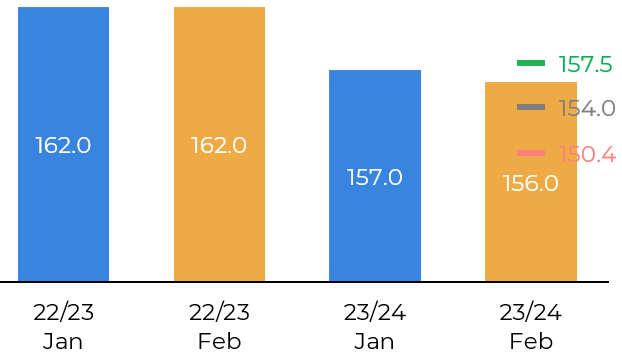

The USDA, as usual, didn't make many changes to its US Supply and Demand estimate for February. Only exports were reduced due to two factors: the concerns over slow pace of shipments at US ports in January and the competition with Brazil.

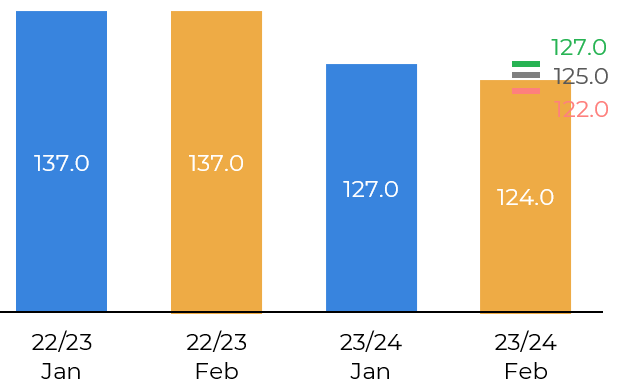

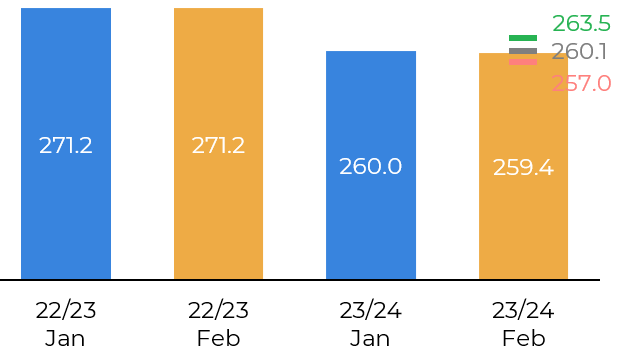

Speaking of Brazil, the cut in the soybean production estimate happened as expected, but to a lesser extent. While agents on average pointed to a cut of 3M mt, the USDA was more conservative and reduced it by just 1M mt to 156M mt.

This movement, combined with Conab's update today, has increased the difference between the two readings. While the USDA expects the Brazilian crop to reach 156M mt, Conab is already working below 150M mt, with an estimate of 149.4M mt, a difference of 6.6M mt.