2026 Q2 Update and Expectations for Q3

Macroeconomic Outlook

2026 Q3 Expectations: While the ceasefire may ease pressure on oil prices and improve risk appetite, a potential increase in U.S. interest rates typically attracts capital to dollar and puts pressure on emerging market currencies. Markets and central banks should continue to closely monitor inflation trends when shaping future monetary policy decisions.

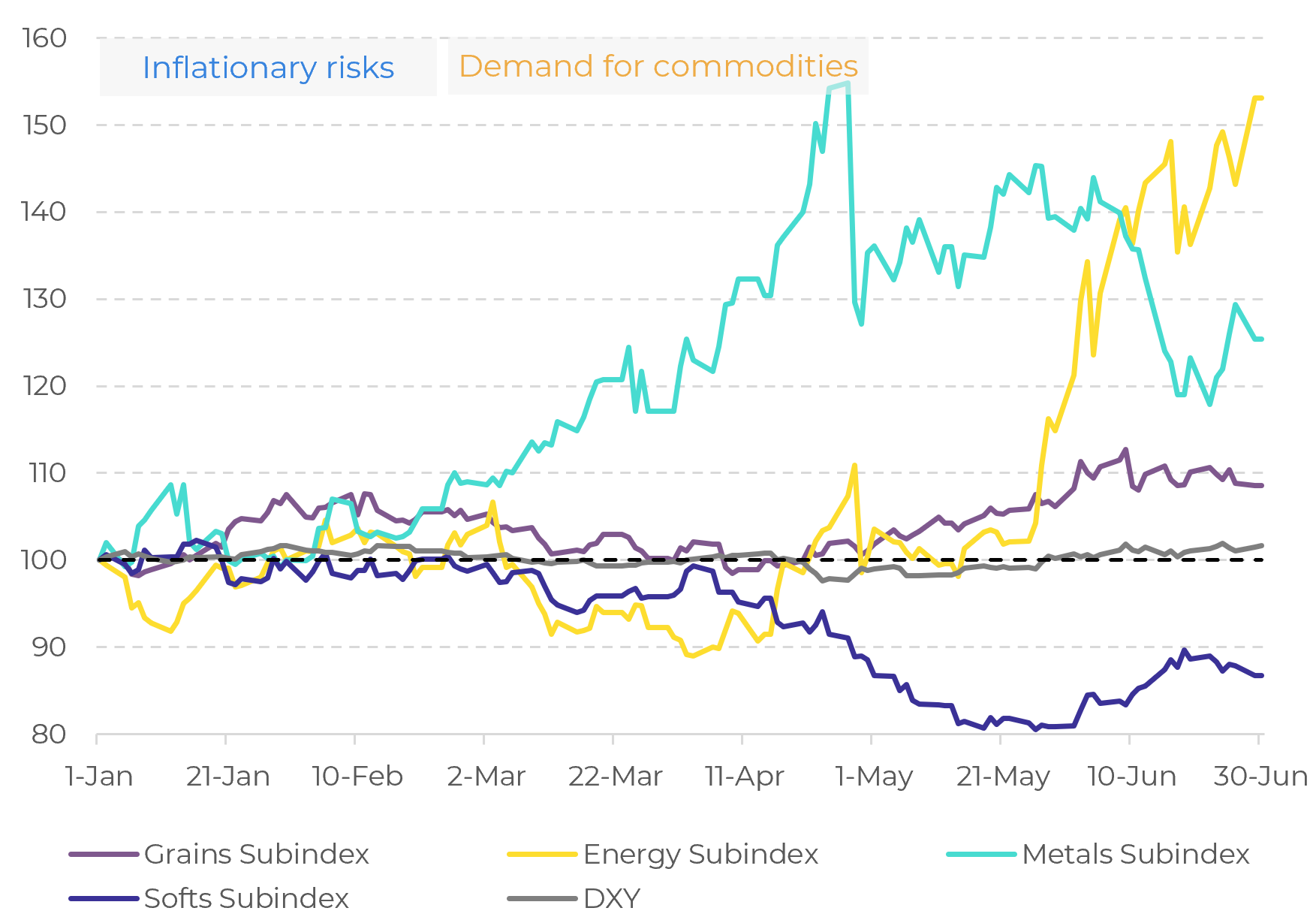

Bloomberg Commodity Subindexes and DXY (Jan26 = 100)

Source: LSEG, Hedgepoint

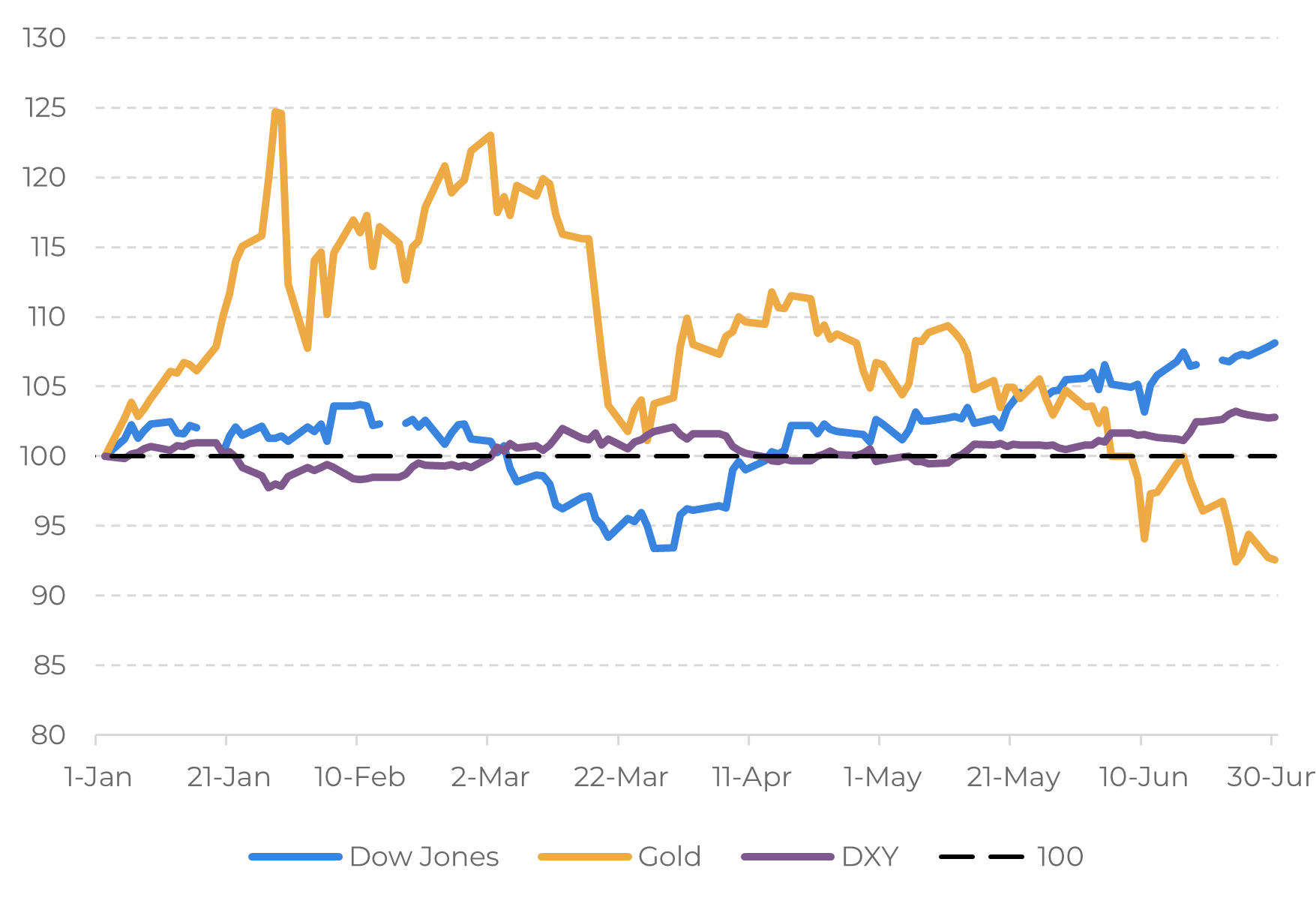

Macro Key Indicators (Jan 26 = 100)

Source: LSEG, Hedgepoint

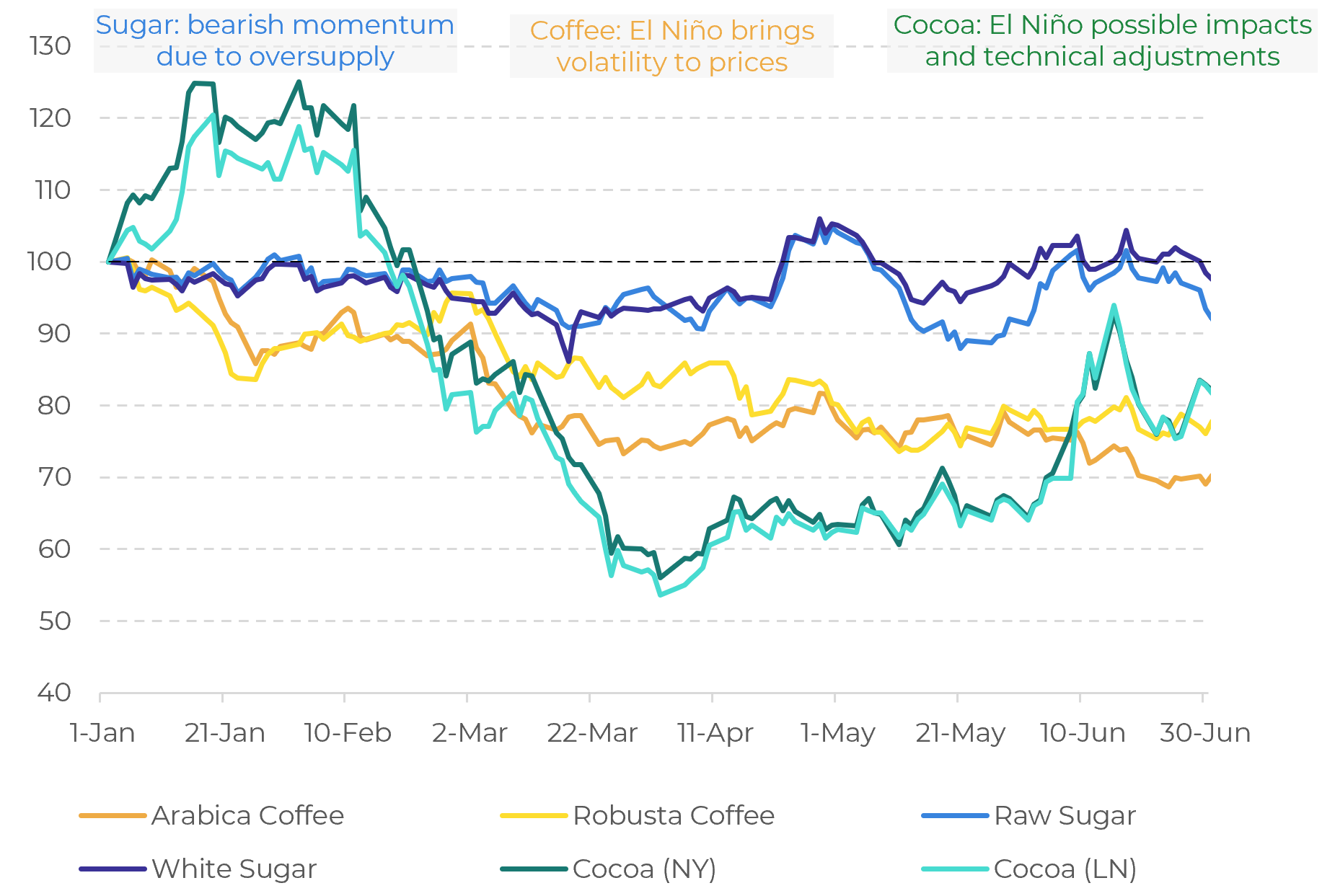

Softs Commodities Outlook

- Sugar: Brazil’s strong 26/27 Center-South season (Apr-Mar) has pushed sugar prices to their lowest levels since 2020. Looking ahead, weather-related risks could tighten supply in the Northern Hemisphere during the 26/27 season (Oct-Sep), providing medium-term support to prices and boosting the white sugar premium.

- Coffee: With a record 26/27 coffee crop in Brazil, broader fundamentals are bearish. However, low stocks in destinations, harvest delays in Brazil, and potential El Niño-related disruptions in other origins are providing some support to prices.

- Cocoa: Cocoa prices remained volatile throughout the quarter. Concerns over potential El Niño impacts on both the volume and quality of the upcoming 26/27 crop have supported higher prices. However, improving certified stocks and strong port arrivals in Ivory Coast may limit sustained upward momentum.

Softs Price Index (Jan26 = 100)

Source: LSEG

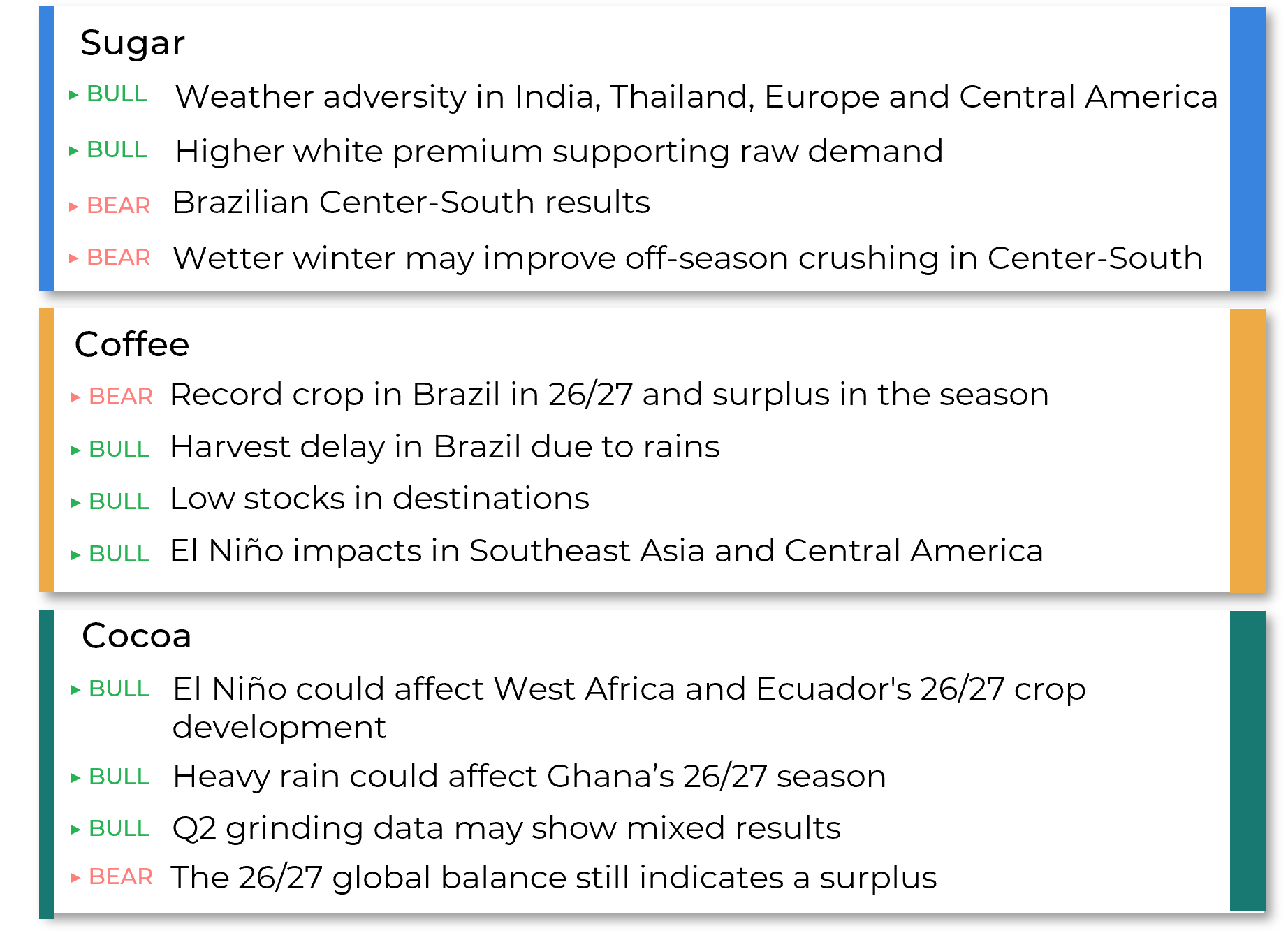

Key Factors Going Forward

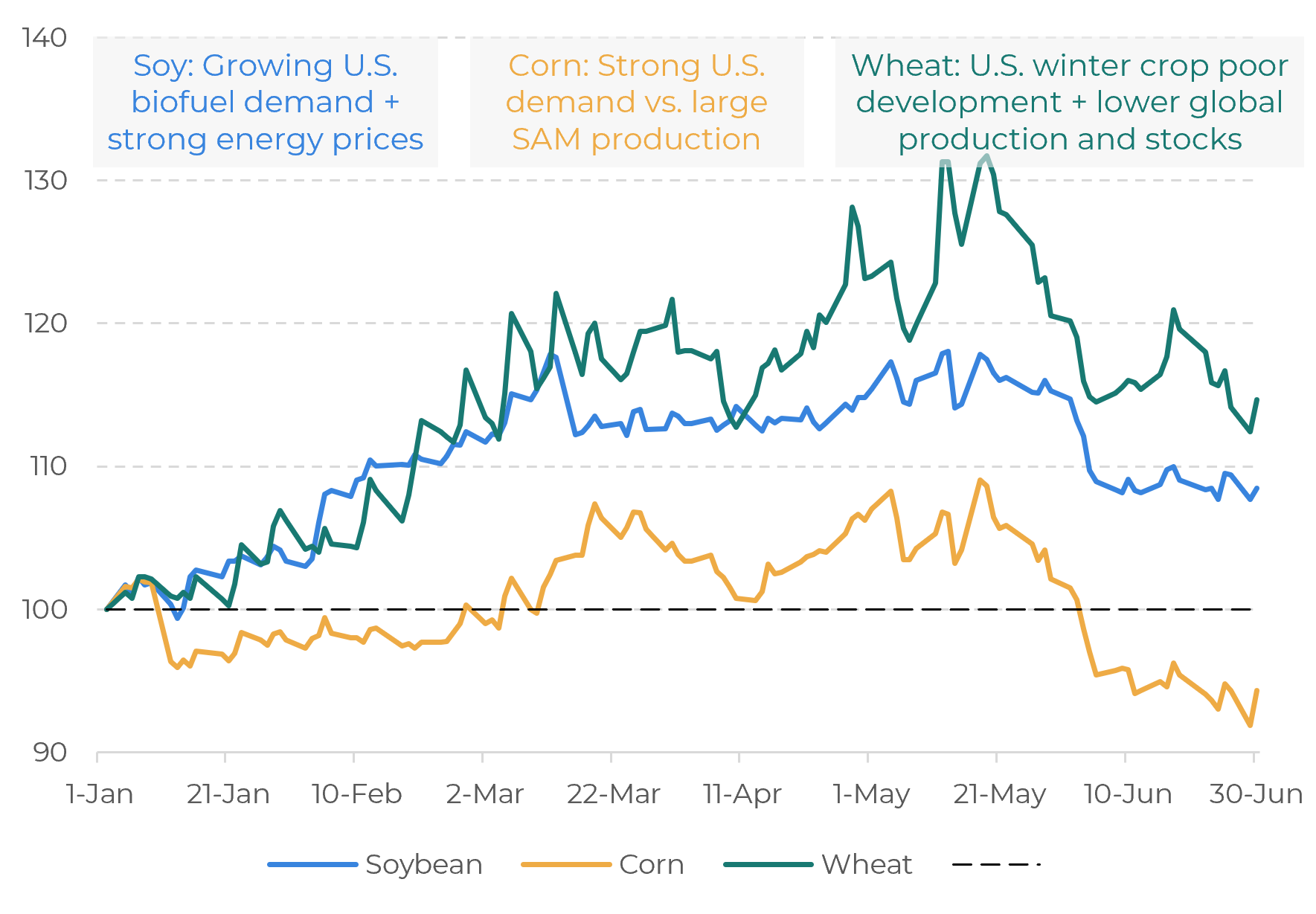

Grains & Oilseeds Outlook

Soybean: Higher biodiesel blending mandates in the U.S. provided fundamental support to prices. In addition, the conflict between the U.S. and Iran kept oil prices elevated, further boosting soybean oil prices.

Corn: Strong demand for U.S. corn remained a supportive factor. However, large crops in South America continued to weigh on the market from the supply side.

Wheat: Poor development of the U.S. winter wheat crop supported prices, which also benefited from expectations of declining global production and lower stocks in the 26/27 season.

Grains Price Index (Jan26 = 100)

Source: LSEG

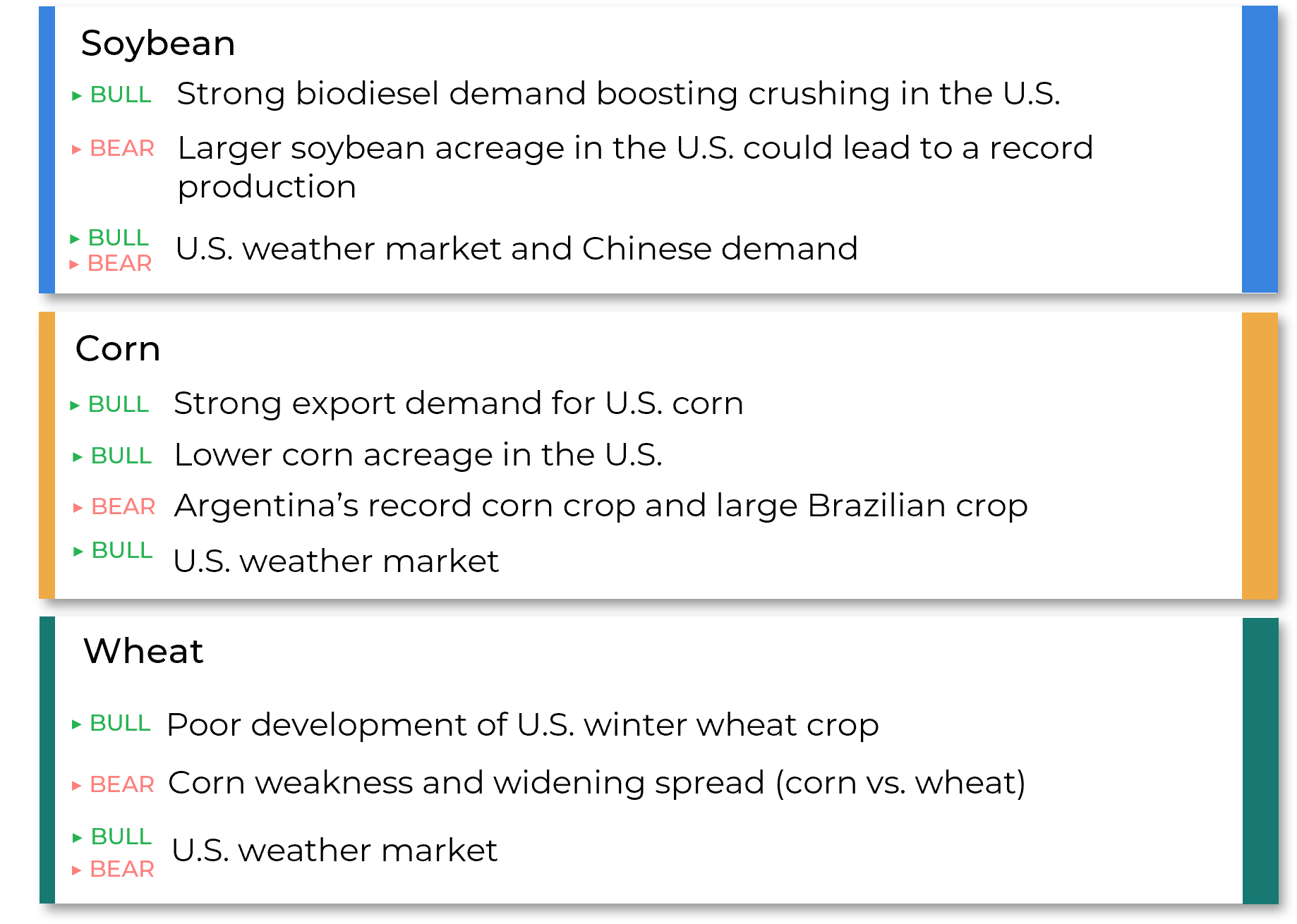

Key Factors Going Forward

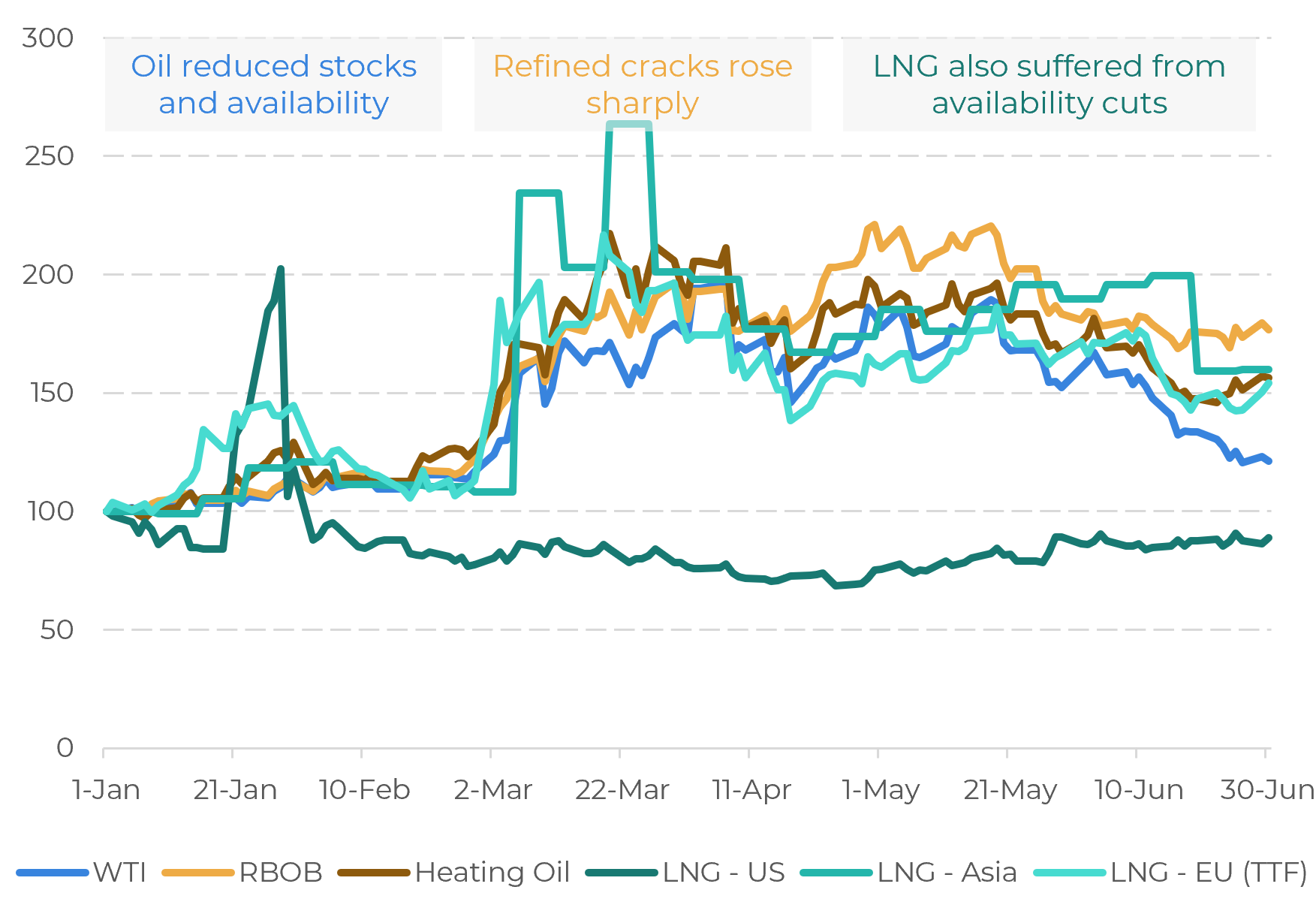

Energy Outlook

- US-Iran conflict removed significant fuel volumes from the market, triggering price volatility as inventories declined and concerns over freight rates and supply security intensified across crude oil, refined products, and LNG.

- OECD and commercial oil inventories declined sharply during Q2, highlighting reduced buffers against potential future supply shocks.

- Tight product availability and refinery disruptions pushed gasoline and distillate crack spreads to exceptionally strong levels throughout Q2.

Energy Price Index (Jan26 = 100)

Source: LSEG

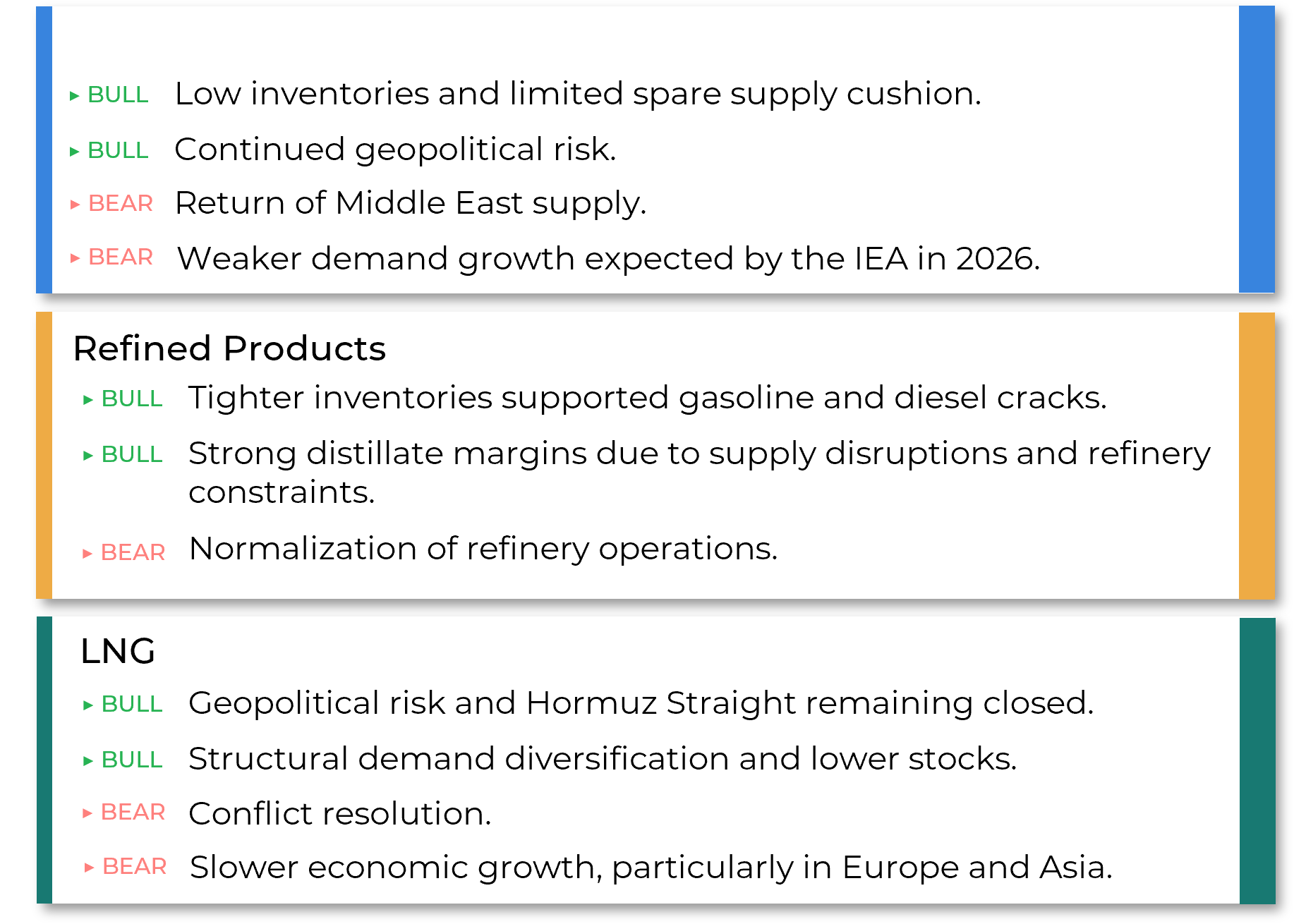

Key Factors Going Forward

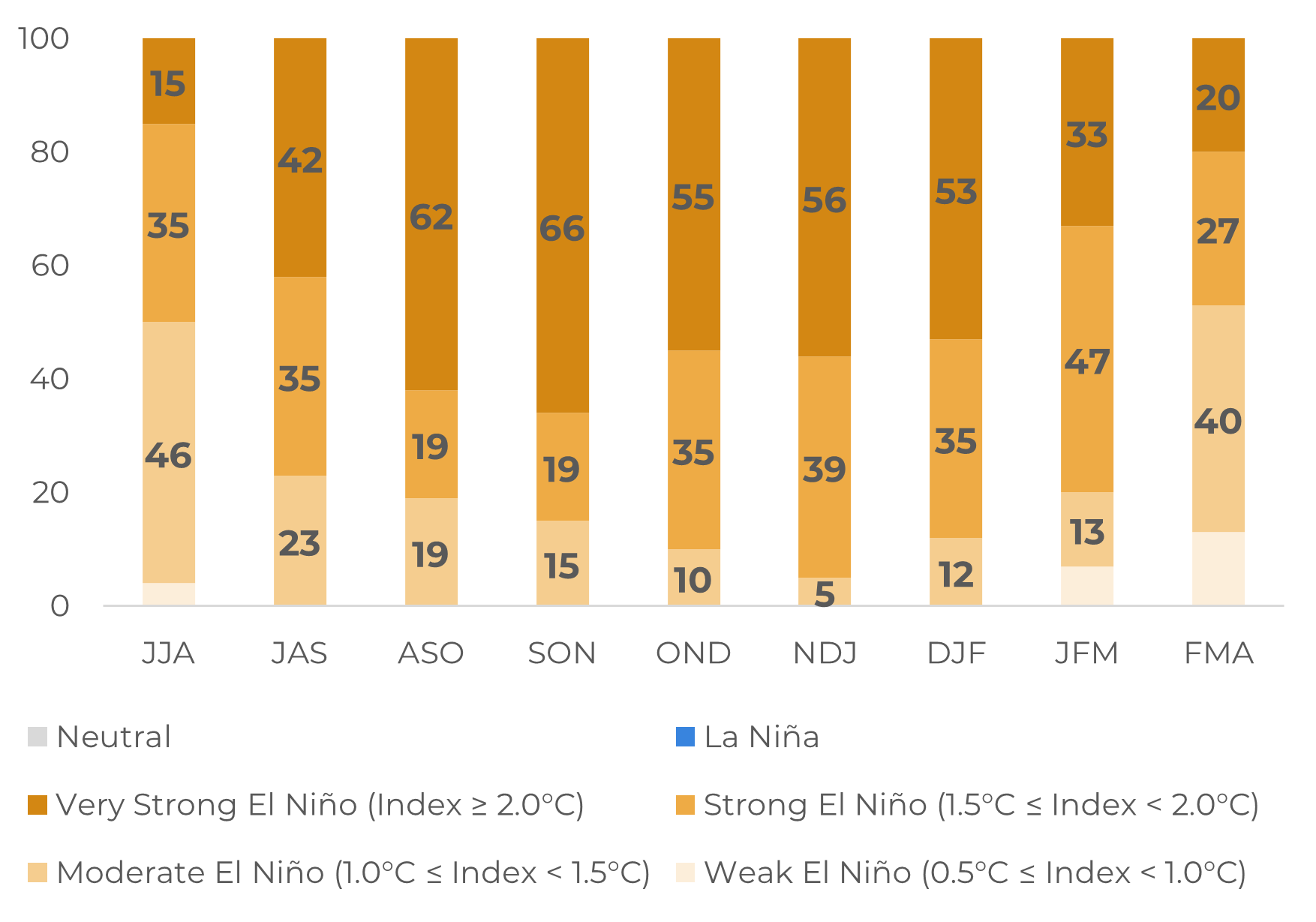

El Niño: a point of concern

NOAA

and IRI models estimates a 97% and 98% probability, respectively, of the

phenomenon occurring between May and July. The likelihood of it persisting

through the second half of 2026 and into early 2027 is virtually certain,

increasing climate-related risks for agricultural commodities.

In addition, the phenomenon is expected to strengthen, with more than 66% probability of reaching very strong intensity between September and November 2026.

CCSR/IRI ENSO Strength Categories (%, June, 2026)

Source: LSEG

El Niño effects in crops

Source: Hedgepoint

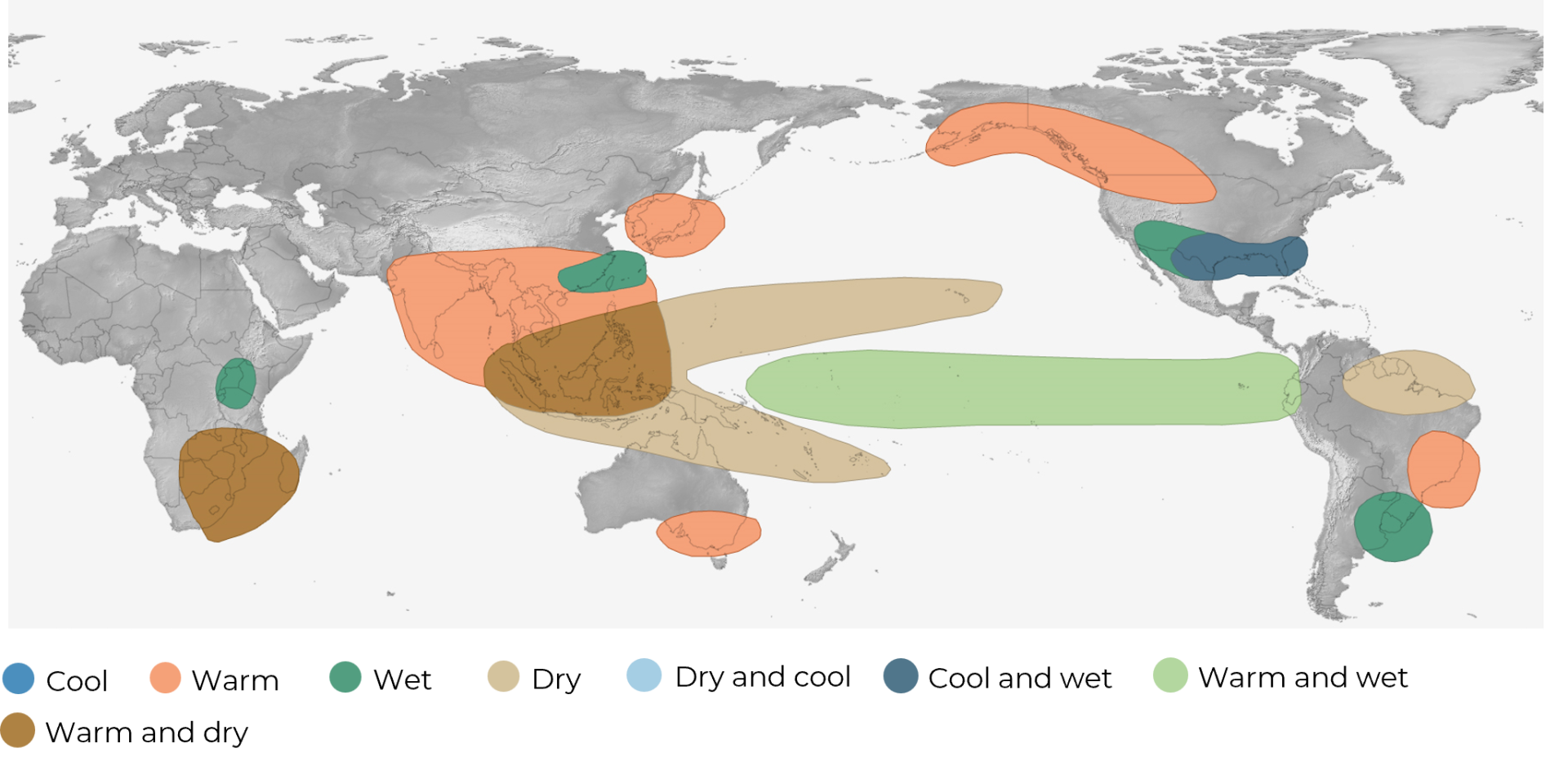

Higher temperatures and uneven rainfall

El Niño could alter monsoon patterns, bringing hotter and drier conditions to Australia, Southeast Asia, and parts of Central America.

Additionally,

it could intensify rainfall in South America and Africa, increasing the risk of

flooding, while also supporting a more active storm track across the southern

United States during the winter.

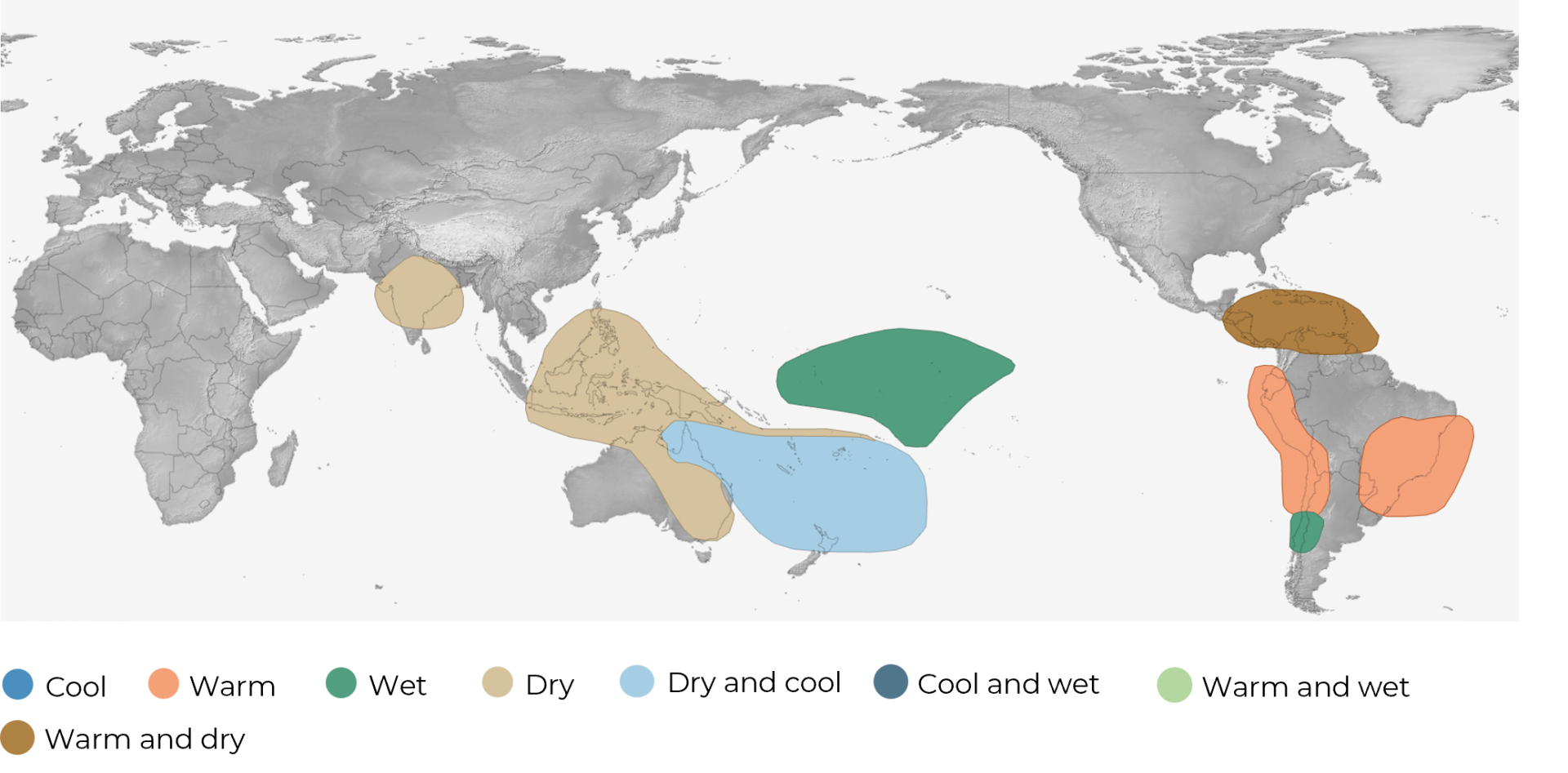

El Niño: Possible Weather Impacts (June-August)

Source: NOAA

El Niño: Possible Weather Impacts (December-February)

Source: NOAA

Special Report — Multicommodities

livea.coda@hedgepointglobal.com

luiz.roque@hedgepointglobal.com

thais.italiani@hedgepointglobal.com