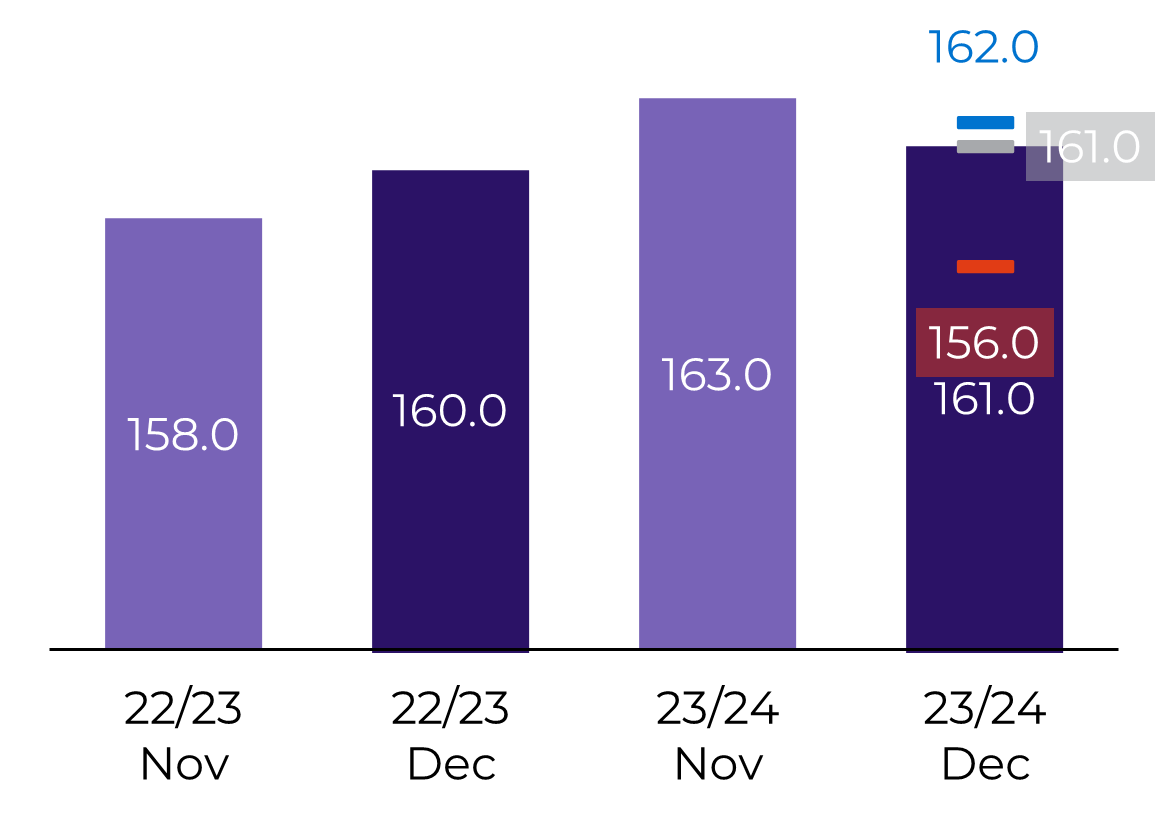

On soybeans, all eyes were on the Brazilian production. The market was pricing a cut, but whether it was coming or not was dubious – the USDA had not adjusted the country’s production in December in the last 10 years.

The cut to production came in line with the estimates (-2M ton), which left Brazil’s ending stocks smaller by the same amount – adjustments to the carry-in and exports offset each other. In our view, the size of the adjustment makes sense, but it just came as a surprise that USDA broke its previous “modus operandi”.

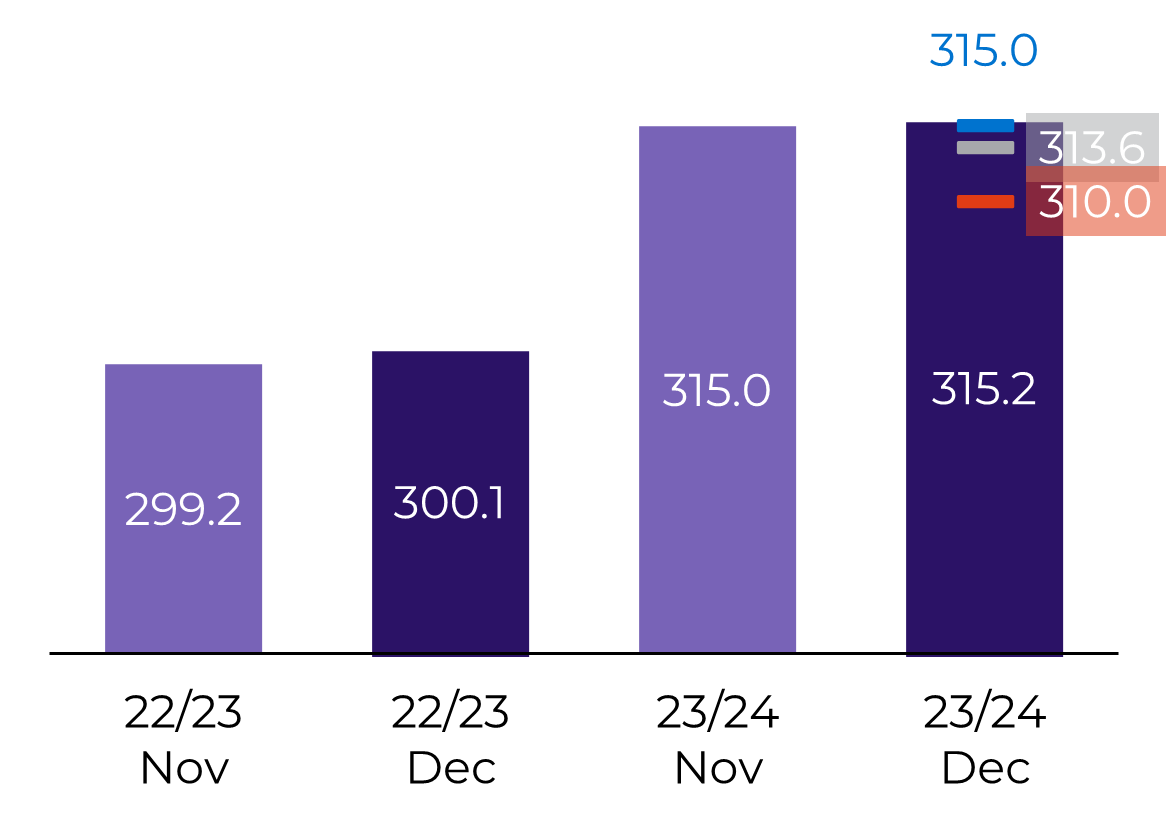

As a result, world stocks were expected to decline. However, increased stocks in China, pushed by bigger imports, kept them unchanged.