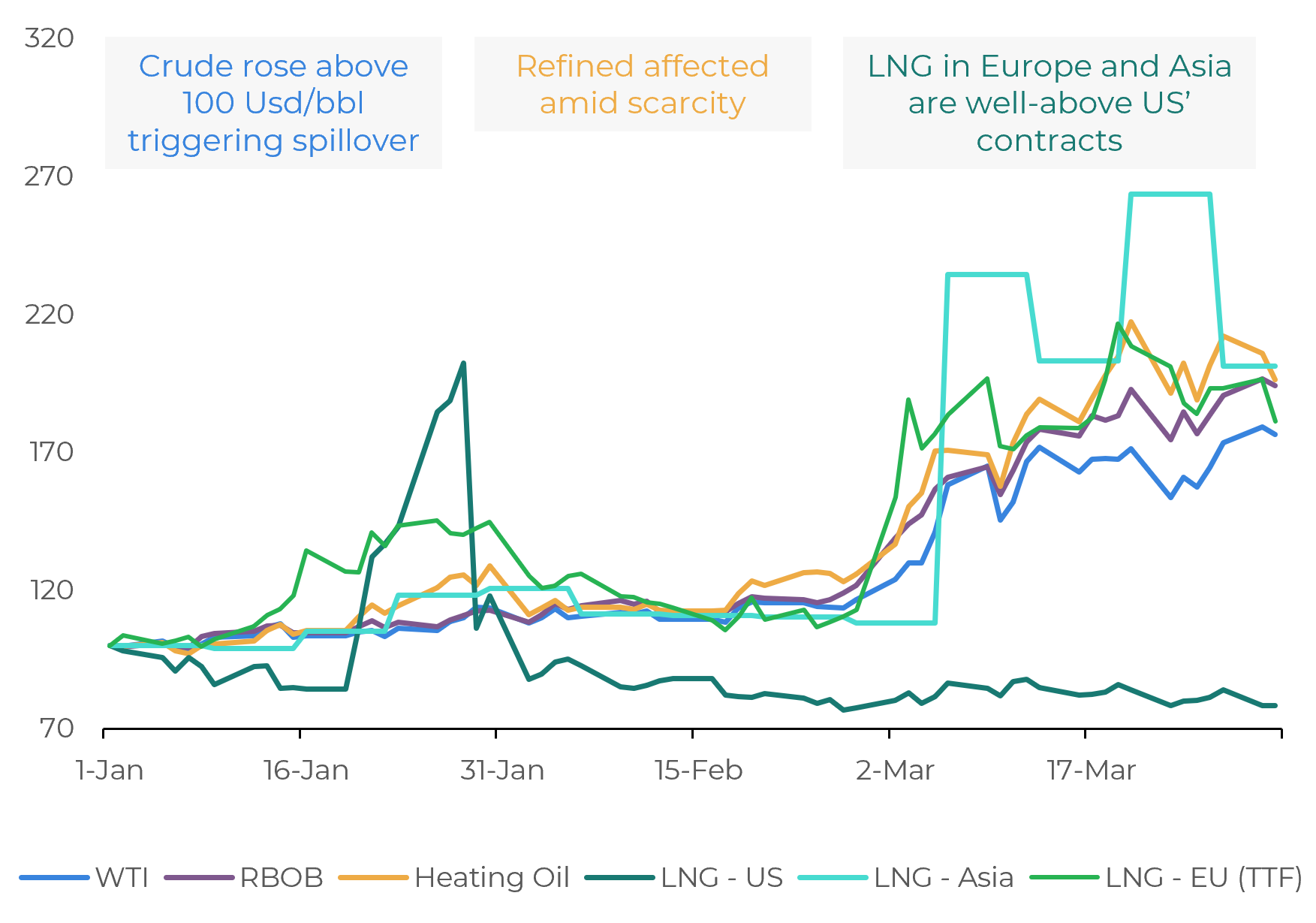

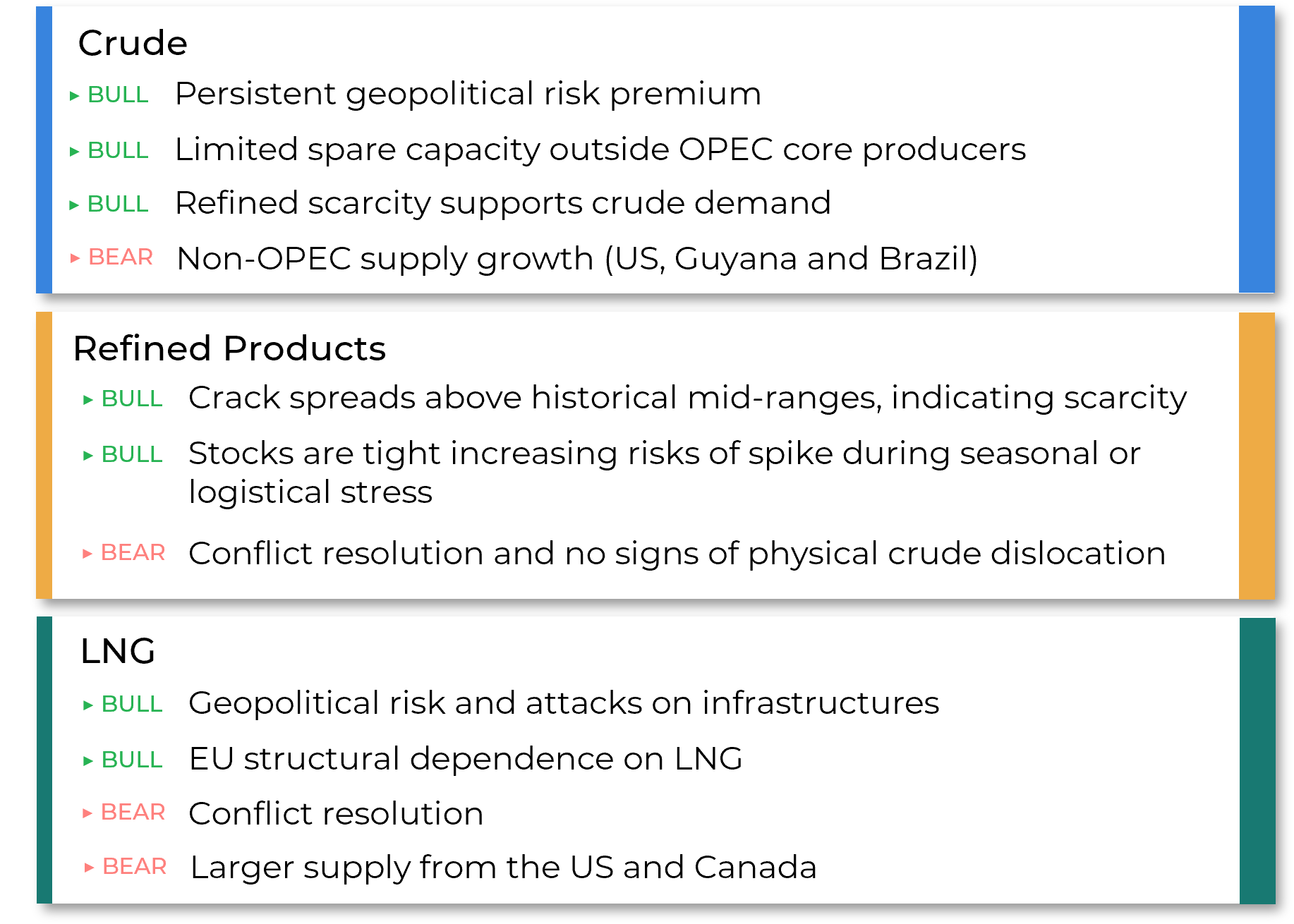

Energy Outlook

- The escalation of the US–Iran conflict sharply disrupted the energy complex from early to late March 2026, as direct attacks on energy infrastructure and shipping routes amplified supply fears.

- The closure of the Strait of Hormuz in early March, which handles about one‑fifth of global oil and LNG flows, supported prices.

- Although strategic reserve releases and temporary easing of sanctions helped smooth some flows, persistent risks around Hormuz kept oil, gas and fuel markets highly volatile through the end of March, embedding a higher geopolitical risk premium across the energy complex

Energy Price Index (Jan26 = 100)

Source: LSEG

Key Factors Going Forward

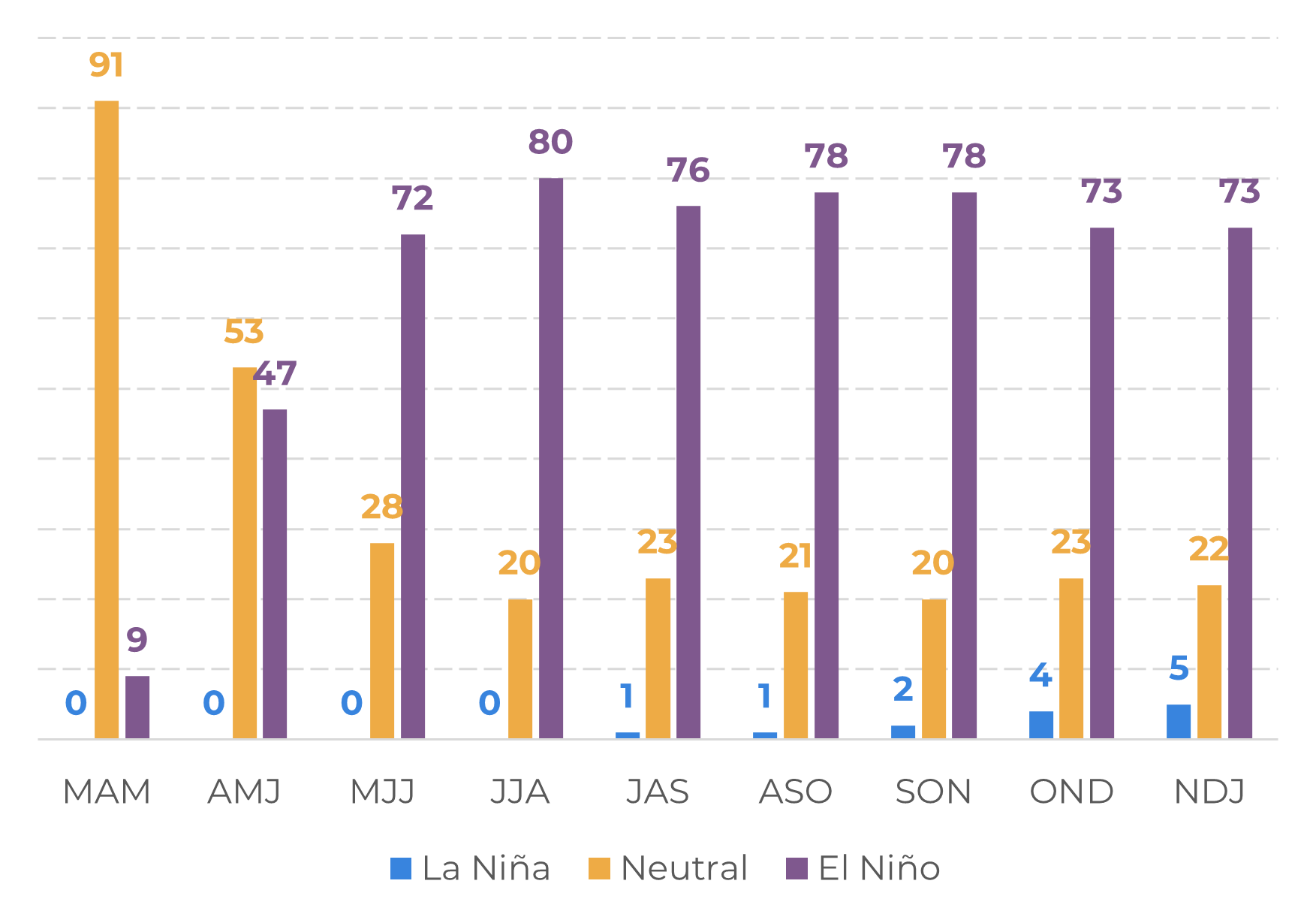

El Niño probability rises

Statistical models point to the end of La Niña in 2026, but an increase in the probability of an El Niño event starting during May-July months. Depending on the phenomenon’s intensity, El Niño tends to reshape global weather patterns, increasing the risk of dry conditions, excessive rainfall, heat waves, and shifts in storm and hurricane activity across key producing regions.

Official IRI ENSO Probabilities (March 2026, %)

Source: International Research Institute for Climate and Society

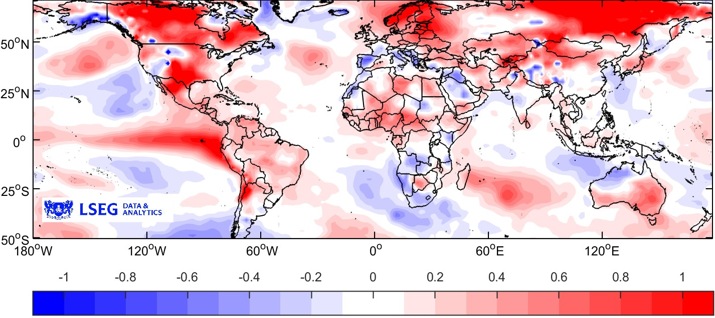

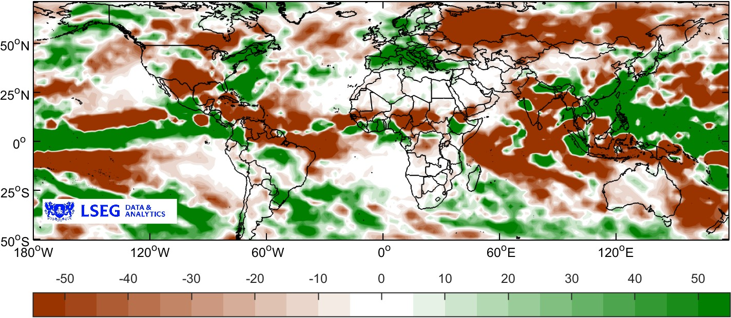

El Niño effects in crops

Higher temperatures and uneven rain

The expected El Niño could bring drier conditions to India, Central Africa, Australia, Southeast Asia, Central America and northern Brazil, while increasing rainfall in Peru, Ecuador, parts of Africa and the Middle East.

As for temperature, heat waves may occur more frequently in South America, the southern US, Africa, Europe, India and Australia.

El Niño Temperature Anomalies | Jun-Aug (ºC)

Source: LSEG

El Niño Precipitation Anomalies | Jun-Aug (mm)

Source: LSEG

Special Report — Multicommodities

thais.italiani@hedgepointglobal.com

luiz.roque@hedgepointglobal.com

livea.coda@hedgepointglobal.com

luiz.roque@hedgepointglobal.com

Disclaimer

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.